Our Ultimate Stock-Pickers' Top 10 High-Conviction Purchases

Several funds see value in technology, energy, and communication services.

/s3.amazonaws.com/arc-authors/morningstar/e03383eb-3d0b-4b25-96ab-00a6aa2121de.jpg)

For roughly the past decade, our primary goal with the Ultimate Stock-Pickers concept has been to uncover investment ideas that reflect the most recent transactions of our Ultimate Stock Pickers in a timely enough manner for investors to get some value from them. In cross-checking the most current valuation work and opinions of Morningstar’s own cadre of stock analysts against the actions of some of the best equity managers in the business, we hope to uncover a few good ideas each quarter that investors can dig into a bit deeper to see if they warrant an investment. With 24 of our Ultimate Stock-Pickers having reported their holdings for the second quarter of 2021, we now have a good sense of the stocks that piqued their interest during the period.

Recall that when we look at our Ultimate Stock-Pickers' buying activity, we focus on high-conviction purchases and new-money buys. We think of high-conviction purchases as instances when managers have made meaningful additions to their portfolios, as defined by the size of the purchase in relation to the portfolio's size. We define a new-money buy strictly as an instance where a manager purchases a stock that did not exist in the portfolio in the prior period. New-money buys may be done either with or without conviction, depending on the size of the purchase, and a conviction buy can be a new-money purchase if the holding is new to the portfolio.

We recognize that our Ultimate Stock-Pickers' decisions to purchase shares of any of the securities highlighted in this article could have been made as early as the start of January, so the prices paid by our managers could be substantially different from today's trading levels. Therefore, we believe it is always important for investors to assess for themselves the current attractiveness of any security mentioned here based on myriad factors, including our valuation estimates and our moat, stewardship, and uncertainty ratings.

The last few months have seen the global economy recovering from the economic headwinds brought on by the COVID-19 pandemic. More recently, the threats of variants have resulted in market anxiety. However, the overall market recovery from mid-2020 has been buoyed by a largely successful COVID-19 vaccine rollout in the United States. Even so, certain industries remain hard-hit (e.g., tourism, in-person shopping), though governments worldwide continue to take steps to mitigate the economic impact. The U.S. Federal Reserve has maintained the federal-funds rate at 0.00%-0.25%, and the U.S. government has taken many drastic measures since then to cushion the blow on the economy, including stimulus programs for consumers, unemployment benefits, easing pressures on debt markets, and establishing the PPP facility to help small businesses. With a democrat in the Oval Office, we could expect these measures to continue as the American economy readies itself for a comeback. Similar programs have been implemented across Europe and Asia as countries seek to boost their economies. The U.S. economy has also been aided by a successful vaccine rollout with the majority of the adult population having received the COVID-19 vaccine by the time this article was written. With vaccine rollouts accelerating across the world amid all this volatility and uncertainty, our Ultimate Stock-Pickers have managed to find value in individual stocks in a wide range of sectors, including technology, communication services, financial services, and healthcare.

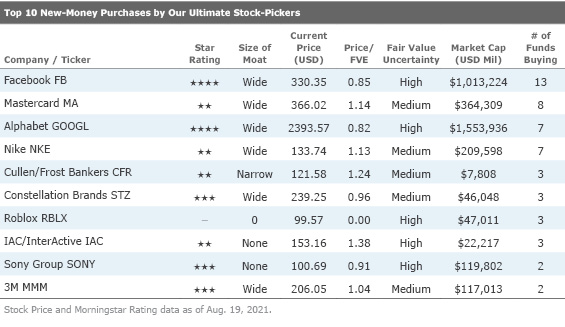

In the top 10 high-conviction purchases list, the buying activity heavily leaned toward the technology and telecommunications sectors, which received four high-conviction purchases this quarter. Communication services was not far behind, with two high-conviction purchases this quarter. Keeping with a trend we have witnessed over the years, nine out of 10 companies in the high-conviction purchases list received a wide or narrow economic moat from Morningstar analysts. The three names we find most interesting on the high-conviction purchases and new-money lists are wide-moat rated ASML Holding ASML, 3M MMM, and Nike NKE. Two money managers made high-conviction purchases of ASML. 3M received two new-money purchases, indicating money managers are putting money into the company despite not having any prior ownership of 3M’s shares. Finally, Nike had four high-conviction purchases.

There was a moderate amount of crossover between our two top 10 lists this period, with seven names appearing on both lists. This quarter, four stocks received four or more high-conviction purchases from our Ultimate Stock-Pickers. These names include Alphabet GOOGL, Mastercard MA, Nike, and Facebook FB. All these companies have economic moats according to Morningstar research, which indicates that money managers are putting down big bucks toward blue-chip stocks in a period of uncertainty.

One company that particularly stood out for us was wide-moat ASML Holding, as it attracted two high-conviction purchases to round off the second half of 2021. The firm currently trades at a 14% premium to Morningstar analyst Abhinav Davuluri’s fair value estimate of EUR 527.

ASML is the leader in photolithography equipment for semiconductor manufacturers. We expect it to materially benefit from the proliferation of extreme ultraviolet, or EUV, lithography, and we believe the uncertainty concerning the long-term extent of EUV insertion has sufficiently diminished to justify a wide moat rating. Photolithography is the process in which a light source is used to expose circuit patterns from a photomask onto a semiconductor wafer. A photomask is a flat, transparent quartz plate containing the microscopic circuit pattern. The latest technological advances in this field allow chipmakers to pursue Moore’s law and continually increase the number of transistors on the same area of silicon.

To continue pursuing Moore's law, chipmakers will require EUV lithography tools. EUV uses lower-wavelength light (13.5-nm versus 193-nm for current immersion tools) and simplifies the process flow (3 to 6 times cycle time reduction as a result of fewer steps and 15% to 50% cost reduction compared with multiple patterning schemes).

Davuluri believes that ASML has a wide economic moat based on its intangible assets around equipment design expertise in addition to research and development cost advantages required to compete for the business of leading-edge chipmakers. As the leading provider of photolithography equipment, the company exhibits considerable scale and technological superiority relative to its competitors. Its technical expertise and large R&D budget ($2 billion) serve as barriers to entry, but competitors do exist (Nikon and Canon), albeit in a substantially lesser capacity. Davuluri also notes that incumbent tool providers have intangible assets related to equipment design derived from service contracts and customer collaboration during process development and subsequent high-volume manufacturing. Taken together, these two sources of competitive advantage allow leading equipment firms to earn excess returns on invested capital over extended periods.

On the moat trend front, Davuluri assigns the company a positive moat trend rating, with the firm’s intangible assets associated with extreme ultraviolet lithography strengthening, especially over the next five years. The company is at the forefront of EUV lithography, a key technology that will enable the continued pursuit of Moore's law in an economical manner with fewer process steps to achieve finer critical dimensions on semiconductors. While this technology had been delayed, the minority equity stakes taken by Intel INTC, TSMC TSM, and Samsung SSNLF (totaling 23% in exchange for EUR 3.85 billion) show how committed these chipmakers are to the proliferation of EUV. As EUV has recently been inserted into high-volume manufacturing (7-nanometer process technologies at TSMC, Samsung, and Intel) the technology will help solidify ASML's position at key customers' manufacturing facilities and widen its economic moat.

Two of our Ultimate Stock-Pickers made high-conviction new-money purchases of 3M, a wide-moat company currently trading at a 4% premium to Morningstar analyst Joshua Aguilar’s fair value estimate of $195.

In Aguilar’s view, 3M is a GDP-plus business. He attributes 3M's ability to remain ahead of GDP based on its suite of innovative products that are a byproduct of its research and development efforts. At its core, 3M is a materials science company. The firm's legion of engineers improves everyday products down to their basic chemistry. For instance, 3M's microreplication technology, which has been around since the 1960s, was originally used in overhead projectors. That technology has now been adapted into multiple use cases, including making signs brighter, reducing friction in aerospace applications, and more recently, it is being developed for vaccine delivery as an alternative to hypodermic needles.

The firm's proprietary secrets are closely held as 3M rarely grants licenses, yet its technology is difficult to imitate. As a result, 3M typically charges a 10% to 30% price premium relative to the market. 3M's ability to adapt its technology into multiple use cases also gives it economies of scope, which helps reduce overall unit costs, evident in its superior gross margins.

Aguilar asserts that the firm can grow its top line about 5.5% over the next five years thanks to broad-based strength, even as respirator sales now become a near-term headwind. With the more recent acquisitions of workflow solutions provider MModal and negative wound care solutions provider Acelity, Aguilar believes that the firm can capitalize on the stable and ever-growing healthcare market.

On the economic moat front, Aguilar believes that 3M has a wide economic moat based on intangible assets and cost advantage. In the diversified industrials space, Aguilar thinks that having a central, leverageable core competence can be pivotal to building an enduring competitive advantage. 3M is an innovative powerhouse that leverages its R&D platform across multiple product categories, with byproducts that include patents, brands, and proprietary technology.

Our Ultimate Stock-Pickers also made four high-conviction purchases in wide-moat Nike, the largest athletic footwear and apparel brand in the world. Nike currently trades at a 13% premium to Morningstar analyst David Swartz’s fair value estimate of $128.

Swartz believes that Nike will overcome the challenges presented by COVID-19. Our wide moat rating on the company is based on its intangible brand asset, as Swartz believes it will maintain premium pricing and generate economic profits for at least 20 years. Nike, the largest athletic footwear brand in all major categories and in all major markets, dominates categories like running and basketball with popular shoe styles like Jordan, Air Max, and Air Force 1. Nike faces significant competition from the likes of Adidas ADDYY, Under Armour UAA, and Puma PUMSY among others, but Swartz believes that the company has proved over a long time period that it can maintain share and pricing.

Swartz asserts that Nike’s strategies allow it to maintain its leadership position. In mid-2017, Nike announced a consumer-focused realignment. It is investing in its direct-to-consumer network while reducing the number of retail partners that carry its products. In North America and elsewhere, the firm is reducing its exposure to undifferentiated retailers while increasing distribution through a small number of retailers, like narrow-moat Nordstrom JWN, no-moat Dick’s Sporting Goods DKS, and Foot Locker FL, that bring the Nike brand closer to consumers, carry a full range of products, and allow it to control the brand message. Nike’s consumer plan is led by its Triple Double strategy to double innovation, speed, and direct connections to consumers. Triple Double includes cutting product creation times in half, increasing membership in Nike’s mobile apps, and improving the selection of key franchises while reducing its styles by 25%. Swartz thinks that the combination of these strategies will allow Nike to hold share and pricing.

On the competitive advantage front, Swartz assigns Nike a wide moat rating based on its intangible brand asset. Nike is the largest athletic apparel company in the world, with more than $44 billion in revenue in fiscal 2021. Its revenue has increased in nine of the past 10 years, with pandemic-affected fiscal 2021 the sole exception. Nike produces apparel and footwear for professional and amateur athletes, sports equipment, and sports-inspired fashion for both athletes and nonathletes alike. As evidence of its competitive edge, Nike’s adjusted returns on invested capital, including goodwill, have averaged 35% over the past decade. Swartz forecasts that the company’s average annual adjusted ROICs, including goodwill, will exceed its weighted average cost of capital over the next 20 years, as required for our wide moat rating.

Disclosure: Justin Pan, Malik Ahmed Khan, and Eric Compton have no ownership interests in any of the securities mentioned above. It should also be noted that Morningstar's Institutional Equity Research Service offers research and analyst access to institutional asset managers. Through this service, Morningstar may have a business relationship with fund companies discussed in this report. Our business relationships in no way influence the funds or stocks discussed here.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/RNODFET5RVBMBKRZTQFUBVXUEU.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LJHOT24AYJCHBNGUQ67KUYGHEE.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/V33GR4AWKNF5XACS3HZ356QWCM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/e03383eb-3d0b-4b25-96ab-00a6aa2121de.jpg)