Travel and Leisure Stocks Look Attractive

Consumers are slowly starting to travel and eat at restaurants again.

/s3.amazonaws.com/arc-authors/morningstar/c612f59b-89e0-422a-8f71-3eb1300d1a2c.jpg)

Although uncertainty surrounding the coronavirus pandemic affected consumer cyclical companies more than others at its peak, the industry has begun to rebound. Trailing 12-month returns for the sector are up 37% compared with the market’s 23% return, which runs in sharp contrast to a quarter ago, when the sector lagged the market’s performance by 300 basis points.

The sector has begun to outperform the market. - source: Morningstar

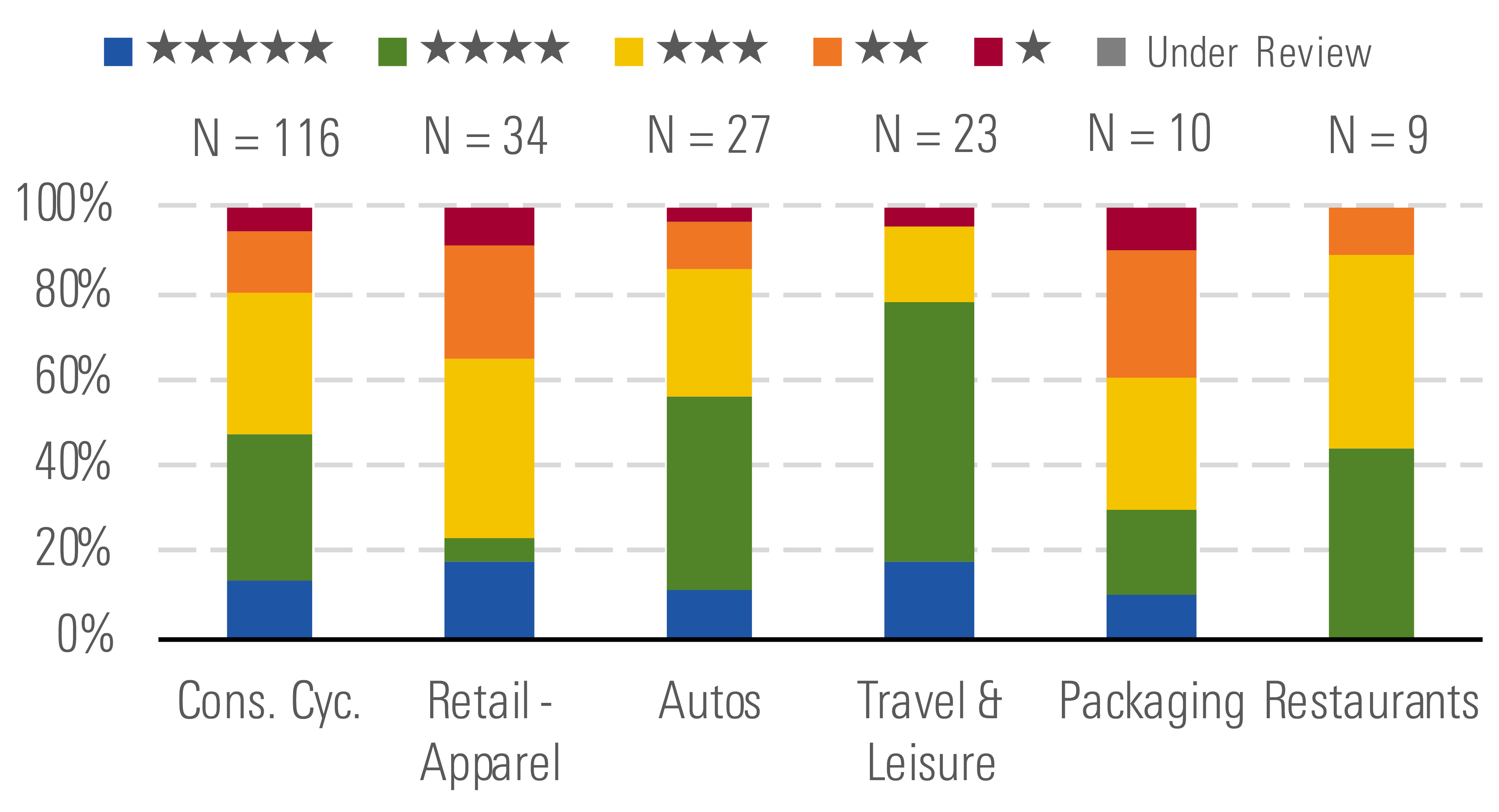

Despite the appreciation, we still think the sector offers pockets of value. We continue to see significant opportunity in travel and leisure, with shares in the subsector trading at a median price/fair value estimate discount of more than 20%, with more than half of our coverage trading in 4- or 5-star territory.

But opportunities remain across every subsector. - source: Morningstar

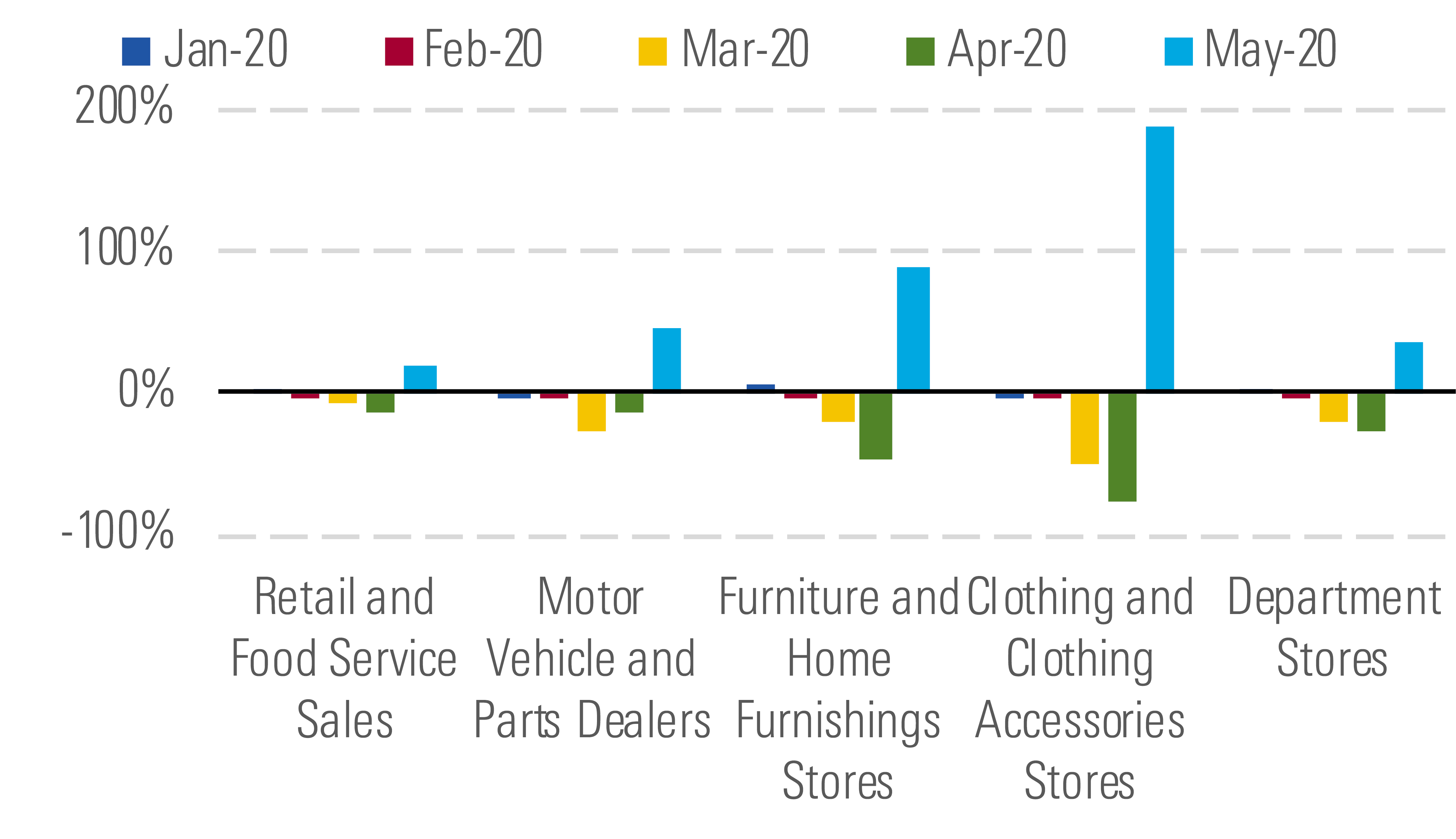

As states start to lift mandatory lockdowns, which has extended to include the reopening of nonessential businesses, we think consumers’ pent-up demand could aid the trajectory of these more discretionary operators. This is already playing out, as May retail sales data (up nearly 18% on an adjusted basis month over month) pointed to growth in many areas, including home furnishings, retail apparel and accessories, and automotive parts. While we think the pace of spending could prove lumpy, we believe the bulk of the retraction in consumer spending was likely concentrated in the second quarter, buoying our expectations for further sales gains over the next few quarters.

Recent retail sales data suggests growth is returning to the sector. - source: Morningstar

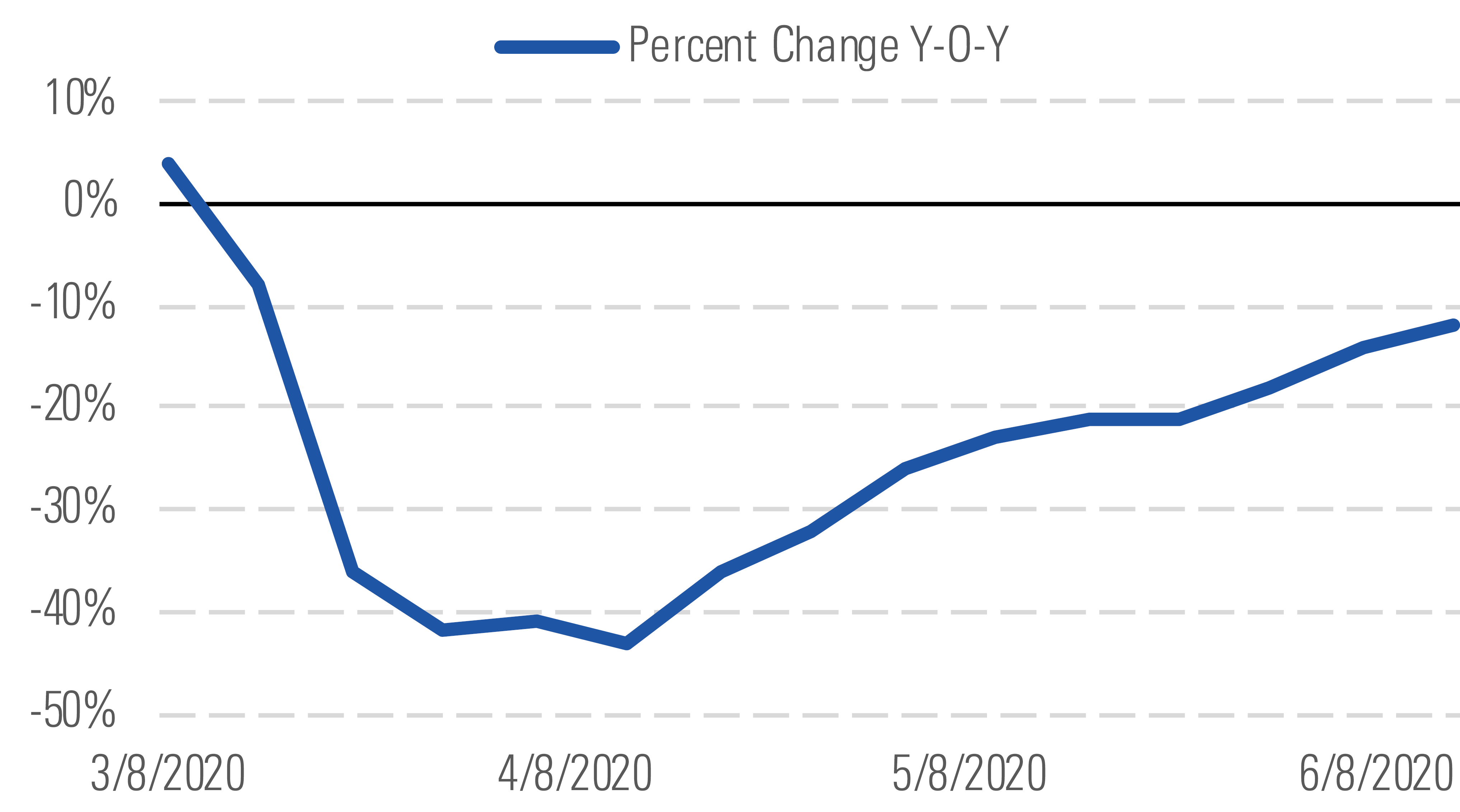

We also believe consumers are ready to resume consuming food away from home, albeit slowly, as social distancing requirements are relaxed. We’re already seeing a moderation in the decline of U.S. chain restaurant transactions and expect these trends to continue into July. As of the beginning of June, over 68% of restaurant units have reopened according to market researcher NPD Group. However, we expect uneven traffic at restaurants in the back half of the year, as they may need to reduce capacity again if a second wave of the pandemic appears, and consumer spending is impaired by still-elevated unemployment. We believe that companies with the scale to be more aggressive on pricing in the near term (value-oriented players tend to outperform during economic shocks) and those with robust mobile platforms and healthy balance sheets (both at the corporate and franchisee level) are best positioned to weather this uneven recovery period.

As restaurants reopen, transaction declines at chains are improving. - source: Morningstar

Top Picks

Hanesbrands HBI Economic Moat Rating: Narrow Fair Value Estimate: $23 Fair Value Uncertainty: Medium

We believe narrow-moat Hanesbrands’ transformation is underappreciated, with investors focused on its low-growth innerwear operations and partial dependence on U.S. physical retail. But through a series of acquisitions since 2013, the firm transformed its brand portfolio into a more diversified and global operation with higher returns. While the coronavirus has slammed all apparel firms, we think Hanes may recover faster than most because its products have limited fashion risk, are purchased regularly regardless of economic conditions, and are available in a vast array of retail outlets, some of which didn’t close during the pandemic.

Tapestry TPR Economic Moat Rating: Narrow Fair Value Estimate: $35 Fair Value Uncertainty: High

We view Tapestry as attractive, trading at about a 60% discount to our intrinsic value. Although Tapestry’s efforts to fix its Kate Spade and Stuart Weitzman brands have stalled, we believe its successful restructuring of Coach (71% of 2019 revenue) will bolster returns. While the short-term outlook is murky as a result of the pandemic, we don’t think Coach’s brand strength (the source of our narrow moat rating) or the firm’s financial health will be impaired. We expect this brand strength and pricing power to support revenue growth for the firm in the long term, particularly given the opportunity we see to grow the brand in China.

Macy's M Economic Moat Rating: None Fair Value Estimate: $17.60 Fair Value Uncertainty: High

Although Macy’s has struggled to find growth in recent years as consumers have moved to e-commerce and discount stores and away from department stores, we still believe it is an attractive investment at around a 60% discount to our fair value estimate. Macy’s is one of the 10 largest e-commerce companies in the U.S., and its digital sales jumped 80% in May while its stores were closed due to the pandemic. We believe Macy’s will close its worst-performing stores soon and that the downsized firm will return to profitability next year. Our long-term view assumes no sales growth but operating margins of about 5%.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/RNODFET5RVBMBKRZTQFUBVXUEU.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LJHOT24AYJCHBNGUQ67KUYGHEE.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/V33GR4AWKNF5XACS3HZ356QWCM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/c612f59b-89e0-422a-8f71-3eb1300d1a2c.jpg)