New Proxy-Voting Options for IVV and Other Index Funds From BlackRock, State Street, and Vanguard

What’s ‘pass-through voting,’ and other insights for index fund investors in 2024.

/s3.amazonaws.com/arc-authors/morningstar/20726617-027d-4959-87ab-429b60ece7ce.jpg)

If you own an index fund, chances are that it’s managed by BlackRock, State Street, or Vanguard, the so-called Big Three asset managers. In the past, the three took care of all proxy-voting decisions for index fund investors. That’s changing. In 2024, they are letting select fund investors have some choice on how to vote proxies for the underlying companies.

That creates an opportunity for index fund investors to vote according to their values, especially investors who are inclined to support sustainability-focused resolutions—and even those who want to reject the proposals. The process is called proxy-voting choice, also called pass-through voting. It allows investors to select an alternative proxy-voting policy that prioritizes climate change or other sustainability or governance objectives that differ from the Big Three’s house policies.

Morningstar devotes a lot of time to analyzing the voting activities of the Big Three. Each of the three firms votes very differently from the others on environmental, social, and governance themes.

Investors hold a very wide range of views on ESG topics as diverse as climate change, nature preservation, workers’ rights, racial equity, and ethical use of technology. So, when it comes to voting, one size certainly doesn’t fit all. That means investors in some of the largest funds offered by the Big Three might feel that the firms’ voting decisions don’t always reflect their personal stance on ESG topics.

Below, we analyze how the Big Three tend to vote, and we sort through the new voting options available to select index fund investors.

Which Funds Are Eligible for Proxy-Voting Choice?

The three managers are still in the process of ramping up their proxy-voting choice programs. Broadly though, the option is being made available to individual investors on several popular U.S. equity index-tracking funds.

For BlackRock, this includes iShares Core S&P 500 ETF IVV. The firm announced in July that the USD 380 billion fund would be eligible for proxy-voting choice in 2024.

This month, Vanguard and State Street also announced additions to the proxy-voting choice options available to investors next year.

Vanguard announced that two more funds will be eligible for proxy-voting choice in 2024: Vanguard Mega Cap Index Fund VMCTX and Vanguard Dividend Appreciation Index Fund VDADX. This adds to the three existing eligible funds from Vanguard: Vanguard S&P 500 Growth Index Fund VSPGX, Vanguard Russell 1000 Index Fund VRNIX, and Vanguard ESG U.S. Stock ETF ESGV.

State Street added a new voting policy choice to its program—an option to align all votes with company boards’ recommendations. (BlackRock and Vanguard already offered similar policy choices.)

According to State Street representatives, the firm’s proxy-voting choice options cover “a broad range of US index equity SPDR ETFs and mutual funds,” including widely held products such as SPDR Portfolio S&P 500 ETF SPLG, SPDR Portfolio S&P 500 Growth ETF SPYG, and SPDR S&P Dividend ETF SDY.

Notably, some of State Street’s largest index portfolios are not eligible for proxy-voting choice, including the USD 440 billion SPDR S&P 500 ETF Trust SPY and the USD 30 billion SPDR Dow Jones Industrial Average ETF Trust DIA. These funds employ a “mirror voting” policy under which the funds’ trustees vote in a manner proportionately reflecting the voting decisions of other shareholders in the companies it holds.

How Do the Three Firms’ House Voting Policies Differ?

Proxy-voting choice is, of course, a choice—investors have the option of continuing to rely on their asset manager’s discretion to make proxy-voting decisions. Sticking with the house voting policy is the easiest option for investors who do not have strong views on ESG issues.

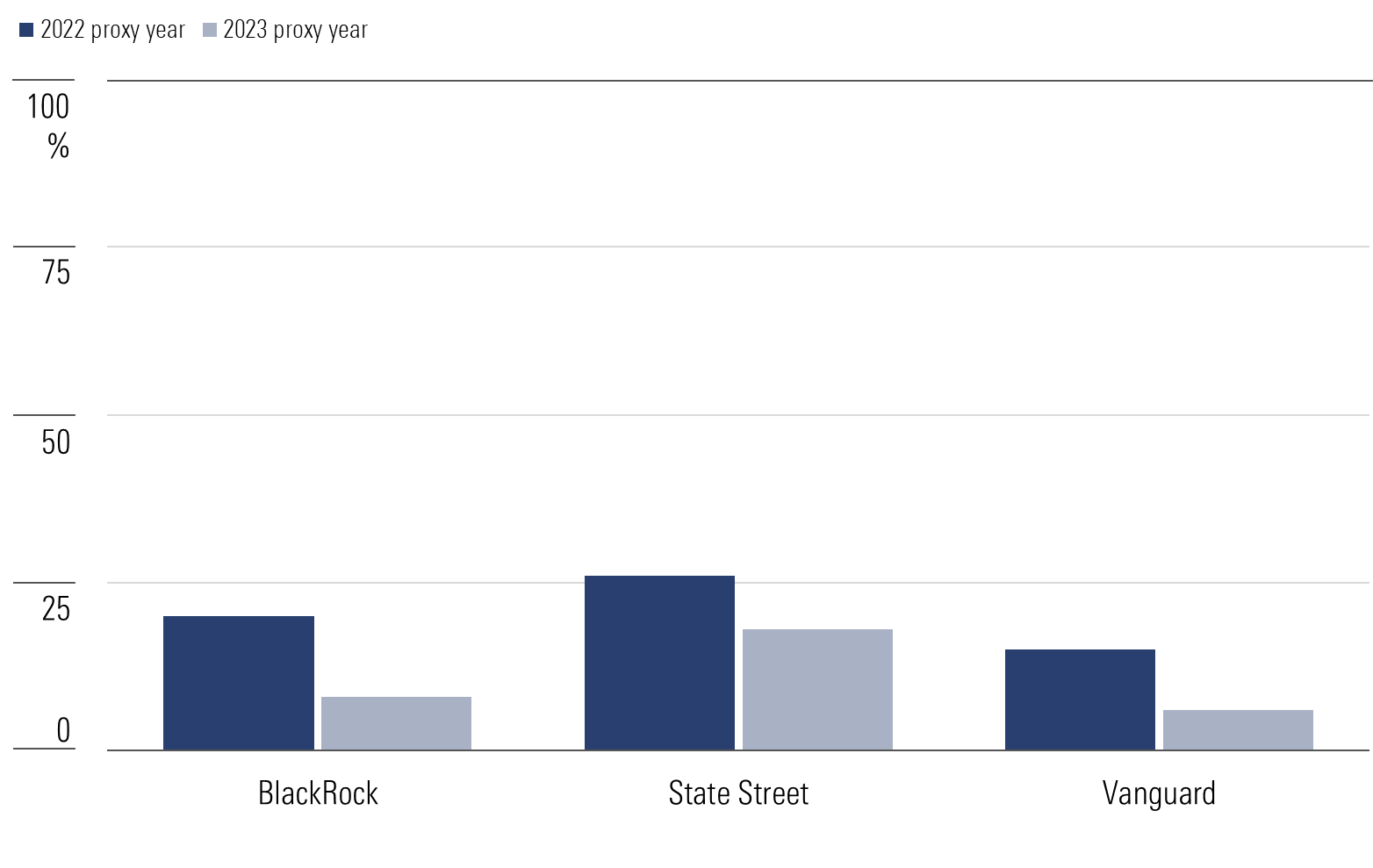

For those that do, it’s important to understand the differences between the Big Three managers’ typical proxy-voting stances. Looking at ESG shareholder resolutions, for example, Vanguard is least likely to support shareholder proposals. State Street is most likely to support them, with BlackRock somewhere in between, as the chart below shows.

Percentage of U.S. Shareholder Resolutions Supported

All three firms recently supported less than one fourth of all U.S. shareholder resolutions. Their support for these proposals is also on the decline, as the three firms hold the view that the quality of shareholder resolutions has fallen amid a steep recent rise in the number of resolutions being filed.

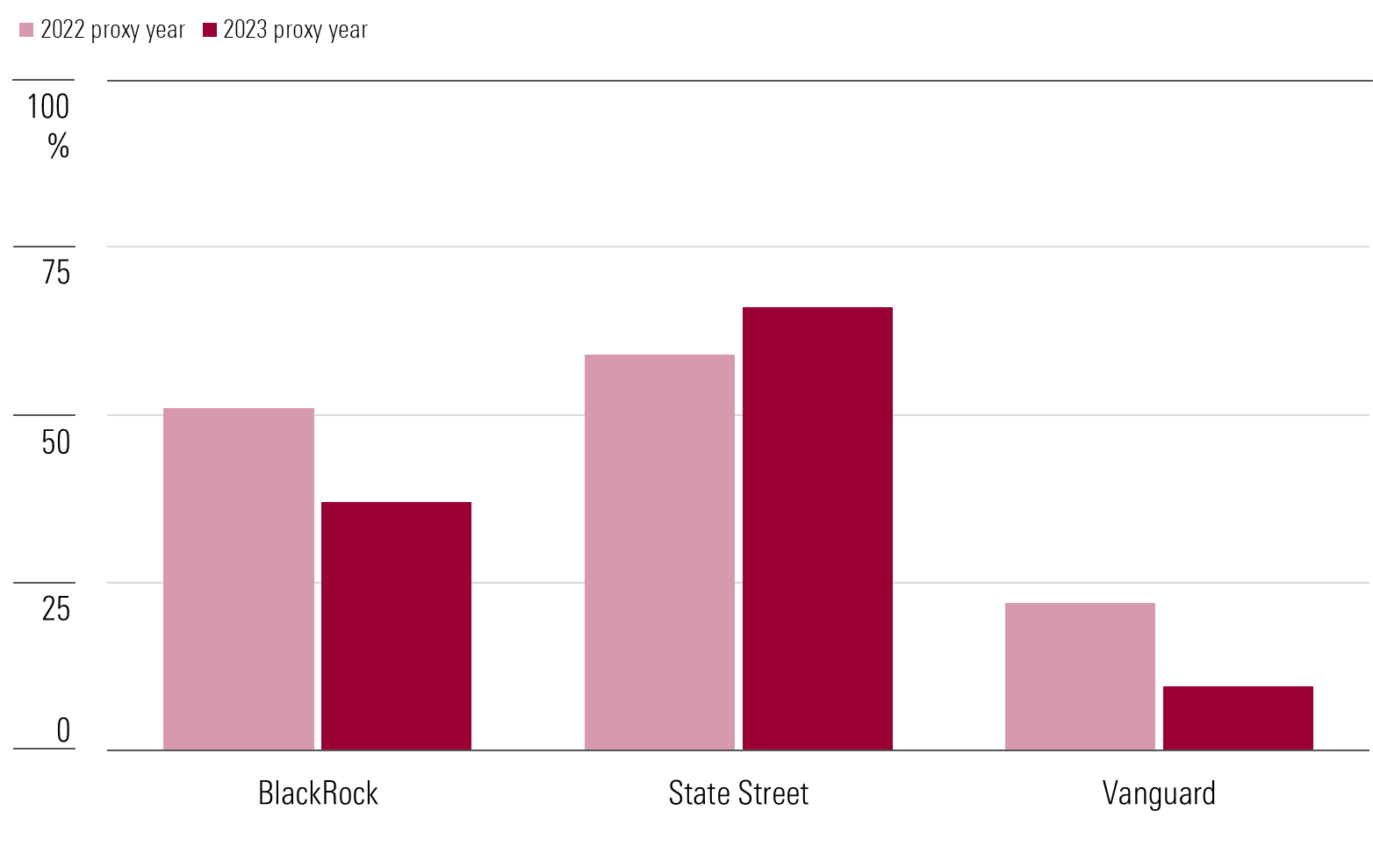

Looking only at well-supported resolutions on environmental and social issues paints a slightly different picture. Every year, we analyze “key resolutions”—shareholder proposals on environmental and social topics with the support of at least 40% of shareholders independent of the company. This analysis gives a more consistent view of which proposals asset managers view as material and are prepared to support.

As the chart below shows, looking at support for key resolutions places the firms in the same order—Vanguard with the lowest level of support, State Street the highest, with BlackRock in between. However, there are greater differences between the three firms’ voting records in 2023, both compared with each other and with the previous year. State Street is also the only firm of the three whose support for key resolutions has risen.

Percentage of U.S. Key Shareholder Resolutions Supported

Overall, investors who are inclined to support sustainability-focused resolutions are likely to be more comfortable with State Street’s or BlackRock’s voting pattern than with Vanguard’s. Of course, the reverse would be true for investors who are inclined to reject such proposals.

However, irrespective of their overall stance, investors with particularly strong leanings in either direction in these matters may not be satisfied with any of the options shown above. This is where the alternative options under proxy-voting choice come into their own.

What Other Voting Policy Options Are on Offer?

The exact policy options that will be made available to individual investors are still subject to confirmation in many cases, and we expect to hear more from the firms in 2024. But we can draw some insights from the alternative policies that have already been offered to institutional investors. The alternative voting policies offered by the Big Three are usually compiled by one of the two major proxy advisors, ISS and Glass Lewis. At present, only BlackRock offers policies by both.

Besides the house voting policy, all three firms offer at least two kinds of alternative voting policies: sustainability-focused policies and board-aligned policies. BlackRock and State Street also allow investors to select the proxy advisors’ benchmark policies, which are the standard policies they publish to be used by voters without specific ESG goals. BlackRock also offers a corporate-governance-focused policy from ISS. Vanguard also offers investors the option not to cast a vote.

- Sustainability-focused policies are much more likely to recommend votes in support of ESG shareholder proposals, or against board director elections, compared with the house policy at any of the three firms. This group includes the ISS Sustainability and Socially Responsible Investment policies offered by BlackRock and State Street, and the Glass Lewis ESG policy offered by State Street and Vanguard. BlackRock also allows investors to choose Glass Lewis’ Climate Policy.

- Proxy advisors’ benchmark policies are also more likely to support ESG shareholder resolutions compared with the firms’ house policies. ISS typically supports more of these proposals than Glass Lewis. These policies oppose director elections less frequently than the sustainability-focused ones but more often than the three managers’ house policies.

- Board-aligned policies simply reflect the board’s voting recommendation at each company, which means they will almost never support a shareholder proposal or oppose director elections or other management proposals. All three firms now offer board-aligned policies.

- Corporate governance-focused policies generally side with management on most issues that come to a vote. In that sense, they are similar to board-aligned policies. Shareholder proposals on corporate governance themes, which generally advocate to improve shareholder rights, are the exception. As you would expect, voting decisions made under corporate-governance-focused policies support more of these resolutions.

BlackRock and State Street also offer specialty policies with more specific voting requirements to accommodate Catholic faith-based voting decisions, requirements for public fund investors, and those prioritizing labor relations issues under the Taft-Hartley Act.

How the ‘Magnificent Seven’ Affects Voting

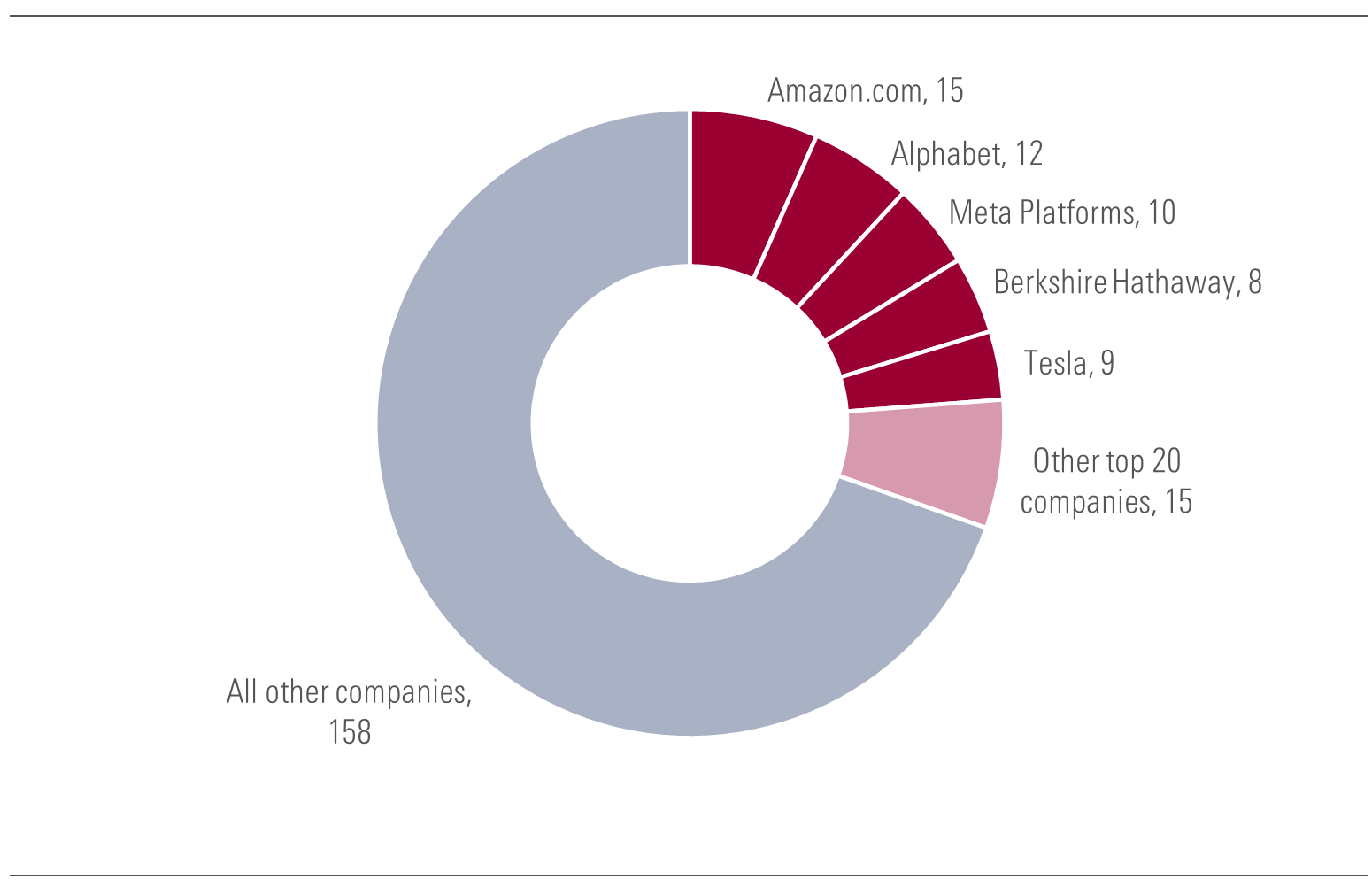

Much has been written about the increasing concentration of the U.S. stock market in a handful of mega-cap companies that dominate broad index performance. This concentration is also apparent when we look at key shareholder resolutions.

Mega-cap companies make attractive targets for proponents of shareholder resolutions, as they receive a lot of public attention. For that reason, the list of resolutions at companies like Alphabet GOOG, Amazon.com AMZN, and Meta Platforms META has been growing.

As the chart below shows, almost one third of the key ESG shareholder resolutions in the last three proxy years were filed at the top 20 companies in the S&P 500. Just five companies—Amazon.com, Alphabet, Meta, Berkshire Hathaway BRK.B, and Tesla TSLA—represented almost one fourth of the total. Other top 20 companies with several key resolutions over the period include Exxon Mobil XOM, Eli Lilly LLY, Home Depot HD, Johnson & Johnson JNJ.

Number of Key Shareholder Resolutions

Out of the funds eligible for proxy choice mentioned above, almost all have relatively high exposure to these mega-cap companies. (The SPDR S&P Dividend ETF is the only exception.)

So, for investors, it’s important to note that when using proxy-voting choice, the level of voting alignment with one’s own values will often depend significantly on voting decisions made at only a few high-profile companies. Morningstar frequently covers these important company meetings throughout the proxy season and will continue to do so in 2024.

Data From the 2023 Proxy Season Delivers Early Insights

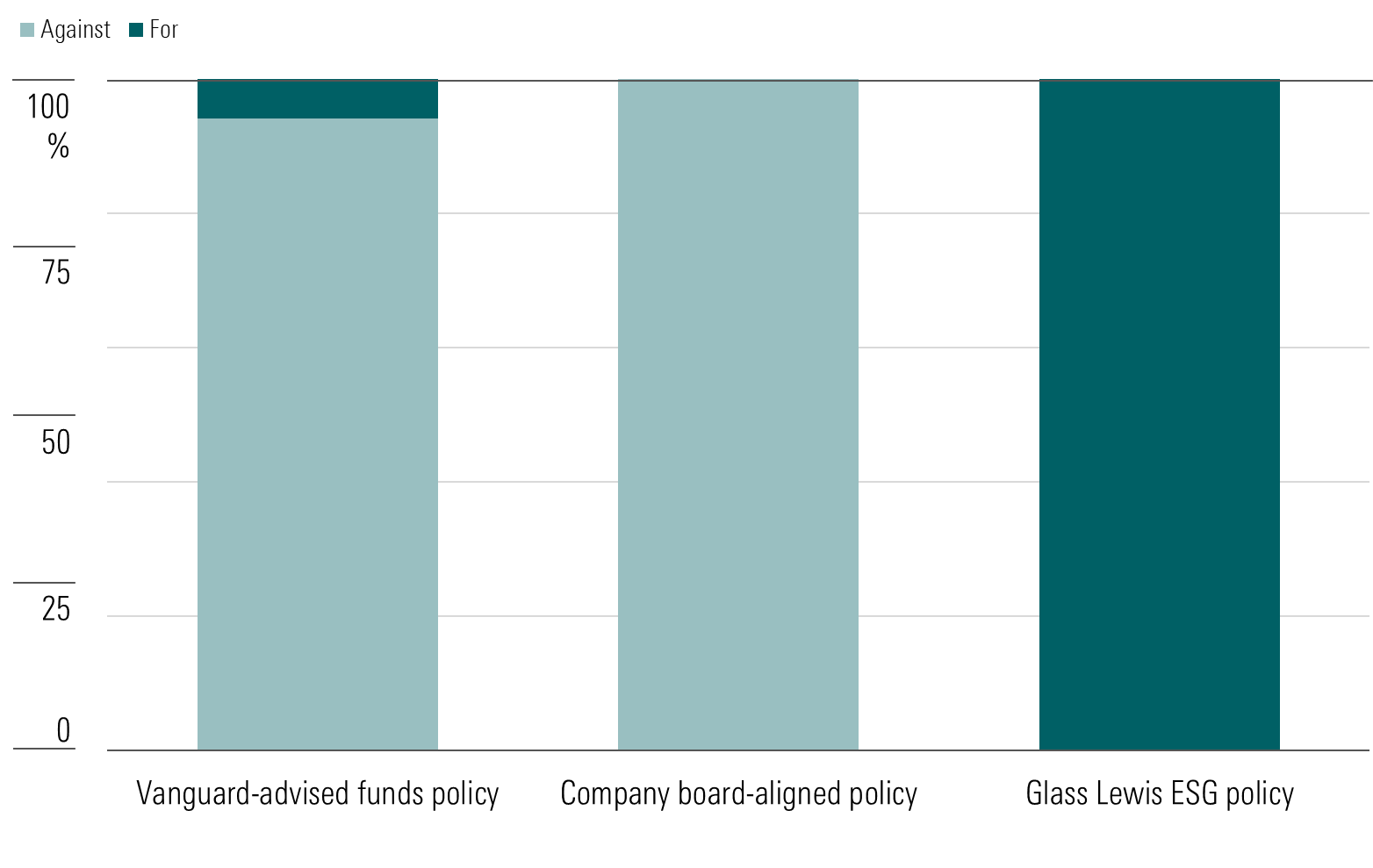

We have a good illustration of this from voting disclosures from Vanguard’s proxy-voting choice pilot in the 2023 proxy year. The chart below shows voting decisions implemented under Vanguard’s house policy, and the two alternative voting policies the firm offers, on 17 key resolutions at Alphabet, Amazon.com, Berkshire Hathaway, McDonald’s MCD, Meta, and Walmart WMT.

The 17 resolutions covered a wide range of topics, including climate risk management, workers’ rights, political influence, online safety, racial equity, and ethical use of advanced technology.

The alternative policies performed as could be expected. Votes under the Glass Lewis ESG policy supported all 17 resolutions, while those under the board-aligned policy voted against all 17. Vanguard’s house policy supported just one resolution, a repeat request for reporting on climate risk management at Berkshire Hathaway, rejecting the other 16.

Vanguard Proxy-Voting Choice

This shows that, in Vanguard’s case, there is likely to be very little difference between a board-aligned policy and the house policy when it comes to support for ESG shareholder resolutions. (We note that Vanguard is slightly more likely to vote against the board recommendation on governance-focused shareholder proposals. Based on the firm’s stewardship reporting, we estimate that Vanguard supported around 9% of these proposals in the U.S. in the 2023 proxy year.)

Conversely, sustainability-conscious investors in Vanguard ESG U.S. Stock ETF may feel that the voting record under the ESG policy option is a better fit with their objectives, given its high support for the key resolutions we observed. We expect to have better information on voting records under alternative voting policies for all three firms in the coming proxy season.

What Should Investors Do?

In light of all this, now is a good time for investors in eligible funds to assess whether their views on sustainability and governance themes are aligned with the voting records of their manager. Morningstar’s research on the topic can certainly help them make that assessment, including our latest ESG Commitment Level assessment for over 100 managers globally.

Ahead of the 2024 proxy season, which kicks off in February, it may be a good opportunity to assess whether an alternative voting policy, or even a similar fund by a different manager, could provide better alignment with one’s own personal values.

In January, we’ll publish a detailed analysis of asset managers’ voting records in the 2023 proxy season, which will be a helpful guide for investors seeking to make that assessment. Stay tuned for that.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/YGF5R6YDPJESJOU7XABKHHIP3Q.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/C3BD5QQZTNEMBAM7D35YO7ZH6A.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/FGC25JIKZ5EATCXF265D56SZTE.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/20726617-027d-4959-87ab-429b60ece7ce.jpg)