Q2 2021 Market Performance in 7 Charts

Bond markets recover and stocks post broad gains.

/s3.amazonaws.com/arc-authors/morningstar/8b2e267c-9b75-4539-a610-dd2b6ed6064a.jpg)

As the global economy moved in fits and starts toward a recovery, global stock and bond markets posted broad gains in the second quarter.

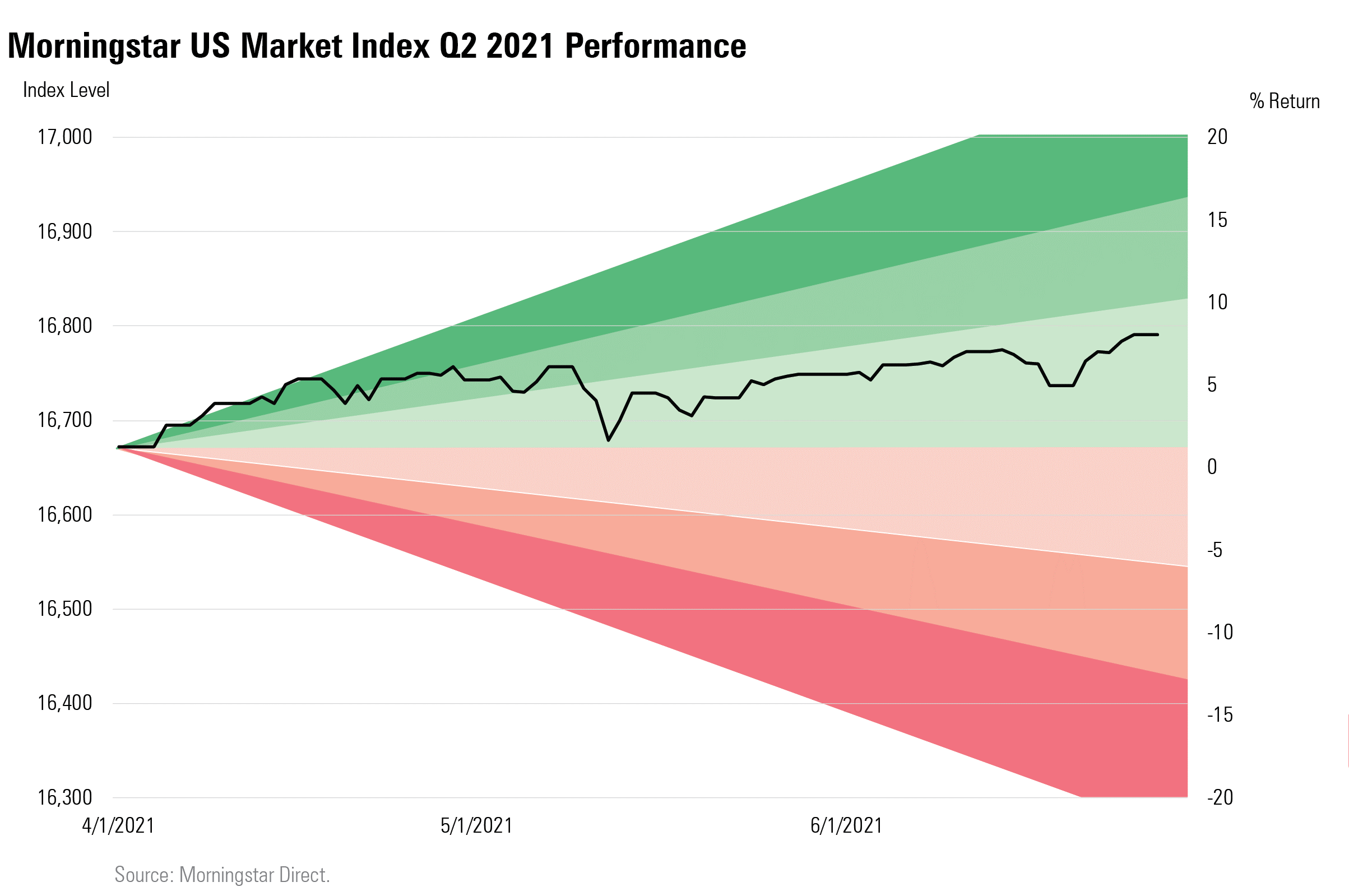

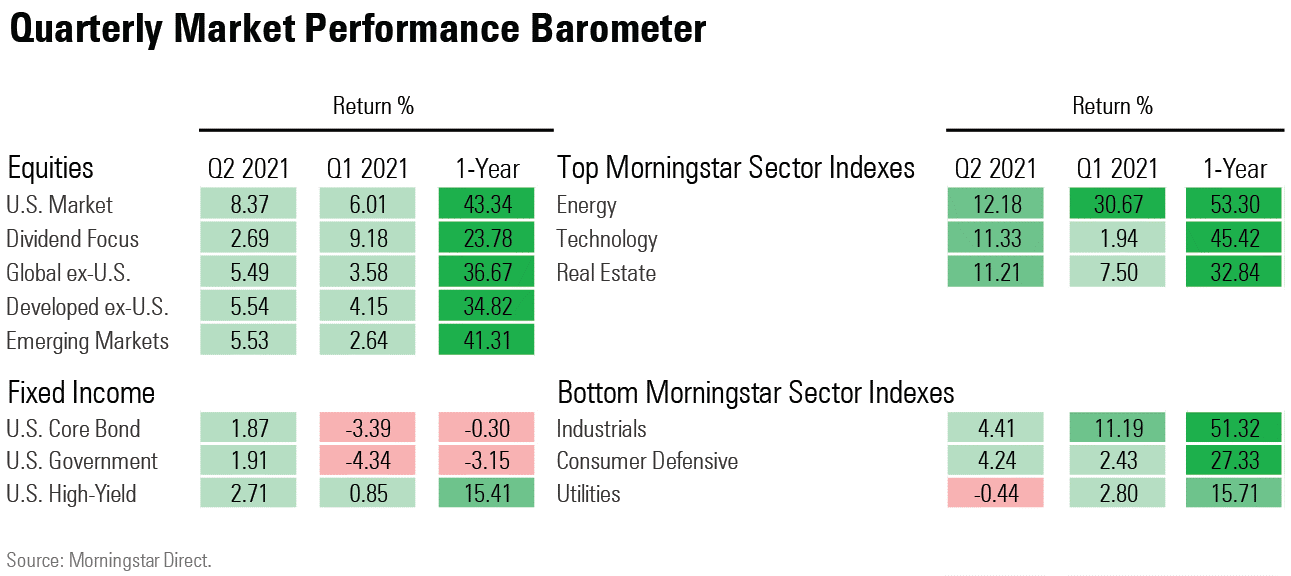

- The Morningstar U.S. Market Index ended the second quarter up 8.4%, adding to a 6% return posted in the first quarter. The index hit a new record high on the last day of the quarter and has gained 43% from a year ago.

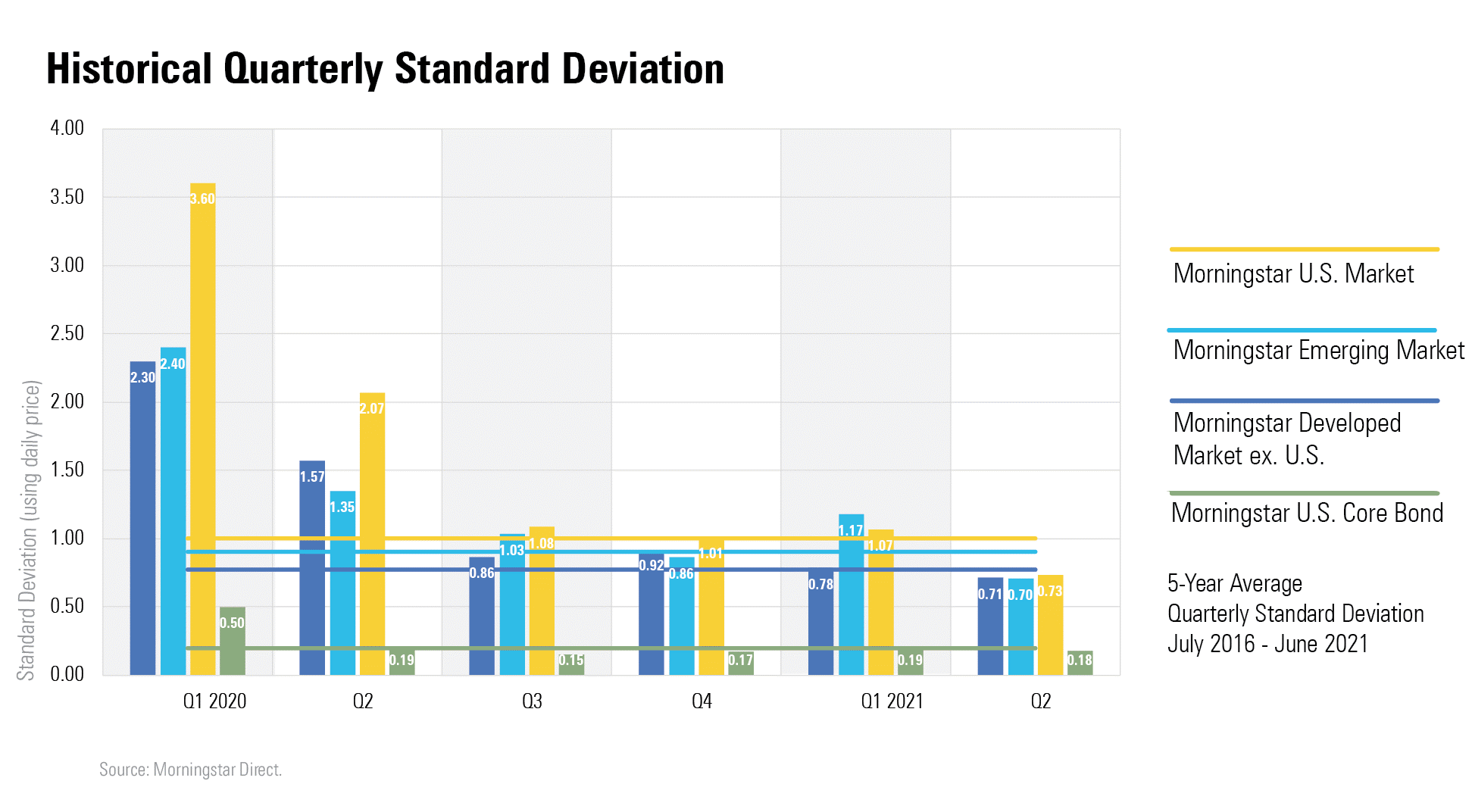

- Volatility across equity markets fell to pre-pandemic levels.

- International stocks continue to lag the U.S. market, with China a drag on returns.

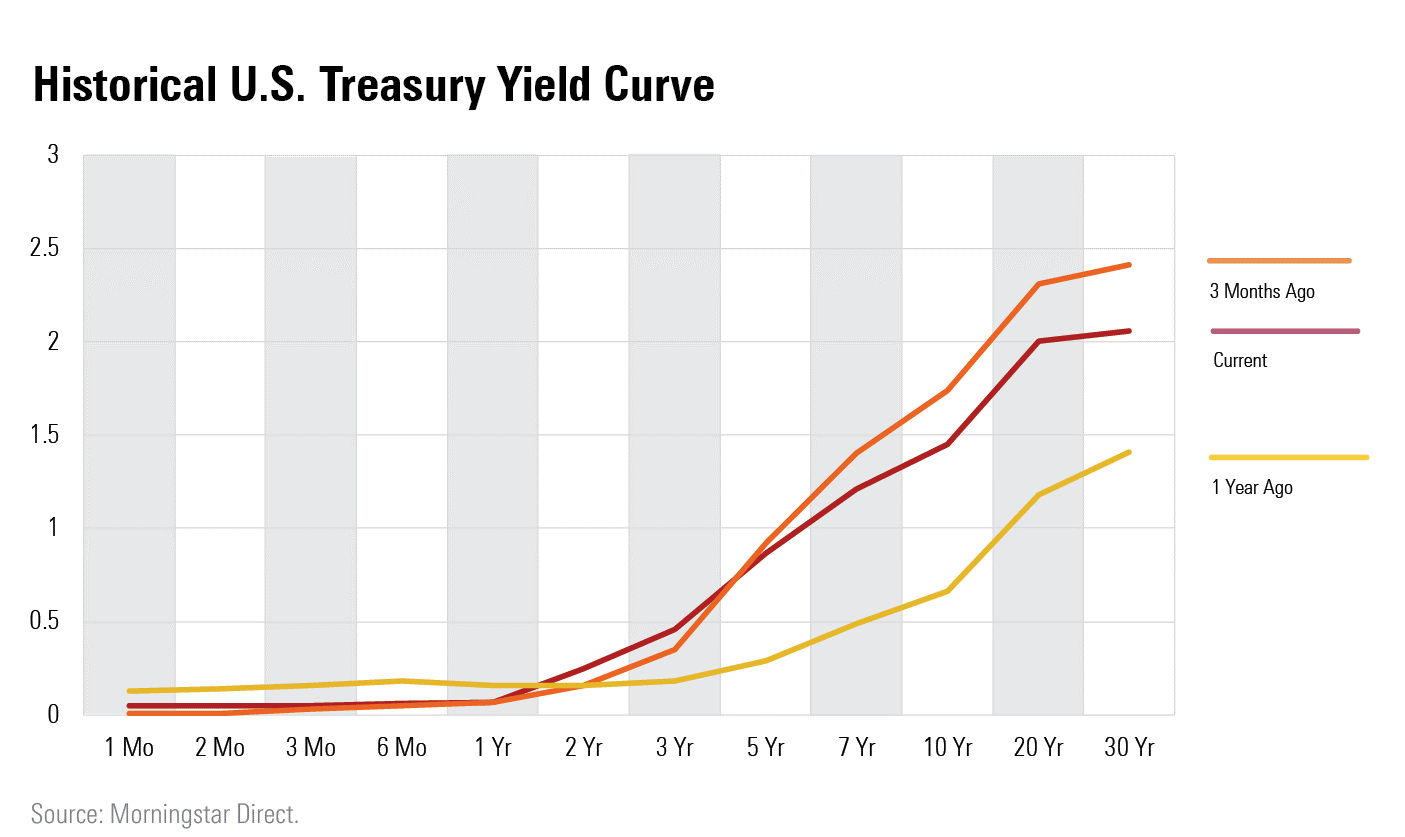

- After the Federal Reserve signaled it was on watch for inflation pressures, bonds mostly recovered from a rough first quarter. The Treasury 10-year yield fell 29 basis points from its high in March to 1.45%.

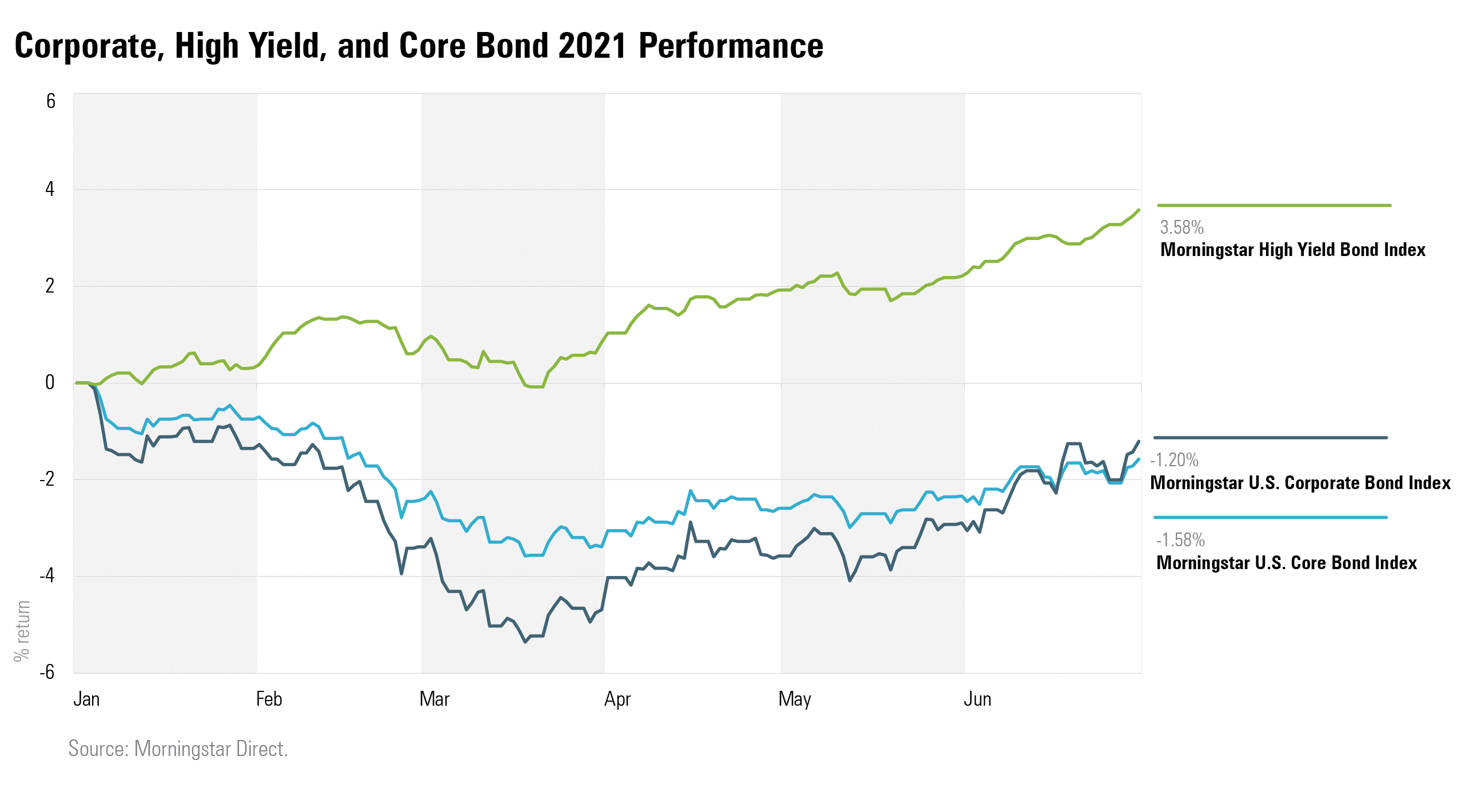

- High-yield bonds continue to outpace government and corporate bonds, with the Morningstar High Yield Bond Index rising 2.7% in the second quarter and 15.4% over the past year.

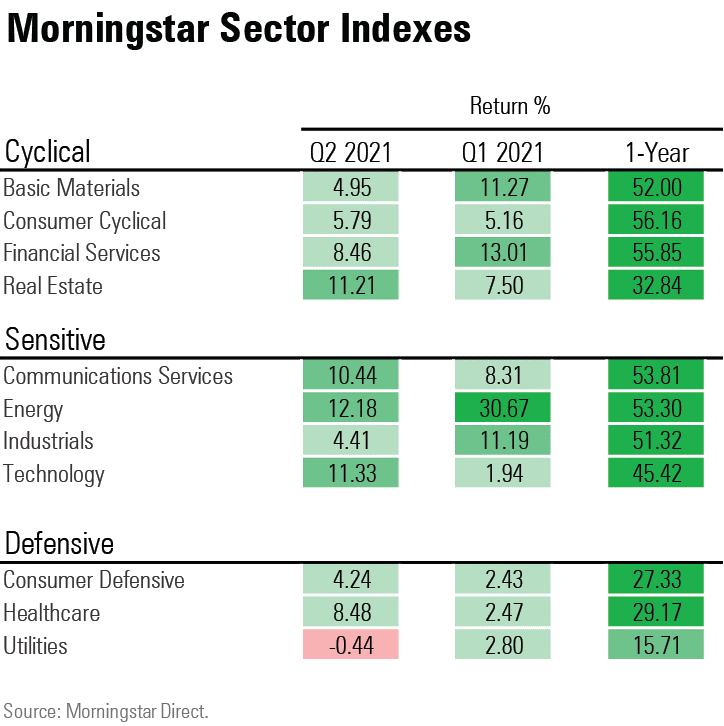

- Renewed demand for oil pushed prices higher and energy stocks topped the sector list, followed by technology stocks. Utilities and industrial sectors dragged.

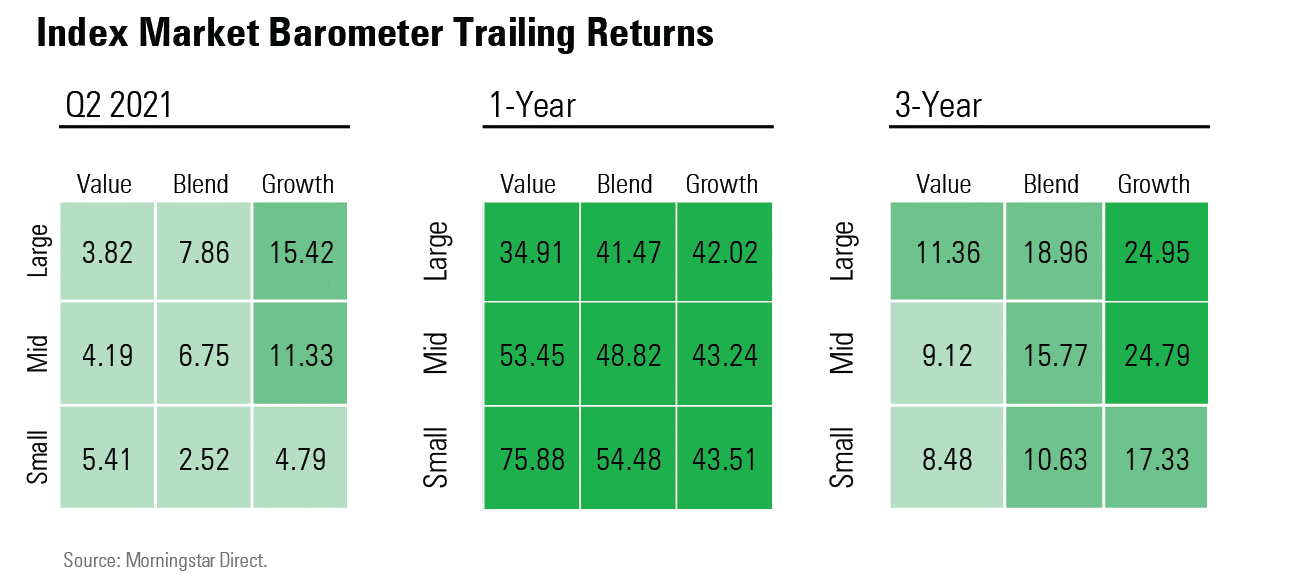

- The contrast between growth and value stocks faded as growth stocks bested value for the quarter across large and mid-cap Morningstar Categories. Small value continues to beat small growth.

In U.S. equity markets, one of the most dominant trends from late 2020 and the first quarter began to fade: the outperformance of value stocks over growth stocks. This shift came as the Federal Reserve indicated in June that it may raise rates somewhat sooner than expected amid signs inflation was beginning to take hold. (Morningstar Direct and Office clients can find out full-length market summary here.)

In the bond market, the headlines out of the Fed sent the yield of the 10-year note down 29 basis points to 1.45% from a recent high of 1.74% in the first quarter.

As the Fed signaled that it recognized the building inflation pressures by bringing forward rate increase expectations, longer-term yields fell, in turn causing the yield curve to flatten from the first quarter. The 10-year yield fell 29 basis points to 1.45% after reaching a recent high in March.

With the Fed keeping the current level of interest rates in place into 2023, markets weren’t spooked. In fact, stock market volatility fell to levels unseen since before the pandemic. In the U.S. market, volatility fell to its lowest level since 2019.

A wide divergence in sector performance during the first quarter narrowed in the second, with all but the utilities sector posting gains. Energy stocks still led, gaining 12%, but technology stocks rose 11.3% after trailing all other sectors in the first quarter. Stronger-than-expected earnings and expectations for a slower economic recovery may have revived tech shares in in the second quarter as investors sought out the category’s growth potential.

Real estate stocks performed better as housing prices rose across the country. The basic materials and industrials sectors cooled from the first quarter but finished the second quarter up still up on the year.

The clear divide in performance between growth and value stocks that dominated the market since October 2020 faded in the second quarter. Value stocks outperformed growth stocks in May, but April and June were strong months for growth stocks as energy returns fell back into step with other sectors and tech shares surged.

For the quarter, large- and mid-cap growth stocks beat their value counterparts but small-cap value still led small-cap growth.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/GJMQNPFPOFHUHHT3UABTAMBTZM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZYJVMA34ANHZZDT5KOPPUVFLPE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LDGHWJAL2NFZJBVDHSFFNEULHE.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/8b2e267c-9b75-4539-a610-dd2b6ed6064a.jpg)