Turbulent September Markets Put ETF Investors on Defense

U.S. ETFs collected modest inflows as stocks and bonds sold off last month.

/s3.amazonaws.com/arc-authors/morningstar/30e2fda6-bf21-4e54-9e50-831a2bcccd80.jpg)

September lived up to its reputation as the worst month of the year for investors. A cocktail of persistent inflation, the Russia-Ukraine conflict, pandemic lockdowns in China, and ominous outlooks from major companies sent the Morningstar Global Markets Index, a broad gauge of global equities, into a 9.63% September decline. That marked its worst month since March 2020. Bonds offered little stability. The Morningstar US Core Bond Index pulled back 4.43%, its deepest one-month drawdown in over 20 years of live and back-tested performance.

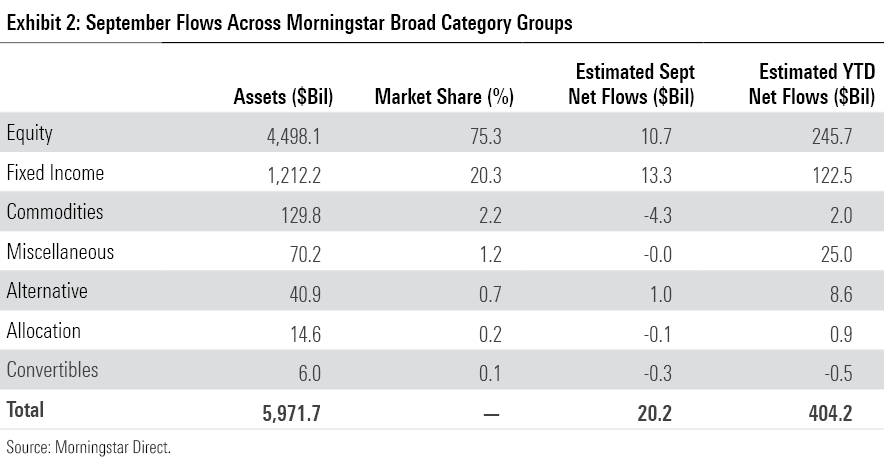

The grim landscape dampened investor enthusiasm, but U.S. exchange-traded funds still finished the month with inflows totaling $20.2 billion. Investors’ desire for stability made short-dated U.S. Treasury funds a popular choice and helped fixed-income funds reel in $13.3 billion last month. Meanwhile, stock ETFs pulled in a modest $10.7 billion as flows into U.S. equity strategies offset outflows from international and sector equity funds. With one quarter remaining on the calendar, U.S. ETFs have absorbed $404.2 billion this year and held nearly $6 trillion of investors’ cash.

Here, we’ll take a closer look at how the major asset classes performed last month, where investors put their money, and which corners of the market look rich and undervalued at month’s end—all through the lens of ETFs.

Stocks and Bonds Backpedal

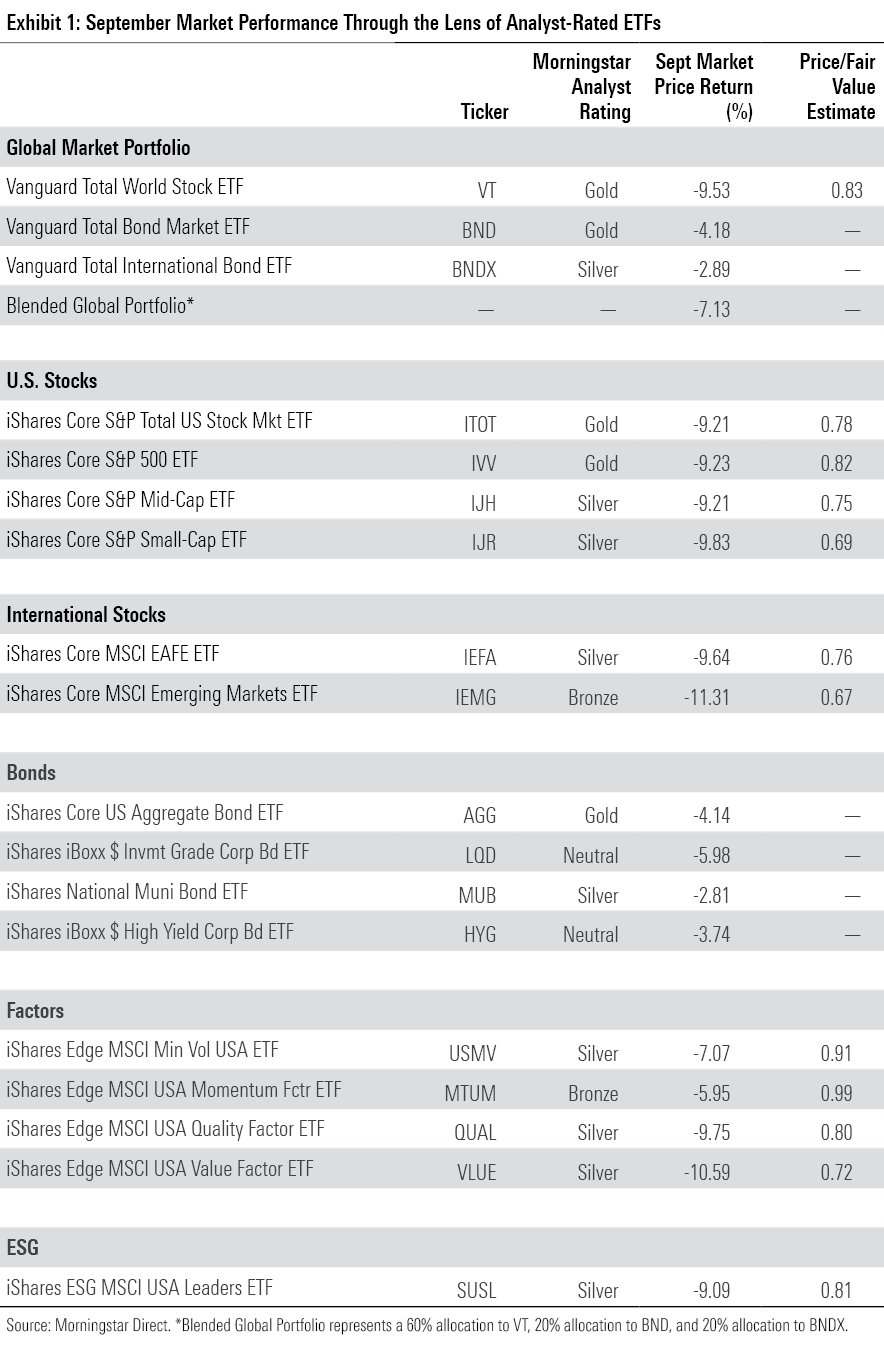

Exhibit 1 shows September returns for a sample of Morningstar Analyst-rated ETFs that serve as proxies for major asset classes. Investors in a blended global portfolio lost 7.13% last month.

Bonds were not able to stabilize the blended portfolio in September, in the latest chapter of a story that has unfolded all year. Vanguard Total International Bond ETF BNDX retreated 2.89%, and Vanguard Total Bond Market ETF BND fell 4.18%, the worst month on its 15-year track record. Stocks and bonds historically show low correlation to one another, but they have followed similar trajectories this year. Over the 10 years through 2021, BND posted a 0.02 correlation to Vanguard Total World Stock ETF VT. That number leapt to 0.79 over the first three quarters of 2022. Similar directional performance between stocks and bonds does not mean the two cannot coexist in a diversified portfolio. Rather, it’s a reminder that a low historical correlation is no guarantee that two assets will move in opposite directions.

Still, stocks have felt more acute pain than bonds this year. Their negative momentum from late August carried into September. VT booked a 9.53% loss last month, which marked a fresh bottom for the current bear market.

International equities slid a bit further than their U.S. counterparts. Vanguard Total International Stock ETF VXUS shed 9.91% of its value in September. Asia-Pacific stocks, which represented nearly half of the portfolio at September’s end, weighed on returns. The Morningstar China Index tumbled 14% in September, stunted by the economic impact of pandemic-driven lockdowns. Other Asian markets wobbled owing to close trade ties with China and/or their focus on the technology sector, which has been hammered by interest-rate hikes around the world. IShares ETFs that track the broad Japanese, Chinese, South Korean, Taiwanese, and Australian markets all fell at least 10% in September.

It's been far from smooth sailing in the United States as well. Vanguard Total Stock Market ETF VTI spiraled 9.22% last month thanks to a panoply of factors, including hotter-than-expected inflation, an interest-rate hike, economic forecasts from the Federal Reserve that implied two more interest-rate raises this year, and ominous guidance from blue-chip firms like FedEx FDX.

Every U.S. equity sector finished last month in the red, but the statistically cheaper ones mostly held up better. Using the SPDR suite of sector ETFs as proxies, healthcare, financials, and consumer staples were the three best-performing sectors. Pharmaceutical companies fared relatively well, as behemoths like Johnson & Johnson JNJ, Eli Lilly LLY, and Merck MRK all scratched out positive September returns. No stock in the S&P 500 Index had a better month than Biogen BIIB, which rode encouraging phase 3 data from its Alzheimer's Disease drug lecanemab to a 36.66% September gain.

Relatively solid returns from the healthcare, financials, and consumer staples sectors helped Vanguard Value ETF VTV beat Vanguard Growth ETF VUG by 2.64 percentage points in September. Those three sectors collectively shape 52% of VTV and only 13% of VUG. Over the year’s first three quarters, VTV’s 14.5% drawdown was less than half that of VUG, which has lost about one third of its value. Growth stocks tend to fare worse than value stocks in rising-rate environments because their forecast cash flows are further in the future, making them more sensitive to increases in the discount rate. That said, the value factor may not be able to chalk up September as a true win. IShares MSCI USA Value Factor ETF VLUE pursues the cheapest stocks within each sector and slid 10.59% last month, which indicates that VTV’s sector composition likely powered its September success.

Returns have been even along the market-cap ladder this year. After iShares Core S&P 500 ETF IVV held up about 60 basis points better than iShares Core S&P Small-Cap ETF IJR in September, the former now trails the latter by 82 basis points for the year to date. Both, however, are behind iShares Core S&P Mid-Cap ETF IJH, whose 21.57% year-to-date pullback is about 1.5 percentage points better than IJR's.

This fund, which tracks the S&P MidCap 400 Index, has also beaten mid-cap competitors iShares Russell Mid-Cap ETF IWR and Vanguard Mid-Cap ETF VO by 2.75 percentage points and 3.88 percentage points, respectively. IJH’s profitability screen, modest value tilt, and smaller market-cap orientation have worked in its favor this year. In fact, IJH and VO—a pair of mid-cap index funds with several hundred positions each—share only six holdings. Differences in their index construction have led to disparate performance, reinforcing the importance of looking beneath funds’ labels.

IShares MSCI USA Minimum Volatility Factor ETF USMV has found its footing after stumbling earlier this year. The low-volatility strategy trailed the Morningstar US Market Index over the first two months of the year, prompting questions over the caliber of its downside protection. But it has responded well. The fund beat the Morningstar US Market Index by about 7.5 percentage points for the year to date through September, which translates into a 73% downside-capture ratio versus that index, a number on par with its performance in prior drawdowns.

Widespread challenges have left stocks undervalued all over the board. As measured by the Morningstar price/fair value ratio, iShares Core S&P Total U.S. Market ITOT traded 22% below its fair value at September’s end. Exhibit 1 indicates that emerging-markets stocks (33% discount), small-cap U.S. firms (31%), and U.S. value companies (28%) are especially attractive areas of the market.

The Safety Dance

U.S. ETFs collected $20.2 billion in September. That marks their mildest month of inflows this year, though they surrendered $11.8 billion in April. Three quarters into 2022, ETFs have hauled in over $404 billion of new investor money.

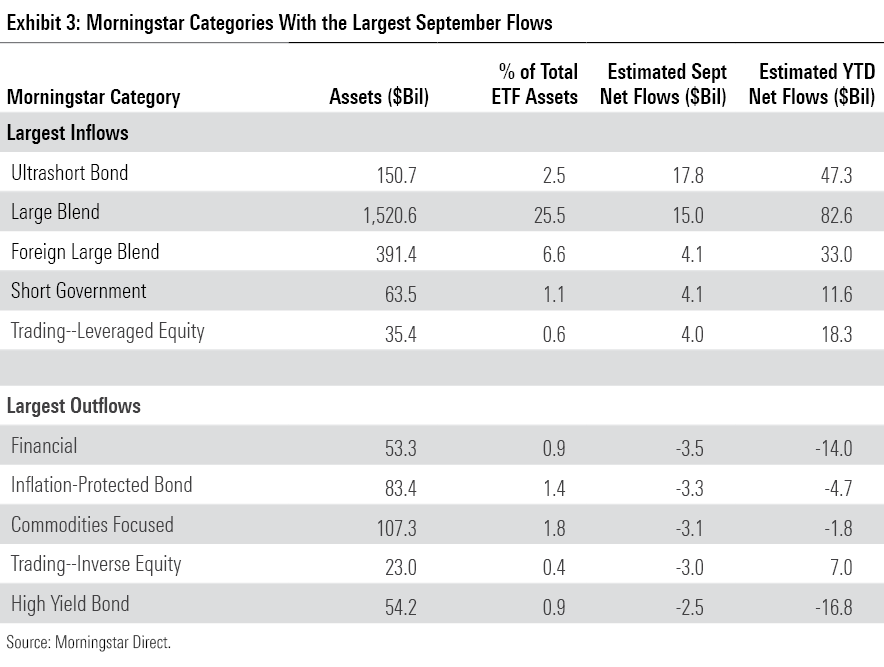

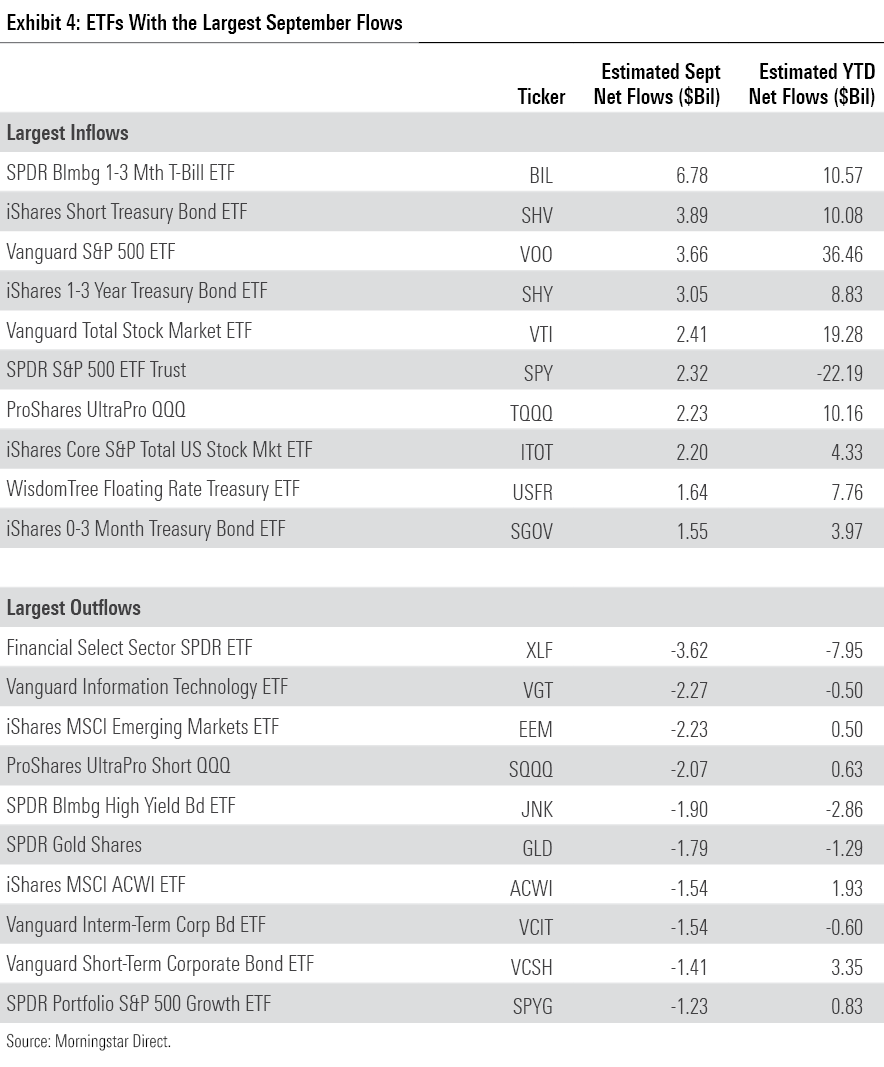

The ultrashort bond Morningstar Category led all categories with $17.8 billion of inflows last month. That translated into a 13.4% organic growth rate for the category, whose $47.3 billion year-to-date haul ranks third among all fund categories. Five different ultrashort bond funds reeled in more than $1 billion, headlined by SPDR Bloomberg 1-3 Month T-Bill ETF BIL, which reeled in $6.8 billion. Ultrashort bond funds are some of the most conservative on the market, often performing similarly to cash. As the prospect of further interest-rate increases continued to cast a cloud over longer-dated bond funds, investors turned to ultrashort bond ETFs to pull interest-rate risk off the table.

Bond ETF investors averted credit risk last month, too. All U.S. government-backed bond categories finished September in positive flows territory, led by short-term government funds ($4.1 billion inflow). On the other hand, riskier bond categories were some of the September’s least popular. High-yield bond, corporate bond, and bank-loan funds—all of which shoulder more credit risk than the broad bond market—bled between $2 billion and $2.5 billion apiece in September. These funds can post attractive returns when credit spreads tighten, but their stocklike performance this year has spelled trouble. For example, iShares iBoxx $ High Yield Corporate Bond ETF HYG slid 15.25% over the first three quarters, suffering $6.4 billion of outflows along the way. When investors seek downside protection, these funds tend to fall out of favor.

Value funds continued to attract more investment than growth-oriented ETFs in September. After investors piled $3.5 billion into the large-cap value category and a modest $16 million into large-growth funds, the categories’ year-to-date inflows stand at $68.7 billion and $17 billion, respectively. Much of the large-value category’s popularity owes to dividend ETFs. These strategies have reeled in $44.2 billion this year, or 64% of net large-value flows. Funds like Schwab U.S. Dividend Equity ETF SCHD and Vanguard High Dividend Yield ETF VYM have deftly navigated the difficult year, and investors have taken note: The funds pulled in $10.9 billion and $7.5 billion over the first three quarters, respectively.

Investors yanked $11.2 billion from sector equity ETFs last month, with all U.S. stock sectors but utilities finishing in outflows. Cyclical sectors bore the brunt of the outflows. Financials and technology ETFs surrendered $3.5 billion and $2.4 billion in September, respectively, adding to their outflows for the year to date. Many investors use sector ETFs as satellite positions that complement their core stock allocation. As the U.S. market continues to show little areas of reprieve, it appears that some investors have waved off their sector bets in favor of more-conservative, better-diversified options.

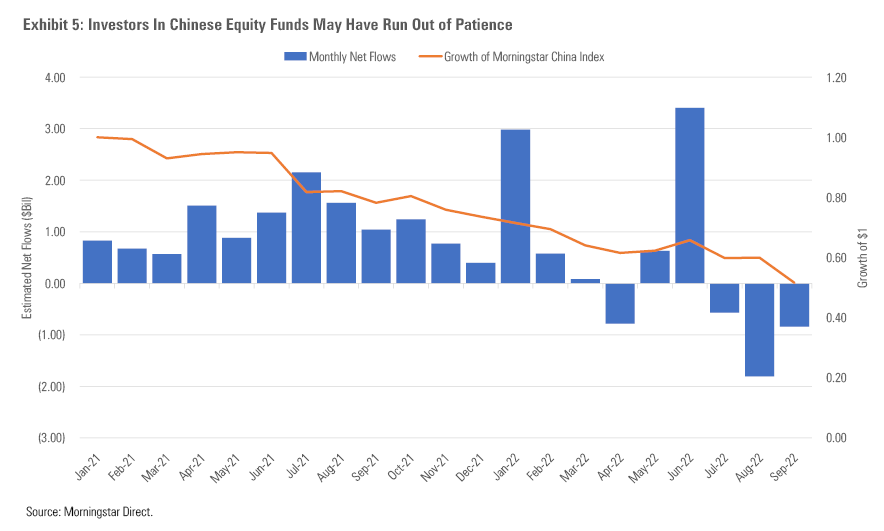

International equities posted modest outflows in September. Investors pulled $840 million from the China region category and $1.7 billion from diversified emerging-markets funds, many of which are heavily invested in Chinese stocks. The China market has moved in reverse since the start of 2021, but investors continued to double down until recently. In 2021, the China region category absorbed $13 billion as the Morningstar China Index plummeted 21.1%, nearly 40 percentage points behind VT. Exhibit 5 shows that some investors kept the faith as recently as June.

Commodity ETFs bled $4.3 billion in their fifth consecutive month of outflows. Investors loaded up on these funds to battle inflation at the start of the year but have since retracted nearly all that money. Over the first four months of the year, commodity ETFs hauled in $21.2 billion. Over the next five, they leaked $19.2 billion.

The State of State Street

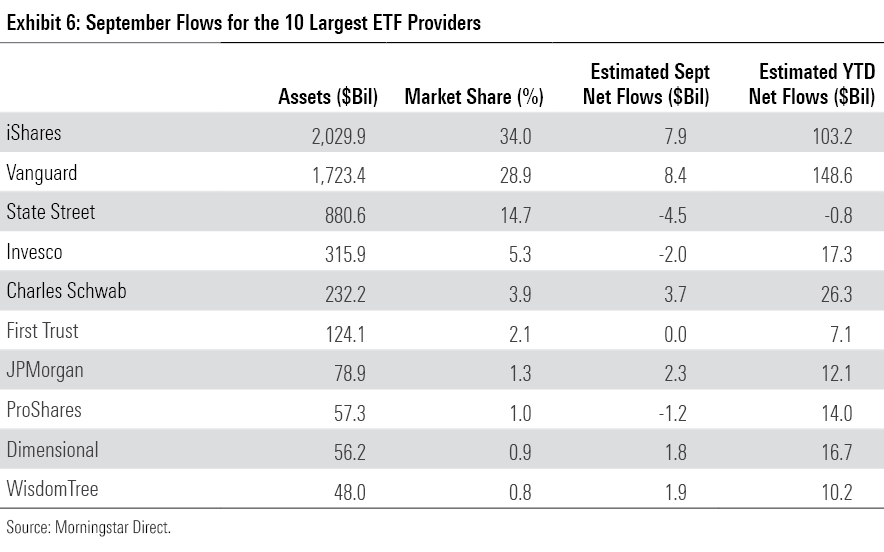

Vanguard led all fund families with $8.4 billion of inflows in September, the fourth month this year it’s finished atop the flow leaderboard. Vanguard’s bread-and-butter lineup of U.S. stock funds pushed it into first place. Core funds like Vanguard S&P 500 ETF VOO and VTI attracted enough new investment to offset outflows from the firm’s fixed-income and sector offerings.

That said, with three months left in the 2022 flows race, iShares rests in first place. Nearly $8 billion of September inflows raised the firm’s year-to-date sum to $65.3 billion, more than double that of its next-closest competitor Vanguard. IShares’ recent success owes to its fixed-income lineup. Its bond ETFs claimed about 63% of the firm’s inflows this year despite representing just one fourth of its total assets. Many investors in search of stability have found it in the form of Treasury funds like iShares 20+ Year Treasury Bond ETF TLT and iShares Short Treasury Bond ETF SHV.

Next to iShares and Vanguard, State Street rounds out the ETF industry Big Three. But the firm has not measured up well versus its two heftier peers this year. About $4.5 billion of outflows in September pushed State Street into negative flows territory for the year to date. The clear culprit is SPDR S&P 500 ETF Trust SPY. The storied ETF, with $22.2 billion of outflows over the first three quarters, is the worst of all ETFs by a wide margin. State Street’s clientele consists of more-tactical traders than Vanguard's. That has been a difficult investor base to serve in such a rocky stretch for markets. When newly minted State Street Global Advisors CEO Yie-Hsin Hung starts her tenure in December, she may face State Street’s first year of outflows since 2015.

Cannabis Funds Continue to Crumble

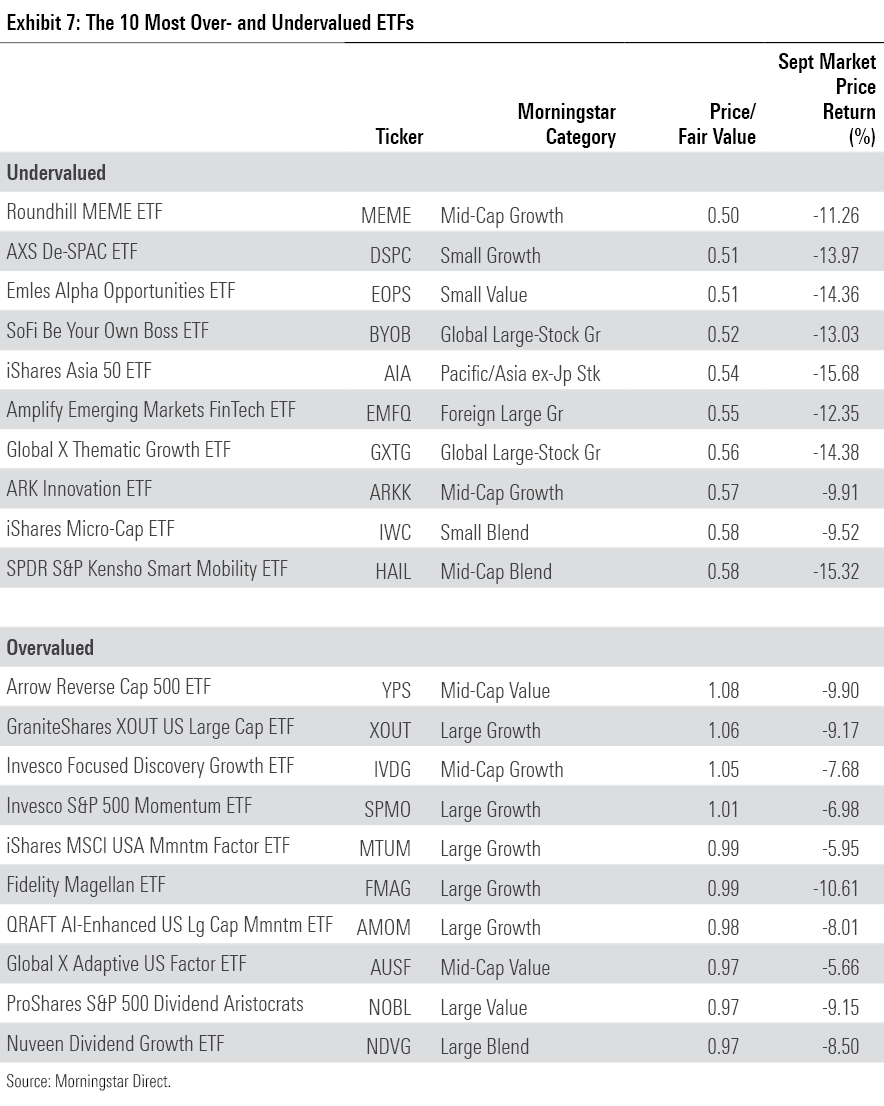

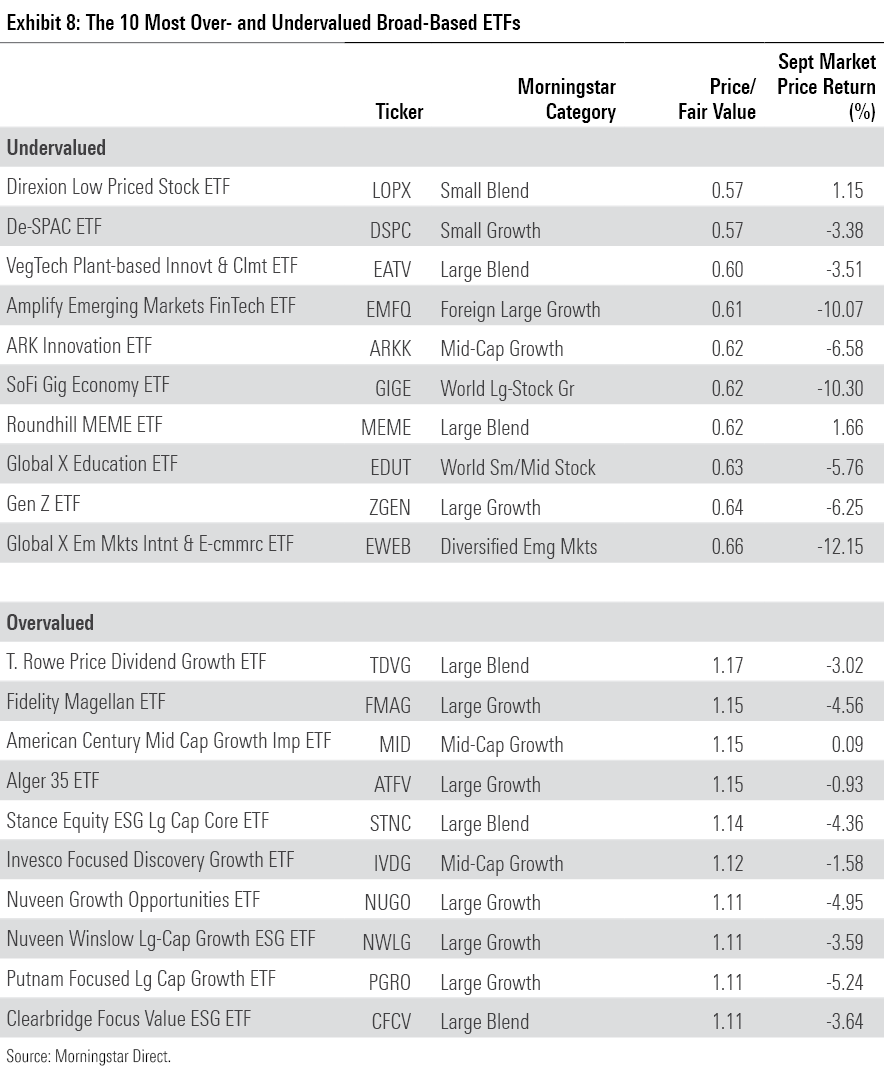

The fair value estimate for ETFs rolls up our equity analysts' fair value estimates for individual stocks and our quantitative fair value estimates for stocks not covered by Morningstar analysts into an aggregate fair value estimate for stock ETF portfolios. Dividing an ETF's market price by this value yields its price/fair value ratio. This ratio can point to potential bargains and areas of the market where valuations are stretched.

Funds that aim to leverage the legalization of cannabis or other drugs dominated the cheaper half of Exhibit 7, claiming eight of the available 10 spots. Each cannabis fund on the list traded at least 50% below their fair value at September’s end, as they could not arrest their free fall last month. The median U.S. cannabis ETF shed 59.5% of its value for the year to date through September. Cannabis ETFs have looked cheap for quite some time, but unfortunately for those that have stuck with these funds, they have not been able to launch a turnaround.

Perhaps none of the ETFs that constitute the more richly valued half of Exhibit 8 have had a more interesting year than iShares MSCI USA Momentum Factor ETF MTUM. This fund selects and weights 125 U.S. stocks by their exposure to momentum, a well-vetted risk factor that has historically been tied to outperformance. Market momentum can shift on a dime, which can make this fund look quite different from one semiannual rebalance to the next. When the fund reshuffled in May, it prioritized recent winners in sectors both defensive (utilities, healthcare, consumer staples) and statistically cheap (energy, financials). That sector shuffle led to an up-and-down summer. The fund ranked within the bottom decile of the large-growth category when faster-growing, more-cyclical stocks came to life in July. But the fund landed in the category’s top decile in August and September, when cheaper, safer stocks fared best. Whichever corners of the market this fund holds, investors should expect its price/fair value ratio to look relatively steep.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/24UPFK5OBNANLM2B55TIWIK2S4.png)

/d10o6nnig0wrdw.cloudfront.net/04-25-2024/t_29c382728cbc4bf2aaef646d1589a188_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/30e2fda6-bf21-4e54-9e50-831a2bcccd80.jpg)