Our Ultimate Stock-Pickers' Top 10 High-Conviction Purchases

Several funds see value in technology and communication services.

/s3.amazonaws.com/arc-authors/morningstar/e03383eb-3d0b-4b25-96ab-00a6aa2121de.jpg)

For the past decade, our primary goal with Ultimate Stock-Pickers has been to uncover investment ideas our equity analysts and top investment managers find attractive, in a manner timely enough for investors to gain value. In cross-checking the most current valuation work and opinions of Morningstar’s own cadre of stock analysts against the actions of some of the best equity managers in the business, we hope to uncover good ideas each quarter that will be of interest to investors. With 22 of our Ultimate Stock-Pickers having reported their holdings for the third quarter of 2021, we now have a good sense of the stocks that piqued their interest during the period.

When we look at our Ultimate Stock-Pickers' buying activity, we concentrate on high-conviction purchases and new-money buys. We think of high-conviction purchases as instances when managers have made meaningful additions to their portfolios, as defined by the size of the purchase in relation to the portfolio's size. We define a new-money buy strictly as an instance where a manager purchases a stock that did not exist in the portfolio in the prior period. New-money buys may be done either with or without conviction, depending on the size of the purchase, and a conviction buy can be a new-money purchase if the holding is new to the portfolio.

We recognize that our Ultimate Stock-Pickers' decisions to purchase shares of any of the securities highlighted in this article could have been made as early as the start of July, so the prices paid by our managers could be substantially different from today's trading levels. Therefore, we believe it is always important for investors to assess for themselves the current attractiveness of any security mentioned here based on a multitude of factors, including our valuation estimates along with our moat, stewardship, and uncertainty ratings.

Despite earlier headwinds created by COVID-19, the overall market recovery from mid-2020 has been buoyed by a largely successful vaccine rollout in the United States. Certain industries remain more impacted than others (e.g., tourism, in-person shopping), though governments worldwide continue to take steps to mitigate the economic impact. The U.S. Federal Reserve has maintained the federal-funds rate to 0.00%-0.25%, and the U.S. government has taken many drastic measures since then to cushion the blow on the economy, including stimulus programs for consumers, unemployment benefits, easing pressures on debt markets, and establishing the PPP facility to help small businesses. With a democrat in the Oval Office, we could expect these measures to continue as the U.S. economy readies itself for a comeback. Similar programs have been implemented across Europe and Asia as countries seek to boost their economies. The U.S. economy has also been aided by a successful vaccine rollout with the majority of the adult population having received the COVID-19 vaccine as of the time of writing. With vaccine rollouts accelerating across the world amid a period of volatility and uncertainty, our Ultimate Stock-Pickers have managed to find value in individual stocks in a wide range of sectors such as industrials, technology, communication services, financial services, and healthcare.

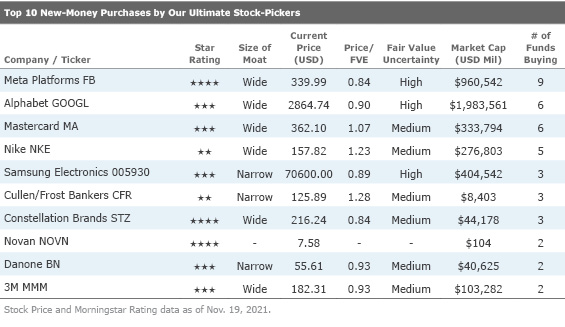

In the top 10 high-conviction purchases list, the buying activity heavily leaned toward technology but also included industrials and healthcare. All 10 companies in the high-conviction purchases list received a wide or narrow economic moat rating from Morningstar analysts, keeping in line with trends we have witnessed over the past years. In the top 10 new-money purchases list, we note a multitude of technology names such as Alphabet GOOGL, Meta FB, and Samsung 005930. Similar to the companies on the high-conviction purchases list, nine out of the 10 companies in the new-money list received either a wide or narrow moat rating from Morningstar, indicating a clear preference for established blue-chip stocks. Meta received the highest number of new money purchases, with nine. Alphabet and Mastercard MA received six each. The three names we find most interesting on the high-conviction purchases and new-money lists are wide-moat rated UnitedHealth Group UNH, Nvidia NVDA, and Paccar PCAR.

There was a moderate amount of crossover between our two top 10 lists this period, with four names appearing on both lists. This quarter, three stocks received four or more high-conviction purchases from our Ultimate Stock-Pickers. These names include Alphabet, Meta, Mastercard, and Nike NKE, with Alphabet having received 10 high-conviction purchases. All three of these companies have economic moats according to Morningstar research, which indicates that money managers place an emphasis toward blue-chip stocks such as these in a period of uncertainty.

Narrow-moat UnitedHealth Group One particularly stood out for us as it attracted three high-conviction purchases to round off the third quarter of 2021. UnitedHealth currently trades at around $440, a premium to Morningstar analyst Julie Utterback’s fair value estimate of $350.

UnitedHealth is the largest private health insurance provider in the United States, providing medical benefits to 48 million members across its U.S. and international businesses at the end of 2020. As a leader in employer-sponsored, self-directed, and government-backed insurance plans, UnitedHealth has obtained massive scale in managed care. Along with its insurance assets, UnitedHealth's continued investments in its Optum franchises have created a healthcare services colossus that spans everything from medical and pharmaceutical benefits to providing outpatient care and analytics to both affiliated and third-party customers.

According to Utterback, UnitedHealth combines the largest private health insurer (UnitedHealthcare), a top three pharmacy benefit manager (OptumRx), a large service provider (OptumHealth), and a widely used health analytics franchise (OptumInsight). The company's integrated strategy has resulted in some of the best returns in the industry in recent years and has been copied, at least in part, by the late 2018 mergers at CVS Health CVS (added Aetna's insurance assets to its existing retail stores and market-leading PBM) and Cigna CI (added Express Scripts PBM assets to its existing insurance operations). Outside of substantial regulator-led reforms, Utterback thinks that these vertically integrated organizations could help bend the healthcare cost curve in the U.S., and UnitedHealth should be one of the key leaders of that charge going forward.

According to Morningstar analysis, UnitedHealth has demonstrated an uncanny ability to remain at the leading edge of changes affecting the industry. For example, its 2015 acquisition of Catamaran greatly increased its PBM scale and helped create a more holistic view of a patient's care. That combination of services has created attractive synergies for clients, such as employers or government programs, seeking to lower overall healthcare costs rather than just pharmacy or medical benefits. Adding service providers to the mix aligns incentives even further, especially since the firm's outpatient care assets offer significantly lower costs than hospital-based services. The firm's analytical tools help organizations pull various healthcare information related to its other operations together to provide an even fuller picture of a patient's health and care options.

By providing those diverse yet connected services, UnitedHealth aims to grow in nearly any regulatory environment. Specifically, it is shooting for 13% to 16% earnings growth in the long run, including strong operational growth and capital allocation activities, such as acquisitions and repurchases. Utterback notes that while some regulatory scenarios could eventually cut into that mission, the value that UnitedHealth provides to the U.S. healthcare system will likely help it remain relevant in the long run.

Utterback’s narrow moat rating for UnitedHealth Group reflects the generally narrow-moat view of the U.S. health insurance and PBM industries and an unclear outlook for economic profitability outside her 10-year explicit forecast period due to regulatory concerns. As the top private U.S. health insurer, a top-three pharmacy benefit manager, a major service provider, and a leading analytics firm, she believes UnitedHealth possesses enough scale-related cost advantages to generate economic profits for at least the next 10 years. Including goodwill, UnitedHealth’s returns currently are more than double its capital costs, and it is projected that they will remain well above its capital costs throughout Utterback’s explicit 10-year forecast period, which is the signature of a narrow-moat firm.

Three of our money managers made high-conviction new-money purchases of Nvidia, a wide-moat company currently trading at a hefty premium to Morningstar analyst Abhinav Davuluri’s fair value estimate of $200.

In Davuluri’s view, Nvidia is the top designer of discrete graphics processing units that enhance the experience on computing platforms. The firm's chips are used in a variety of end markets, including high-end PCs for gaming, data centers, and automotive infotainment systems. In recent years, Davuluri has noted that the firm has broadened its focus from traditional PC graphics applications such as gaming to more complex and favorable opportunities, including artificial intelligence and autonomous driving, which leverage the high-performance capabilities of the firm's graphics processing units. Traditional GPU uses include professional visualization applications that require realistic rendering, including computer-aided design, video editing, and special effects. Nvidia has experienced success in focusing its GPUs in nascent markets such as artificial intelligence (deep learning) and self-driving vehicles. Hyperscale cloud vendors have leveraged GPUs in training neural networks for uses such as image and speech recognition.

Davuluri posits that the linchpin of Nvidia’s current business is gaming. PC gaming enthusiasts generally purchase high-end discrete GPUs offered by the likes of Nvidia and AMD AMD. Going forward, he expects the data center segment to drive most of the firm’s growth, led by the explosive artificial intelligence phenomenon. This involves collecting large swaths of data followed by techniques that develop algorithms to produce conclusions in the same way as humans. As Moore’s law-led CPU performance improvements have slowed, GPUs have become widespread in accelerating the training of AI models to perform a task. However, the other solutions are more suitable for inferencing, which is the deployment of a trained model on new data. Today’s basic variants of AI are consumer-oriented and include digital assistants, image recognition, and natural language processing.

According to his analysis, Nvidia views the car as a “supercomputer on wheels,” and the firm possesses the opportunity to grow its presence in cars beyond infotainment as drivers seek autonomous features in newer vehicles. Nvidia's Drive PX platform is a deep learning tool for self-driving that is being used in R&D at more than 370 partners. More recently, Nvidia acquired Mellanox to bolster its data center offerings in the networking realm to raise switching costs and improve performance of Nvidia’s existing portfolio. In September 2020, the firm agreed to purchase ARM from SoftBank for $40 billion.

On the moat front, Davuluri believes that Nvidia possesses a wide economic moat stemming from its intangible assets related to the design of graphics processing units, or GPUs. As the originator of and leader in discrete graphics, the firm has captured the lion’s share of the market from longtime rival AMD. Furthermore, the market has significant barriers to entry in the form of advanced intellectual property, as even chip leader Intel was unable to develop its own discrete GPUs (despite its vast resources) and ultimately needed to license IP from Nvidia to integrate GPUs into its PC chipsets (though more recently Intel is vying to develop its own discrete GPU). To stay at the cutting edge of GPU technology, Nvidia has a large R&D budget relative to AMD and smaller GPU suppliers that allows it to continuously innovate and fuel a virtuous cycle for its high-margin chips.

Our Ultimate Stock-Pickers also made three high-conviction purchases in narrow-moat Paccar, a manufacturer of medium and heavy-duty trucks. Paccar currently trades at a slight premium to Morningstar analyst Dawit Woldemariam’s fair value estimate of $98.

According to Woldemariam, Paccar is a leading manufacturer of medium- and heavy-duty trucks under the premium brands Kenworth and Peterbilt, which are primarily sold in the NAFTA region and Australia, and DAF trucks, which are sold in Europe and South America. Its trucks are sold globally through over 2,200 independent dealers. Paccar Financial Services provides retail and wholesale financing for customers and dealers, respectively. The company commands approximately 30% of the Class 8 market share in North America and 16% of the heavy-duty market share in Europe.

Paccar’s strategy focuses on creating high-quality premium products for customers, which Woldemariam believes will continue to translate into market share gains in the near term. He also thinks Paccar will continue to extend its global reach, as government authorities in Brazil, India, China, and Australia introduce new emission standards. The global trucking industry is going through a fundamental shift today, brought on by new emission regulations that will force fleet owners to refresh their fleet with more emission-compliant trucks over the next few years, benefiting Paccar. Woldemariam believes Paccar is making the necessary investments today in order to succeed in a zero-emission world. In early 2021, the company entered into a partnership with Aurora, an autonomous driving software provider and has also launched BEV prototypes. Paccar is expected to reach modest production volume over the next few years, as electrification in the trucking industry proliferates.

Woldemariam expects Paccar to excel in the near term, given strong trucking industry tailwinds. The global health pandemic depressed freight demand early on, but trucking activity has since rebounded. Strong consumer spending on consumer goods and e-commerce growth pushed demand higher. He expects new truck orders to increase in the near term, as the current backlog of orders is likely to supply production for the remainder of the year. Woldemariam noted that in good times, truck operators replace aging trucks and opt to expand their fleet to meet strong demand. Longer term, he thinks Paccar will be one of the leading players in the trucking industry, which he expects to be largely zero-emission. The company can use strong returns from its diesel business today to fund investments.

On the competitive advantage front, Woldemariam assigns Paccar a narrow economic moat rating, thanks to its strong brand reputation in the trucking industry. Paccar’s premium brands, Peterbilt, Kenworth, and DAF draw strong brand loyalty from fleet owners. The company’s trucks are some of the strongest performing and most durable in the industry. Paccar’s strong operational performance and focus on fuel efficiency helps customers lower the total cost of their operations. Woldemariam believes fleet owners are willing to pay higher up-front prices if it means they’ll save on fuel, maintenance, and repair costs over the life of a truck. Customers also find value in Paccar’s strong secondary market, where fleet owners can easily sell their trucks to optimize their fleet. In his view, switching costs are rather low for truck manufacturers. Most tractors are compatible with different trailer platforms, making it possible for fleet owners to operate a diverse set of tractors.

Disclosure: Justin Pan, Eden Alemayehu, and Eric Compton have no ownership interests in any of the securities mentioned above. It should also be noted that Morningstar's Institutional Equity Research Service offers research and analyst access to institutional asset managers. Through this service, Morningstar may have a business relationship with fund companies discussed in this report. Our business relationships in no way influence the funds or stocks discussed here.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ECVXZPYGAJEWHOXQMUK6RKDJOM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/KOTZFI3SBBGOVJJVPI7NWAPW4E.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/V33GR4AWKNF5XACS3HZ356QWCM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/e03383eb-3d0b-4b25-96ab-00a6aa2121de.jpg)