5 min read

Faith-Based Investing Is a Small, But Growing, Niche

A fundamental review of religiously themed funds using Morningstar’s faith-based strategy tags.

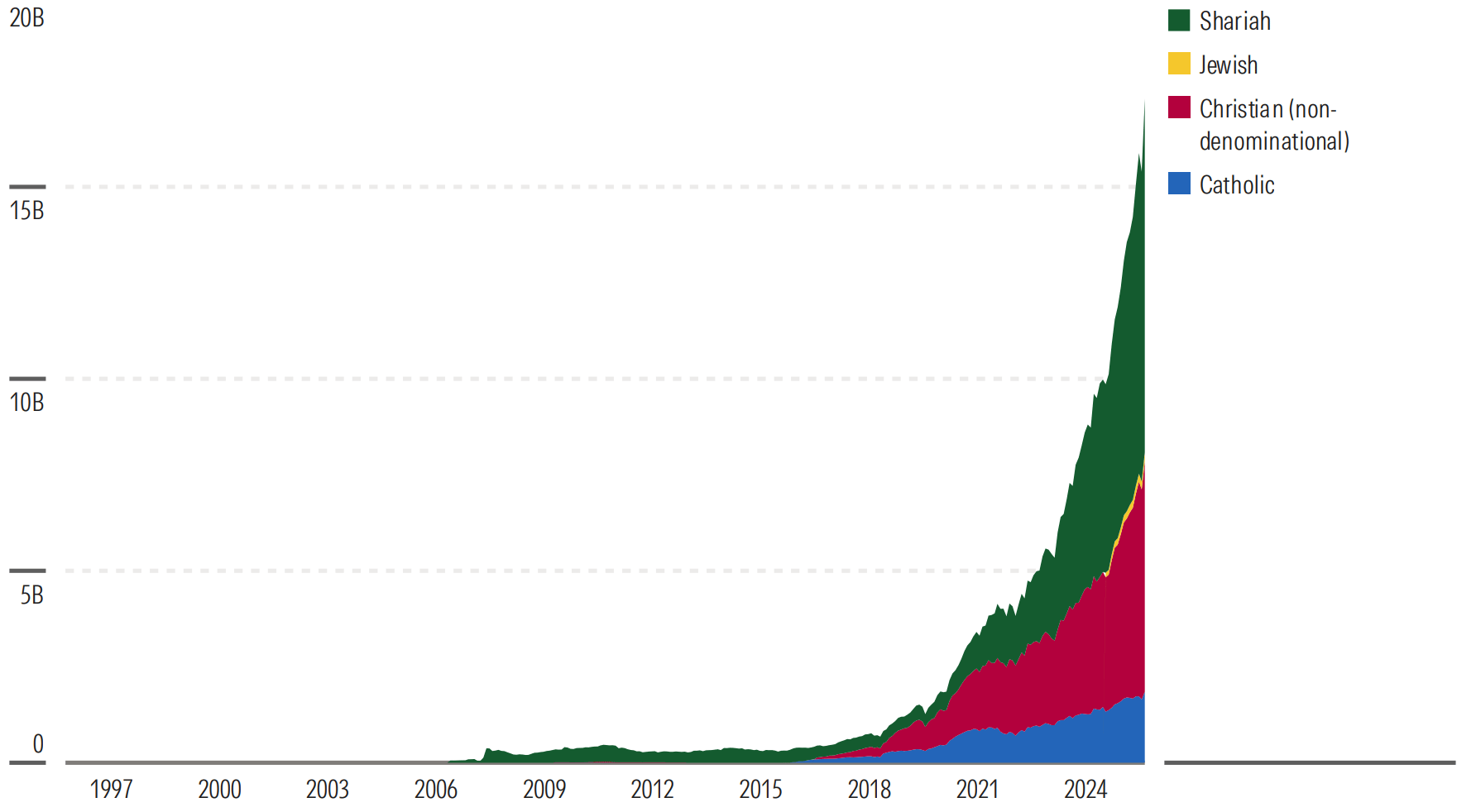

Faith-based investment strategies, which comply with certain religious convictions, have grown substantially in recent years, with AUM growing at a compound rate of 18% over the 30 years to March 2026 and the number of strategies growing by 11% per year.

We’ve extended our total universe of faith-based funds to a total of 853 active funds across the US, Middle East, Asia, and Europe as of April 30, 2026. Of these 853 funds, 650 were Shariah, 114 were non-denominational Christian, 87 were Catholic funds, and one was a Jewish fund.

Here's how these investing strategies stack up based on manager tenure, total expenses, and fund flows.

AUM in Religious ETFs Has Grown Rapidly Over Recent Years

Source: Morningstar Direct. Data as of April 30, 2026.

How Morningstar Categorizes Faith-Based Strategies

The faith-based strategy tag, available in Morningstar Direct and licensed data feeds, indicates strategies that invest according to certain religious convictions based on explicit prospectus language. It can help financial advisors find appropriate investments for clients who want to build portfolios in accordance with their clients' faiths.

The tag is not a formal analytical rating. Since Morningstar allows funds to self-identify their religious affiliation and influences, screening criteria can vary among and even within the types.

The brief definitions below summarize common portfolio characteristics.

Catholic Investing Strategies

US Catholic mutual funds and ETFs often apply investment screens based on the Socially Responsible Investment Guidelines of the U.S. Conference of Catholic Bishops, or USCCB, organized around five principles:

- Protecting human life

- Promoting human dignity

- Enhancing the common good

- Pursuing economic justice

- Saving our global common home

These funds typically exclude companies involved in abortion, contraception, embryonic stem cell research, euthanasia, pornography, gambling, tobacco, and weapons of mass destruction.

Christian (Non-Denominational) Investing Strategies

Non-denominational Christian funds, sometimes referred to as Biblically Responsible Investing approaches, often apply investment screens rooted in broadly evangelical Christian or interdenominational Protestant values. They are not affiliated with a single church body or formal doctrinal standard. This category makes up most of the faith-based universe in terms of assets under management.

These funds often exclude companies involved in abortion, pornography, alcohol, tobacco, and gambling, though individual fund families vary in the breadth and strictness of their screens.

Sharia Investing Strategies

Sharia-aligned funds are usually structured to comply with Islamic law. They apply both qualitative screens that exclude companies in categorically forbidden industries—including alcohol, pork, conventional banking, gambling, tobacco, and weapons—and quantitative financial screens that restrict investment in companies with excessive interest-bearing debt.

Sharia-aligned portfolios avoid conventional bonds. They achieve fixed income exposure through sukuk, which are debt-like financial instruments structured to comply with Islamic law’s prohibition against interest.

Jewish Investing Strategies

There is currently only one Jewish faith-based fund, and it aligns its investments with Jewish values, emphasizing shareholder advocacy over broad exclusionary screening.

Core principles include combating antisemitism and hate, supporting Israel, and advancing tikkun olam—repairing the world—through promotion of social justice, environmental responsibility, and ethical corporate behavior.

Unlike Christian and Sharia investing approaches, Jewish funds generally do not screen out alcohol or gambling.

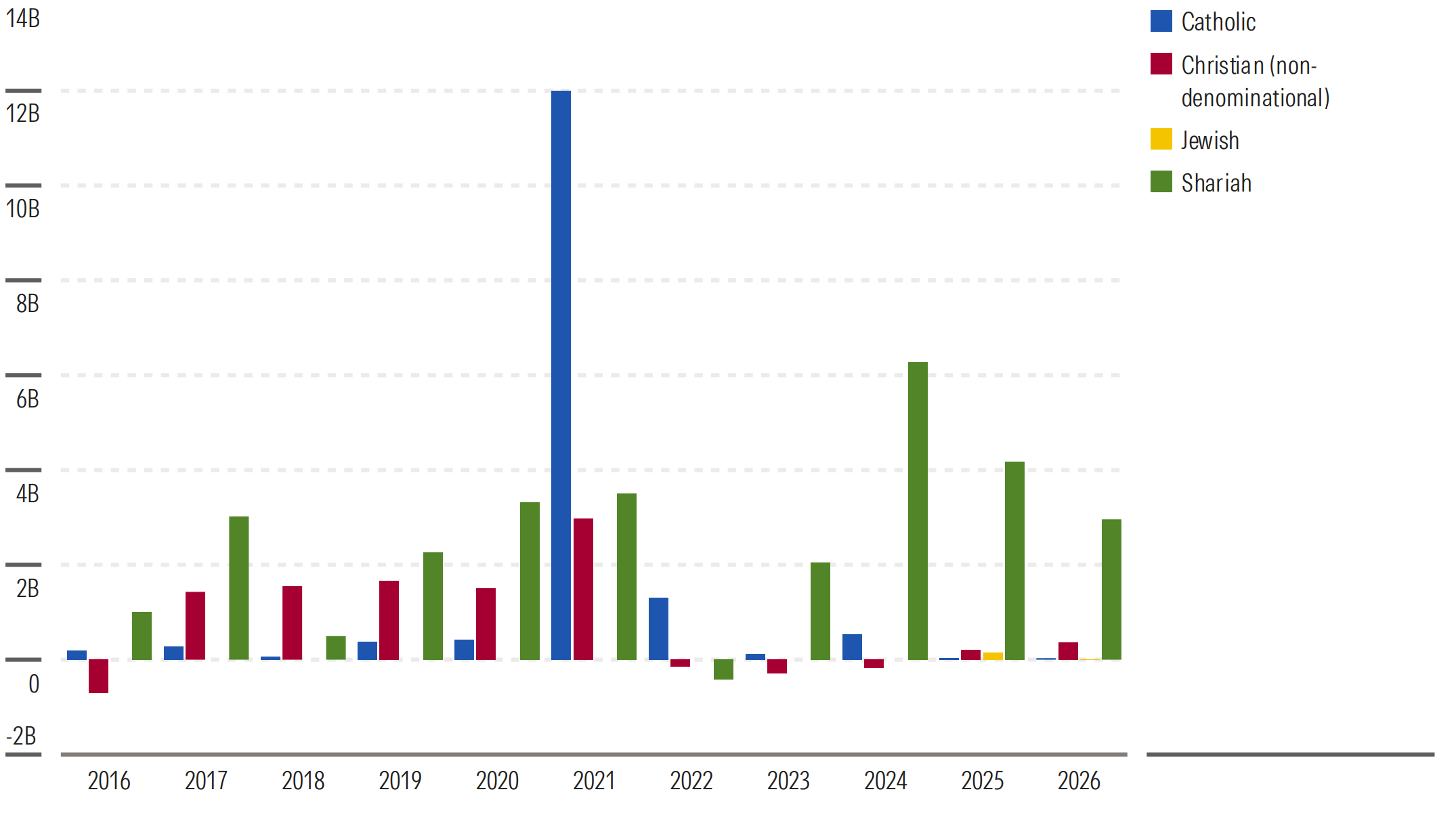

A Look at Faith-Based Fund Flows

Shariah flows have generally led over the 10 years to 2026, albeit with the most volatility in the peer group; for instance, despite strong overall inflows over recent years, we saw substantial outflows of USD 2 billion for Middle East-domiciled Shariah products over 2022.

While we saw substantial Catholic inflows over 2021, this was due to the launch of several Catholic Responsible Investments products, as opposed to net inflow into an existing strategy. Catholic strategies have tended to have small but continuously positive flows, particularly driven by the US with European Catholic and Christian strategies having net outflows over 2023-26.

Annual Flows by Faith

Source: Morningstar Direct. Data as of April 30, 2026.

Given the small universe, movements among and within religiously themed asset managers can have a big effect. The largest firms by AUM continue to be US-based Christian and Catholic investment houses, most of which built their franchises around actively managed strategies rather than index tracking products, such as GuideStone, Catholic Responsible Investments, and Eventide, although we have seen several of these firms venture into the passive space. Given the considerable growth we have seen in Shariah assets, houses such as HSBC, Amana, and Aham Asset Management have rapidly grown in the open-end fund space.

Faith-Based Investing Often Costs a Little More

On average, religious funds are more expensive than their non-religious counterparts, reflecting perhaps less competition, particularly from passives, which have only gained market share rapidly in the past few years. A more niche audience and lower allocation of institutional capital have also perhaps led to a less competitive landscape in terms of fee pressures. That said, there were some competitively priced products, notably active Shariah equity funds in Europe and the US.

Notably though, there is a considerable premium on faith-based passives, where average fee level generally sits at double that of the non-religious cohort. This likely reflects smaller fund sizes and a lack of scale economics in faith-based passive ranges, rather than any meaningful difference in the complexity of the underlying index construction.

To look more granularly at the regional differences, we calculate asset-weighted average fee levels by faith and domicile. We see the Middle East and Other (largely Malaysian-domiciled Shariah funds) as being relatively expensive for active funds, whereas US-based non-equity strategies were generally competitively priced. Again though, we see the US as dominating in terms of passive offering, where fees were considerably lower than their European, Middle Eastern, and Asian peers.

Faith-Based Fund Managers Often Have Shorter Tenures

Average and median manager tenure for faith-based funds are often shorter than those of the broader mutual fund and ETF universe. The shorter tenures, in part, owe to the relative youth of faith-based funds, nearly half of which launched in the last 10 years.

Tenure also does not always equal experience. Guidestone Funds Medium Duration Bond’s average manager tenure is less than four years, for example, but much more seasoned managers from established firms, including PIMCO, Loomis Sayles, and Guggenheim, subadvise the strategy.

Ave Maria Value Focused Fund AVERX, which invests in accordance with Catholic teachings, and Iman Fund IMANX had the longest average manager tenures among faith-based funds.

Faith-Based Portfolios Cluster Around the Core

Faith-based funds cluster around the core column of the Morningstar Style Box, based on the size and value-growth scores of their holdings. They also offer more options in the growth area of the style box than in the value zones. Particularly in Europe we see Christian and Catholic funds with a more prominent growth tilt than their US counterparts, who have more of a value leaning in aggregate.

Sharia funds typically exclude financials and debt-laden companies, which gives them a growth tilt. Amana Growth AMAGX, for example, has more than half its assets in technology stocks and none in more value-leaning financials, basic materials, and utilities companies.

Faith-Based Equity Style by the Numbers

Investors have fewer choices for faith-based fixed income funds, but providers offer the basics. Most of the offerings are in the short-term, intermediate core, and intermediate core-plus categories, which can serve as the linchpins of fixed income portfolios.

Christian (non-denominational) asset managers have the widest variety of bond offerings, including at least one high-yield one: Timothy Plan High Yield Bond TPHAX.

There are no Jewish-themed bond funds. Sharia-compliant fixed income offerings are all in the global bond and short-term bond categories, which can hold sukuk.

How Does Faith-Based Investing Differ From ESG Investing?

ESG investing and faith-based investing both aim to deliver positive returns while aligning with specific investor values, often through exclusions. However, environmental, social, and corporate governance concerns include a more varied group of potential issues.

Faith-based investing approaches often use exclusionary screenings to avoid investments that don’t align with religious convictions, while many ESG funds exclude industries like oil and gas, as well as optimizing for exposure within the context of a diversified portfolio. Both approaches may also prioritize impact investing, stewardship, and risk mitigation.

Not all funds with the ESG label prioritize the same issues. The term broadly refers to a range of material financial issues, including water and land use, carbon emissions, and broader impact on the community, among others.

How Do I Evaluate Faith-Based Investing Strategies?

The faith-based strategy tag in Morningstar Direct and licensed data solutions allows financial advisors and asset managers to filter investments by their stated objectives. Teams can use the tag for workflows like:

- Investment screens based on client values or objectives.

- Comparison of the risk and return tradeoffs of incorporating a faith-based fund into a portfolio.

- Competitive analysis against similar strategies with fund flows data.

From there, professional investors can use portfolio comparison tools to evaluate past performance, expenses, and any style tilts that may inform a fund’s role in a portfolio.