Do Black Households Have More Wealth in the South?

Comparing the financial outcomes of Black households.

/s3.amazonaws.com/arc-authors/morningstar/ff370d56-5946-45e8-a1ea-5e50301bc997.jpg)

/s3.amazonaws.com/arc-authors/morningstar/e03cab4a-e7c3-42c6-b111-b1fc0cafc84d.jpg)

In recent research, we’ve discussed the status of finances in Hispanic households in the United States. Now we’d like to do the same for Black households.

On the surface, a major source of the growing racial wealth gap in the U.S. is straightforward: Many Black households continue to have less in savings and assets than white households. However, there is some important nuance under the surface worth examining.

First of all, despite millions of Black people leaving the South as part of the Great Migration, the South is still where most Black families live, and we found that it's offered them better financial outcomes in recent decades. This continues the work our behavioral research team conducted on how where you live affects savings based on our own analysis of PSID data.

Also, when we level the playing field by comparing Black and white families with similar levels of income, education, and location, among other factors, the differences in savings rates between Black and white households disappear and the disparities in retirement savings are reduced. This means that differences are not primarily because of race, but to disparities in social and economic circumstances which could be ameliorated through potential structural and policy changes.

Do Black Households Fare Better Financially in the South?

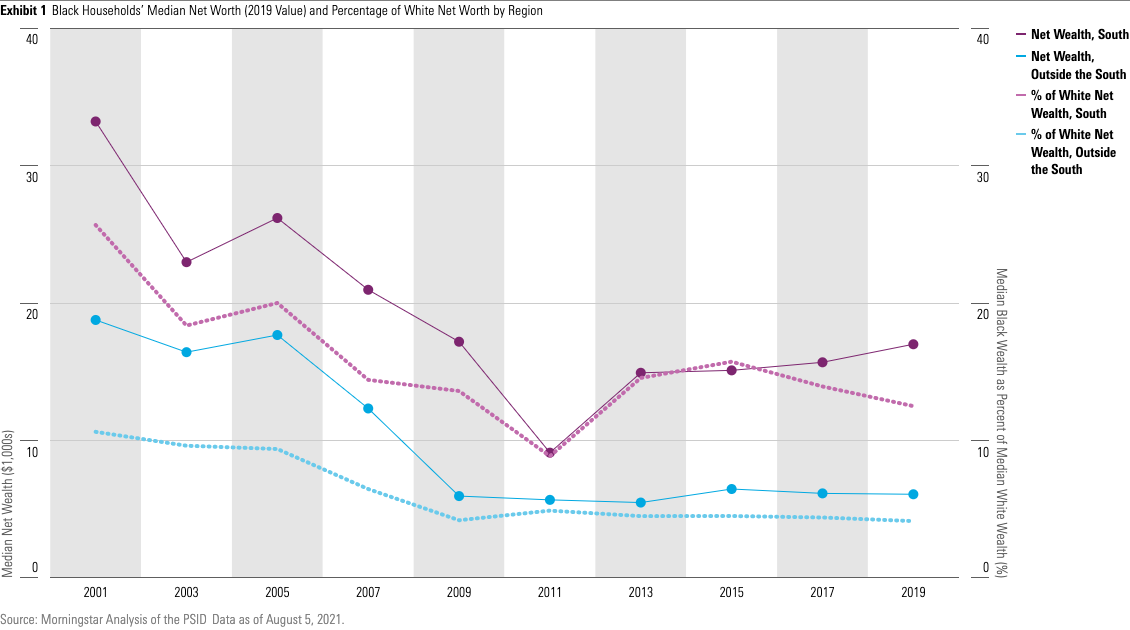

Across all U.S. households, wealth inequality is rapidly increasing, with a more concentrated impact on Black households. For example, the median Southern Black household saw its wealth decline from $33,000 in 2001 to consistently below $20,000 from 2009 to 2019 (Exhibit 1). Outside of the South, median Black households had about 50% less wealth during this period, starting with only $19,000 and dropping to under $6,000 through 2019.

Median white households also saw large drops in their net worth--especially outside of the South--but these drops were not as drastic as they were for Black households. As a result, the size of the racial wealth gap between median households grew.

At the start of this period, we estimate that the median Black household typically had about 25% of a median white household’s wealth in the South. However, this ratio dropped to 13% by 2019. The racial wealth gap was far greater outside the South since a median Black household had only 10% of a median white household’s wealth in 2001 to start with and this number declined further to only 4% by 2019.

Black Household Wealth Is Invested in Lower-Yield Assets

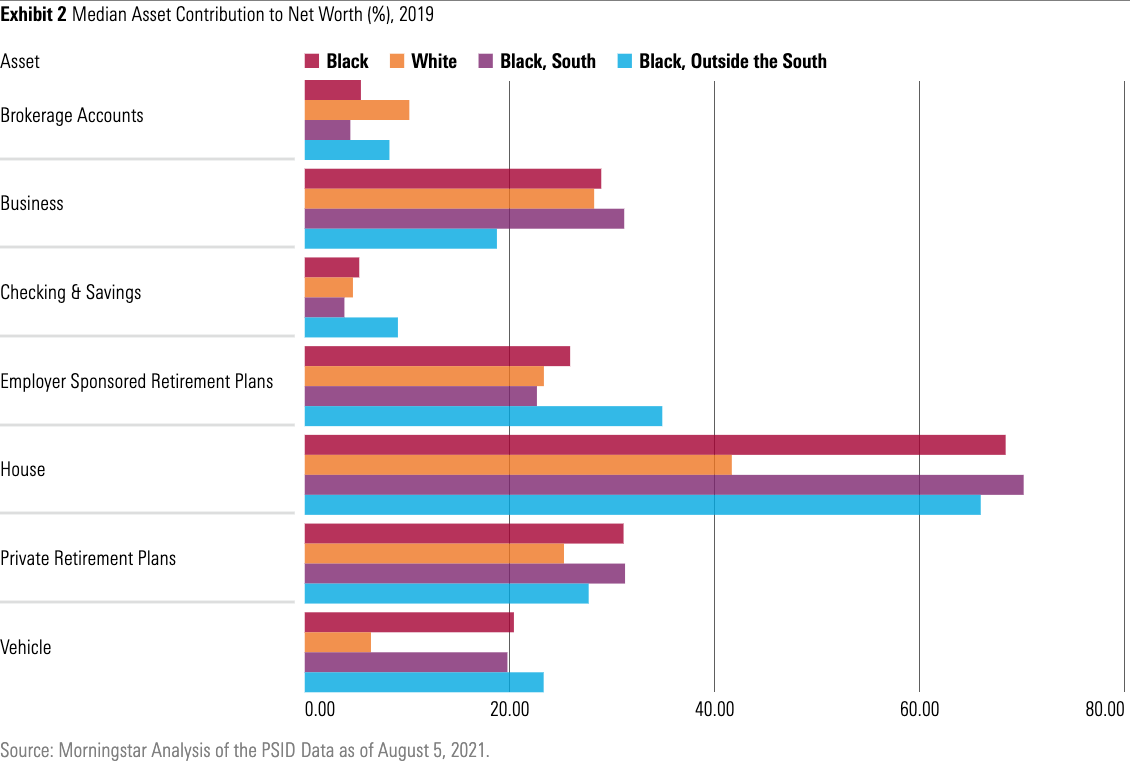

A general rule of building and maintaining wealth is that distributing it across multiple asset classes (for example, equities, bonds, valuable collections, and so on) can help reduce exposure to financial risk. However, Black household wealth seems more concentrated on low-yield assets, such as homes and automobiles, when compared with white households, who have more of their wealth placed in nonretirement brokerage accounts.

This trend is consistent with past research, which finds that lower-income households may be forced to focus on lower-yield assets out of necessity. While trends are similar by location, Southern Black households' wealth is slightly more focused on tangible assets, such as a house or business, while Black households outside of the South seem to have more wealth in workplace retirement and brokerage accounts.

Black Households Save Less, Including for Retirement

One factor that’s directly worsening the racial wealth gap is the racial savings gap, which has become consistently large over the past few decades.

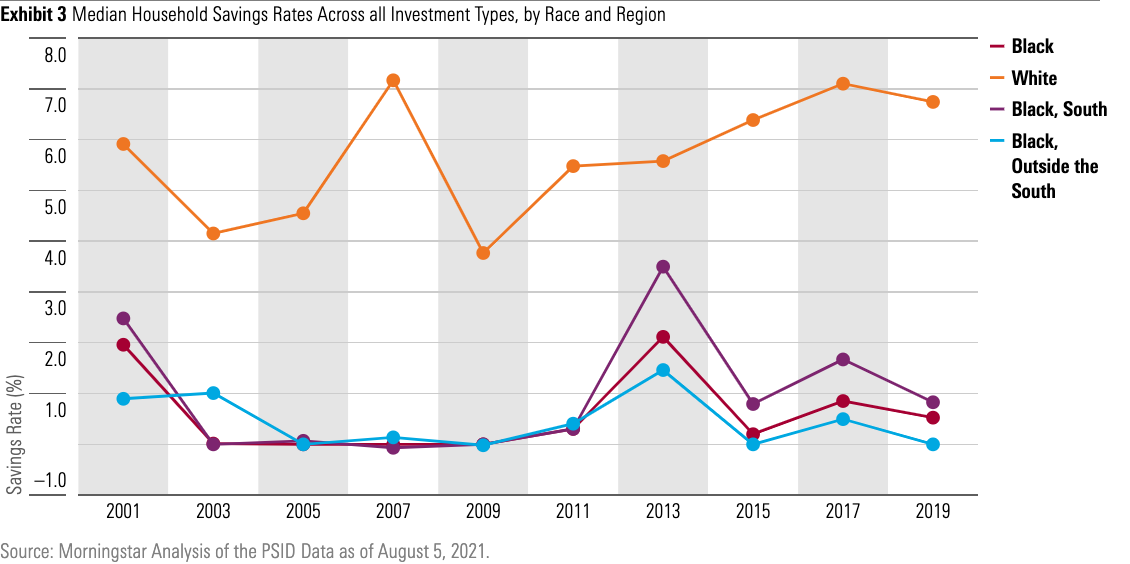

Exhibit 3 shows that the typical Black household only saved about 1%-2% of its income between 2001 and 2019, including several years where families were not able to save at all. Median white households, however, saved between 4% and 7% throughout this period. Median Black households outside the South generally saved similar proportions of their income to their Southern counterparts though in recent years their rates appear slightly lower.

Our research found that most Black households didn’t have a workplace retirement plan during the 2001-19 period. There was also a remarkable lack of growth in median assets in those plans, which rose only slightly from $16,600 in 2001 to $20,000 in 2019. Meanwhile, white households’ workplace retirement plan participation stayed stable and median assets doubled from $23,500 in 2001 to $55,700 in 2019.

Income and Education Boost Black Household Savings Rates

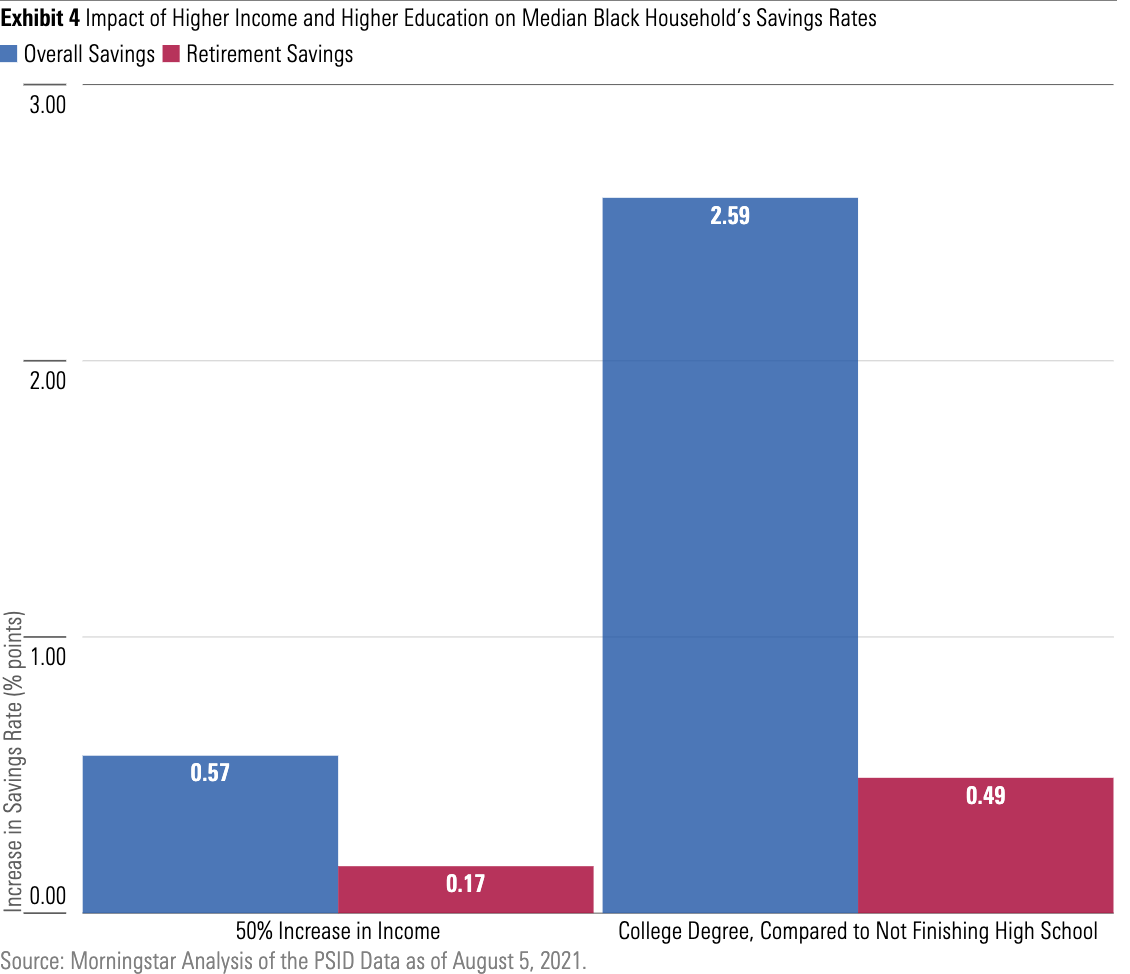

When we examine an array of factors that may contribute to Black households’ level of saving, income and education top the list. These factors have such a major impact that when we compare two median households--one Black and one white--that are practically similar otherwise, they save at the same rate.

Among median Black households, earning 50% more income is linked to a 0.6-percentage-point boost in their overall savings rate and a 0.2-percentage-point boost in retirement savings (Exhibit 4), even when we account for education and other factors. Southern Black households in particular show higher boosts to savings linked to higher income.

The boost education gives to savings rates is even stronger. When we compare two households that are otherwise similar on income and other factors, median Black households outside of the South led by a college graduate save at a rate that is significantly higher than those led by an adult who did not complete high school. For retirement savings, there is also a higher rate for median Black households outside of the South led by a college graduate compared with households led by an adult who did not finish high school.

Increasing Savings Is Key

Our results strongly suggest that improving Black households' access to higher income and education could boost their savings rates and thereby reduce the racial wealth gap. It would also be helpful for future research to reveal what aspects of the South allow median Black households to have better financial outcomes than other parts of the U.S. The fact that the South has larger proportions of Black residents, less urban racial segregation, and a lower cost of living offer a few important clues.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/NNGJ3G4COBBN5NSKSKMWOVYSMA.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/6BCTH5O2DVGYHBA4UDPCFNXA7M.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/EBTIDAIWWBBUZKXEEGCDYHQFDU.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ff370d56-5946-45e8-a1ea-5e50301bc997.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/e03cab4a-e7c3-42c6-b111-b1fc0cafc84d.jpg)