How Much in Taxes Is Taken Out of Your Paycheck?

Where does the money go, and what is it used for?

/s3.amazonaws.com/arc-authors/morningstar/96c6c90b-a081-4567-8cc7-ba1a8af090d1.jpg)

/s3.amazonaws.com/arc-authors/morningstar/3a6abec7-a233-42a7-bcb0-b2efd54d751d.jpg)

If you’re making money, chances are you’ll have to pay taxes on it. In fact, Uncle Sam takes a decent-sized chunk of your paycheck before it even hits your bank account. Before you sign a lease or nail down your budget, you’ll need to figure out your “take-home pay,” or the amount of your hard-earned money that will actually end up in your pocket.

In this article, we’ll answer two questions: How much can you expect to pay in taxes, and just what is that tax money used for?

What Is Your Take-Home Pay After Taxes?

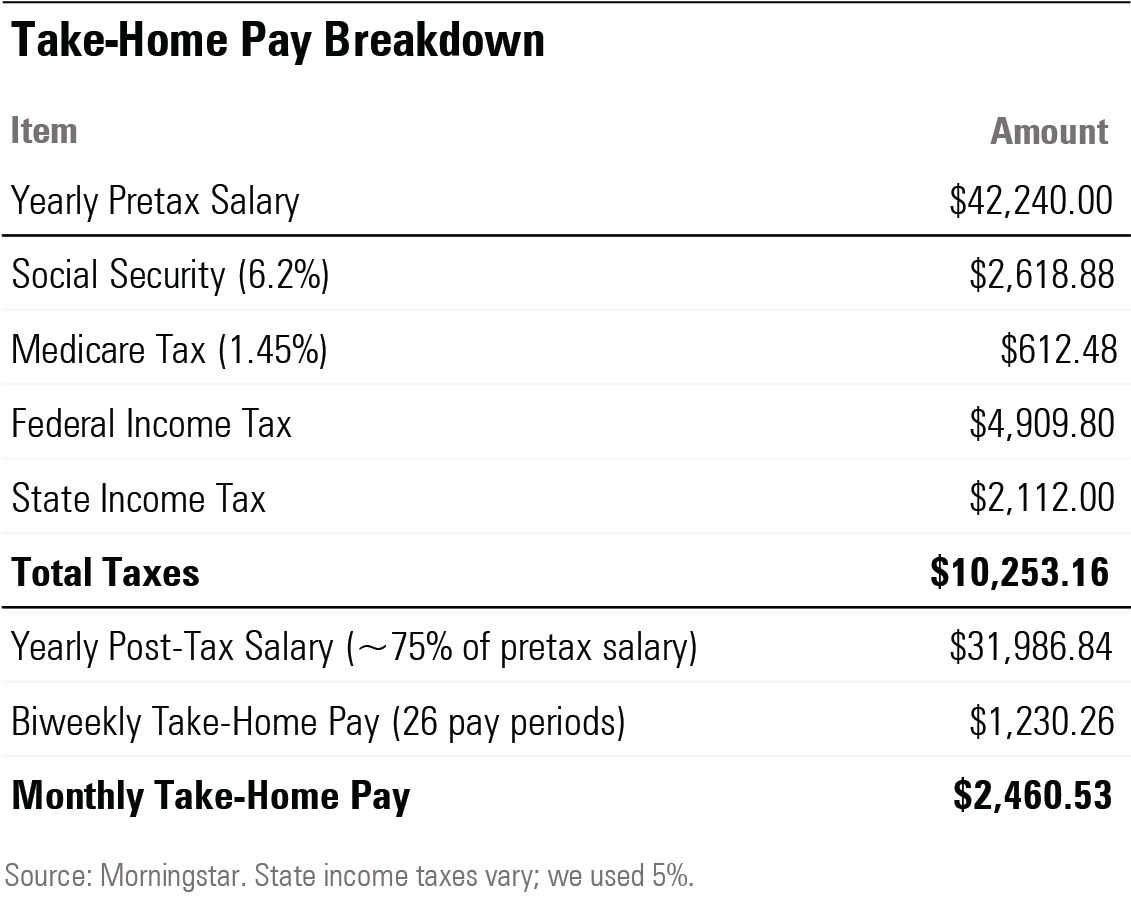

Let’s say you got a new job that pays $22/hour. Assuming you work 40 hours per week, that works out to $880 per week, $3,520 per month, and $42,240 per year—before taxes. How much of that can you expect to take home after taxes?

Take-Home Pay Breakdown

Where Do the Taxes Taken From Your Paycheck Go?

Federal income tax is the government’s biggest source of revenue. It is used to pay the country’s ongoing expenses, such as national defense, infrastructure needs, social assistance programs, and paying interest on the national debt.

Many people are surprised to learn that all of the income you make is not taxed at one rate. Let’s say you are the single filer in the example above, earning $42,240 per year. Your income falls into the 22% tax bracket. But, if you paid a flat 22% tax rate, you’d owe $9,293. Yikes. What gives?

Federal income taxes are paid in tiers. For a single filer, the first $10,275 you earn is taxed at 10%. The next $31,500 you earn—the amount from $10,276 to $41,775—is taxed at 15%. Only the very last $465 you earned would be taxed at the 22% rate. This IRS Tax Table can help you figure out how much federal income tax you owe. Keep in mind that your tax bracket also depends on your filing status.

Morningstar’s Christine Benz breaks down important tax dates and federal tax information, including the federal income tax brackets that tell you how much in federal taxes you will owe based on your income in the 2023 tax year.

What Is FICA?

Social Security and Medicare withholding are also known as FICA, the Federal Insurance Contributions Act. You pay 6.2% of your salary up to the Social Security wage cap, which is $160,000 for 2023, and 1.45% in taxes for Medicare (note that there is no wage cap for Medicare tax). When you work for a corporation, these FICA taxes are matched by your employer, for a total tax paid of 12.4% of salary up to the Social Security wage cap and 2.9% Medicare tax. When you’re self-employed, you pay both halves yourself. Also, if your yearly salary is $200,000 or more, you will have to pay an additional 0.9% in Medicare tax.

Social Security is a U.S. government program that provides federal aid to Americans. It includes many federal aid programs: unemployment assistance, disability assistance, Medicaid, and so on. One of the largest Social Security programs is retirement benefits. For many Americans, retirement benefits are a crucial piece of their retirement income.

Eligibility for retirement assistance through Social Security involves accumulating 40 Social Security Credits. Because four credits can be earned in most every year, Americans will need to work for at least 10 years to be eligible. Social Security benefits include survivor benefits. If the immediate beneficiary passes away, eligible family members may receive the benefits in their place.

Medicare is the federal health insurance program for people who are 65 or older. Though Medicare benefits likely will not cover every medical service and prescription a person may need, this taxpayer-subsidized program helps people manage medical costs as they age.

Editor’s note: A version of this article was published on June 22, 2021.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/KD4XZLC72BDERAS3VXD6QM5MUY.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/BZ4OD6RTORCJHCWPWXAQWZ7RQE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/JNGGL2QVKFA43PRVR44O6RYGEM.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/96c6c90b-a081-4567-8cc7-ba1a8af090d1.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/3a6abec7-a233-42a7-bcb0-b2efd54d751d.jpg)