Measuring Client Risk Tolerance: How Better Methodology Can Give Advisors an Edge

Advisors who can clearly demonstrate how they understand and manage client risk are better positioned to build trust, retain clients, and stand out in a crowded market.

Across global markets, regulators are raising the bar for advisor accountability. From Regulation Best Interest in the U.S. to Client Focused Reforms in Canada and the UK’s Consumer Duty, advisors are being asked to prove that their recommendations truly reflect clients’ best interests.

Market volatility only adds to the pressure, increasing the odds of many investors making emotional, counterproductive decisions.Against this backdrop, Morningstar is rethinking what it means to deliver personalized, suitable, and scalable advice. Can new processes provide a strong competitive advantage that meets or exceeds regulatory requirements and, more importantly, leads to better investor outcomes?

Why Does Risk Matter for Advisors?

For advisors, the stewardship of people’s money already comes with heavy responsibility and increasing compliance costs. At the same time, product-related fees are declining and client expectations are increasing. Advisors are increasingly in demand of ways to demonstrate value and differentiate themselves if they want to retain clients for the long run.

The good news is that interest in investing is strong, and advisors are reaping some of the benefits. Stock ownership in the US is at a high of 62%,1 and younger investors are starting earlier: 37% of 25-year-olds are entering the market in 2025 compared with 6% in 2015.2 Lower entry barriers—from technological accessibility and increasing awareness of the benefits of starting early—are driving the trend.

Many individuals are seeking help because times are uncertain. Geopolitical tensions, economic uncertainty, and recent private credit turmoil in the US have led to rapid price swings in various sectors. While uncertainty has led some to seek advice, others choose a do-it-yourself approach. Many of these younger investors, who are often not targeted by advisors, found themselves with growing investment accounts and no significant experience to temper their feelings of invincibility. Advised investors, too, are dabbling in DIY, with 74% managing a portion of their own money.3

What Happens When Risk Is Misjudged?

During the 2008 financial crisis, many investors sharply reduced equity exposure after markets fell, often locking in losses and missing the recovery that began in March 2009. Research shows this behavior couldn’t be explained by market movements alone, suggesting a deeper mismatch between investors’ true risk tolerance and the portfolios they held.4

Several factors may have led to this costly behavior: Clients may not have had access to good advice; the assessments of clients’ risk tolerance may have been overestimated; or the risk levels of the portfolios may have been too high. Regardless of the cause, the effect was a significant loss of hundreds of billions of dollars by retail investors.

Advisors feel the impact as well. On average, 20% of clients leave their advisor within the first year.5 When asked why, the three top reasons were:

- Lack of good service and personal communications

- Lack of understanding about the client’s overall financial goals

- Poor understanding of the client’s risk tolerance

The bottom line: Getting risk wrong can result in direct losses for retail investors as well as lost clients and legal and regulatory complaints for advisors.

Why Do Traditional Risk Tools Fall Short?

Most risk assessment systems used in financial services today still rely on processes developed decades ago.

The typical process follows these steps:

- Define a series of five or six risk bands—for example: 1=Very Conservative, 2=Conservative, 3=Balanced, 4=Aggressive, and 5=Very Aggressive.

- Create a questionnaire that asks questions recommended by the regulator or commonly used in the industry, then create a scoring model to assign investors into one of the risk bands.

- Assign risk levels to the product shelf. Usually, cash and money market funds go into Band 1, fixed income into Band 2, balanced funds into Band 3, developed-market equities into Band 4, and other equities (country-specific, sector-specific, and so on) into Band 5.

- Since investment products can come in many flavors, some firms may use a rolling standard deviation as a measure of the product’s risk and the risk band it belongs in, allowing advisors to demonstrate the value of diversification for aggregate portfolios (that is, by combining products from different risk bands.)

- The suitability process then matches the investor’s assigned risk band to the product risk band (that is, Balanced investors are matched to Balanced products or portfolios).

While administratively simple, this approach has real drawbacks. Labeling a client as “balanced” alongside millions of others is far from personalized, and product risk classifications can shift dramatically during volatile markets.

For example, during periods of growth and stability, typical balanced funds or portfolios might be categorized as moderate risk. Those same investments may suddenly be deemed aggressive during volatile times because their standard deviations have shifted dramatically. In such a scenario, advisors might be obliged to move clients out of the now “aggressive” investments to a lower risk band, crystallizing losses and setting them up to miss out on the inevitable recovery.

It’s no surprise that many advisors view risk-tolerance questionnaires as a compliance checkbox rather than a meaningful planning tool. Better a blunt instrument than no instrument at all, but in a world where investors can see personalized and targeted ads in their browser moments after any search, why should they expect to be treated like another cog in the wheels of the advisors managing their accumulated wealth?

The next generation of investors is younger, comfortable with technology, and views consumption as an expression of individual identity.6 As a result, this cohort expects advisors to work with them to tailor their financial plans to meet their needs, circumstances, and personality.

What Makes a Better Risk Assessment?

Risk tolerance reflects people’s emotional comfort with uncertainty, and it can be hard for individuals to express their feelings about uncertainty on a scale. That makes it difficult to measure.

Not all risk tools are created equal. The two most common methods are:

- Stated preferences questionnaires, which ask people to self-report behaviors and attitudes. For example: “How do you respond when things go wrong financially?”

- Revealed preferences exercises, which present hypothetical choices or gambles. For example: “Would you prefer a guaranteed payoff of X, or a 50/50 chance of gaining Y (nothing otherwise)?”

Both can be useful, but they have limitations as well. While they can produce profiles for specific situations, that isn’t enough when it comes to measuring people’s risk preferences for investing.

Morningstar’s 2025 Voice of the Advisor survey7 shows that advisors want tools that are:

- Easy to understand

- Useful for client conversations

- Supportive of relationship-building, not just scoring

How Should Advisors Evaluate Risk Tools?

Morningstar uses three guiding questions:

Is it effective?

A strong risk tool must be scientifically sound—valid (measuring what it claims to measure) and reliable (producing consistent results over time).

Is it engaging?

Risk discussions are emotional. The right tool should help clients articulate their comfort with gains and losses in real-world terms, not abstract gambling scenarios.

Is it efficient?

Risk profiling should integrate smoothly into the advice workflow, supporting documentation, monitoring, and compliance without adding friction.

Can Risk Tolerance Be Measured Reliably?

Through psychometrics, we can determine if a risk measure is effective. Namely, it must be both valid—measures what it purports to measure—and reliable—measures consistently over time with known accuracy. Well-designed psychometric stated preferences questionnaires have been shown to give greater insight into actual risk-taking behavior in the real world and greater test-retest stability compared with gambles-based exercises.8

Repeated testing (test-retest), where people take the same questionnaire multiple times, years apart, can indicate whether the measure is reliable.

Exhibit 1 shows the risk-tolerance results of about four thousand individuals who have taken the Morningstar stated preferences RTQ on two different occasions. People’s scores are usually within one standard deviation (+/-10) of their prior score.

So, someone with a relatively low risk tolerance might score a 20 the first time and a 23 the next. Someone with a higher risk tolerance might score around 60 first, then 55 next. Generally, there are relatively small changes.

Source: Morningstar.

The upshot? People’s risk tolerance is relatively stable—including before, during, and after the 2008 global financial crisis and the 2020 pandemic period—debunking the common belief that a client’s risk tolerance changes as markets rise and fall.

However, while robust risk measures are available, most advisors do not use any form of validated tool. Home-grown risk measures are commonplace, often combining multiple risk factors into a single scoring algorithm, leading to erratic results, which likely explains why advisors mistrust such questionnaires to begin with.

How Better Risk Conversations Build Trust

Effective risk tools do more than assign a score. They create a shared language for discussing uncertainty, expectations, and long-term behavior. By grounding conversations in realistic scenarios, advisors can help clients understand what volatility feels like—not just what it looks like on a chart.

Revealed preference exercises, on the other hand, can feel more like abstract games or, worse yet, time at a casino. Abstract numerical questions with gambling terminology may disconnect people from the natural emotions around investing and be a disservice for people unaccustomed to, or uncomfortable with, thinking in bets. Ultimately, risk-tolerance measures should help people find their emotional comfort, balancing the thrill of gains with the anxiety of losses. Questionnaires that explore a range of past and present scenarios are more likely to capture this balance accurately and assist in making trade-offs, adding value to the advisory relationship.

Moving Beyond One-Size-Fits-All Risk Buckets

Portfolio risk is often explained using short-term volatility metrics that can confuse investors and promote poor timing decisions. A more durable approach connects client risk tolerance to portfolios designed for long-term behavior.

Morningstar’s risk framework links validated risk profiles to portfolio risk. It uses a set of well-diversified Target Allocation Indexes to define what it means to be “Conservative,” “Moderate,” or “Aggressive,” and our Portfolio Risk Score visuals depict the range of potential risk for each type of portfolio.

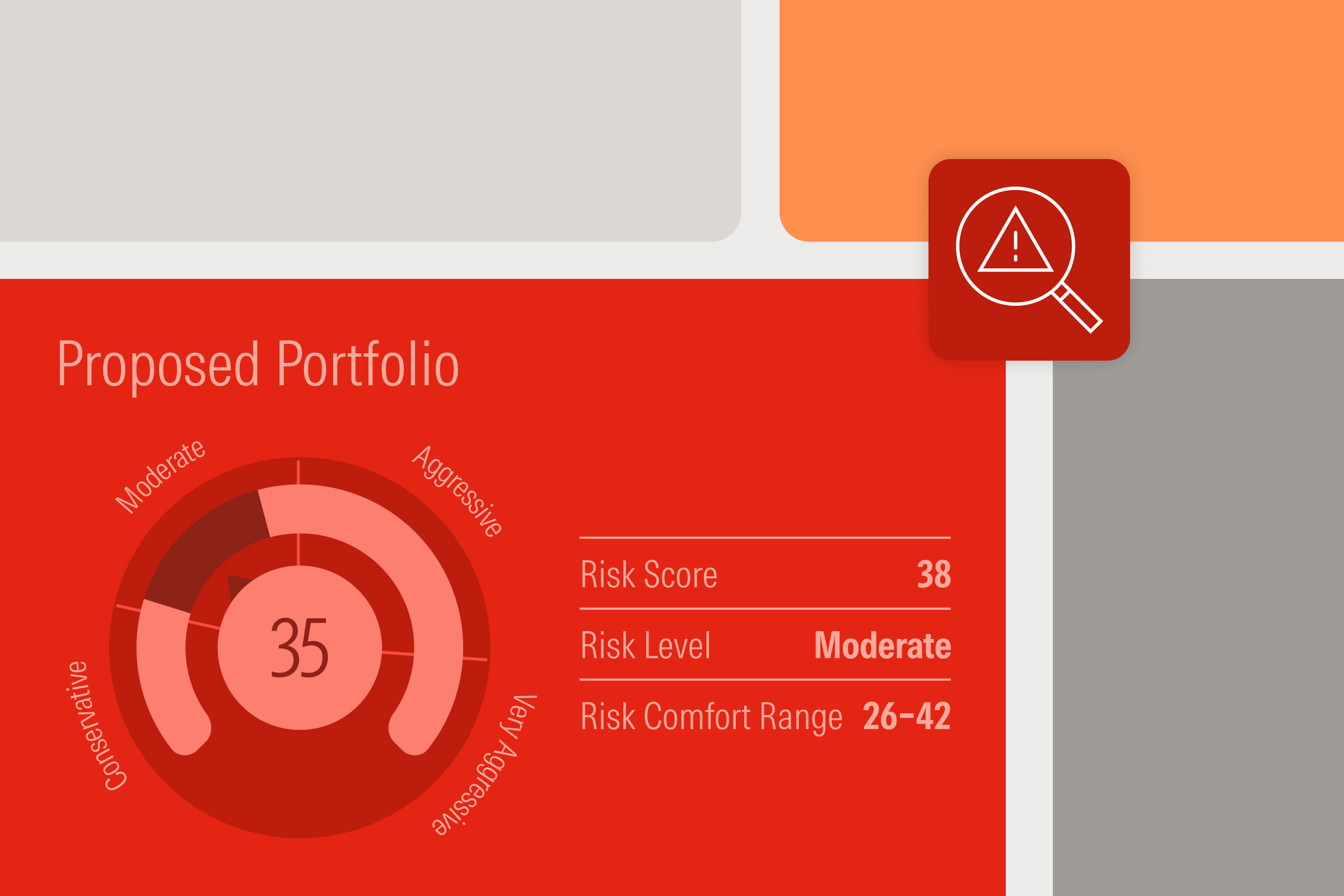

Exhibit 2 illustrates a risk of a hypothetical portfolio (53) against the client’s risk comfort range (43 to 56), derived from Morningstar’s RTQ and empirically tested risk mapping methodology.9

Source: Morningstar.

Not only is this more engaging for the investor, but it also allows a more appropriate determination of the products on an advisor’s shelf and how they fit for that investor. For instance, if a client’s risk comfort range crosses the frontier from one traditional bucket to another, the advisor can craft a portfolio that sits between the two traditional profiles, rather than force-fitting the client into one or the other.

Risk Done Right Is a Competitive Advantage

Clients don’t hire advisors for performance alone. Morningstar research10 shows that an equal number of clients choose their advisors for emotional reasons like trust and communication.

By adopting a proven, defensible approach to measuring risk tolerance, advisors can improve client understanding and confidence, strengthen regulatory defensibility, and build deeper, longer-lasting relationships.

1 Gallup U.S. Stock Ownership, Annual Trends 2025

2 JPMorgan Chase Institute: A decade in the market: How retail investing behavior has shifted since 2015

3 YCharts Client Communication Survey 2024

4 Browning, C., Finke, M. 2015. “Cognitive ability and the stock reallocations of retirees during the Great Recession.” Journal of Consumer Affairs, Vol. 49, No. 2, P. 356.

5 E*Trade Advisor Services. 2019. “Client Retention: Why Clients Leave and Five Ways to Encourage Them to Stay.”

7 https://www.morningstar.com/business/insights/research/voice-of-the-advisor

8 Grable, J.E., Hubble, A., Kruger, M., & Visbal, M. 2020.” Predicting financial risk tolerance and risk-taking behaviour: A comparison of questionnaires and tests.” Financial Planning Research Journal, Vol. 6, No. 1, P. 21.

9 Davey, G. 2015. “Getting risk right.” Investment Management Consultant Association Inc., March-April, 33-39.

10 Morningstar. 2023. “Why Do People Hire Their Financial Advisors?”