The Key to Personal Financial Planning: Being Lazy

There are benefits to following a simplified approach.

/s3.amazonaws.com/arc-authors/morningstar/e03cab4a-e7c3-42c6-b111-b1fc0cafc84d.jpg)

The problem: So many options overwhelm and overcomplicate personal financial plans.

Many of us want to improve our finances, but that’s much easier said than done. The truth is, it’s hard to make sense of all the tools, options, and information at our disposal.

If you’re feeling this same stress, you’re not alone. According to the American Psychological Association, most adults in the United States reported that money was a significant source of stress.

Furthermore, our research has shown that a lack of confidence in making financial decisions is a primary reason why investors hire financial advisors and keep them. Although helping investors build confidence in managing their money plays a big role in financial advisors’ value, this research speaks to the prevalence of money-related stress and lack of confidence.

To make matters worse, the financial industry can sometimes add fuel to the fire with the rate at which it introduces state-of-the-art financial products, shiny new tools, and novel investing opportunities. These tools offer investors new opportunities but are also often overwhelming.

What happens: Mistakes and avoidance.

So what happens when people are faced with monumental decisions with dizzying arrays of choices? There are a few possibilities.

Some people may excel and use these tools and options to create financial plans perfectly tailored to their circumstances. Others may fall into the trap of inertia, where they avoid the decision altogether. Another group of individuals may instead do “too much.”

Research has noted that some investors overtrade, leading to overall poor performance and lost returns. Some investors are also prone to overconfidence, which may prompt them to take part in financial opportunities that they do not have enough experience in and are bound to make mistakes.

What to do instead: Personal finance simplified.

Instead of jumping on every investing trend or obsessively watching personal finance videos, many individuals may benefit from “being lazy.”

Now, this is not a recommendation to disengage and leave your financial future to fate. Instead, it means designating a “too hard” pile, using handy rules of thumb, and automating wherever you can.

1. Too hard, don’t care. (THDC—let’s make this abbreviation a thing!)

This idea from Morningstar’s Christine Benz (inspired by the late Charlie Munger) is worth repeating. As Benz explains, she ignores investments, economic information, and even financial information that can be categorized as “too hard.” Her designation of “too hard” has grown to include not just items that are too complicated but also those that are too time-consuming or detailed or feature fleeting short-term fluctuations. For example, her current “too hard” pile includes individual stocks, frequent rebalancing, leveraged-type investments, short-term market forecasts, and short-term market news. Take the time to make your own list of any items that do not matter to you and your long-term financial goals. Then, actively ignore these things when they come about. This may require you to turn off news notifications or unfollow financial influencers who are constantly chasing the next get-rich-quick investing scheme.

2. Use rules of thumb.

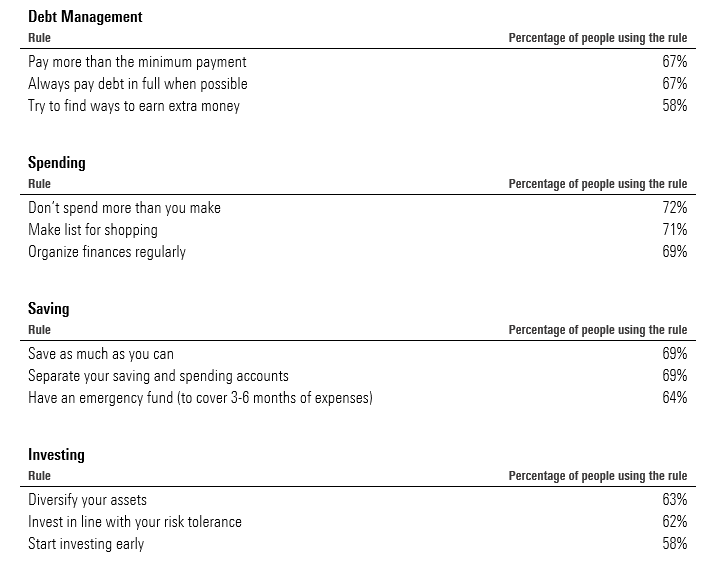

We’re all guilty of assuming that the more advanced (aka complicated) a concept, the better, but this isn’t always true. When it comes to personal finances, sometimes the simple rule of thumb may be better for you than a complicated model or multistep decision process. In past research, we looked at the correlation between common financial rules of thumb and financial well-being. Although we didn’t find that any one rule was more impactful than the rest, we did find strong positive relationships between a person’s habitual use of rules and financial well-being. In other words, find a sensible rule of thumb that you can stick to, then stick to it. For inspiration, here are the top rules that people followed, as reported in our data, separated by financial topic.

Top 3 Rules Per Topic, Based on Frequency of Use

3. When you can, automate the decision.

To make a decision as easy as possible, use technology to automate the process. Nowadays, most of us can set up automatic transfers on our bank apps to move money from our checking accounts to our savings accounts or automatic increases of our retirement contribution rates that correspond to our raises. This is the ultimate “lazy” way to personal finance because once you set up the automated process, the key is to not touch it.

Correction: In a previous version of this article, the exhibit included duplicate information. It has been replaced with a corrected version.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/WDFTRL6URNGHXPS3HJKPTTEHHU.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IFAOVZCBUJCJHLXW37DPSNOCHM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/JNGGL2QVKFA43PRVR44O6RYGEM.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/e03cab4a-e7c3-42c6-b111-b1fc0cafc84d.jpg)