How Where You Live Impacts Savings Rates

Examining regional differences and similarities in savings rates across the U.S.

/s3.amazonaws.com/arc-authors/morningstar/ff370d56-5946-45e8-a1ea-5e50301bc997.jpg)

Where we live can affect our careers and lifestyles, but also how much we save for our financial future.

There are distinct differences in how American families save depending on where they live, according to research from behavioral researcher Steve Wendel and me. These differences, primarily focused on four regions and urban/rural areas, are further influenced by social and economic factors such as household makeup, race/ethnicity, income, education, age, nativity, and financial giving.

Our key focus is active savings--how members of a median household, those at the 50th percentile, directly save through putting a portion of their income into a bank account, investing in business or home renovations, or purchasing investments like brokerage stocks.

We primarily used data we processed for public use from the Panel Study of Income Dynamics.

Similar Saving Rates and Impact of Income and Education Across Regions

Despite the reputation certain regions may unfairly have attached to them, savings rates are very similar across all four regions when they’re placed on an equal playing field.

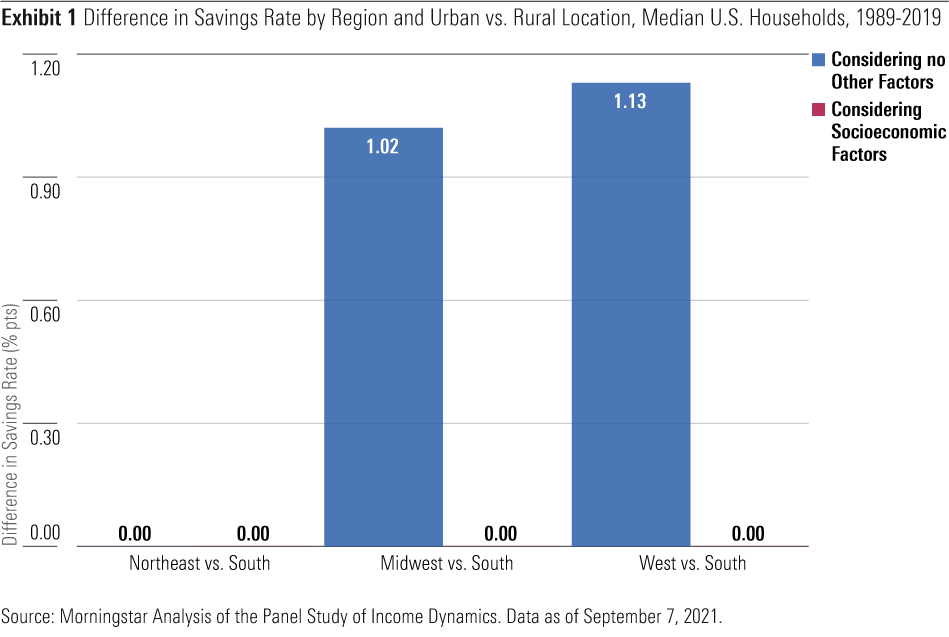

While Southern households appear to save less than those in Midwestern and Western regions, when we compare median households led by adults with similar income, education, and other characteristics mentioned earlier, they actually save at similar rates.

Income and education are the two most influential factors that affect household savings in the U.S. This is the case across the board as it remains true in each region. Even when all factors are considered, a household having 50% more income is associated with a higher savings rate of 1.6 percentage points across the United States and within each region.

We also found that households across the U.S. headed by college graduates save 2.4 percentage points more than households led by adults without a high school diploma. While the education advantage differs somewhat by region, in all cases we observe large gaps between the savings of median households where an adult has a college degree versus not.

Unique Regional Factors That Influence Savings Rates

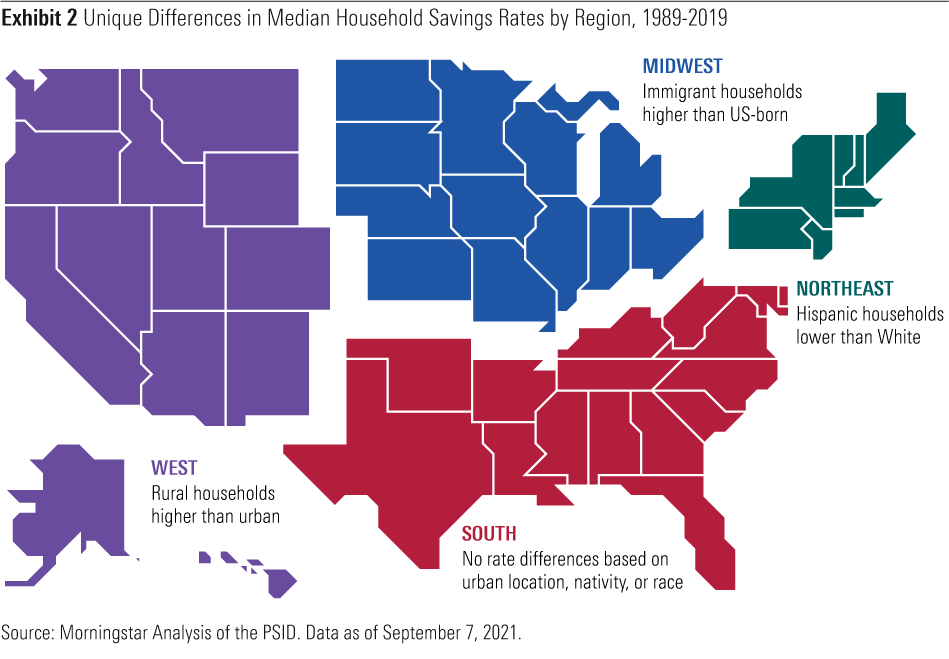

While we found consistencies across all regions, there are still unique differences between them that influence the typical household’s savings rate.

- source: Morningstar Analysts

In the Northeast, there is a large racial savings gap even when we control for household factors. Hispanic households save far less than white households--by 5.6 percentage points--and Black households also appear to save less. The overall savings rate gap in the U.S., and its impact on wealth inequality, appears to be driven largely by the Northeast since we do not notice such an influential difference by race in other regions.

Nativity, or where a person is born, stands out as a unique factor influencing savings rates in the Midwest since it is not similarly observed in other regions. Controlling for other factors, Midwestern households led by adults born or raised abroad save a remarkable 3.2 percentage points more than those households with adults born and raised in the U.S.

The factors that influence median household savings in the South appear very similar to the U.S. at large with no noteworthy differences based on race, nativity or urban location--factors that were each influential in one of the other regions.

Finally, the urban versus rural difference in savings rates is what appears to distinguish Western households from other regions. Urban households--those who live in a metropolitan statistical area--save 1.6 percentage points less than those in rural areas, accounting for other household characteristics. The large difference in the West is largely responsible for the 0.55-percentage-point rural-urban gap in savings rates nationwide.

Location-Based Saving Strategies

Tailoring solutions by location is important for advisors and policy makers as they help households meet their savings goals.

In the Northeast, it would be crucial to understand the unique challenges faced by Hispanic households attempting to save, given the large racial gap in savings. The high savings rate of immigrant communities in the Midwest is noteworthy given their increasing economic importance in this region, and these diverse and entrepreneurial new residents may need more investment support. Southern households save at equal rates to households in other regions, though more could be done to ensure their saving leads to higher levels of investment given the South's relatively high proportion of unbanked and underbanked households.

The fact that urban households in the West save significantly less than their rural counterparts suggests these households need better opportunities to save, which may be associated with their particularly high expense burdens. All households, and particularly urban Western households, could benefit from more access to public and employer-sponsored savings programs for retirement, as well as health, emergency, and commuter savings.

For advisors, our analysis of savings rates shares important insights about typical households by region, though it cannot replace the need to understand the unique situation of a particular client. That said, there may be less obvious but strong opportunities to encourage investment for households in the South and Midwest--areas with lower levels of income but higher rates of saving.

Additionally, as financial advisors assist clients who are considering a move, they would be wise to point out how living in a new state or city may affect a client’s ability to achieve financial goals.

You can read the full research on Morningstar Direct.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/WDFTRL6URNGHXPS3HJKPTTEHHU.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IFAOVZCBUJCJHLXW37DPSNOCHM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/JNGGL2QVKFA43PRVR44O6RYGEM.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ff370d56-5946-45e8-a1ea-5e50301bc997.jpg)