The Impact of Race and Location on Savings Rates

Examining how race, residency, and place of birth impact financial outcomes.

/s3.amazonaws.com/arc-authors/morningstar/ff370d56-5946-45e8-a1ea-5e50301bc997.jpg)

Higher levels of saving can lead to financial security but, despite recent improvements linked to the coronavirus pandemic, most Americans still save far too little for retirement and emergencies. This lack of savings is even worse for many people of color due to the substantial racial wealth gap linked to savings inequality.

We previously discussed how where you live may predict how much you save. But what about differences in savings by race?

It may be obvious that total income and level of education impact savings rates for people of color. But our research shows that where people were born, raised, and live in the United States are also significant factors.

The Racial Savings Gap is in Northeastern Cities

At first glance, households living in urban areas--specifically those considered "Metropolitan Statistical Areas"--appear to save more than rural households. But we find the opposite is true when we compare urban households with rural households that have similar levels of income, education, age, household structure, and other factors. With these considerations, our research shows that the typical urban household saves at a rate that's 0.5 percentage points less the typical rural household.

The existence of a racial savings gap may come as a surprise because we don't see one nationwide or across urban areas as a whole. However, after taking a closer look at each U.S. Census region, we see a substantial gap in Northeastern urban areas, specifically.

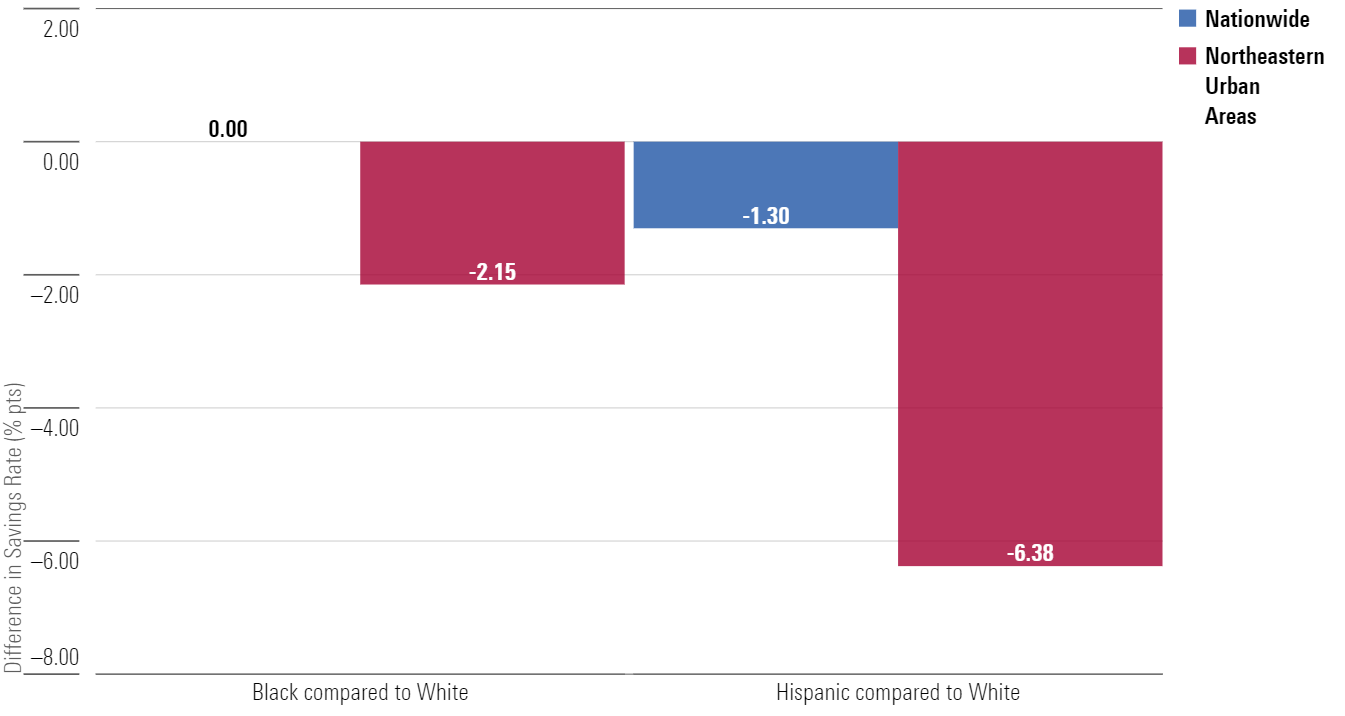

In the urban Northeast, the median Black household saves 2.2 percentage points less than the median white household (Exhibit 1). Across the U.S., median Hispanic households save 1.3 percentage points less than median white households. Examining this disparity further, we do not see a consistent gap across all urban areas but a tremendous gap within Northeastern cities of 6 percentage points (Exhibit 1).

Exhibit 1: Difference in Active Savings Rates (% pts) in Northeastern Urban Areas for Median Households, 1989-2019

Source: Morningstar Analysis of the PSID. Data as of Sept. 7, 2021.

These savings gaps in the urban Northeast are all the more striking considering that we don't see significant differences by race among median households within the other three Census regions. We can't say why this is happening; our data cannot confirm the cause of these disparities. But we suspect that the Northeast's high levels of racial and economic segregation, combined with its high cost of living, may be at play.

Immigrants Save More Than U.S.-Born Adults

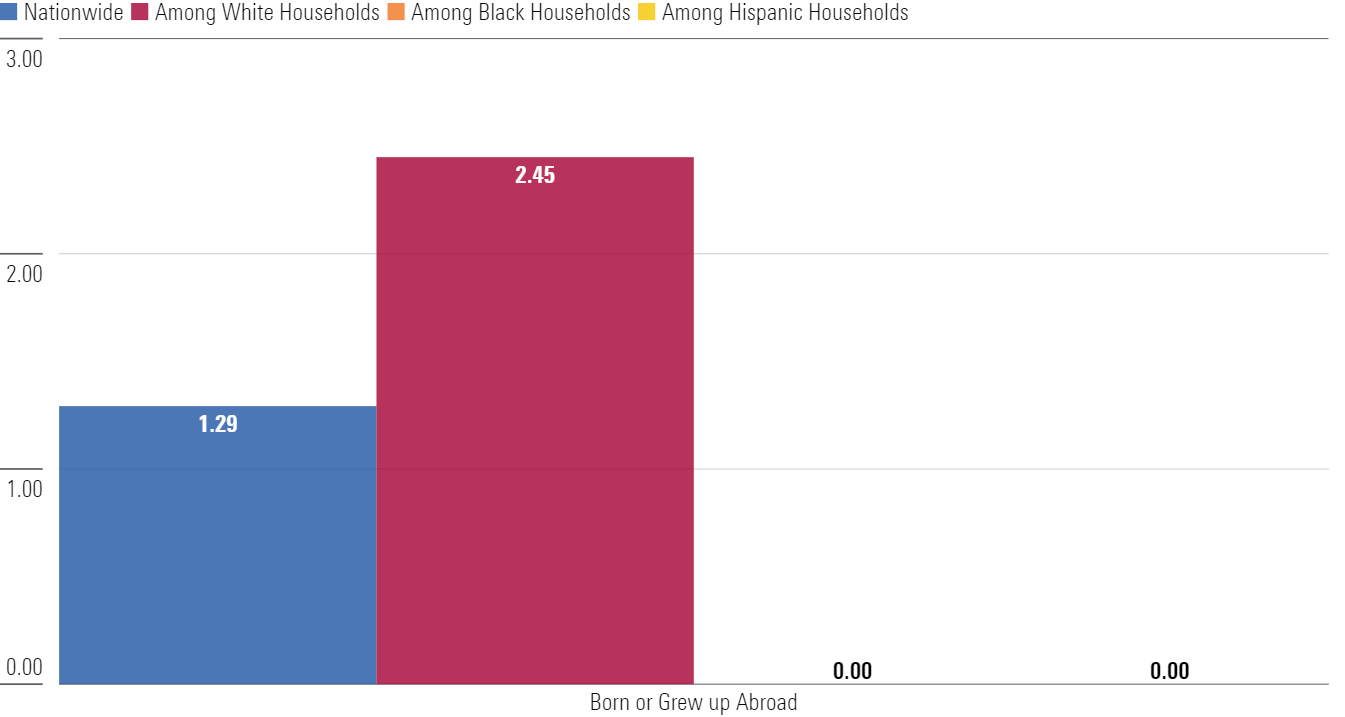

Across the U.S., median households led by adults born or raised outside of the U.S. save 1.3 percentage points more than similar households that are led by U.S.-born adults (Exhibit 2). However, a closer look at this result reveals that this immigrant savings advantage is mostly led by white households.

To be exact, the median white immigrant household saves 2.5 percentage points more than the median household led by U.S.-born adults. However, median Black and Hispanic immigrant households do not save at higher rates, making clear that the immigrant saving advantage does not extend to immigrants of color.

Exhibit 2: Difference in Active Savings Rates (% pts) for Immigrant Households compared to U.S. Born Households by Race, Median U.S. Households, 1989-2019

Source: Morningstar Analysis of the PSID. Data as of Sept. 7, 2021.

Income and Higher Education Can Boost Savings

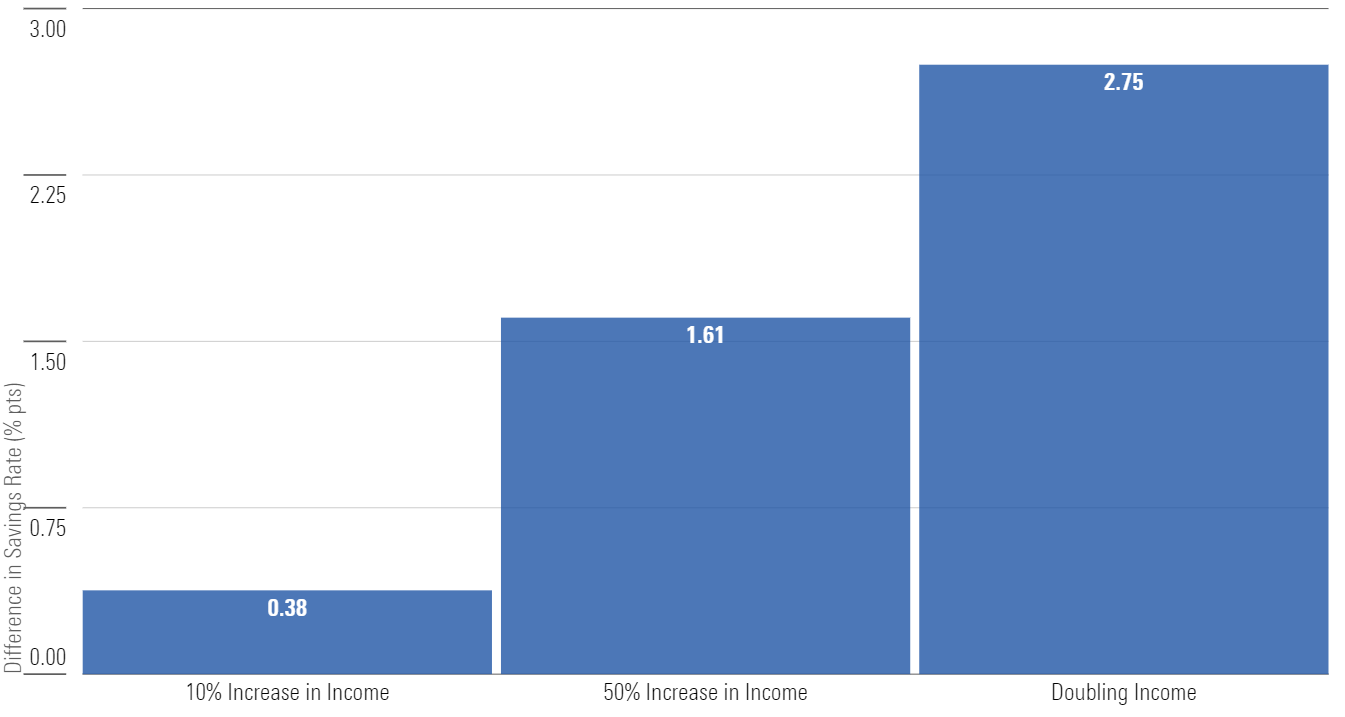

The most consistent finding of our research is that earning more income does not only increase the amount of income that a household saves, but significantly increases the rate at which it saves.

Overall, even when we compare households that are otherwise similar, we see that even a household with just a 10% higher income saves 0.4 percentage points more (Exhibit 3). As income increases 50% (from the median), the saving rate increases 1.6 percentage points and, as income doubles, savings increases 2.8 percentage points.

Simply put, having access to higher income appears to give families a better ability and confidence to save rather than spend disposable income. The fact that Black and Hispanic households have lower levels of income is a key factor driving disparities in savings and overall wealth.

Exhibit 3: Difference in Active Savings Rates (% pts) by Increase in Income, Median U.S. Households, 1989-2019

Source: Morningstar Analysis of the PSID. Data as of Sept. 7, 2021.

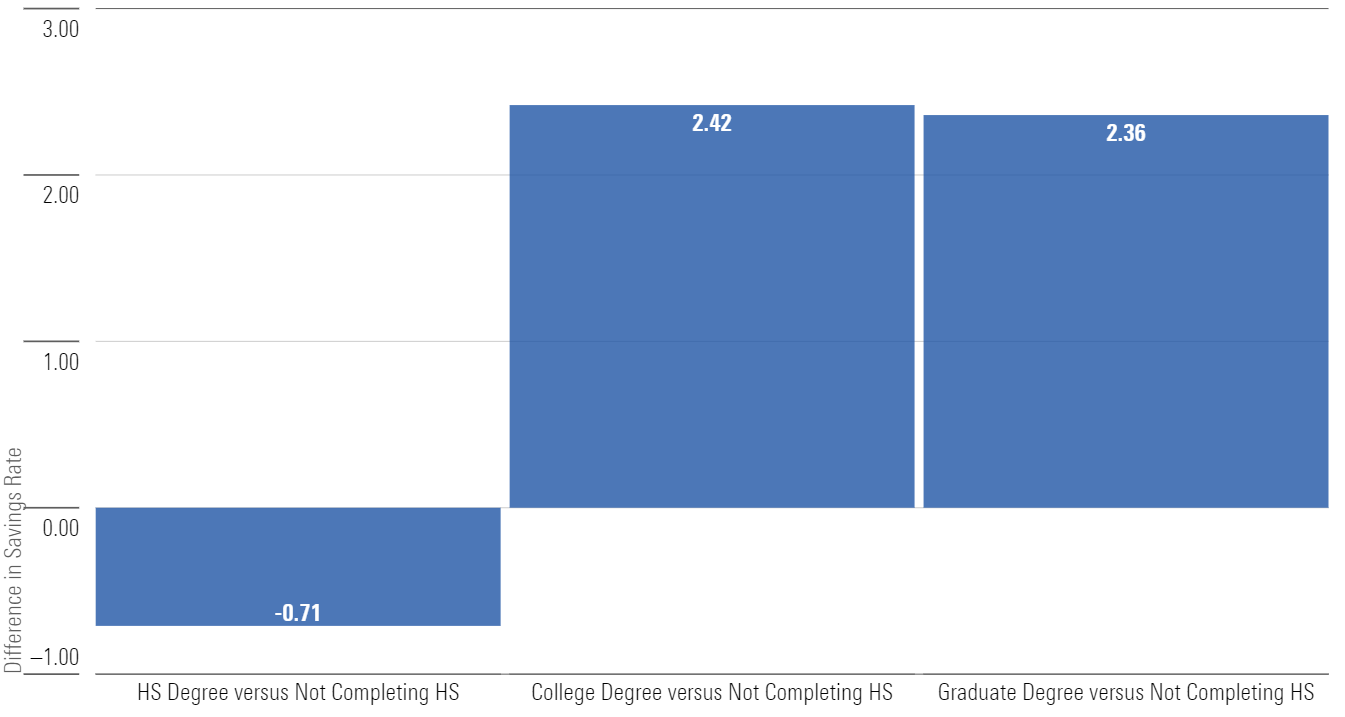

Higher education also plays a major role in higher savings rates. When we compare two similar households those led by adults with a college or graduate degree save 2.4 percentage points more than those led by adults who did not complete high school (Exhibit 4).

A surprising discovery was that median households led by an adult with a high school degree save 0.7 percentage points less than those without a high school degree where households earn the same income and are otherwise similar. However, the typical high school graduate earns substantially more than a non-graduate so, in balance, is likely to save more in total given the boost associated with higher income. While there is considerable discussion on the merits of financial education , our research shows that higher education more broadly is associated with higher levels of saving.

Exhibit 4: Difference in Active Savings Rates (% pts) by Level of Education of Head of Household, Median U.S. Households, 1989-2019

Source: Morningstar Analysis of the PSID. Data as of Sept. 7, 2021.

Supporting Diverse Families Toward Higher Earning, Learning, and Saving

Our research has clear implications for policymakers and financial advisors who want to help people secure their financial futures. To help reverse the rising tide of income inequality and racial disparities, it’s essential to enable lower-income earners to save.

Several policy proposals could help at the federal or state level: increasing the minimum wage, making higher child tax credits permanent, or introducing baby bonds. Employers can help by auto-enrolling workers into retirement and other savings plans, with smaller employers investigating ways to incorporate pooled employer retirement plans.

Our results also point to the importance of higher education for boosting savings since households led by college graduates save more than those led by non-college graduates, even when we account for income. This difference may be because of the education process itself, or other correlated outcomes such as people who complete a college education gain important soft skills and social networks that improve saving behavior. More could be done to shore up such financial acumen. Of course, promoting better financial literacy at earlier stages of education would serve as an important precursor.

Finally, even though immigrants are typically more entrepreneurial than people born in the U.S., we only see higher saving rates linked to typical white immigrants. Given that immigrants generally have low access to financial resources, advisors can play a crucial role in ensuring that non-white immigrants are better able to save and invest in business.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/KD4XZLC72BDERAS3VXD6QM5MUY.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/BZ4OD6RTORCJHCWPWXAQWZ7RQE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/JNGGL2QVKFA43PRVR44O6RYGEM.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ff370d56-5946-45e8-a1ea-5e50301bc997.jpg)