It's Not Either/Or: How Investors Meet Both Financial and DEI Objectives

Employer-managed plans can offer both high returns and an opportunity to support DEI.

/s3.amazonaws.com/arc-authors/morningstar/ff370d56-5946-45e8-a1ea-5e50301bc997.jpg)

Considering ongoing gender equality and racial justice movements, investors increasingly care about building wealth in ways that align with diversity, equity, and inclusion.

In line with broad motivations ranging from investing based on values to reducing risk, DEI investing is part of the trend of investing based on environmental, social, and governance factors, which has risen almost ten-fold since 2018.

Some investors even appear willing to select pro-ESG funds at the expense of some financial returns, though increasing evidence points out there is not necessarily a need to sacrifice one for the other. In fact, sustainable funds typically match or outperform non-ESG funds, as do companies with more-diverse staff and leadership teams.

Our research finds potential investors clearly favor meeting both financial and DEI goals when given the opportunity through their retirement plans (see the full report). Through experiments in two surveys, we asked potential investors to consider a scenario where they were new employees and needed to allocate their savings across 13 hypothetical funds in their company's retirement plan.

For each fund, we shared standard financial information used to make such decisions: historic five-year total return, expense ratio, and Morningstar Rating (or “star rating”). In addition, randomly selected participants were provided one other piece of information--either a diversity-related metric about the fund or fund asset manager or a less-relevant financial metric--to examine how their fund-allocation decisions may differ in response. For four of the funds, we informed participants that no net asset value or DEI was disclosed to test whether failure to share this information may also influence allocation decisions.

High Growth Funds With High DEI Scores--a Winning Combination

Participants in our first survey--a representative sample of U.S. adults--were randomly placed in four groups that all received standard financial information. The Standard Information control group received no additional information, while the NAV control group received additional NAV information in dollars--a less relevant financial metric that we implemented to tell us if any additional information might influence participants. The next two groups received diversity-related information as an integer ranging from 1=low to 5=high: The DEI group received a DEI score, and the Gender Equality group received a GE score.

We found that participants in the DEI or GE groups allocated 6.7 percentage points more and 7.3 percentage points more to funds with high DEI or GE scores, respectively, when compared with respondents’ selection of the same funds that were assigned high NAV scores in the NAV control group. This shows they were clearly motivated to allocate money based on diversity-related metrics.

In supporting funds with higher diversity-related scores, DEI and GE groups still achieved similar average historic five-year returns in their portfolios though were willing to accept slightly higher expense ratios (about 1 or 2 basis points) and a slightly lower star rating on average.

To achieve this balanced result, participants in the DEI and GE groups selected funds with high returns just as frequently as NAV group participants but were strategic in prioritizing funds that also had strong DEI or GE scores.

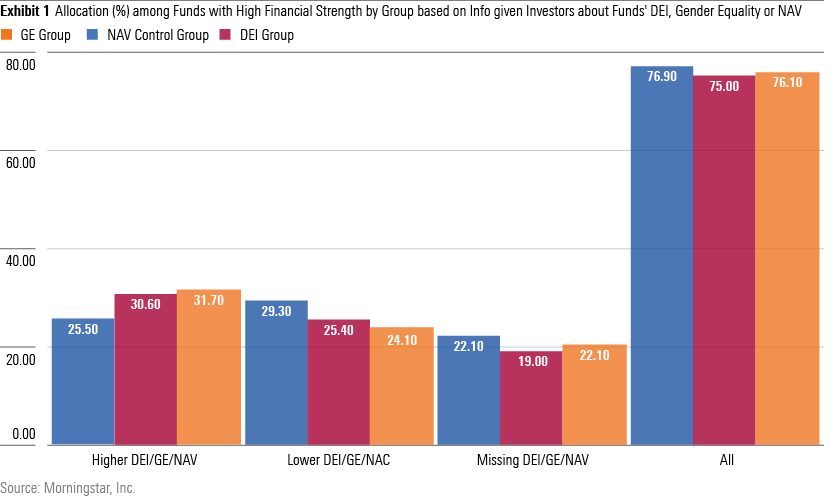

To illustrate, here is how participants across groups would allocate a $100,000 contribution based on our test results. We see that while, on average, participants in all three groups allot around three fourths of their money to high-performing funds, participants in the DEI and GE groups gave more to funds with both high returns and high DEI or GE scores--$5,000 more and $6,200 more, respectively--than NAV participants.

Correspondingly, DEI or GE group participants gave relatively less to high-performing funds with low DEI or GE scores, and DEI group participants even penalized funds with missing DEI information relative to their NAV participants.

High Growth Funds With High DEI Asset Managers--Another Winning Combination

The second survey for our research polled a sample of U.S. adults who have some investing experience and placed them randomly in two groups. Participants in the Standard Information control group received only standard financial information about the funds, while the DEI group participants also received a DEI score (an integer ranging from 1=low to 5=high) about the funds’ asset managers.

We see a strong influence of the DEI information presented to our potential investors-- those in the DEI group allocated 13.2 percentage points more to funds whose asset managers had high DEI scores than members of the control group who did not receive those scores. Markedly, this preference for DEI did not result in DEI group participants choosing funds with significantly lower average five-year returns, though they were willing to tolerate a slightly higher expense ratio (1.5 basis points) and a lower star rating (0.12 points).

DEI group participants were highly strategic in how they balanced their allocations to achieve strong historic returns and strong asset manager DEI scores since they still managed to select almost an identical proportion of high-performance funds as members of the control group.

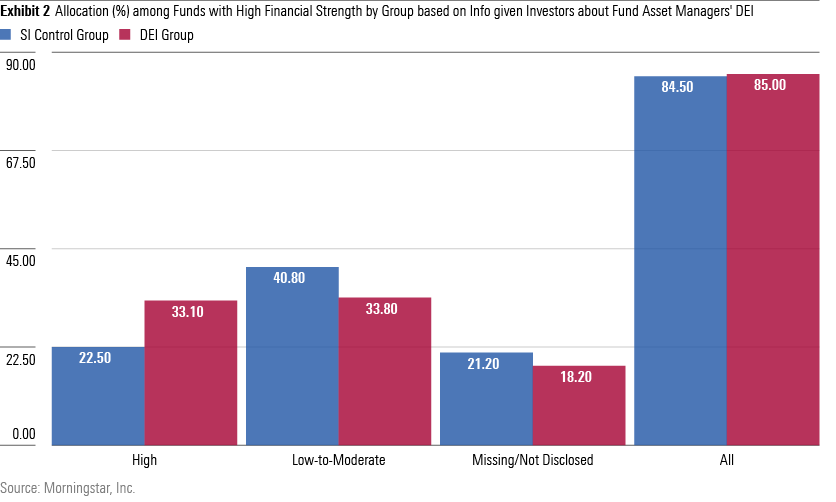

Exhibit 2 shows how they would allocate a $100,000 contribution based on our experiment's results. Both groups allocate about $85,000 to these outperformance funds, but participants in the DEI group gave $10,600 more to funds with both high returns and high asset manager DEI scores than control group participants. To accommodate their DEI support, DEI group participants gave $7,000 less to high-performing funds whose asset managers had low DEI score information.

Implications for Advisors and Asset Managers

So, for everyday retirement savers, could employer-managed plans serve as a path toward a secure financial future as well as an opportunity to support diversity, equity, and inclusion? Our results answer this question with a resounding “yes.”

Investors are savvy enough to pursue both their primary goal of securing their financial future and rewarding companies and asset managers who have strong track records on diversity-related metrics. They do so without limiting potential yields and with only minor sacrifices to their portfolio’s expense ratio and star ratings, while allocating less money to high-yield funds with only low-to-moderate diversity scores.

Advisors can differentiate themselves by providing DEI information to clients in a way that aligns with their fiduciary duty. All advisors incorporate returns and expenses into their advice to investors as primary considerations but have an opportunity to personalize options for clients who have clear preferences for DEI and are less interested in funds that do not support diversity initiatives.

There are also incentives for asset managers who have high levels of diversity that they can showcase to their clients--investors are far more willing to select their funds over the funds of competitors without strong DEI.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/RFJBWBYYTARXBNOTU6VL4VSE4Q.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/WYB37DY4NVDTVNZTSBDENH3GMI.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/JPJHXR5CGSNR4LKQF5ZKLCCVYQ.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ff370d56-5946-45e8-a1ea-5e50301bc997.jpg)