2020 Market Performance in 7 Charts

We take a closer look at the stock and bond markets in Q4 and more.

/s3.amazonaws.com/arc-authors/morningstar/8b2e267c-9b75-4539-a610-dd2b6ed6064a.jpg)

A tumultuous 2020 ended with U.S. stocks pushing to new record highs during the fourth quarter, riding hopes that coronavirus vaccines, a decided U.S. presidential election, and expected U.S. fiscal stimulus would finally help the dust settle following months of economic and political uncertainty.

Fueling fourth-quarter rallies in riskier corners of the financial markets, as well as some of the sectors that had suffered the most earlier in the year, were aggressive efforts by the Federal Reserve and other major central banks to prop up the global economy in the wake of the economic collapse caused by the COVID-19 pandemic.

But even amid that hope, bond yields remained at historic lows, reflecting concerns that a return to economic normalcy is still far off on the horizon.

Here are some of the fourth-quarter and full-year 2020 highlights:

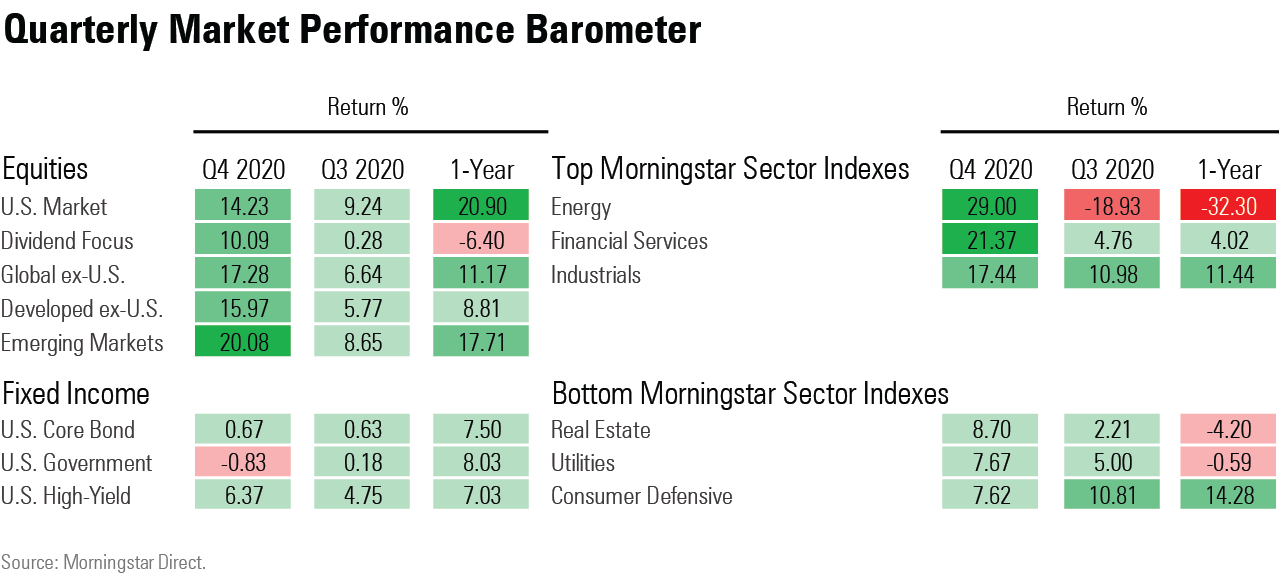

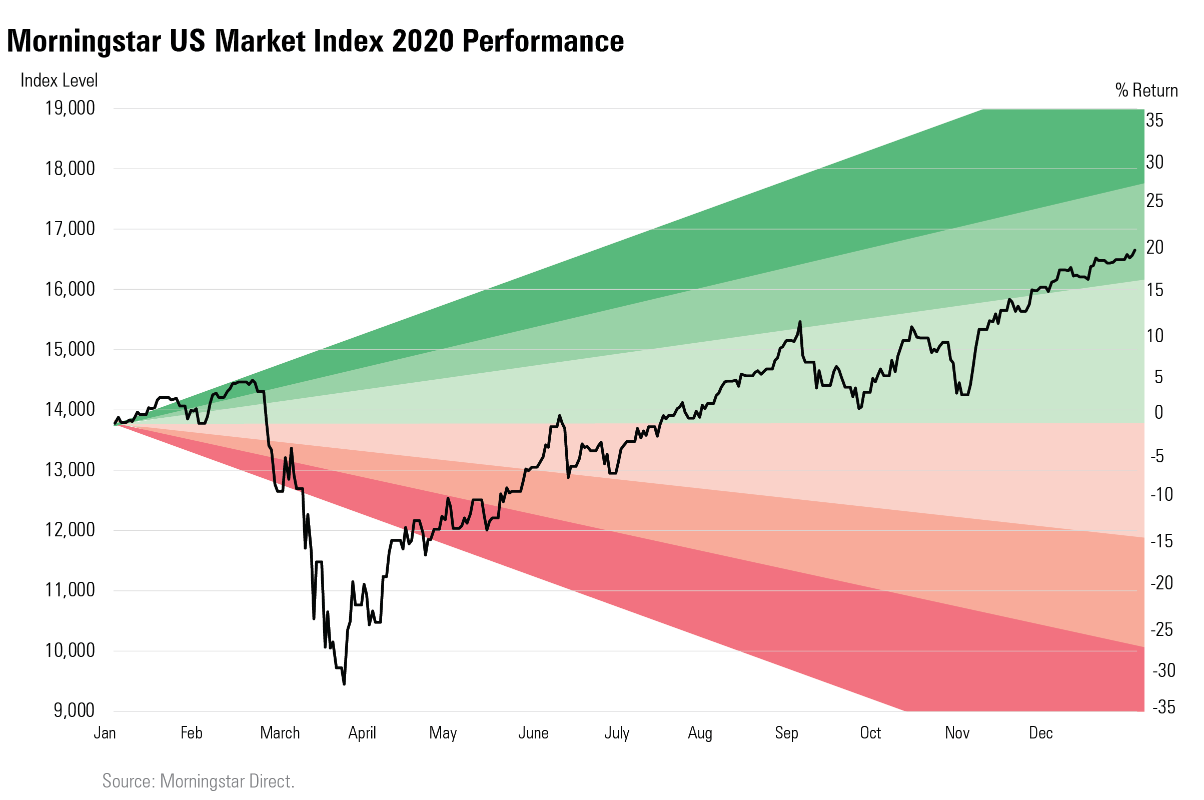

- The Morningstar U.S. Market Index rose 14.2% in the fourth quarter, finishing 2020 with a 20.9% return.

- At year-end, the U.S. market index had rallied 70% from March lows, which had seen the index down almost 30% for the year.

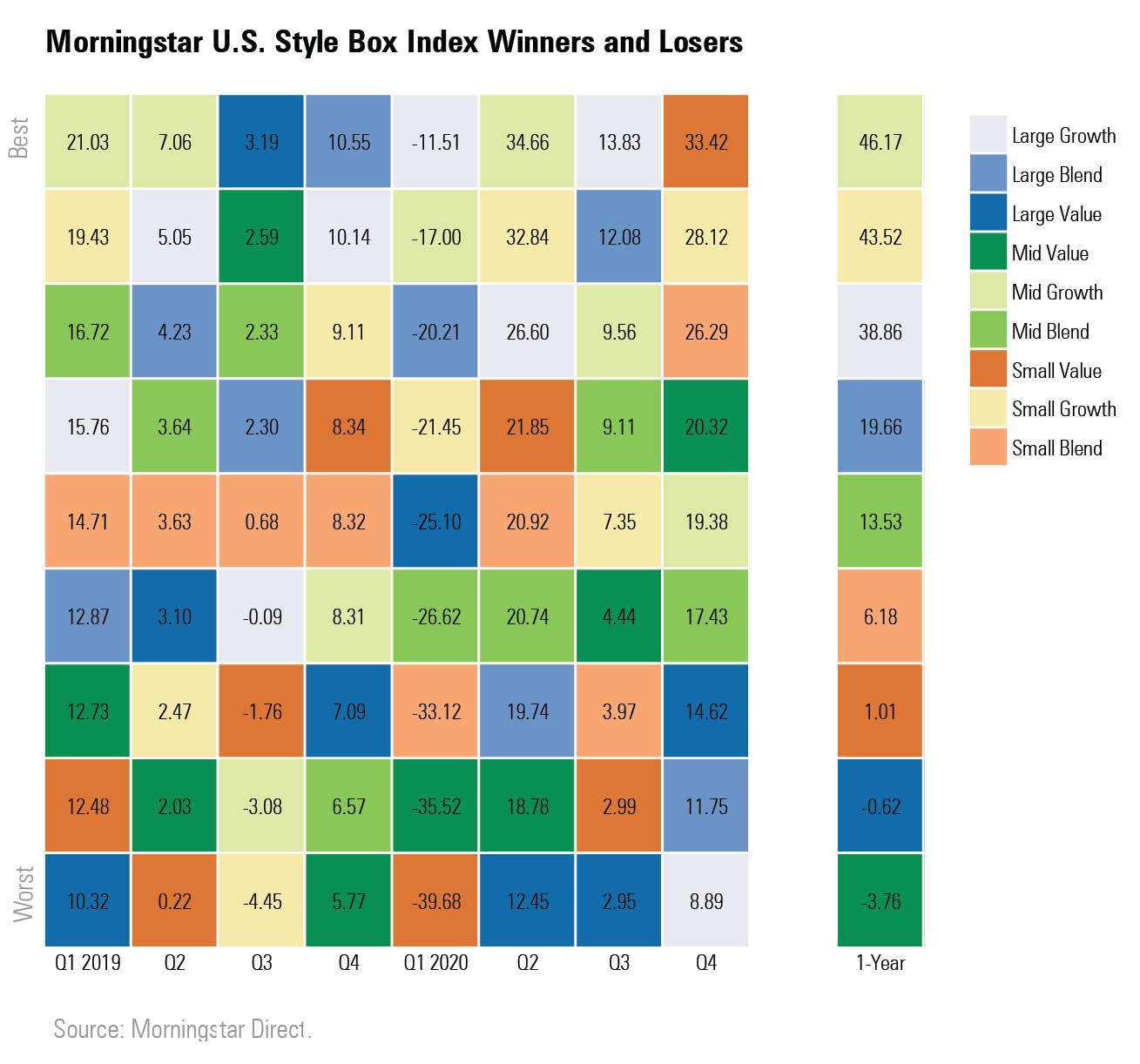

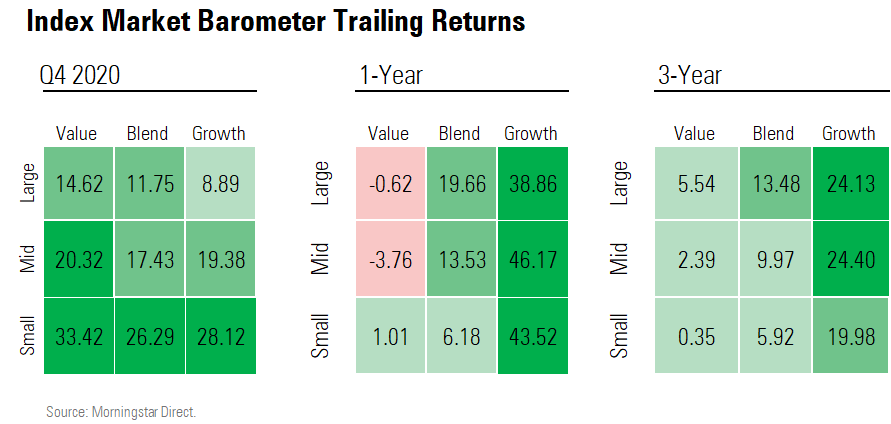

- Small-value stocks topped the Morningstar Style Box in the fourth quarter, but value still trails growth categories by massive margins for longer time frames.

- Dividend stocks bounced back strongly in the fourth quarter but lagged the broader market for the year.

- International and emerging-markets stock indexes outperformed the U.S. market during the fourth quarter.

- Despite a fourth-quarter rally, energy stocks were the worst performing sector for the fourth consecutive year.

- Consumer cyclical and technology stocks soared throughout the year.

- Yields on the U.S. Treasury 10-year finished 2020 down nearly 1 percentage point from 2019.

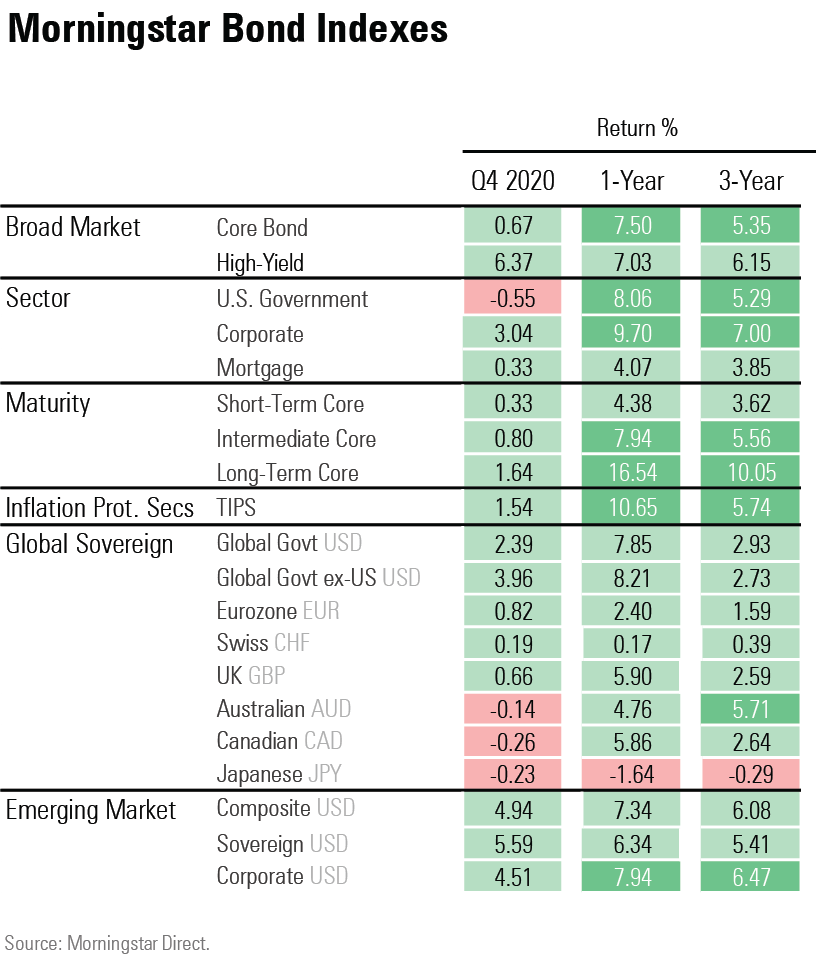

- The Morningstar U.S. Core Bond Index rose just 0.67% in the fourth quarter but returned 7.5% for the year.

- Inflation hedges, such as Treasury Inflation-Protected Securities and gold, all had a strong 2020 while safe-haven currencies suffered.

Equities While the fourth quarter started with renewed stock market volatility, equities rolled higher following the November U.S. elections, finishing the year with new record highs.

This reflected a remarkable recovery for stocks after the U.S. market experienced its fastest bear market in history during the first quarter as the threat of the pandemic hit home. The U.S. market index had lost 32.6% from its peak on Feb. 19 to its trough on March 20. But the strong recovery has been relatively steady, aside from declines in October and early November.

Stocks briefly dipped ahead of the U.S. election but then rallied strongly as COVID-19 vaccines began to be rolled out and because of investor views that the potential of a split government in the United States--with Democrats controlling the House of Representatives and Republicans the Senate (pending a January Georgia Senate run-off)--would make it harder to levy higher taxes on corporations.

Hopes surrounding the rollout of COVID-19 vaccines also bolstered confidence among investors that the worst of the economic damage would be history, helping fuel a rally in long-struggling small-value stocks. The fourth quarter marked the first time in four years that small value was the top performer within the style box.

Still, the strong quarter for small value did little to mitigate 2020’s woeful performance for the group. The Morningstar US Small Value Index barely finished the year in positive territory. Over the last three years, small value ranks as the worst stock style-box category, and its 0.3% average annual return for the last three years is dwarfed by the Morningstar Mid Growth Index's return of 24.4% for the time frame.

Large-value and mid-cap value stocks, meanwhile, on balance couldn’t make it into the green for 2020.

The value rebound was mirrored by a revival in dividend stocks. The Morningstar Dividend Yield Focus Index had plunged by more than 25% in the first quarter, 5 percentage points worse than the Morningstar U.S. Market Index. As stocks began their rebound in the spring, dividend payers lagged. But dividend payers have mounted a comeback and have outpaced the broader market since early November.

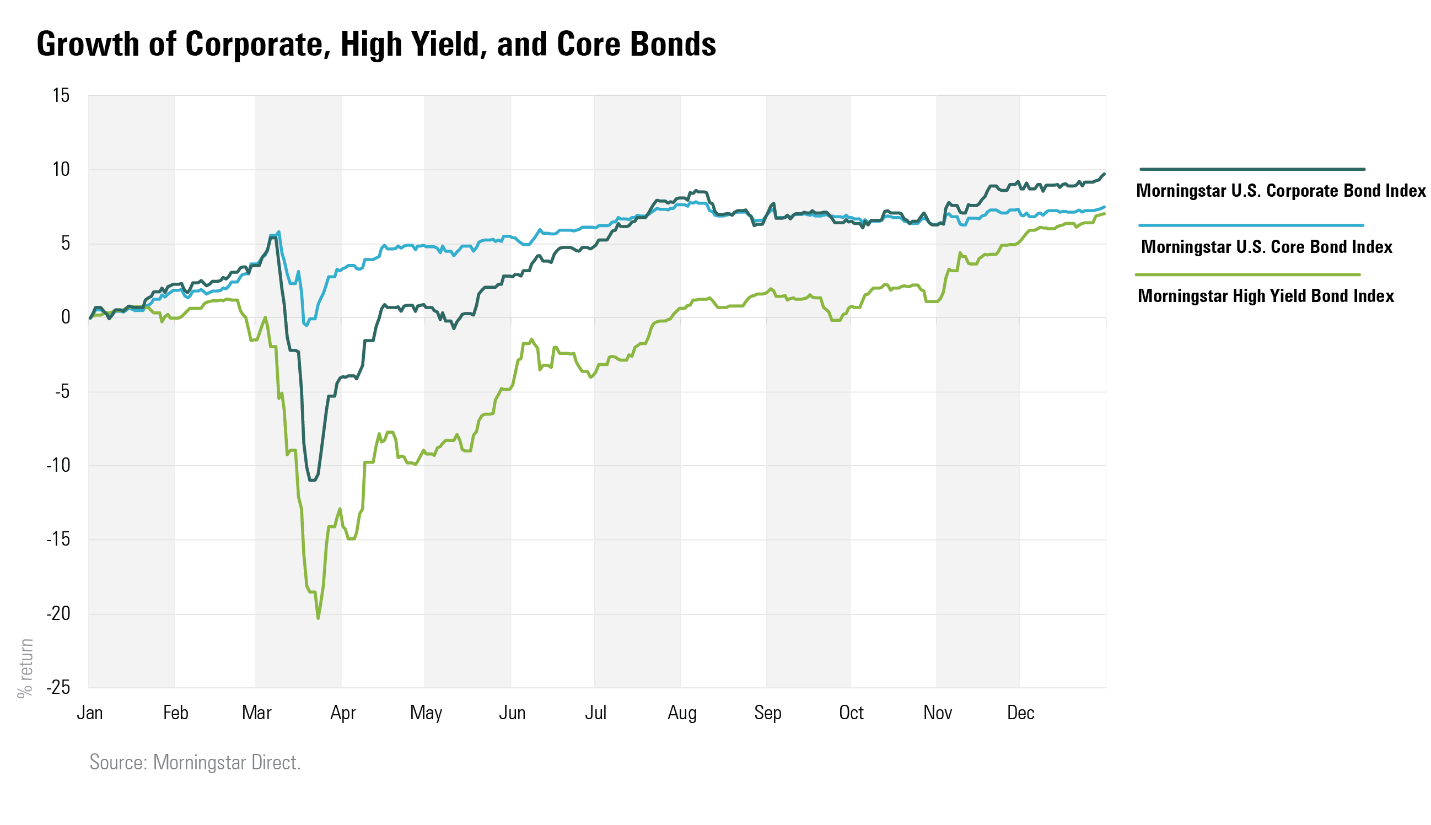

Fixed Income Expectations for another round of U.S. fiscal stimulus, coupled with optimism that COVID-19 vaccines will stanch the economic bleeding, sent interest-rate-sensitive bonds lower in the fourth quarter. Meanwhile, riskier high-yield and emerging-markets bond categories performed the best.

For the year, TIPS have gained 10.7% during the year, as investors anticipate rising inflation thanks to the Fed’s policy shift that would allow for higher inflation in order to give the economy more room to grow.

Throughout the year, Japanese bonds lagged and global government bonds outperformed U.S. Treasuries.

The economic damage from the pandemic held high-yield bonds back for most of the year, but the group made up lost ground in the fourth quarter. At mid-year, the high yield index was down 3.94%, while core bonds were up 6.11%. During the second half, high yield returned 11.3% compared with the core bond indexes’ gain of 1.14%.

By year-end, the Morningstar Corporate Bond Index had pushed into the lead thanks to the combination of low rates and a less gloomy economic outlook.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/GJMQNPFPOFHUHHT3UABTAMBTZM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZYJVMA34ANHZZDT5KOPPUVFLPE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LDGHWJAL2NFZJBVDHSFFNEULHE.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/8b2e267c-9b75-4539-a610-dd2b6ed6064a.jpg)