4 min read

Drawing an ESG Materiality Map

Ranking countries’ ESG practices and their levels of carbon risk.

According to Morningstar research, European countries—particularly those in the north—lead the pack in ESG practices. While those nations have always been ahead of the curve on this front, a few other countries also feature exceptionally strong sustainability profiles. Financial advisors and asset managers can use this data to identify countries with the greatest ESG investment opportunities and most significant risks.

In March 2020, Morningstar Sustainalytics used the constituents of Morningstar country indexes to examine the sustainability profiles of 48 country-specific equity markets. Sustainalytics calculated the company-level scores and also powers the ESG Risk Rating for funds.

Here, we explore some key findings about the ESG practices of countries around the world.

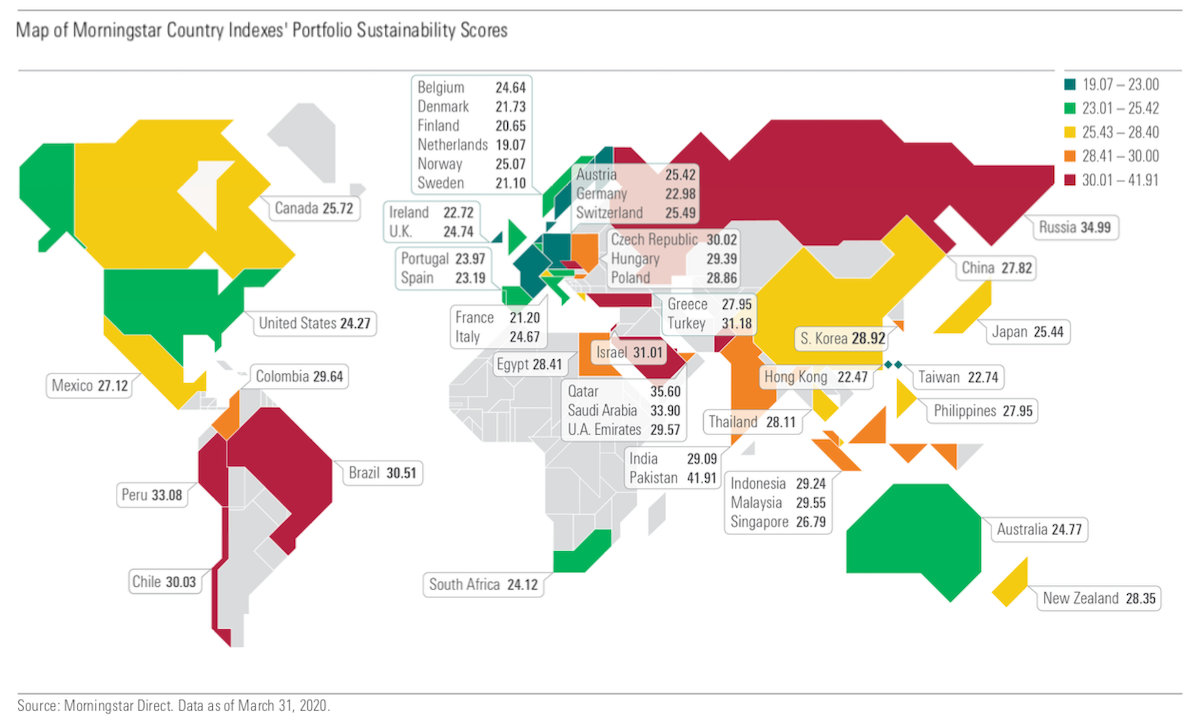

The Netherlands Topped the List for Strong ESG Practices; Emerging Markets Lagged

The Nordics and eurozone came out on top of sustainability rankings. Specifically, the Netherlands had the strongest overall score, followed by Finland and Sweden. Hong Kong was the world’s best-scoring non-European market for sustainability; Taiwan also landed in the first quintile in terms of sustainability.

On the other hand, several big Asian markets scored poorly on sustainability: Japan and China landed in the third quintile and South Korea in the fourth. And a group of Middle Eastern, Latin American, and Eastern European emerging markets, including Russia and Brazil, occupied the globe’s bottom quintile.

The full set of rankings is shown on the map below.

A few additional highlights include:

- The Netherlands ranked as the world’s most sustainable stock market. Holdings like information-services company Wolters Kluwer WTKWY and semiconductor-equipment producer ASML Holding ASML, the biggest constituent of the benchmark, fueled the score.

- Finland, former world champion of sustainability, ranked second. Its consistently strong score was owed to companies such as Nokia NOK, a leader within the global technology hardware industry.

- The United States ranked 13th out of 48. Companies like Microsoft MSFT and Visa V, leaders from a sustainability point of view, help the country’s score. On the other hand, big names such as Meta META faced high levels of ESG risk in the study.

- China fell right in the middle, with a ranking in the third quintile for overall score, based on the Morningstar ESG Risk Rating. Entertainment-software player NetEase NTES and education and technology enterprise TAL Education TAL showed low ESG risk exposure.

- Russia ranked second in terms of Morningstar ESG Managed Risk Score, which evaluates how well a country index manages the ESG risks that it is exposed to. But it owes the strong exposure of its domestic market to the energy sector, finishing third to last in the overall ranking.

- Italy ranked third on ESG Managed Risk but slipped to 15th place for overall Morningstar Portfolio Sustainability Score, owing the high exposure to material ESG issues involving key companies like Enel ESOCF and Eni EIPAF.

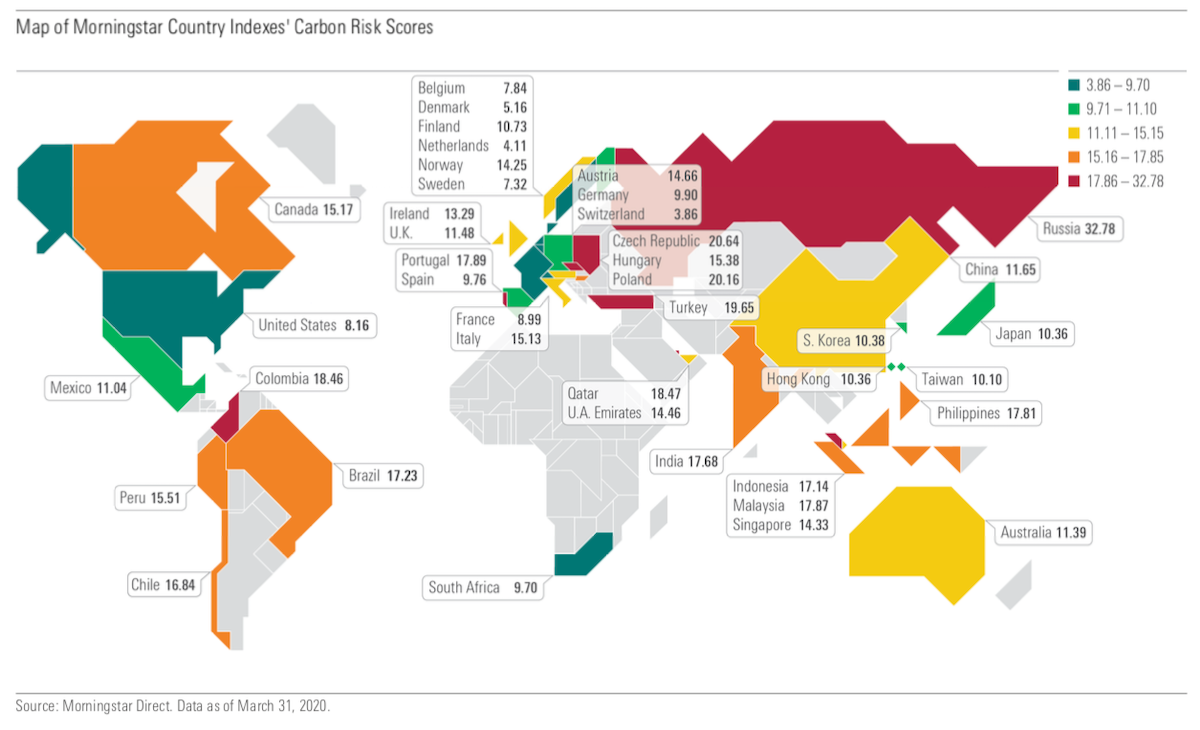

Do Countries With Strong ESG Practices Also Carry Low-Carbon Risk?

Western European markets like Switzerland, the Netherlands, Denmark, Sweden, Belgium, and France carried the lowest levels of carbon risk, as did South Africa and the United States. The full map of scores is shown below.

Despite being the world’s second-largest carbon emitter, the US has a low level of stock market value that is at risk from the transition to a low-carbon economy. This is because healthcare and technology companies represent more than 37% of US equity market cap and financials stocks account for almost 14%, while energy is around just 2.5%.

On the flip side is Russia, which holds nearly 55% of its market cap in energy stocks and consequently carries the world’s highest level of carbon risk.

The information, data, analyses and opinions presented herein do not constitute investment advice; are provided solely for informational purposes and therefore are not an offer to buy or sell a security; and are not warranted to be correct, complete or accurate. Past performance is not a guide to future results.

The opinions expressed are as of the date written and are subject to change without notice. Except as otherwise required by law, Morningstar shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information contained herein is the proprietary property of Morningstar and may not be reproduced, in whole or in part, or used in any manner, without the prior written consent of Morningstar.

Investment research is produced and issued by Morningstar, Inc. or subsidiaries of Morningstar, Inc. including, but not limited to, Morningstar Research Services LLC, registered with and governed by the U.S. Securities and Exchange Commission.