5 min read

How to Benchmark Multi-Asset Funds

In some markets, multi-asset strategies lack benchmarks altogether, leaving investors in the dark. Here's how to compare multi-asset funds.

After the global financial crisis of 2008, investor capital flooded into funds that combine stocks, bonds, and other asset classes. According to Morningstar data, assets in multi-asset mutual funds and ETFs reached $4 trillion in 2024, up from roughly $1 trillion in 2008.

While they go by different names and come in varying shapes and sizes, these multi-asset funds share built-in asset allocation and often target an objective. As they say at industry conferences, today’s investors prefer “solutions over products.”

While multi-asset strategies have many positives, they present a real challenge when it comes to benchmarking. Defining the investable universe in a way that facilitates measurement is a difficult task.

Multi-asset investment managers respond with a wide range of solutions. The result is a muddle for investors.

What Are Multi-Asset Funds?

Multi-asset funds contain a range of asset classes—such as equities, bonds, and cash—in one portfolio. Because of their diversification, multi-asset funds can help investors manage risk.

The landscape for multi-asset funds is diverse. Their roots can be traced to traditional balanced funds, including the classic 60/40 split between stocks and bonds, as well as institutional investors’ “policy portfolios.” Their growth has been paralleled by the burgeoning model portfolio market in the United States.

Implementation of multi-asset strategies can vary, from baskets of securities to a fund-of-funds approach. Some use a strategic asset allocation while others are tactical or dynamic. Asset class building blocks can be passive or active, closed architecture, or unfettered.

Multi-asset funds are often described as a “one-stop-shop.” Their diversified nature allows investors to outsource portfolio assembly, which became more appealing after the global financial crisis of 2008.

Target-date or target-maturity funds, which have become default options in many retirement plans, are a true “set it and forget it” solution. Higher-education-focused investments also have an built-in lifecycle.

But many other multi-asset strategies that don’t follow glide paths have also proliferated. Some are referred to by mixing and matching descriptors like “objectives,” “goals, or “outcomes,” to “based,” “oriented,” or “focused.”

Within this framework, Morningstar researchers have created such groupings as multi-asset income, multi-asset inflation protection, and target risk.

Multi-asset funds with relatively static asset mixes fall into Morningstar categories defined by their equity allocations—30-50%, for example. Category naming conventions vary by geography, some using adjectives such as “Cautious” and “Adventurous.”

Morningstar data shows that multi-asset funds generally deliver a good investor experience. According to Morningstar research, allocation funds produced the best money-weighted returns of all US fund types, with a positive gap of 40 basis points. European allocation funds are used similarly well.

This is partly because allocation funds limit volatility, so investors are less tempted by dramatic performance swings to mistime purchases and sales. It also owes to the fact that allocation funds are often used as core long-term holdings.

How Do You Benchmark Multi-Asset Funds?

Benchmarking a multi-asset strategy differs substantively from a managed strategy focused on a single-asset class. A traditional index reflects the opportunity set for an investment strategy.

The benchmark named in a prospectus or investment policy statement sets direction and serves as a gauge of value-added (or subtracted). Benchmarking is also critical to understanding risk and return drivers and measuring portfolio characteristics.

The many dimensions of a multi-asset strategy complicate analysis.

First, there’s the allocation between stocks, bonds, and other asset classes. Then, there are the kinds of stocks (size, style, geography) and bonds (sector, duration, credit quality, geography). If the strategy uses actively managed underlying funds as opposed to index funds, there’s an additional layer of security selection within each sleeve. And for objectives-oriented funds, there’s the outcome to consider.

Multi-asset funds address the benchmarking dilemma in a variety of ways. In some markets, they lack benchmarks altogether, leaving investors in the dark.

Others use peer group averages, which are not investable, can reflect heterogeneous groupings, and flatter a fund that is the best of a bad bunch.

Still, others use a single asset class benchmark or measure themselves against somewhat arbitrary and non-investable measures, such as inflation plus 4%, or easy-to-beat benchmarks, such as cash rates.

Custom benchmarks are also common. When managers exercise discretion in assembling their own benchmark, it raises questions of independence and appropriateness.

Stitching together indexes from a range of providers may create inconsistencies when each provider follows a different methodology. It may also introduce licensing issues for asset managers.

Maintaining blended benchmarks can also be technically challenging, especially in volatile market conditions or when the fund changes its strategic asset allocation. Complexity is another challenge, as is consistency across strategies. As regulators take an increased interest in benchmarking, multi-asset strategies could come under scrutiny.

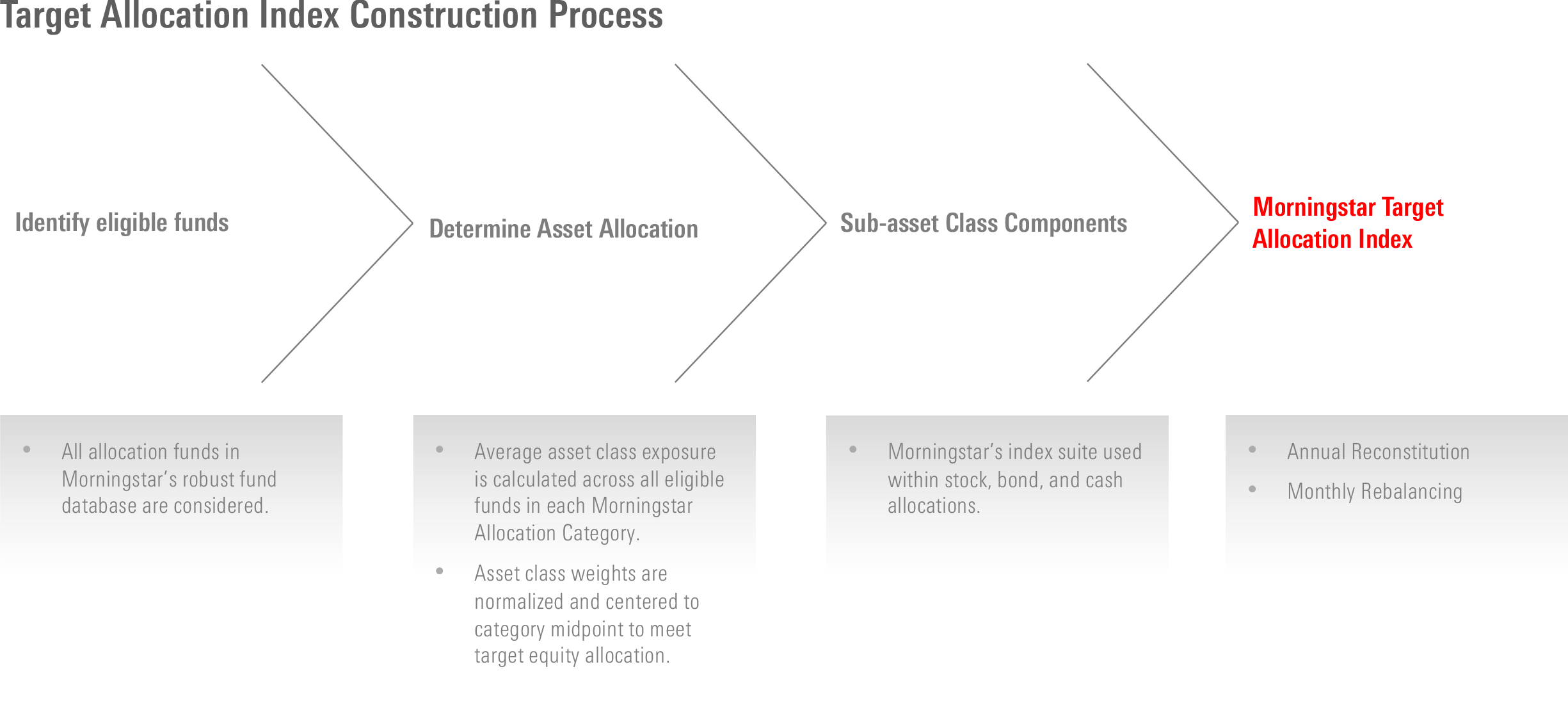

Benchmarking Multi-Asset Funds Through the Morningstar Target Allocation Index Family

Morningstar Multi Asset Indexes provide investors with tools to benchmark the performance of multi-asset funds across risk tolerances. Aligned with the Morningstar categories for funds, the indexes are the first allocation benchmarks to follow a consistent construction approach across regions.

They take a data-driven approach to reflecting home bias, currency exposure, and local asset class preferences in eight regions:

- United States

- Canada

- Europe

- United Kingdom

- Japan

- Australia

- New Zealand

- Europe, Asia, South Africa (EAA USD funds)

Although they may not capture every strategy’s specific objective, such as income, they are useful as a broad measuring stick.

The indexes take their asset allocation cues from Morningstar’s multi-asset fund categories. The indexes set equity allocations to the category midpoint. Leveraging Morningstar’s survivorship-bias-free database of investment portfolio holdings, category averages drive index weights within the stock, bond, and cash sleeves.

This aligns the indexes with the actual investment behavior of multi-asset managers. Short-term fluctuations in the asset mix are smoothed out by using a three-year look-back period. Meanwhile, Morningstar’s range of single-asset indexes fills the sleeves.

These building blocks are pure and non-overlapping—the most commonly used exposures by professional asset allocators. The methodology is transparent and the resulting benchmarks replicable.

Benchmarking allocation strategies is critical, and the current tools available to investors are inadequate.

As multi-asset funds gain traction across the globe, multi-asset indexing needs to evolve. Morningstar’s Target Allocation Index Family aims to empower multi-asset investor success by providing a clear, convenient, and consistent measuring stick.

Learn more about our multi-asset indexes.