7 min read

US Housing Market: A Quarterly Update

As mortgage rates begin to cool down, it creates a ripple effect across the housing market.

Key Takeaways

Falling mortgage rates are providing a silver lining for the housing market, with the average 30-year fixed rate reaching its lowest level since October 2024.

Homebuilder sentiment increased in October.

Renter-occupied household growth has outpaced owner-occupied growth for eight consecutive quarters, continuing a trend spurred by affordability challenges and increased multifamily supply.

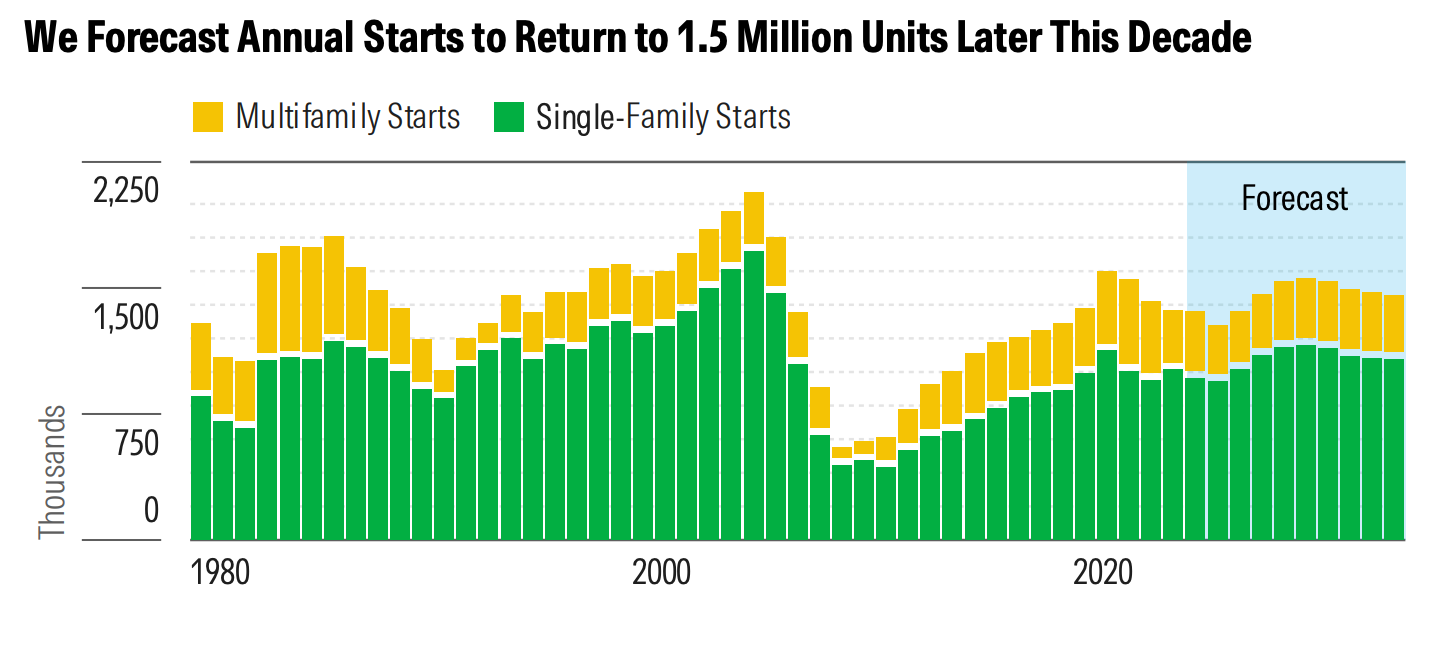

We expect single-family starts will rebound strongly from 2027 to 2029 as economic uncertainty fades and lower mortgage rates improve affordability.

Regional disparities are significant; major metros in the South and West face excess inventory and price declines, while the East Coast and Midwest have supply shortages and see moderate price appreciation.

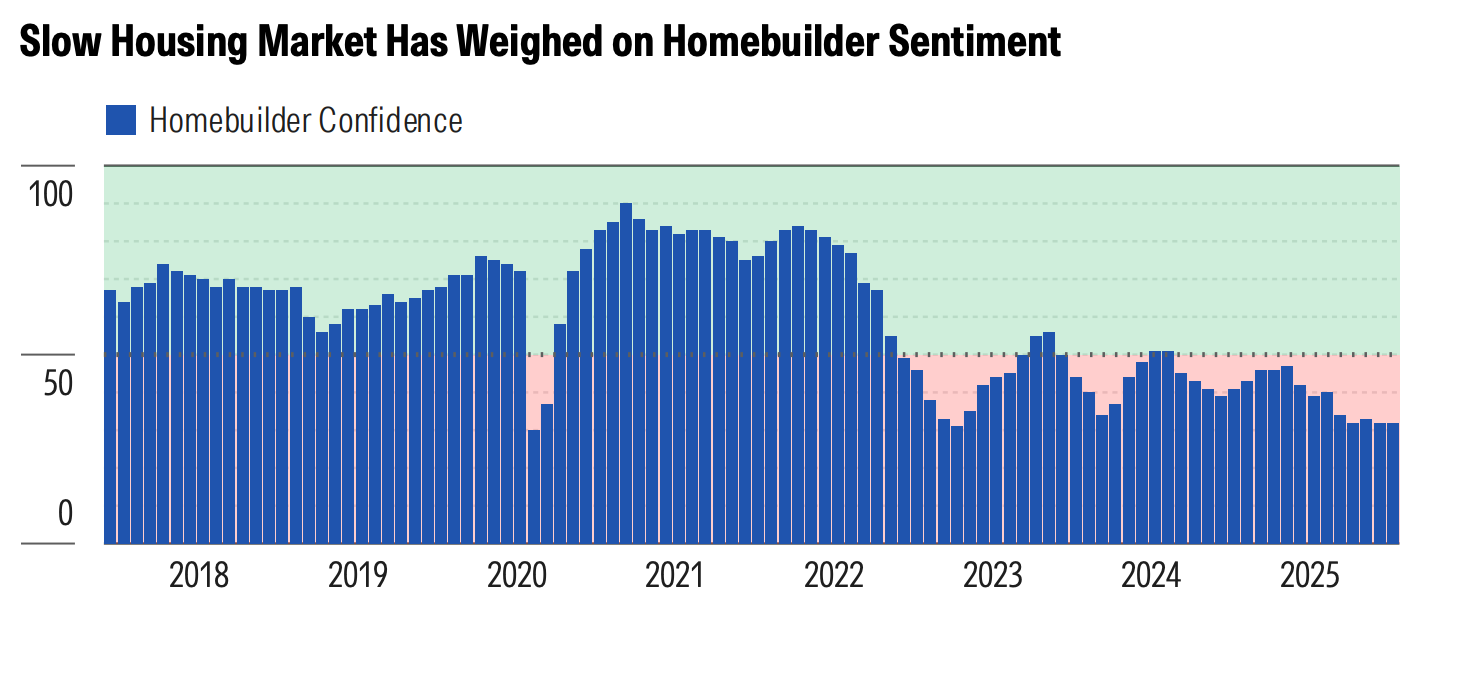

Homebuilder sentiment has shown notable shifts over the past year, according to The National Association of Home Builders/Wells Fargo Housing Market Index, a critical gauge of homebuilder sentiment.

The data shows that sentiment soured during the summer of 2024 as mortgage rates near 7% kept buyers on the sidelines. The index has yet to return to the neutral level of 50, with the October 2025 reading of 37 showing continued frustration with soft demand, especially in key Southern and Western markets.

Historically, however, homebuilder confidence has a strong negative correlation with mortgage rates. With the average 30-year fixed-rate mortgage trending lower since May and reaching below 6.30% in mid October, we think homebuilder confidence will improve if this trend continues.

Despite the challenging environment, many public homebuilders have maintained gross profit margins above prepandemic levels. This financial cushion allows them to use sales incentives to maintain a reasonable sales pace, a flexibility that smaller private builders may not share.

This article was adapted from the recently published report: US Housing Market Pulse: Q3 2025. Download it for free.

Homebuilder confidence ebbed and flowed over the past two years.

Renter Occupied Household Growth Continues to Outpace Owner-Occupied Growth

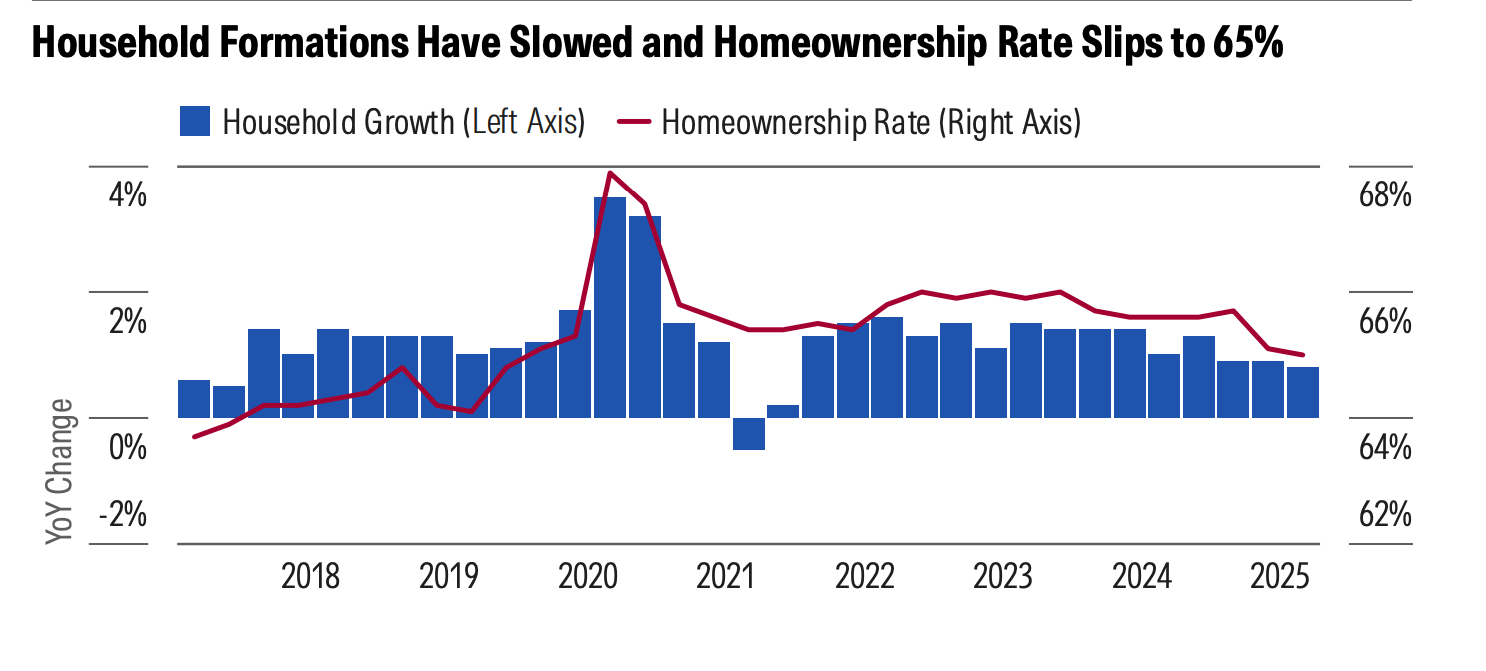

The number of occupied housing units in the United States increased roughly 1% so far in 2025, which equates to 1.2 million household formations this year. And most of these new households have been renters.

Data from the second quarter of 2025 shows that renter-occupied units grew 2.7% year over year, while owner-occupied units remained roughly flat. This marks the eighth straight quarter that renter growth has surpassed owner growth.

Considering challenging homeownership affordability and more supply of multifamily units entering the market as 2025 continues, we think renter-occupied growth will continue to outpace owner-occupied growth. This new supply has put downward pressure on the national median rent, making renting a more attractive option for many. Consequently, the national homeownership rate fell to 65.0% in the second quarter of 2025, down from a recent high of around 66% during 2021-24.

The 35–44-year-old cohort has seen the strongest homeownership rate gains since 2019.

Single-Family Home Construction May Briefly Decline Between 2025 and 2026

After a disappointing spring selling season, we expect single-family starts to decline approximately 5.0% in 2025. An elevated supply of unsold completed homes has made builders more cautious, and they are slowing the construction pace until stronger demand materializes.

New multifamily construction activity this year has been more robust than we had anticipated. We now expect multifamily starts to increase by 13% in 2025 but fall by roughly 16% as the market absorbs the outsized number of new units and slower economic growth discourages new development.

Looking further ahead, we project a strong rebound in residential construction between 2027 and 2029. As the US economy strengthens and lower mortgage rates improve affordability, we see a clear runway for greater homeownership rates among younger Americans. Over the next decade, we forecast an average of 1.5 million annual housing starts.

Despite challenges, we still see a runway for greater headship and homeownership rates among younger Americans, especially if mortgage rates ease as we expect.

How Tariffs and Construction Costs Are Affecting the Market

Construction cost inflation has eased significantly since the spikes seen in 2020-22. After a period of deflation in late 2023, modest low-single-digit inflation returned in 2024. While tariffs could raise construction costs by a low-single-digit percentage, homebuilders’ bottom lines have not yet been materially affected. Larger builders have the scale to negotiate with suppliers or find alternative sources if costs rise.

The Rate Lock-In Effect is Loosening Its Grip

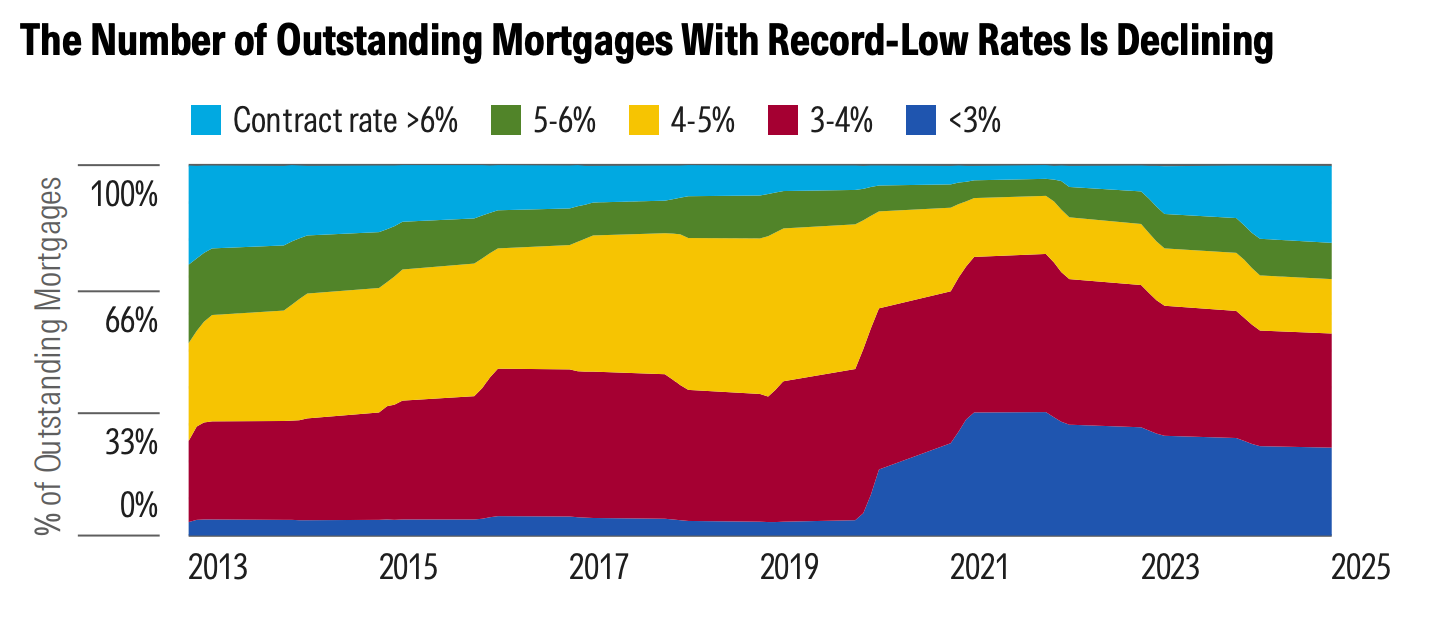

Morningstar forecasts the average 30-year mortgage rate to fall to 5.00% by 2028. Such a rate move should lessen the rate lock-in effect, resulting in more housing turnover (that is, existing home sales). According to the Federal Housing Finance Agency, 69% of outstanding mortgages still have a rate of 5% or less.

However, the percentage of outstanding mortgages with low rates sits below the peak levels seen in 2022, when 92% of outstanding mortgages had a rate of 5% or less. We expect the so-called “rate lock-in effect” will continue to loosen its grip on the US housing market as time passes, and if mortgage rates move lower as we expect.

For much of the past two years, homebuilders built more speculative homes (that is, building a home without a sales contract) to capitalize on a tight supply of existing for-sale homes. This strategy paid off for homebuilders, but broader adoption of spec building across the industry has caused the inventory of unsold completed homes to almost quadruple since the spring of 2022. We expect unsold inventory will gradually shrink throughout 2025 as homebuilders continue to offer sales incentives to maintain a steady sales pace while also starting construction on fewer spec homes.

We believe higher mortgage rates have been a major barrier preventing greater housing turnover. That’s because many homeowners are reluctant to sell homes financed with a low mortgage rate only to purchase a home with a much higher mortgage rate.

Affordability Remains a Key Headwind for the US Housing Market

The median sales price for existing homes increased 50% between 2019 and 2024, from $271,900 to $407,600, according to the National Association of Realtors. While affordability remains poor, there have been some signs of improvement. Median existing-home price appreciation has moderated this year, to approximately 2%, while nominal wage growth remains above 4%. Moreover, the average 30-year fixed rate mortgage has trended lower since May 2025, reaching below 6.30% in mid October, the lowest level since October 2024.

Homebuilders have used sales incentives, base price reductions, and smaller floor plans and lot sizes to make homes more affordable, and these actions have buoyed new-home sales. According to the National Association of Home Builders, the share of builders offering incentives (such as mortgage rate buydowns) in October was 65%, and 38% of homebuilders reported lowering base prices by 6% on average.

Top Housing Stock Picks, How to Proceed, and More Industry Coverage

As of mid October 2025, half of our housing-related stock coverage was undervalued.

Lennar (LEN): We believe the market isn't giving this homebuilder enough credit for its more capital-efficient, asset-light land strategy.

Fortune Brands Innovations (FBIN): We think the market is too pessimistic about this building products manufacturer's growth and margin prospects, even with potential tariff impacts.

RH (RH): We see long-term growth opportunities for this home goods retailer tied to its international expansion and a new brand launch set for 2026.

Invitation Homes (INVH): This residential REIT can create value by optimizing its portfolio of single-family rental homes, moving out of noncore markets and into higher-growth areas.

Weyerhaeuser (WY): We like this company's diverse exposure to wood products and its valuable timberland portfolio, which provides multiple revenue streams.

Additional topics covered include:

- Homebuilder data

- Consumer health and sentiment

- Repair and remodeling spending

During this period of economic uncertainty, it’s essential to remember that prospective homeowners and financial investors should still consider their long-term goals when making home purchases.

The author or authors do not own shares in any securities mentioned in this article.