One Year Since the Coronavirus Crash: U.S. Market Volatility and Performance in 7 Charts

Investors who stood firm were rewarded as the markets recovered, and then some.

/s3.amazonaws.com/arc-authors/morningstar/8b2e267c-9b75-4539-a610-dd2b6ed6064a.jpg)

A year after the coronavirus pandemic sparked financial turmoil, one thing is clear: Investors who didn't panic during the panic have been rewarded.

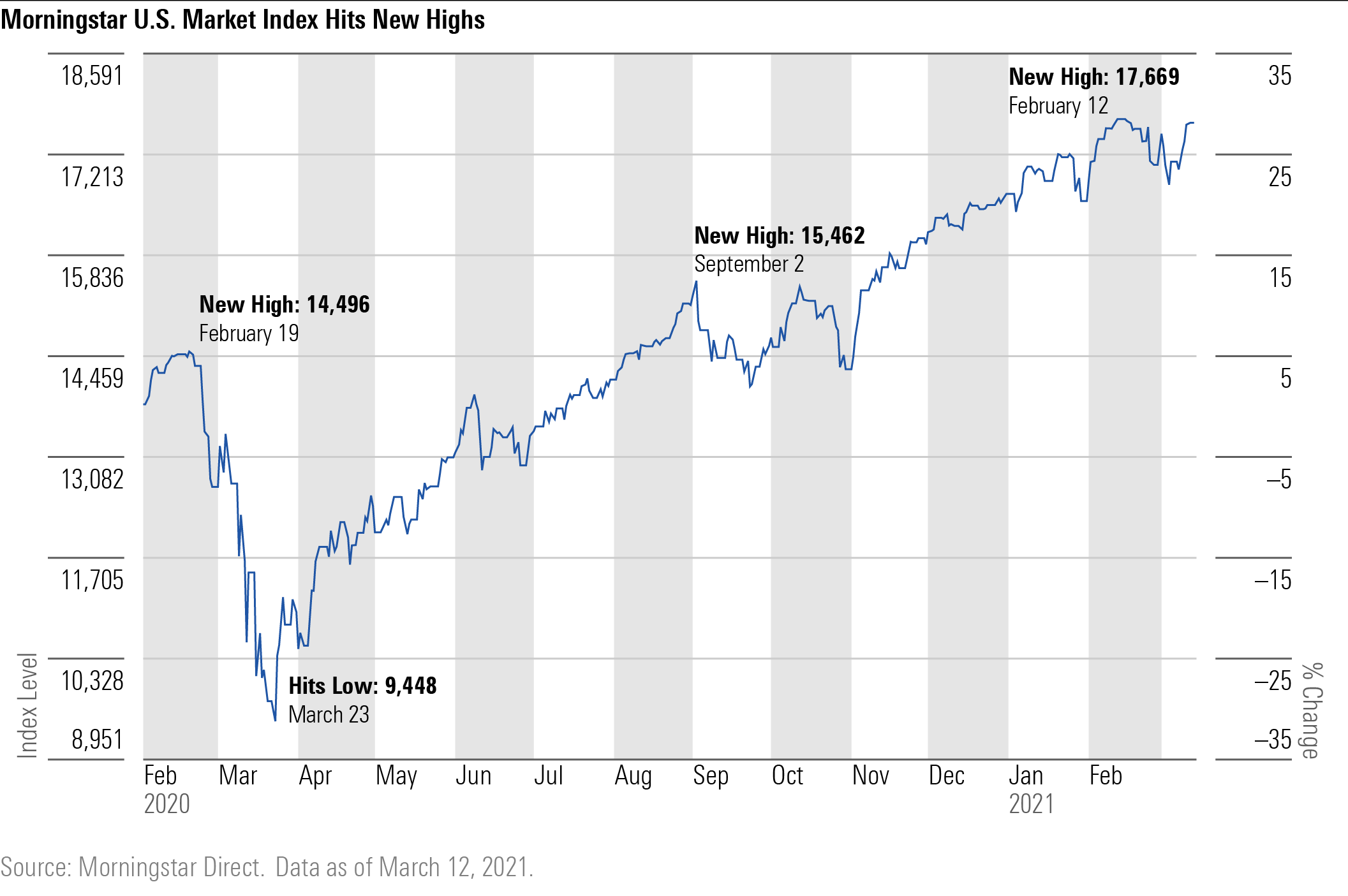

Given the broader upheaval in the global economy, social unrest, and political sea change in Washington, it may be hard for some investors to remember just how bad the markets were a year ago. The Morningstar US Market Index hit a new peak on Feb. 19, 2020, marking the start of the quickest bear market in history. The index then fell 35% in 33 days, hitting a low on March 23.

Not only did the markets stabilize and rebound quickly by historical standards, stocks are hitting new highs. The Morningstar US Market Index is 20% higher than it was on Feb. 19, 2020. Credit markets, too, where worries about the economic collapse hammered prices, have recovered.

Overall, investors have adjusted to the new environment, and along with record fiscal stimulus and strong Federal Reserve action, markets have stayed buoyant and volatility has ebbed.

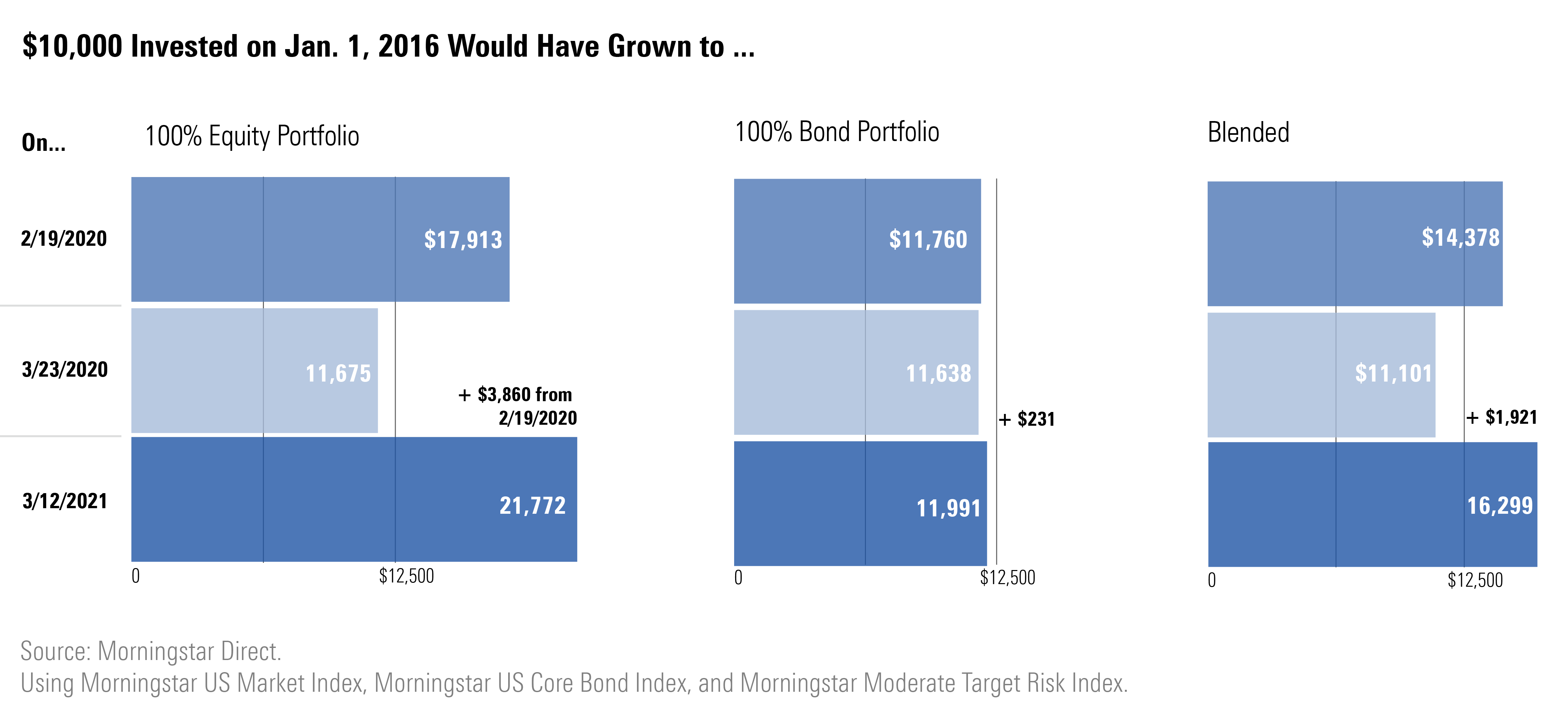

Investors who weathered the volatility have been rewarded. Basic portfolios composed of stocks, bonds, or a mix of the two that were already reaching five-year highs in February 2020 have all gained since.

Here another look at the data: $10,000 invested in the U.S. market in 2016 would have grown to $17,913 by February 2020, and investors who managed to stomach the 35% drop would have ended up with $21,722 one year later.

Less-risky core bonds stayed steady, falling only 1% from highs in February 2020, and investors still ended up with $11,991 in March 2021.

The blended portfolio that stood at $14,378 in February 2020 would have fallen 23% to $11,101 in March of last year, but investors would have recovered to $16,299.

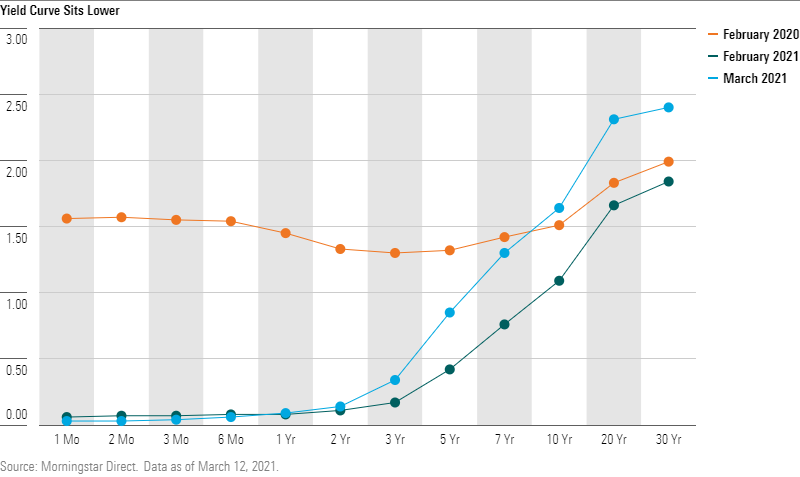

In the background, fixed-income investors were already facing historically low yields, but the COVID-19 crisis pushed them even lower. The 10-year yield hit a historical low of 0.318% on March 8, 2020. One year later it recovered to 1.64%.

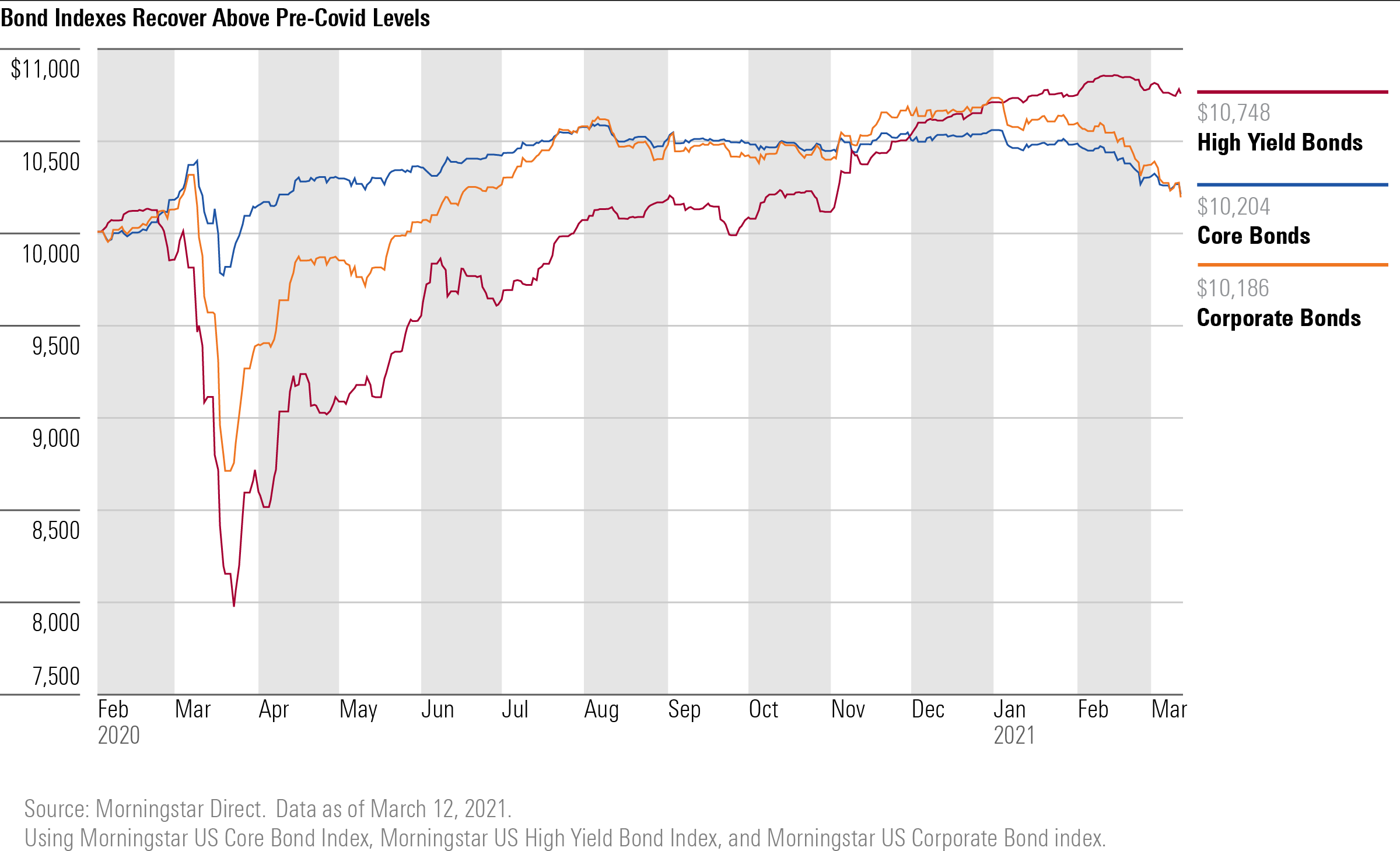

Although much of the attention last March was on the stock market, the ripples from the overnight shutdown of the global economy also hit the bond market, especially credit-sensitive bonds.

High-yield bonds took a hard hit with the Morningstar US High Yield Bond Index falling 20% from Feb. 19, 2020, to March 23, 2020, amid fears of mass defaults. But after aggressive efforts from the Federal Reserve, which included direct purchases of bonds and exchange-traded funds, markets stabilized and then recovered. The index gained 35% from its low in March, outpacing corporate-bond and core bond indexes.

Investors who purchased $10,000 in high-yield bonds at the beginning of 2020 would have at once been down to $7,967 but almost a year later ended up with $10,748.

Meanwhile, the same amount invested in the core bond index would have been down to $9,763 in March 2020 and recovered to $10,204 one year later.

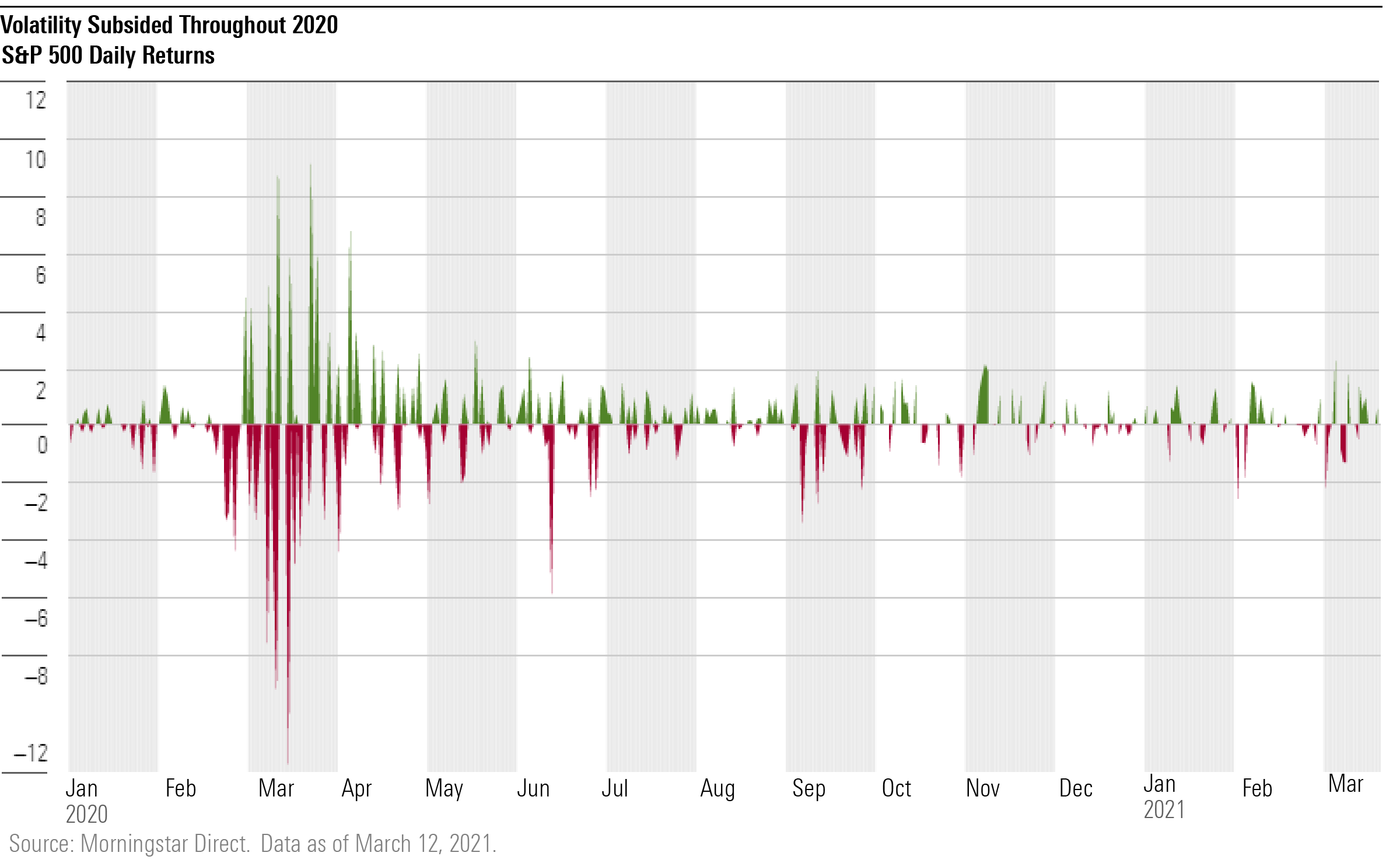

With assurance from the Federal Reserve that they would do all it takes to shore up markets, volatility subsided in the U.S. stock market in the second half of 2020. But the year still had the most one-day moves in the history of the S&P 500. The index moved more than 2% on 44 days, but by the fourth quarter things looked more normal--there were only two days the index moved more than 2%.

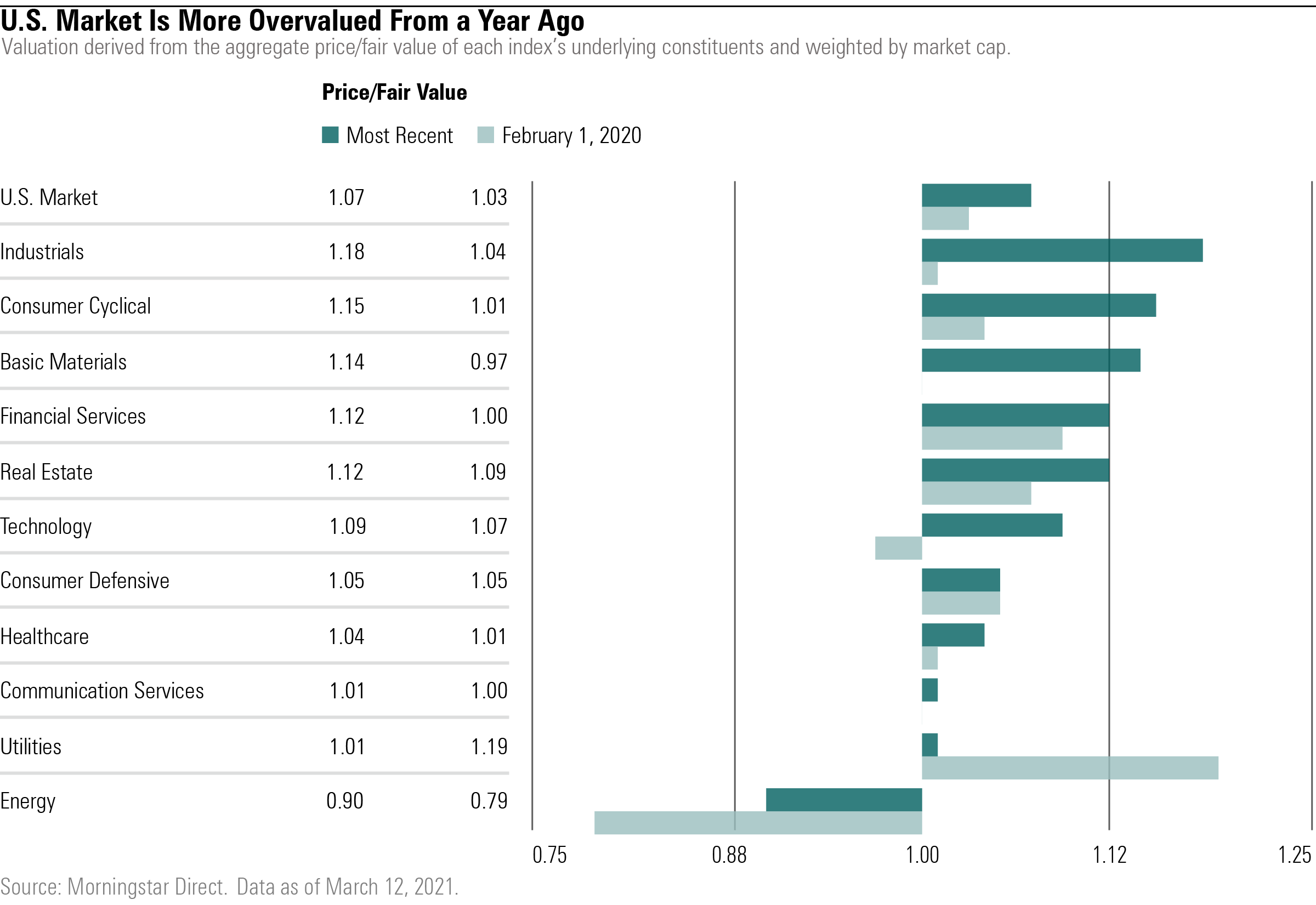

The swift recovery has left most of the U.S. market even more overvalued compared with early 2020. According to Morningstar's equity research only 18% of our coverage list is currently undervalued, compared with 21% the year before.

The overall market carries a price/fair value of 1.07, 4 basis points higher than a year before. Currently, industrials and consumer cyclical stocks look the most overvalued. In February 2020, utilities were trading the highest above their fair value, but after a dismal performance last year, the sector now looks more fairly valued.

One thing has stayed constant, though, energy stocks by Morningstar’s measures remain severely undervalued.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T5MECJUE65CADONYJ7GARN2A3E.jpeg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/VUWQI723Q5E43P5QRTRHGLJ7TI.png)

/d10o6nnig0wrdw.cloudfront.net/04-22-2024/t_ffc6e675543a4913a5312be02f5c571a_name_file_960x540_1600_v4_.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/8b2e267c-9b75-4539-a610-dd2b6ed6064a.jpg)