5 min read

How Does Investment Risk Tolerance Affect Portfolios?

Delivering personalized investment strategies can encourage successful, long-term client relationships.

Key Takeaways

Risk tolerance is a person’s willingness to take risks in exchange for the long-term possibility of reward—this trait remains consistent regardless of market wins or losses.

Creating risk profiles and considering risk composure can help advisors deliver holistic portfolios that fit a client’s real risk preferences.

Morningstar Direct Advisory Suite is built to connect risk, goals, and portfolio alignment within a single workflow.

As an advisor, your job is to not only help clients reach their goals—but feel comfortable in their investment decisions. Yet that idea of reassurance doesn’t look the same for all investors: While some love the thrill of watching their investments spike and tumble, others might cautiously guard their nest egg against any market whims.

So how accurately can you predict a client’s reaction to future downturns?

Our data shows that risk tolerance, a person’s willingness to take risks in exchange for the long-term possibility of reward, is a stable personality trait that allows advisors to engage with clients more confidently and create better-aligned portfolios. With a validated, psychometric approach to measuring risk tolerance, advisors can help clients stay the course during severe market volatility—creating clarity and trust when it matters most.

Here’s what advisors need to know.

Risk Tolerance Doesn’t Change With the Stock Market

While markets may fluctuate, research shows that risk tolerance is consistent despite those wins or losses. In fact, we found that global risk tolerance scores have remained meaningfully the same during volatile markets of the last 20 years.

Risk Profiling Matters

Risk tolerance and risk profile are often used synonymously, but they’re distinct constructs when determining suitable risk levels for clients. While risk tolerance is how an investor feels emotionally about taking risk, a risk profile describes the amount of investment risk that’s suitable in the pursuit of an investment goal.

Building risk profiles can help advisors address evolving trends like:

Growing Need for Advice

Employers have made a seismic shift from pension plans to defined contribution plans, for example. This means employers contribute money, but employees are on their own to decide where to invest, how much to save, and how to allocate their portfolio.

If an investor wants a dignified retirement, they hold the responsibility to accomplish this goal. But without the professional training of advisors, it may be difficult for people to identify whether they’ve put away enough money for their future or are managing risk well. Unsurprisingly, only about 20% of households have a formal financial plan. Today’s investors need advisors who can translate complex risk concepts into simple, clear guidance—and show alignment between portfolios and goals.

Raised Customer Expectations

From healthcare to financial advice, consumers look for personalized experiences. Your clients want plans that reflect their unique needs instead of off-the-shelf options.

In one McKinsey survey, 70% of respondents ranked personalization as highly important to their banking experience. Advisors who deliver risk clarity and personalization can strengthen trust and long-term loyalty.

Increasing Regulatory Scrutiny

New know-your-client regulations require advisors to understand their clients in specific ways. These rules require advisors to document their work to recommend investments in their client’s best interest. Our defensible, data-backed methodology for the Morningstar Portfolio Risk Score helps advisors demonstrate compliance while proving the value of their recommendations.

Enhanced rules include:

- Regulation best interest

- The Department of Labor’s Prohibited Transaction Exemption 2020-02 governing 401(k) rollovers and client best interest

- The SEC marketing rule requiring advisors to show clients performance data net of fees

Sprawling Tech Stacks

Practices often piece together software to cover the full advisor process, seeking out the best-in-class options. But not all products live up to their promises of seamless data integration.

Disparate systems can lead to workflow snags, higher costs, and uneven advisor-client experiences. Financial advisors need a steady workflow with consistent outputs that clients understand. Morningstar's Direct Advisory Suite—our connected suite of tools—helps advisors quickly build plans, organize their business, communicate with clients, and more.

How Risk Profiles Might Influence Retirement Planning

While risk tolerance is a stable personality trait, other factors—like the time horizon—can affect how much risk your clients can afford. For instance, high-octane clients might feel ready to assume financial risk. But if they plan to retire in five years, their limited time horizon constrains their portfolio options. By aligning portfolios with both clients’ personality and time horizon, advisors can keep clients comfortably invested for the long term—transforming risk clarity into lasting confidence.

A Look at Risk Composure

As an element of risk tolerance, risk composure is the emotional reaction that people have when markets and portfolio values move up and down. If advisors can only measure risk composure, they won’t have a reliable understanding of their clients without also measuring risk tolerance. Portfolios that holistically fit a client’s real risk preferences can help them avoid impulsive decisions that don’t align with their goals.

Investment planning tools within Direct Advisory Suite give you an at-a-glance client overview. Advisors can build proposals and portfolios that fit clients’ goals and simplify the planning process with profiling tools that drive deeper conversations.

Identifying a Risk Tolerance Score

Today’s clients want to see portfolios that are made for their preferences, goals, and life circumstances—not pulled from a generic list. Morningstar's risk profiler has been administered nearly two million times, allowing advisors to benchmark clients with confidence.

When paired with the Morningstar Portfolio Risk Score, advisors gain a full-circle view:

- The Risk Tolerance Score shows who your client is.

- The Portfolio Risk Score shows what their portfolio is doing.

- Together, they reveal alignment—or misalignment—at a glance.

That transparency makes it easy to have meaningful, visual conversations about whether a client’s investments fit their comfort zone.

Four Steps for Portfolio Personalization

While Morningstar might be best known for its data and ratings, our KYC capabilities help you better understand investors.

Get started on personalizing portfolios with these tips:

1. Set goals and uncover preferences

With science-backed surveys, advisors can uncover why clients are investing—their priorities, motivations, and tradeoffs. Goals-based planning also helps your clients stay focused on the outcomes, not on the numbers. When clients understand why they’re investing, they can be more motivated to stick to the plan.

2. Analyze current portfolios

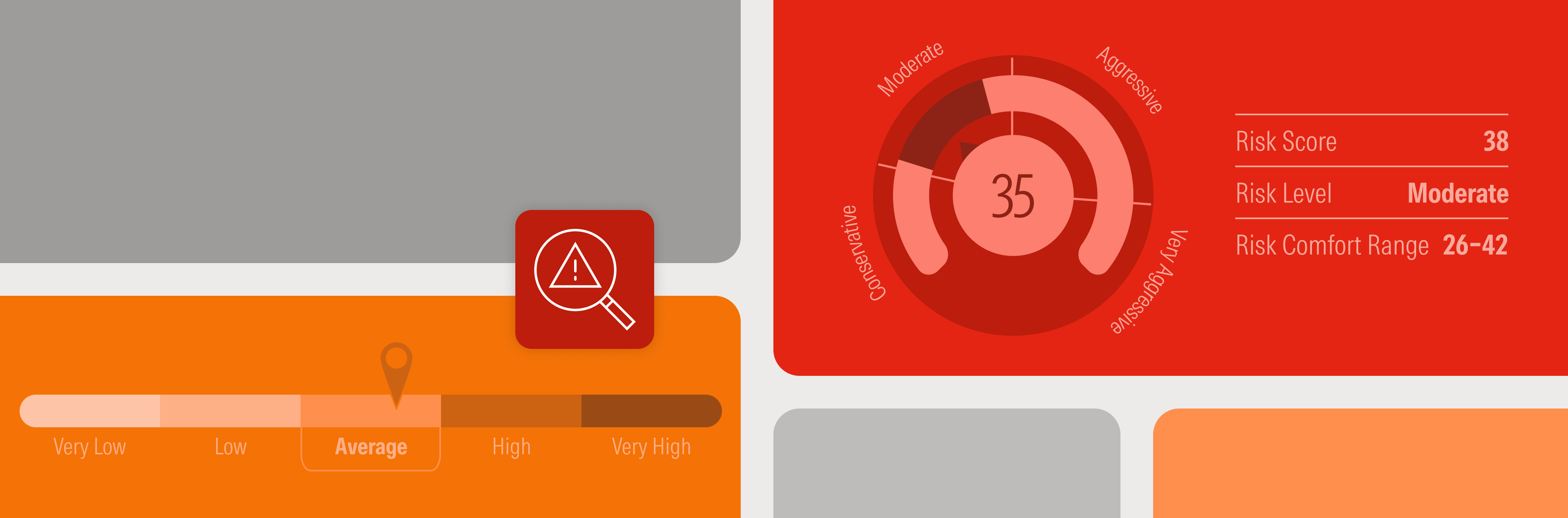

The Morningstar Portfolio Risk Score translates portfolio complexity into a simple, numeric score grounded in global target allocation indexes. It provides a transparent, data-driven benchmark to discuss risk exposure and ensure clients see exactly what level of risk they’re taking.

3. Measure risk tolerance and comfort range

The risk tolerance profiler quantifies each client’s willingness to take on risk, generating a Risk Comfort Range—a flexible zone of portfolio risk scores that fit their personality and goals. When portfolios fall inside this range, advisors can show true alignment and when they fall outside, they can proactively explain tradeoffs.

4. Build proposals with clarity and compliance

Within Direct Advisory Suite, advisors can seamlessly adjust allocations, document rationales, and create FINRA-reviewed client reports—turning what used to be a complex conversation into a clear, visual story that reinforces advisor value and client trust.

Together, these capabilities create risk clarity and help advisors prove value with transparent, data-backed recommendations that stand up to scrutiny and inspire confidence in every client conversation.

Better Support Clients

Every investor has different financial goals. When advisors know how to identify their clients’ attitude and comfort toward risk, it can be easier to provide personalized recommendations and improve relationships.

Build trust while streamlining your practice. Morningstar's Direct Advisory Suite turns client understanding into action by connecting risk, goals, and portfolio alignment within a single, compliant workflow.

.jpg?format=webp&auto=webp&disable=upscale)