Our analysts take a closer look at the Morningstar Model Portfolios universe.

By Jason Kephart and Gabrielle DiBenedetto

Portfolio Construction

By Jason Kephart and Gabrielle DiBenedetto

Read Time: 4.5 Minutes

One of the main benefits of model portfolios is that they’ve enabled financial advisors to free up their time to focus on other responsibilities. These may include deepening the client relationship to cover priorities other than portfolio returns—such as planning for college savings or a wealth transfer—or paying attention to growing their business.

But an additional benefit is that most model portfolios offer significantly lower costs than similarly allocated mutual funds. Model portfolios are one of the cheapest ways for investors to buy a professionally managed, diversified portfolio.

We took a closer look at the portfolios in Morningstar Model Marketplace and Model Portfolio database in Morningstar Direct℠ to evaluate the state of the model portfolios market. Below, explore some of our findings.

Model portfolios’ biggest differentiator may be just how cheap they can be.

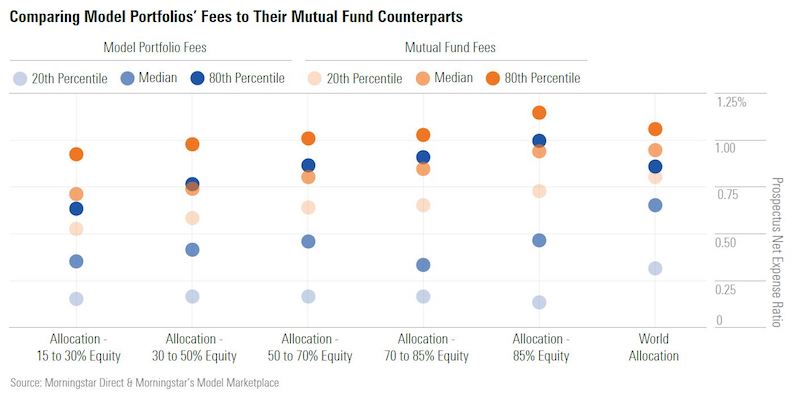

To quantify their cost advantage, we calculated the asset-weighted expense ratio of the underlying funds for strategies in Morningstar’s model portfolio database and on the Morningstar Model Marketplace.

After excluding asset managers that have not reported a portfolio in 2019 and any portfolios that had more than 10% of assets allocated to assets without an associated expense ratio, we were able to calculate the asset-weighted fee for approximately 640 portfolios, or about 80% of the model portfolio universe in Morningstar Direct. We then compared the 20th-percentile, median, and 80th-percentile fees for model portfolios with mutual funds by their allocation category.

As shown on the chart below, the median fee for a model portfolio is cheaper than even the 20th percentile of fees for a similarly allocated mutual fund in every allocation category. And in every category, each level of model portfolio fee—20th percentile, median, and 80th percentile—was significantly cheaper than its mutual fund counterpart.

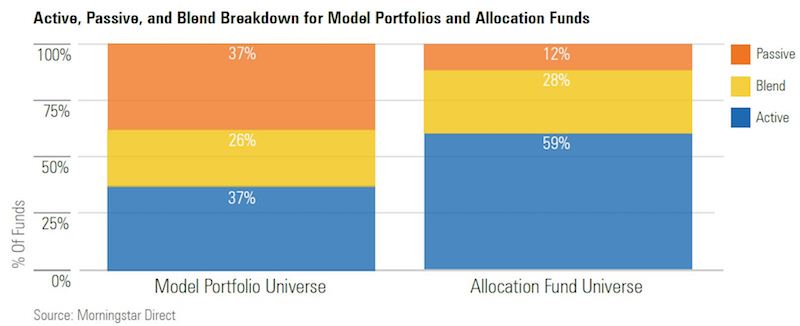

While the cheapest model portfolios tend to be 100% passive, there are plenty of options that blend active and passive together or rely solely on active funds.

For our evaluation of the spread among these models, we defined passive and active portfolios as having at least 80% of underlying assets in passive or active funds, respectively; and a blend of active and passive as those that had less than 80% in one or the other.

The chart below shows the breakdown of model portfolios across passive, blend, and active options. Active and passive models make up similar shares of the universe, with each constituting 37%; blended models aren’t far behind at 26%.

The chart also shows how the allocation fund category breaks down. This category has substantially more active options and substantially fewer passive options, though the percentage of blend options is similar.

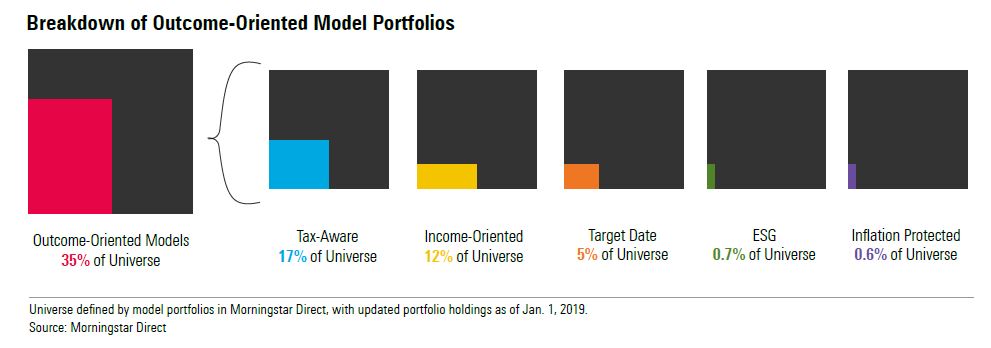

Although outcome-oriented strategies garner a lot of talk, they still constitute only a minority of our Morningstar model portfolio universe. This sector is defined as including models that are tax aware, income-oriented, target date, inflation-protected, or ESG-focused.

The graph below shows that altogether, this group constitutes 35% of the model portfolios universe.

Here’s a look at a few subcategories within the outcome-oriented strategies group.

Tax-aware models, which aim to manage investor tax liability, make up the largest subcategory of outcome-oriented strategies at 17% of the universe.

Most of these models are from asset managers—Russell Investments was an early mover here, and BlackRock, Vanguard, and PIMCO all launched their own models in 2018—although a small portion are third-party managed. These include active and passive, municipal bond, large-cap world stock, and equity and fixed-income allocation.

Target-date models, which build portfolios that span a predetermined time period, constitute 5% of the model portfolio universe. Since all share classes or retirement dates are treated equally, this subcategory includes only three series: Northern Trust Goal Engineer, Wilshire Total Allocation, and Wilshire Global Allocation.

ESG-focused models, which factor sustainability into investment decisions, make up the smallest portion of the universe at 0.7%. BlackRock is the only asset manager with an ESG-focused offering: the BlackRock Target Allocation ESG Series. The firm offers equity-only, 80/20, 60/40, and 40/60 models, which hold an assortment of iShares ESG ETFs in different asset classes, like iShares ESG MSCI Emerging Markets ETF (ESGE) and iShares ESG USD Corporate Bond ETF (SUSC).

While BlackRock is the sole asset manager in this space, multiple third parties have comparable offerings, such as Loring Ward and Litman Gregory, the latter of which just launched a series this year.

A few models cross multiple subcategories. For example, third-party CMC offers the CMC Income Tax-Advantaged portfolio and CMC Income Tax-Advantaged ETF portfolio, which are classified as both income-oriented and tax-aware—meaning they can serve as an investor’s income and are designed to manage tax liability.

Model portfolios are a promising way for financial advisors to spend more time focusing on client relationships and running their businesses, while outsourcing asset allocation and fund selection to third parties and asset-management firms.

A large portion of the Morningstar model portfolios we analyzed have launched within the last 18 months, indicating that as more advisors adapt, more firms will likely join in on the trend and create more offerings. As with any other investment vehicle, advisors who are interested in these models should remain mindful of the whole picture, including fees, strategy focuses, and risk tolerance.

For advisors who want to learn more about asset allocation and the model portfolio universe, try Morningstar Direct.

Disclosure

The information, data, analyses and opinions presented herein do not constitute investment advice; are provided solely for informational purposes and therefore are not an offer to buy or sell a security; and are not warranted to be correct, complete or accurate.

The opinions expressed are as of the date written and are subject to change without notice. Except as otherwise required by law, Morningstar shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information contained herein is the proprietary property of Morningstar and may not be reproduced, in whole or in part, or used in any manner, without the prior written consent of Morningstar.

Investment research is produced and issued by Morningstar, Inc. or subsidiaries of Morningstar, Inc. including, but not limited to, Morningstar Research Services LLC, registered with and governed by the U.S. Securities and Exchange Commission.