7 min read

Managed Care Organizations: 2025 Outlook and Policy Shifts

Regulatory and policy challenges are mounting as Medicaid faces potential spending cuts.

Managed care organizations (MCOs), which primarily offer medical and pharmaceutical benefit plans, play a central role in the United States healthcare system. By managing health plans for individuals and groups, they help mitigate risks within the complex multipayer landscape.

In 2025, the managed care sector faces a challenging environment. The healthcare sector outlook is shaped by rising medical cost ratios (MCRs), increased regulatory scrutiny, and potential membership declines driven by shifting healthcare policy.

The full Managed Care Organizations report breaks down the state of MCOs in 2025, explores key growth drivers, and analyzes the long-term outlook for the industry. Download the free report.

Who Are the Top Companies in the Managed Care Industry?

A handful of major players dominate the managed care industry. In 2024, six large MCOs accounted for a significant portion of the $5.3 trillion in US national health expenditures:

- UnitedHealth Group: 10%

- CVS Health: 8%

- Cigna: 5%

- Elevance: 4%

- Centene Corporation: 3%

- Humana: 3%

Collectively, these six companies provided health insurance for 52% of the US population in 2024. This marks a substantial increase from 2014, when they insured just 41% of the population, highlighting their growing influence in the healthcare system.

Trends in the Managed Care Organizations Industry

Managed care organizations manage approximately one-third of the nation’s total health expenditures. However, their profitability is coming under pressure. On average, MCRs are expected to be more than 300 basis points higher in 2025 than they were in the preceding five years.

Mismatched Rates/Utilization Pressuring MCO Profits

_Profits_2025.png?format=webp&auto=webp&disable=upscale)

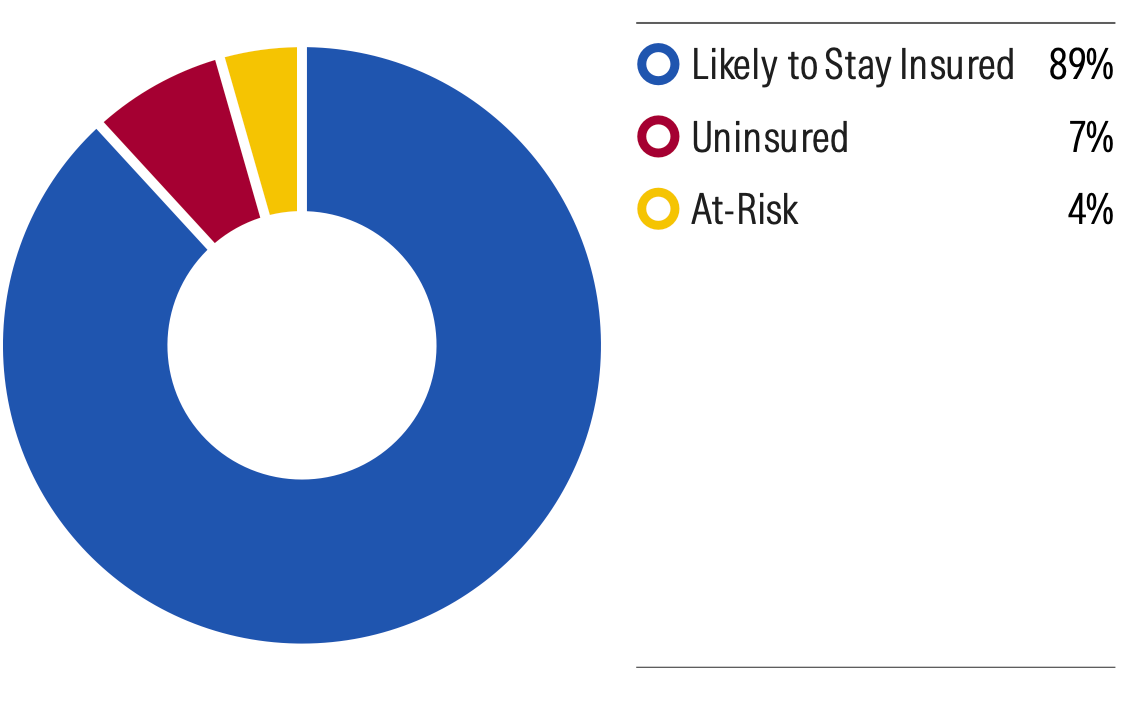

The US insured rate could decline by about 400 basis points from recent peaks (93% in 2023) due to the Republican Party policies that could reduce coverage by about 15 million

people, according to the Congressional Budget Office:

- An estimated 10 million people may lose Medicaid coverage by 2027 due to new eligibility requirements.

- Another 5 million people are at risk of losing coverage from individual exchanges if federal subsidies under the Affordable Care Act expire in 2026.

One Big Beautiful Bill Act Could Reduce Insured Rate

Key Growth Drivers and Opportunities

Despite the pressures, several areas offer significant growth opportunities for managed care organizations.

Medicare Advantage

The Medicare Advantage market remains a powerful growth engine. The senior population is projected to grow at a compound annual growth rate (CAGR) of 1.8% through 2035, steadily increasing the pool of potential members.

- Medicare Advantage enrollment is estimated to grow at an 8% CAGR through 2034, adding approximately 200 basis points to its market share.

- UnitedHealth and Humana are the dominant forces in this segment. In 2024, UnitedHealth insured 29 million Medicare Advantage members, while Humana insured 18 million.

Medicaid

While overall Medicaid spending is set to grow at a 3% CAGR through 2034, spending on Medicaid MCOs will expand at a faster pace of 4% CAGR, driven by states increasingly outsourcing the management of their Medicaid programs to improve efficiency. Centene Corporation leads the market with a 17% membership share in 2024.

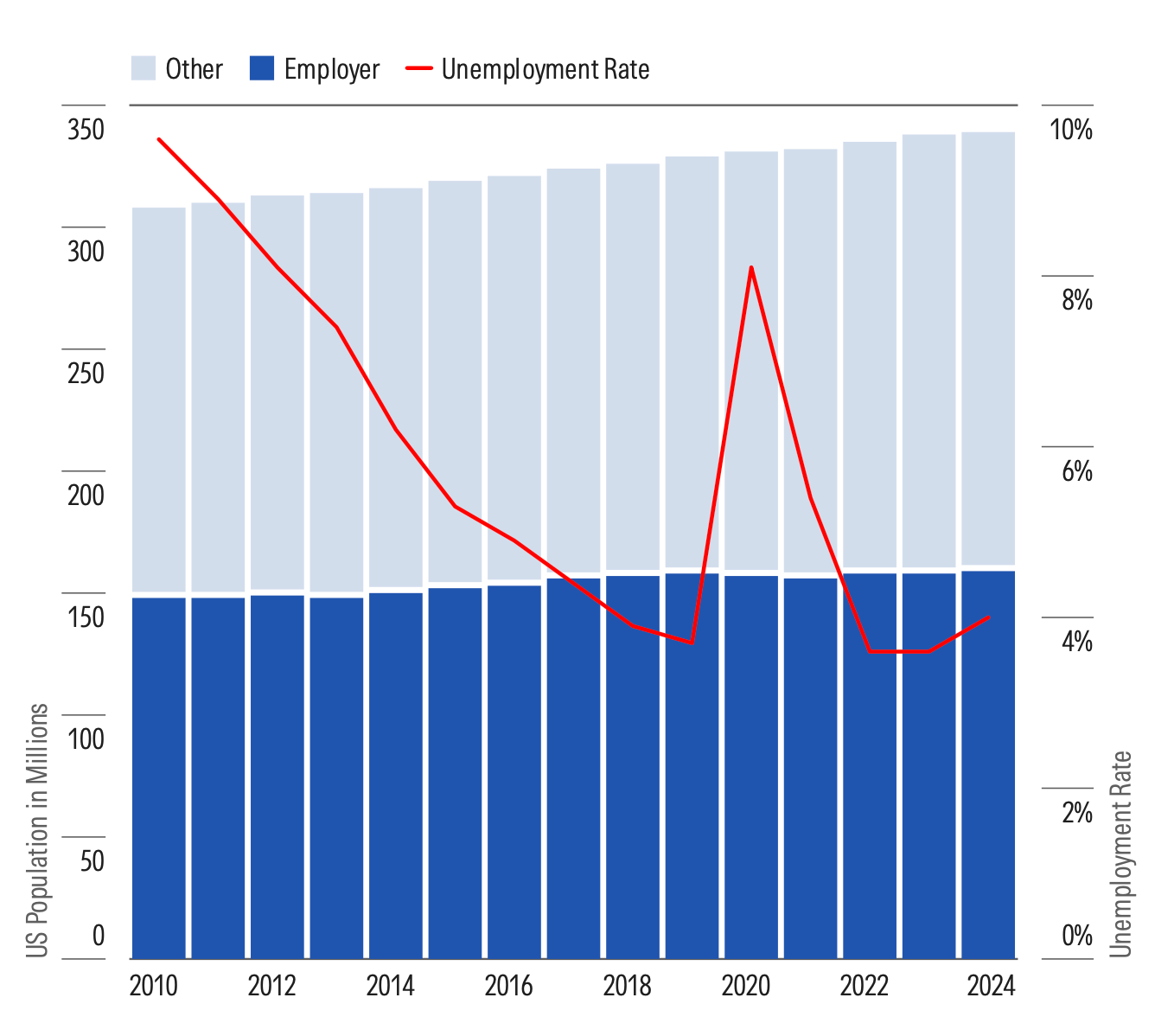

Employer and individual markets

The employer-sponsored health insurance market has remained stable, covering between 47% and 48% of Americans from 2014 to 2024. Spending per member in this market is on track to grow at a CAGR of about 4% through 2034.

Employer Plans Plateau, Even as Unemployment Rates Stay Near Historic Lows

The individual exchanges face near-term uncertainty, with 5 million members at risk of losing coverage if subsidies expire in 2026. However, the long-term growth forecast for this segment remains positive, with expectations of mid-single-digit growth.

Competition Among the Largest MCOs

The competitive landscape for MCOs reflects the influence of vertical integration and local market concentration. Many of the largest MCOs also operate as pharmacy benefit managers (PBMs), managing prescription drug benefits and other healthcare services.

- In 2024, the top three PBMs—operated by Cigna, CVS Health, and UnitedHealth Group—handled 80% of all pharmaceutical claims, up from 65% in 2015.

- This integration gives these companies a significant competitive advantage in controlling costs and negotiating drug pricing.

Membership is also highly concentrated. As of 2024, the top MCOs reported the following membership numbers:

- UnitedHealth: 49 million

- Elevance: 46 million

- CVS: 27 million

- Centene: 22 million

- Cigna: 18 million

- Humana: 14 million

At the local level, certain MCOs hold dominant positions. For example, Elevance, which operates in 14 Blue Cross/Blue Shield states, holds a 52% market share in Cincinnati.

ESG Snapshot

From an Environmental, Social, and Governance (ESG) perspective, MCOs face several key risks.

The most significant of these are ensuring access to care, protecting data privacy, and maintaining sound product governance. The major cyberattacks on UnitedHealth’s Change Healthcare network in 2024 highlighted the critical importance of cybersecurity and data protection for the entire healthcare system.

The policy outlook for MCOs is closely tied to political control. A change in administration could bring shifts in regulations related to the Affordable Care Act, the Inflation Reduction Act, and oversight from the Centers for Medicare and Medicaid Services (CMS).

Forging the Path Forward

US healthcare spending is forecast to grow at a 5% CAGR through 2034. MCOs are poised to capture a larger share of this growth, with their insured portion of the US population expected to increase from 52% in 2024 to 56% by 2034.

US Healthcare Spending (5% CAGR) Will Likely be Led by Medicare (8% CAGR), Offset Somewhat by a Medicaid Deceleration (3% CAGR) Through 2034

.png?format=webp&auto=webp&disable=upscale)

Source: Morningstar analysis of Centers for Medicare & Medicaid Services and Congressional Budget Office estimates as of September 2025. CAGR = compound annual growth rate.

While profit margins may recover as medical cost ratios improve, they are unlikely to return to the higher averages seen before 2020.

Advisors should be prepared for shifts in the regulatory landscape, particularly concerning the Affordable Care Act, the Inflation Reduction Act, and oversight from the Centers for Medicare and Medicaid Services

The data evaluated in the report was generated in Morningstar Direct, a comprehensive application that helps asset and wealth managers build their assets and manage their portfolios. Start a free trial of Morningstar Direct today.