Assets in Global Climate Funds March Steadily Higher

Appetite for U.S. climate investment funds rebounds in 2023.

/s3.amazonaws.com/arc-authors/morningstar/987376c2-20a0-406b-b3ec-df530324b39c.jpg)

Demand for climate funds continued climbing in the first half of 2023, with assets under management clocking in at more than $500 billion. The strongest appetite came from Europe. Investors also clamored for climate transition funds, which invest in companies that consider climate change in their business strategy. Those gains came even as demand slackened for sustainable funds broadly. Climate funds focus on climate-related topics, ranging from clean energy to decarbonization.

Over the past 18 months, investors and politicians wrangled over climate change mitigation strategies, net-zero commitments, and virtually all environmental, social, and governance topics. Still, demand for climate funds held steady.

In our recently released report, “Investing in Times of Climate Change,” we examined the global landscape of climate-focused funds, grouped these into five mutually exclusive categories, uncovered the growth in climate funds across markets, and drilled down to understand the characteristics of different strategies.

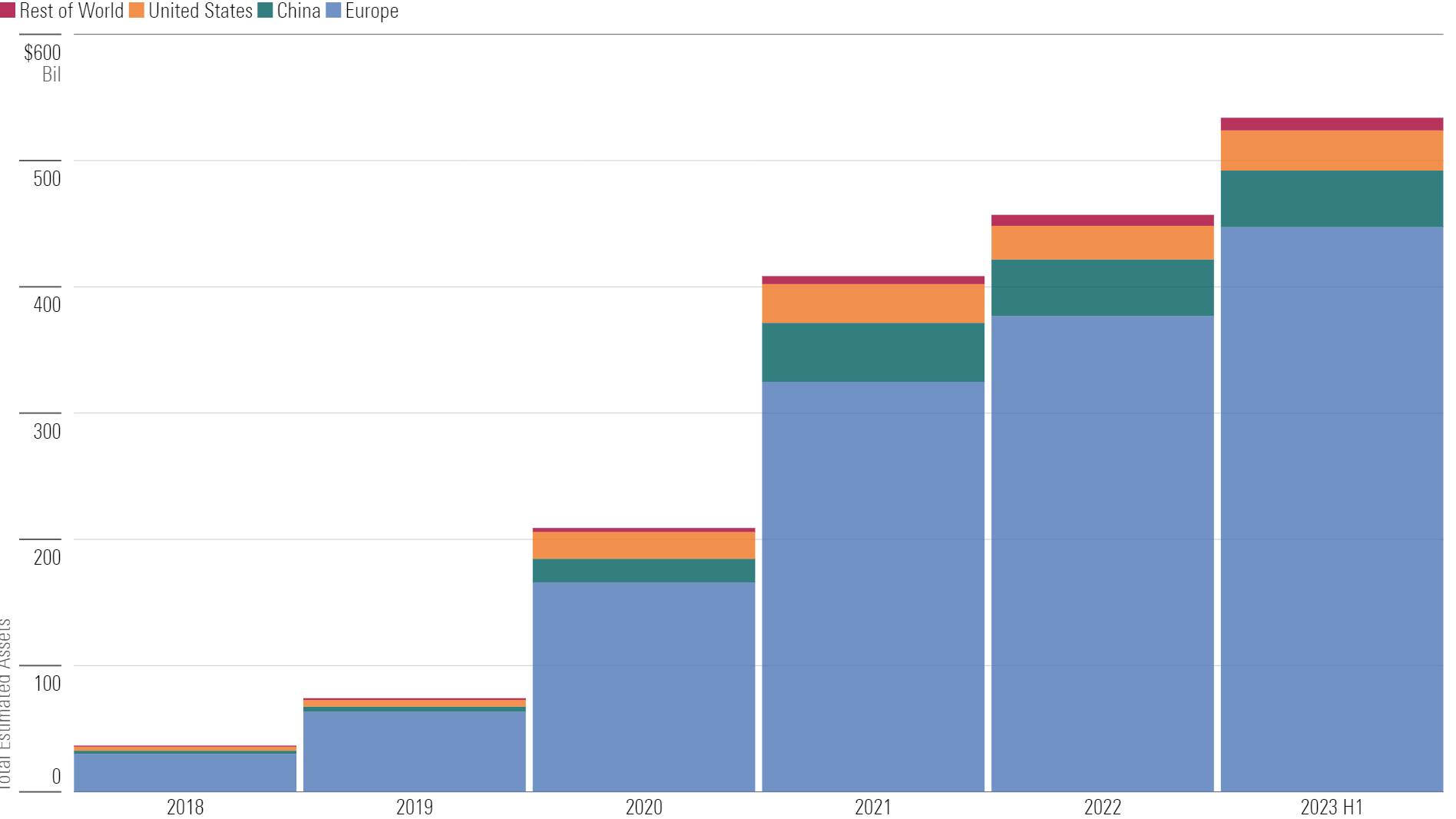

Halfway Through 2023, Assets in Climate Funds Balloon to Over Half a Trillion Dollars

As of June 2023, there were 1,407 climate-related open-end funds and exchange-traded funds that fit our definition, with collective assets under management of $534 billion worldwide. These represent almost 20% of the global sustainable funds landscape.

The global universe of funds with a climate-related strategy has surged by 30% in the past 18 months, driven by continued inflows and product development. Climate fund assets have grown at a faster clip than the global sustainable funds landscape and the broader open-end fund and ETF landscape, which have slid by 5% and 8%, respectively, since December 2021. Money invested in climate funds globally has increased 14-fold in the past five and a half years (since December 2018).

Europe Dominates, China and the U.S. Far Behind

Unsurprisingly, given the regulatory push toward climate neutrality, Europe remains the largest market for climate funds, accounting for 84% of global climate fund assets. Assets in European-domiciled funds with a climate-related strategy climbed by 38% over the past 18 months to $447 billion. As of June 2023, we identified 870 climate funds in Europe, compared with 223 in China and 117 in the United States.

Global Landscape of Climate Funds

China and the U.S. rank far behind at second and third, with market shares of 8% and 6%, respectively. Despite China’s continued commitment to reach peak CO2 emissions by 2030 and carbon neutrality by 2060, assets in climate funds domiciled in the country shrank to $44 billion as of June 2023, compared with the historic high of $47 billion at the end of 2021. In local currency, however, Chinese climate fund assets rose by 16% over the period. The decline in dollar terms is attributed to the weakening yuan, which mostly reflects China’s patchy economic recovery from its zero-Covid policy.

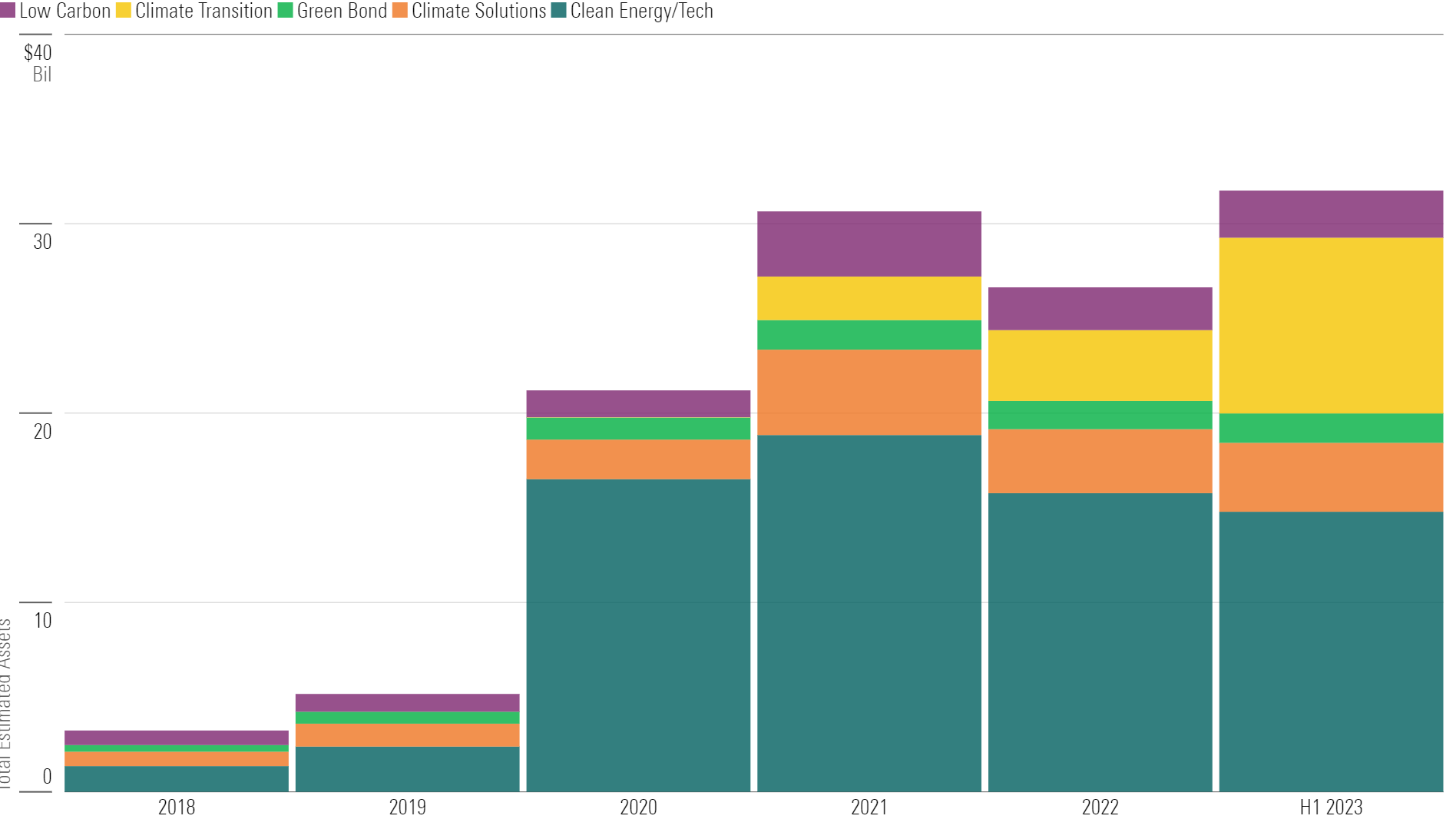

Assets Rise on the Back of Fresh Inflows

In stark contrast with Europe, assets in U.S. climate funds increased only slightly (by 4%) over the past 18 months. Assets shrank in 2022 on account of the challenging macro environment of high energy prices in the wake of Russia’s invasion of Ukraine and rising interest rates as central banks wrestled with inflationary pressures. In this environment, renewable energy stocks suffered. But strong flows into Climate Transition funds in the first half of 2023 sent assets to a new record of $31.7 billion at the end of June.

Clean Energy/Tech Funds Suffer From Poor Performance

While Clean Energy/Tech funds remain dominant among U.S. climate funds, they have lost assets and other categories have gained ground. As of June 2023, Clean Energy/Tech funds accounted for almost $14.8 billion in assets, or 47% of the total, down from a record 78% of market share at the end of 2020. Although these funds have suffered outflows, the decline is mostly attributable to falling valuations. Clean/Energy Tech funds tend to have high exposure to growth stocks, which often suffer in a rising-rate environment.

Meanwhile, assets in Climate Transition funds — which seek to invest in companies that consider climate change in their business strategy and are therefore better prepared for the transition to a low-carbon economy — have quadrupled over the past 18 months on account of $5.8 billion in net deposits over that time.

Assets in U.S. Climate Funds

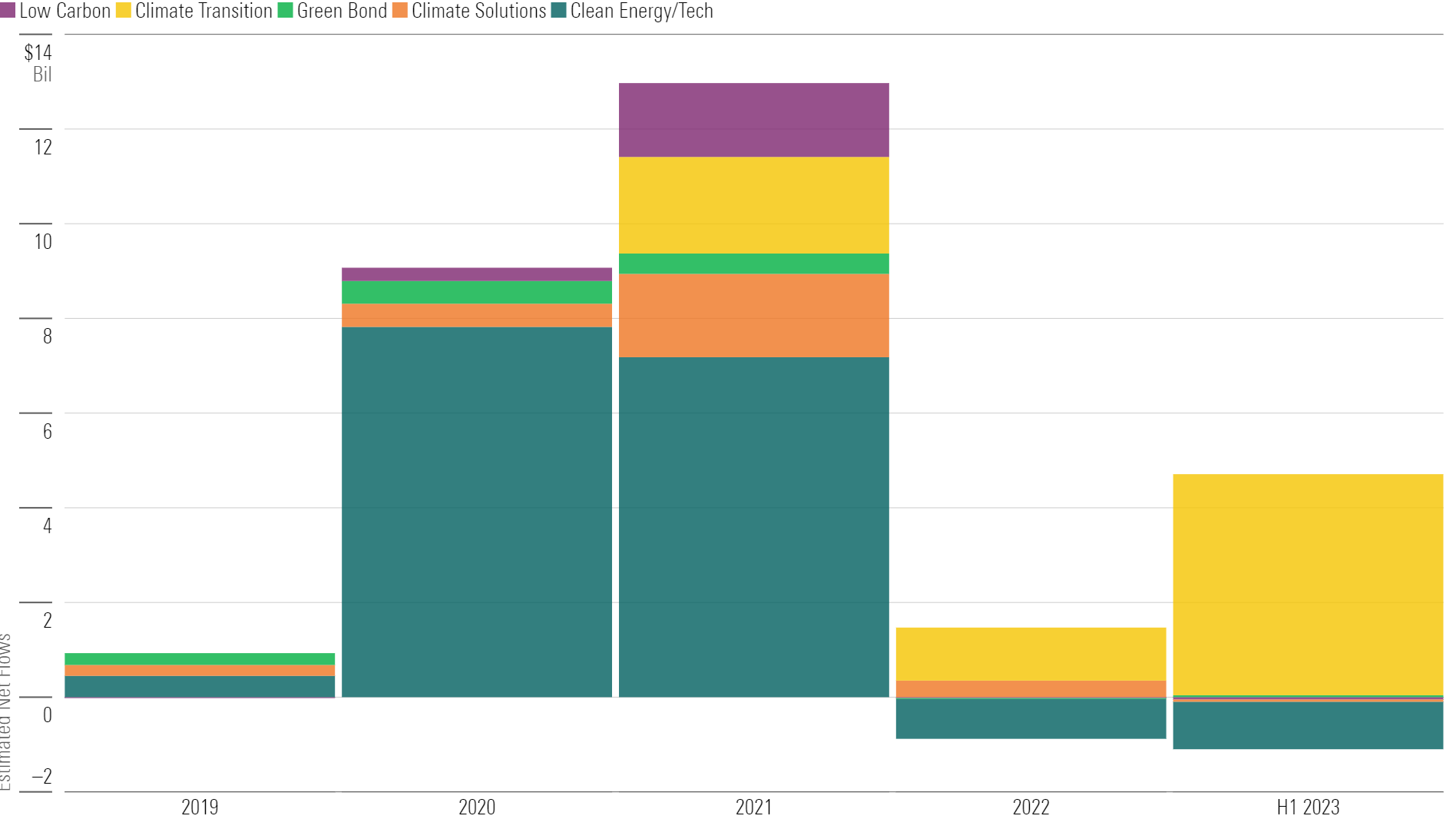

Climate Transition Funds Attract Most of the Flows

Except for Climate Transition funds, attracting new money hasn’t been easy. U.S. climate funds collected more than $3.6 billion so far in 2023, a notable drop from the segment’s record $13 billion haul in 2021. Still, flows into climate funds have been more resilient than in the rest of the U.S. Sustainable Funds Landscape, where 2022′s annual flows sank to their lowest level in seven years, and sustainable funds shed more than $5 billion in the first half of 2023.

Flows into U.S. Climate Funds

Within the climate funds landscape, Climate Transition funds were the clear winners, attracting $5.8 billion over the past 18 months and more than offsetting outflows from Clean Energy/Tech funds. Nearly three fourths of this haul went to Xtrackers MSCI USA Climate Action Equity ETF USCA and iShares Climate Conscious & Transition MSCI USA ETF USCL alone. Both funds track indexes that lean into companies that are well-positioned for the transition to a low-carbon economy or that are actively engaging in the climate transition relative to peers. These processes consider the companies’ carbon emissions intensity and emissions reduction targets, among other factors.

Product Development Activity Declines

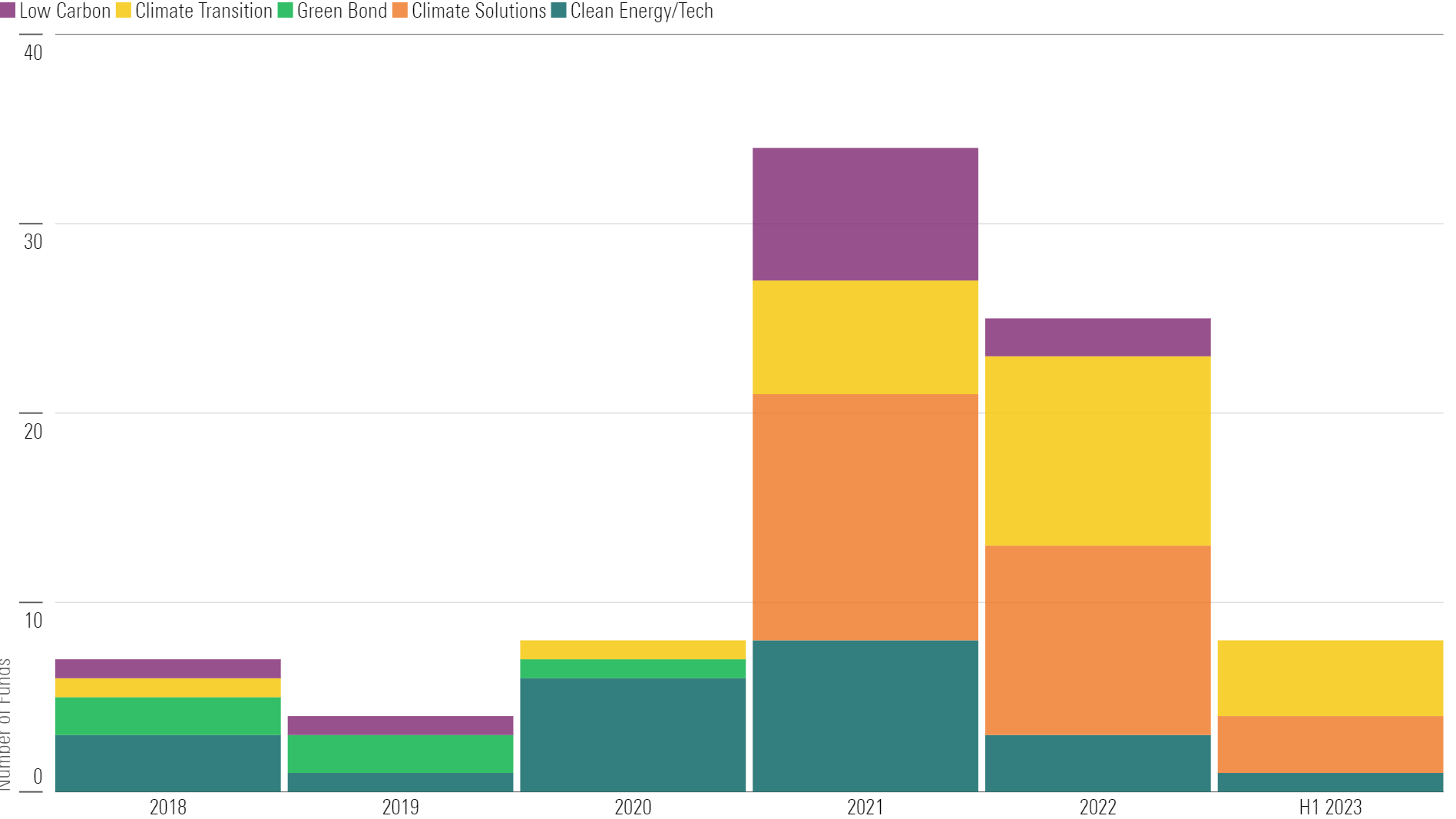

In line with the broader slowdown seen recently in the U.S., product development in climate funds has dropped since the peak in 2021. So far in 2023, only eight new climate strategies launched, roughly one fourth of the total seen in 2021. New sustainable fund launches have also slowed since 2021, so climate strategies still account for more than one fifth of the new strategies launched over the past 18 months.

Launches of U.S. Climate Funds

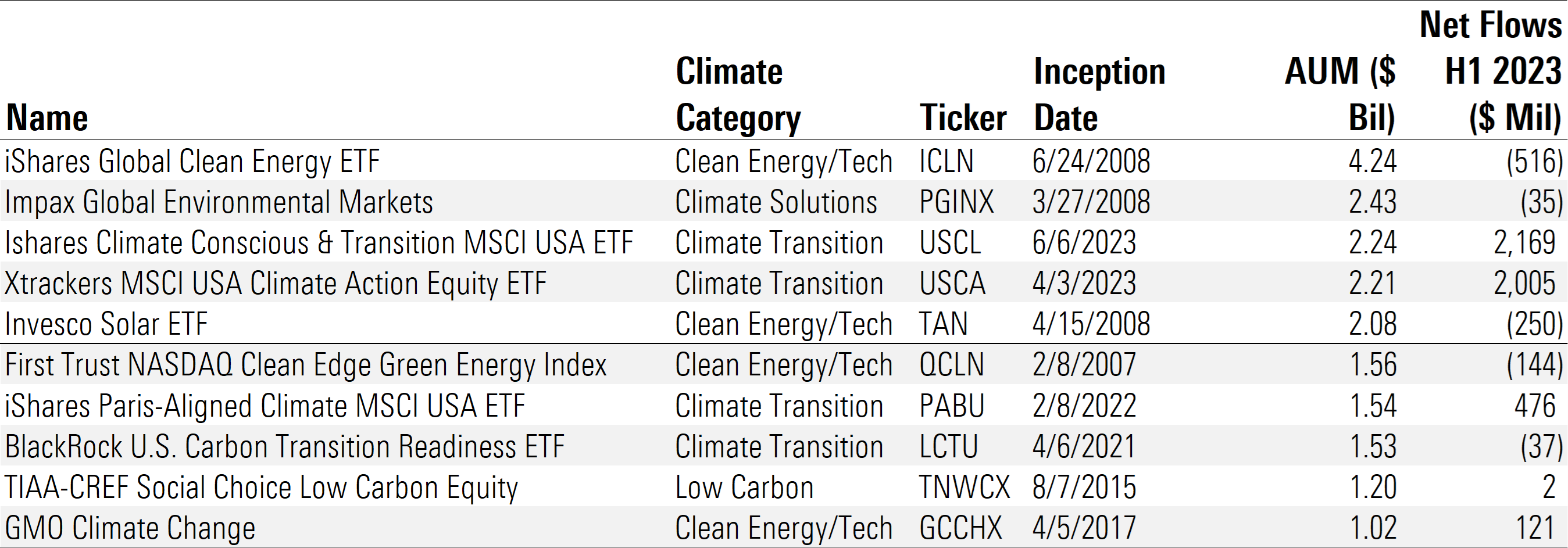

Below we list the 10 largest U.S. climate funds as of June 2023. Worth highlighting is iShares Global Clean Energy ETF ICLN, the largest fund in our climate fund universe, which suffered more than $500 million in outflows so far this year (the worst of any U.S. climate fund).

Top 10 Largest U.S. Climate Funds

Four of the 10 largest climate funds available to U.S. investors are Climate Transition funds. New to this year’s top 10 list are iShares Climate Conscious & Transition MSCI USA ETF, Xtrackers MSCI USA Climate Action Equity ETF, iShares Paris-Aligned Climate MSCI USA ETF PABU, and GMO Climate Change GCCHX. The first two launched in 2023′s second quarter but quickly shot up the ranks of the largest U.S. climate funds.

These new launches bring the total number of climate funds in the U.S. to 117 at the end of June.

To download the full report, click here.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/PJQ2TFVCOFACVODYK7FJ2Q3J2U.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/PVJSLSCNFRF7DGSEJSCWXZHDFQ.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/NNGJ3G4COBBN5NSKSKMWOVYSMA.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/987376c2-20a0-406b-b3ec-df530324b39c.jpg)