8 min read

Pharmaceutical Tariffs on Biopharma: Key Insights for Advisors and Investors

Pharmaceutical companies may face earnings pressure, but long-term fundamentals and opportunities remain. Find out what advisors and investors should know about the risks, potential price concessions, and where long-term opportunities may emerge.

Key Takeaways

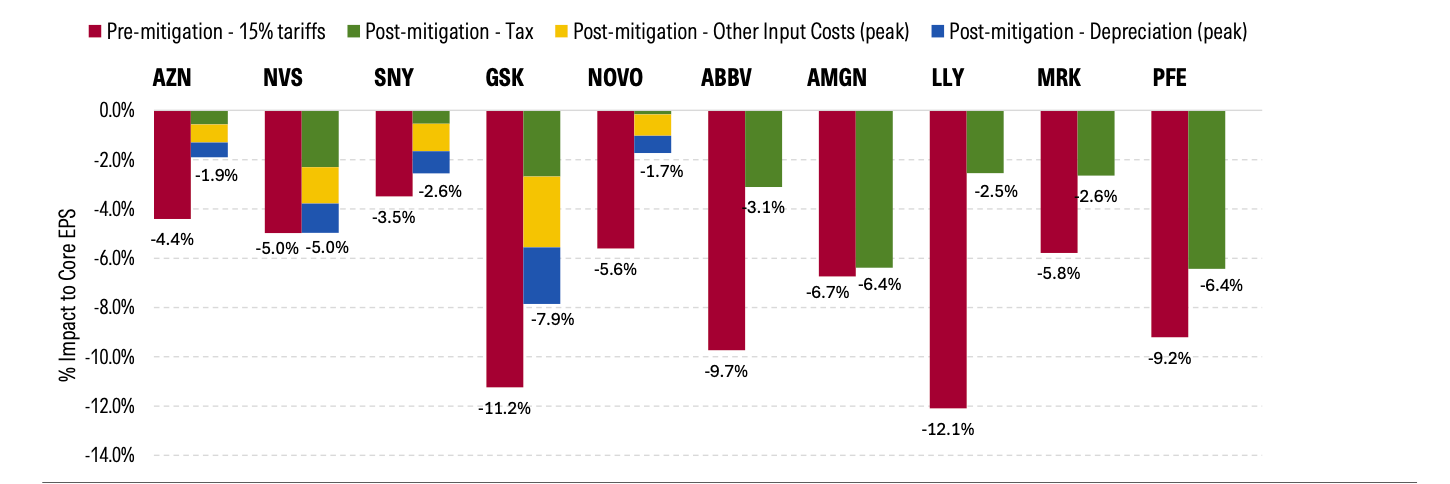

Based on our preliminary analysis of a basket of 10 large US and European drugmakers, we conclude that 15% tariffs for imports into the US would have an average unmitigated hit to core earnings per share of 9% for US companies and 6% for European companies. In reality, we expect mitigation strategies to soften the impact.

We view the risk of broad most-favored-nation pricing in the near term as exceedingly low. We believe attempts to compel broad-based MFN pricing using existing regulatory powers will likely fail, as it may harm patient access to drugs. Moreover, we will consider buying the sector if it dips again because of the threat of an MFN demonstration pilot.

Discussions of tariffs, or potential tariffs, have affected various industry outlooks—and the biopharmaceutical industry is no exception. In addition to announcing its plans to place tariffs on pharmaceuticals imported into the US, the Trump administration also proposed lowering US drug prices to most-favored nation, or MFN, prices.

For financial advisors and investors, understanding these policy shifts is critical, as they directly influence sector earnings forecasts and can shape investment decisions in healthcare portfolios.

In response, we predict many drugmakers will mitigate the impact by shifting manufacturing and technology to new locations within the US. We estimate that 15% tariffs for US imports will have an average hit to core earnings per share of 9% for US companies and 6% for European companies. However, we don’t see any impact to our moat ratings or fair values.

Our latest report analyzes five large US and five large European drugmakers to estimate these effects, as well as implications for the global supply chain and the revived push for US drug prices to be lowered.

Advisors can use these insights to better anticipate client concerns, explain short-term market volatility, and highlight long-term opportunities in the healthcare sector. For a more in-depth look at how these geopolitical influences will potentially affect investment decisions in the biopharmaceutical space, download the full report.

Source: Morningstar, company reports. Company data as of Dec. 31, 2024. EPS = earnings per share. Novo Nordisk figures use IFRS metrics. Amgen is a special case, and it is unlikely the current tariffs will be the catalyst for the full EPS impact from higher taxes shown here.

Initial, Mid-Term, and Long-Term Impact of Tariffs

As of this writing, tariffs on pharmaceutical imports into the US are likely to be implemented. We assume tariffs on pharmaceuticals will be capped at 15% for the European Union and Japan, because of recently announced trade deals with the two territories.

Our analysis is based on two key assumptions:

The amount of the company’s US sales supplied by ex-US manufacturing facilities

The customs value of the imported inventory

Though the specifics of tariff policy vary, in the near term, we expect no immediate impact from tariffs due to inventory management. Most big pharmaceutical companies carry at least six months of inventory, and many have been increasing inventory days in preparation for tariffs.

In the mid-term, we expect drugmakers to employ a variety of mitigation strategies, including outsourcing production to contract manufacturers and dual sourcing key ingredients. In some cases, drugmakers with existing approvals to manufacture drugs made in US facilities may be able to shift production from overseas facilities to the US quickly.

In the long term, we expect companies to change their supply chains so that most of their US sales are supplied by US manufacturing facilities. For European drugmakers, we believe most have a significant mismatch between their US sales and manufacturing footprints. Therefore, shifting supply to the US will require them to invest heavily in new facilities and bear the costs associated with ramping them up.

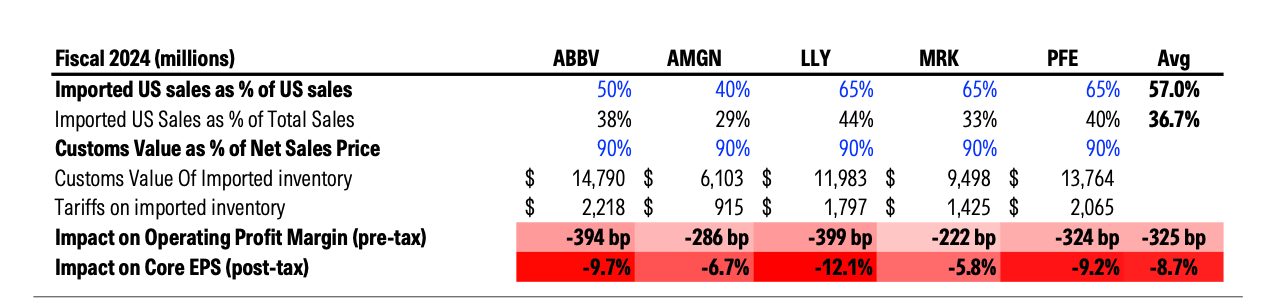

For US drugmakers, we think they already have abundant facilities in place, and therefore, the most significant cost is higher taxes.

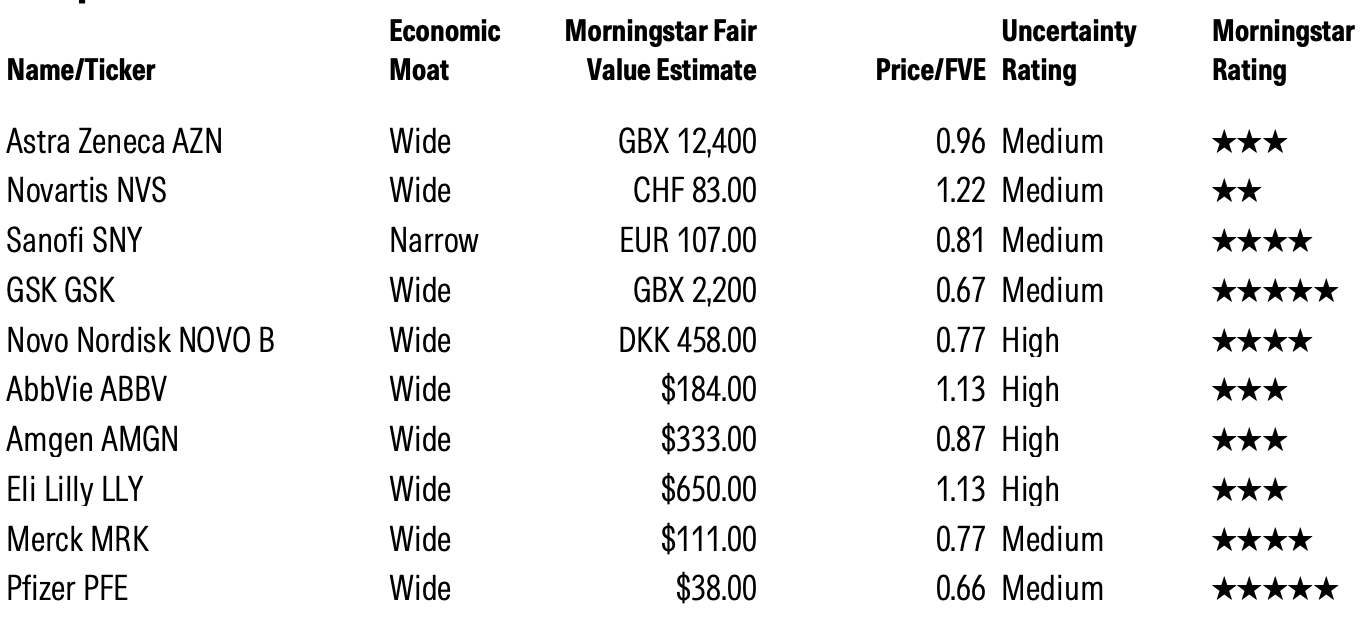

This year, in anticipation of potential tariffs, many pharmaceutical companies already announced plans to invest in US manufacturing and research facilities. European companies such as AstraZeneca, GSK, Sanofi, and Novartis have plans to invest tens of billions of dollars into the US by 2030.

After relocation, we expect the initial hit from tariffs to be replaced by an average peak impact of 3.8% to core earnings for European companies, which will partly abate over time. This includes a combination of costs associated with new capital expenditure, increased input costs associated with labor and raw materials, and higher taxes for some European companies.

We expect the former two to abate over time, whereas higher taxes paid should be permanent as long as tax rate remain unchanged.

Main Impact From Relocation to US Pharmaceutical Companies: Higher Tax Rates

For US pharmaceutical companies, relocating operations and/or implementing a region-for-region supply chain probably won’t require as much new capital expenditure beyond what had already been planned, but it will result in higher taxes.

After shifting supply, we expect the initial hit from tariffs to be replaced by a 4.2% average peak impact to core earnings for US companies, which we do not think will abate unless tax rates change.

Source: Morningstar, company reports. Company data as of Dec. 31, 2024. COS = cost of sales. Bp = basis points.

US companies already have larger manufacturing footprints (based on the percentage of total property, plant, and equipment in the US) and have also been investing more in the US since 2017, following the US’ reduction of its top federal corporate tax rate to 21% from 35%.

Because US companies already have large existing US manufacturing footprints, we believe that they will be able to relocate manufacturing to the US more quickly than European companies, which may have to spend more time and money building greenfield facilities.

Trump Administration Seeks Price Concessions

In 2020, the first Trump administration attempted to use regulatory rulemaking to implement a broad demonstration pilot that would have lowered Medicare reimbursement for Medicare Part B drugs to MFN-level prices.

The Centers for Medicare & Medicaid Services, or CMS, selected 50 high-cost drugs to be covered by the pilot, which composed almost 80% of Medicare Part B’s total drug spending. Participation would have been mandatory for most Medicare-participating providers.

However, certain types of hospitals and clinics were exempt, including cancer hospitals, children’s hospitals, critical access hospitals, rural health clinics, and US Indian Health Service facilities. Courts delayed the implementation of the MFN pilot because the Trump administration failed to observe the standard notice-and-comment period required by the Administrative Procedure Act, which is typically a minimum of 60 days.

However, beyond this, courts did not rule on whether the terms and structure of the proposed model fell within the scope of the statute supporting the demonstration pilot.

Nonetheless, we believe that if the current administration proposes another nationwide pilot today, we think its chances of succeeding are improbable, as it would have an adverse impact on patient care, which is a politically unpalatable outcome.

With broad reforms out of reach, we expect the current Trump administration to pursue quick, narrow concessions from drugmakers.

Most recently, the Trump administration has called upon drugmakers to provide MFN-level prices to Medicaid patients and to stipulate to other developed nations that they will not offer better prices for new drug launches than what is being offered in the US.

As of this writing, the Trump administration’s most recent public demands were conveyed in letters sent to 17 drugmakers on July 31, 2025. Although we have low certainty in how this situation will develop, we speculate that limited concessions in these areas may be within striking distance:

Lower Medicaid pricing for some drugs.

Lower US prices for select high-volume drugs.

Higher prices outside of the US for new-drug launches.

Investment Opportunities in the Biopharma Industry

For our basket of 10 US and European Big Pharma companies, we estimate an unmitigated average tariff headwind of 7% to core earnings per share.

Despite the harsh public tone that the Trump administration has adopted toward large pharmaceutical companies, we believe its end objectives are much narrower in scope and are partially aligned with drugmakers’ goals.

US drugmakers such as Pfizer, AbbVie, Amgen, Eli Lilly, and Merck already possess significant domestic manufacturing capacity, allowing them to offset tariff impacts quickly, even with the higher tax burden.

European drugmakers, including AstraZeneca, Novartis, Sanofi, GSK, and Novo Nordisk, face greater costs from shifting to US facilities. But once facilities are built, these companies will be shielded from future trade policy risks.

For financial advisors and investors, understanding these dynamics helps in assessing portfolio risk, guiding client allocations, and identifying opportunities in the biopharma sector.

It is a common strategy for the Trump administration to issue very high demands initially but later settle for more moderate terms. We have seen this strategy employed across policy sectors, including the recent trade negotiations.

It is our view that the Trump administration understands that drugmakers by themselves are unable to reform the US drug pricing system, much less force other governments to pay higher drug prices, and is actually seeking quicker, less ambitious concessions from drugmakers that do not require congressional action or accords with other nations.

Advisors can explore these insights further using the Morningstar Direct Advisory suite to support investment decisions and client conversations.