3 High-Quality Dividend-Payers Selling at a Discount

We highlight the cheapest stocks among the 14 new entrants to the Morningstar Dividend Yield Focus Index.

/s3.amazonaws.com/arc-authors/morningstar/3a6abec7-a233-42a7-bcb0-b2efd54d751d.jpg)

Note: This article is part of Morningstar's Guide to Dividend and Income Investing special report.

It's never a good idea to buy a stock without considering multiple valuation metrics and understanding how the business works. But it can be particularly perilous to buy a stock with a very high yield without investigating how safe that dividend is.

A company's dividend yield is the total of dividends paid in a calendar year divided by the company's share price. If the share price is plummeting--which would mean denominator of the fraction is decreasing--there will be a higher dividend yield than if the stock were trading at a higher price. This is not always a sustainable situation. It could indicate that the company is in financial trouble and a dividend cut is on the horizon.

The Morningstar Dividend Yield Focus Index can help investors find high-yielding stocks of companies that are financially healthy enough to sustain and even grow their dividend. (In contrast to most other dividend indexes that use only backward-looking criteria, the Dividend Yield Focus also considers qualitative forward-looking measures.)

To find the constituents in the Dividend Yield Focus, we first screen the Morningstar US Market Index--a broad market index targeting 97% of the overall market capitalization--for the highest-yielding companies. (The dividend must come from qualified income, so real estate investment trusts are not included.) We also apply quality screens: We search the high-yielders for companies that have a Morningstar Economic Moat Rating of wide or narrow, meaning we think they have competitive advantages that will allow them to continue to earn above-average profits and sustain their dividends for 20 or 10 years, respectively. We also consider a company's distance to default ratio, which is a proprietary metric that uses market information and accounting data to determine how likely a firm is to default on its liabilities.

The 75 highest-yielding stocks that make it through the quality screen are then included in the index. The index is dividend dollar-weighted (constituents are weighted according to the total dividends paid by the company to investors). You can see the current holdings here.

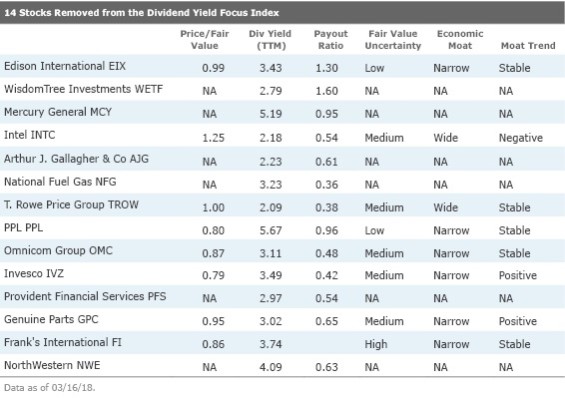

New Dividend-Payers in the Index In the table below, we show the 14 newest entrants to the Dividend Yield Focus Index, which pass our strict requirements for high yields, sustainable competitive advantages, and financial health. (Note that the dividend yields listed below are backward-looking and could change.)

On a price/fair value basis, McDonald's, Eli Lilly, and Hershey currently look undervalued relative to our analysts' fair value estimates.

Nonexistent switching costs, intense industry competition, and low barriers to entry make it challenging for restaurant operators to develop an economic moat. Although McDonald's has faced many headwinds, consumer sector strategist R.J. Hottovy believes it still possesses a wide moat. The moat rating is based on a mix of structural and intangible competitive advantages, including a widely recognized brand, a franchisee system aligned on driving unit-level productivity improvements, and meaningful economies of scale. The shares are currently undervalued at a price/fair value ratio of 0.85, and Hottovy notes that he doesn't "see many downside catalysts, with new sales levers becoming greater contributors and cash return levels set to accelerate."

Eli Lilly's innovative culture and strong financial commitment to developing the next generation of drugs set the company apart from its peers and fuel its long-term growth, says healthcare sector director Damien Conover. Following a very steep patent cliff in 2014, Lilly's growth prospects are improving as the company is launching several new blockbusters and patent losses are fading, he said. In Conover's view, patents, economies of scale, and a powerful distribution network support Eli Lilly's wide moat. The shares are currently trading at a 14% discount to our $94 fair value estimate.

Hershey's solid brand intangible assets and cost advantage warrant a wide economic moat, says consumer sector director Erin Lash. Hershey operates as a leading player in the confectionery space, expanding its market share over the past five years to around 45% of the U.S. chocolate industry, with its top five brands generating more than $5 billion in annual sales (about two thirds of its consolidated total), including Reese's ($1.9 billion), Hershey's ($1.5 billion), Kit Kat ($700 million), Ice Breakers ($475 million), and Kisses ($460 million). With the stock selling at a 14% discount to our $118 fair value estimate, we see this as an opportunity for investors to add wide-moat Hershey to their basket.

Five stocks--WisdomTree Investments WETF,

The other nine companies on the list were removed because their distance to default ratios crept into a range that we weren't comfortable with.

Distance to default is another other safety-oriented metric that we use to build the index. True to its name, it's focused on financial health. Distance to default uses option-pricing theory to measure whether a firm is falling into financial distress. It's gauging whether the value of a company's assets will fall below the sum of its liabilities. If a company is in distress, the dividend is at risk and there's trouble ahead. So, like moat, distance to default is another important screen for this index. (Read more about distance to default here.)

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click here for a list of investable products that track or have tracked a Morningstar index. Neither Morningstar, Inc. nor its investment management division markets, sells, or makes any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/YTLLJ3VT4NFZTCTDNZPCUR27D4.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/347BSP2KJNBCLKVD7DGXSFLDLU.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/KD4XZLC72BDERAS3VXD6QM5MUY.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/3a6abec7-a233-42a7-bcb0-b2efd54d751d.jpg)