Obesity Drug Stocks: Where to Invest Now

Eli Lilly and Novo Nordisk have staged big rallies. Here’s how investors can approach this potentially huge opportunity.

Pharmaceutical investing has seen huge moves this past year, with one area grabbing particular attention: obesity drugs.

Since the end of 2022, the booming market—and potential for massive growth—for obesity drugs has led to big rallies for the stocks of the two manufacturers leading the race to market: Novo Nordisk NVO, producer of Ozempic and Wegovy, and Eli Lilly LLY, which manufactures Mounjaro and Zepbound. Both stocks are posting their biggest gains when it comes to year-to-date performance since 1997.

The challenge is that both stocks currently trade in overvalued territory, according to Morningstar analysts. Investors looking to put new money to work in companies developing products in this potentially significant market must decide which of the more attractively valued competitors are best positioned to muscle their way in.

“While Eli Lilly and Novo deserve a premium, the current valuations seem to imply too much of a premium, and don’t fully factor in the challenges from pricing, competition, and side effects,” says Damien Conover, director of healthcare research for Morningstar.

Other Big Pharma companies looking to gain traction with their own obesity drugs include Roche RHHBY, Pfizer PFE, and Amgen AMGN.

Key Obesity Drug Stocks and Their 12-Month Performance

- Novo Nordisk: 56.8%

- Eli Lilly: 61.1%

- Pfizer: -38.8%

- Amgen: -1.9%

- Roche: -7.8%

Obesity Drugs’ Sudden Impact On Pharma Stocks

Amid the obesity epidemic in the United States, for years, pharmaceutical companies have been attempting to develop effective treatments. “I don’t think we’ve ever seen this sort of level of innovation,” Conover explains. “Historically, obesity has been an area of a lot of failed drug development. It’s always dangerous to say, ‘This time, it’s different.’ But this time, it really does seem different.”

Karen Andersen, a healthcare strategist at Morningstar, notes that many investors initially didn’t seem to pay much attention. “The first clear phase 3 data for Wegovy came out in June 2020 with about 15% weight loss. The stock barely moved,” she says. “Wegovy was approved in June 2021. The stock went up a little, but the shortages were so bad that sales didn’t really start to take off until toward the end of 2022. That’s when sales started exploding and it became clear what the demand was for these drugs … and though there are gaps in coverage, a lot of plans are covering them.”

Andersen continues: “So it was a sort of slow realization after the data, approval, shortages ... and then it took off. I think we had all been expecting less, given that the launch of Novo’s previous obesity drug, Saxenda, wasn’t very successful—albeit with about 5% weight loss.”

However, investors have now definitely taken note, changing the landscape of pharma stocks. That came in part as Lilly has seen unparalleled efficacy in its weight-loss drug therapy, and its stock reflects that progress with its big 2023 rally. Meanwhile, Novo is now the largest company in Europe as measured by market capitalization.

Stock Performance of Obesity Drug Developers

Obesity Drug Market Potential

Underlying these gains are expectations of massive growth for these drugs. Conover and Andersen project that the global market for obesity drugs will be more than $100 billion in 2032. The overall market for the kinds of treatments employed in these medications—which are known as GLP-1s and are also used to treat Type 2 diabetes—is seen as even larger, at some $168 billion.

Conover and Andersen forecast that over 25% of obese Americans and 15% of overweight Americans will receive treatment in 10 years, and the vast majority will receive branded GLP-1 therapies. They predict the bulk of those sales will go to Novo and Lilly.

Global Projection of Obesity Drug Developer Sales

Obesity Drug Stock Variables

With new gates being opened for these drugs, investors have multiple variables to consider when it comes to stocks that can benefit.

One of the biggest factors will be pricing—both the prices manufacturers can charge and what end consumers pay after insurance. Both Lilly’s Zepbound and Novo’s Wegovy have a listed monthly price over $1,000. But this is not necessarily reflective of what the typical consumer will be billed; the net payment could be discounted by as much as 79%. Such pricing could make a big difference in sales. “It’s such a big market that you don’t need to change the penetration levels that much and you would have substantially different projections,” says Conover.

Meanwhile, already-intense competition is being fueled by a steady stream of studies of drug effectiveness. Truveta recently published the first comparative study between Lilly’s Ozempic and Novo’s Mounjaro, which found that patients taking the Lilly product were three times more likely to achieve 15% weight loss than those taking Novo’s.

That competition is part of the reason Conover and Andersen expect a substantial pricing decline over time. They estimate companies are currently charging an average of $7,000 for obesity drugs, but that will likely decline to under $3,000 by 2031.

Obesity Drug Costs

“Competition and efforts to expand commercial—private payer—reimbursement contracts tend to lead to lower prices at bigger volumes,” Andersen says.

Though many unforeseen corners could lie ahead, one thing is clear: Lilly and Novo revolutionized the weight-loss landscape through years of continual therapy improvements. “They had been on this steady path until they got to the point where this obesity data came out,” Andersen explains. “It had somehow broken through this barrier for prior obesity drugs, since their efficacy was undeniable, and it really turned a corner.”

Which Obesity Drug Stocks Should You Buy Now?

“Novo and Lilly are kind of doing their own thing in the stock market, and really in innovation,” says Conover. “They are bringing out some of the most powerful new drugs for sales generation, in our estimation.”

Andersen says, “I think we’re at a point in this market where it’s accepted that Novo and Lilly are both strong players and poised to benefit incredibly. I think it would be tough to really take down either, unless there was some drastic reduction in supply or a massive safety issue that we somehow didn’t see until now.”

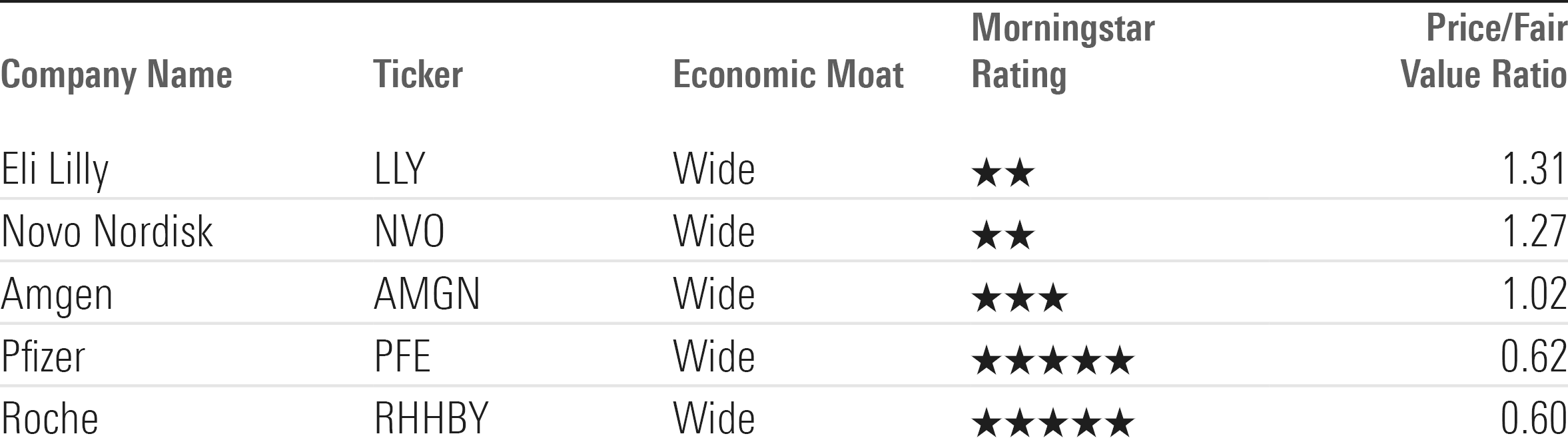

However, for investors, there are valuations to consider. Lilly is currently trading at a price/fair value ratio of 1.31, meaning it is 31% overvalued compared with Conover’s fair value estimate of $450. Meanwhile, Novo has a price/fair value ratio of 1.27, based on Andersen’s fair value estimate of $80.

Price/Fair Value Ratios of Obesity Drug Developers

“Lilly in particular is moving dramatically differently than the rest of the group,” Conover explains. “Its price/earnings multiple is much higher than the average, close to 50 times, while the group average is about 15 times ... Novo also trades at a pretty high premium.” But competitors are doing their best to gain entry.

Pfizer has been considered a significant contender, but on Dec. 1, the company announced it was stopping work on a twice-a-day version of its oral obesity drug danuglipron, due to a high level of unfavorable side effects. On that news, Conover lowered his fair value estimate for the company’s stock to $47 from $48 per share.

“Pfizer is still in the hunt here, but the setback will likely delay them at least a year,” Conover says. However, he sees the stock as undervalued, with “a broad portfolio of currently marketed products and a robust pipeline to support its wide moat.”

Another aspirant is Amgen. “They are committed to entering the obesity market—either with the lead candidate (similar to Lilly’s Zepbound, it’s targeting GLP-1 and GIP) or additional drugs that are in phase 1 and preclinical studies,” says Andersen. “We expect phase 2 data from the lead AMG133 program in the second half of 2024. The key selling point so far, based on phase 1 data, could be that it requires less frequent administration—it could be administered monthly, instead of the weekly Zepbound—and may lead to longer maintenance of weight loss after stopping therapy.”

In addition, Andersen says Amgen’s offering has showed “compelling” speed of weight loss. “It will be interesting to see longer-term data to see the final plateau of weight loss.” She adds that given the minimal data so far from the company, “Amgen is sort of a wild card, as it could either be best-in-class or encounter issues with tolerability or safety that make it less compelling.”

Then there is Roche, which just this past week entered the fray with the acquisition of private biotechnology company Carmot, which has three clinical-stage obesity drugs in the works. “Investors might be better served by taking a less focused approach toward investing in obesity stocks and consider a firm like Roche, where we like the overall portfolio and investors get some exposure to new obesity drug development,” Conover says.

Here’s a look at Morningstar’s take on key obesity drug developers and their stocks:

Obesity Drug Developer Stocks

Eli Lilly

- Fair Value Estimate: $450.00

- Morningstar Rating: 2 stars

- Morningstar Economic Moat Rating: Wide

- Morningstar Uncertainty Rating: High

“We are raising our fair value estimate for Eli Lilly to $450 from $368 after updating our long-term GLP-1 model to include wider use of and greater adherence to these cardiometabolic drugs.

“Lilly’s internal pipeline is well-positioned to mitigate the patent losses during the next decade. The company tends to spend a low-to-mid-20s percentage of its sales on financing the development efforts of new drugs, much higher than the high-teens industry average. The robust pipeline is a result of Lilly’s strong commitment to research.

“We believe cardiometabolic drugs Mounjaro, Zepbound, Trulicity, and Jardiance, immunology drug Taltz, and cancer drug Verzenio hold the highest sales potential of Lilly’s currently launched drugs. Further, pipeline drugs lebrikizumab (atopic dermatitis), mirikizumab (immunology), and donanemab (Alzheimer’s) hold major blockbuster potential.”

Read more of Conover’s take on Eli Lilly.

Novo Nordisk

- Fair Value Estimate: $80.00

- Morningstar Rating: 2 stars

- Morningstar Economic Moat Rating: Wide

- Morningstar Uncertainty Rating: High

“We’re raising our fair value estimate of Novo Nordisk to $80 from $70 after updating our long-term GLP-1 model to include wider use and greater adherence.

“Growth is largely coming from GLP-1 therapies, which include daily Victoza, weekly Ozempic, and daily oral Rybelsus. Strong efficacy and cardiovascular benefits should allow Novo to continue growing sales of GLP-1 therapies in diabetes. While Novo lost share to Lilly’s once-weekly Trulicity, Ozempic’s recent launch, the launch of Rybelsus, and high-dose versions of each drug are revitalizing growth and expanding Novo’s reach. Lilly’s novel drug Mounjaro is again gaining share, although class growth is so strong that we expect both franchises to see double-digit growth for years to come.

“Semaglutide’s potential in new indications also gives us confidence in Novo’s wide moat. The drug received U.S. approval as Wegovy in obesity in June 2021, and is in phase 3 testing in areas like NASH, Alzheimer’s, and heart failure. Novo is also testing new combination regimens like cagrisema, which could offer even more compelling blood sugar control and weight loss, helping Novo maintain solid positioning against Lilly.”

Read more of Andersen’s take on Novo Nordisk.

Roche

- Fair Value Estimate: $59.00

- Morningstar Rating: 5 stars

- Morningstar Economic Moat Rating: Wide

- Morningstar Uncertainty Rating: Low

“Roche has announced that it will acquire private biotech Carmot Therapeutics for $2.7 billion upfront and an additional $400 million if certain milestones are reached in the firm’s obesity pipeline. Carmot has three clinical-stage obesity programs for patients with and without type 1 or 2 diabetes, including GLP-1/GIP weekly injectable CT-388 (ready to begin phase 2) and daily oral GLP-1 CT-996 (phase 1).

“We have slightly raised our fair value estimate of Roche stock to $59 from $56, as we’re including peak sales above the value of the transaction. Further data updates could lead us to increase our market share assumptions and give Roche a chance to become a significant player.

“We’re assuming CT-388 could reach the market by 2027 in obesity/overweight, with global sales approaching $4 billion by 2032. With our recently updated obesity market forecast, this implies a potential 3% share of the more than $100 billion opportunity in this space by 2032. Roche sees potential best-in-class efficacy for CT-388, which has phase 1b data showing 8.4% weight loss at four weeks at the highest dose, as well as no discontinuations for adverse events and rates of nausea and vomiting that appear similar to Wegovy. Carmot had planned to release additional data on higher doses of the drug in the first half of 2024. The rate of weight loss in phase 1b is much faster than seen with Novo’s Wegovy or Lilly’s Zepbound at four weeks, although the trial is small and longer-term data will be needed before we increase our estimates significantly.”

Read more of Andersen’s take on Roche.

Pfizer

- Fair Value Estimate: $47.00

- Morningstar Rating: 5 stars

- Morningstar Economic Moat Rating: Wide

- Morningstar Uncertainty Rating: Medium

“We have lowered our fair value estimate for Pfizer stock to $47 per share from $48, based on the disappointing phase 2 obesity study for danuglipron. We believe the unfavorable side effect profile (up to 73% rate of nausea) shown in the study would make the drug less competitive. While Pfizer is still evaluating the drug by formulating the dosing for once daily instead of twice, it will not move the drug forward into phase 3 development at the twice-daily dose. Given the setback, we believe the drug’s probability of success is lower, and we have significantly lowered our assumed peak annual sales potential from over $3 billion to less than $1 billion.

“Even following our fair value estimate reduction, we view Pfizer’s shares as undervalued. The firm maintains a broad portfolio of currently marketed products and a robust pipeline to support its wide moat. While the setback to danuglipron likely removes a key blockbuster opportunity, we expect Pfizer to move several new drugs into late-stage development over the next year.

“Further, if the once-daily reformulation of danuglipron is unsuccessful, we would expect Pfizer to continue development with another GLP-1 drug sourced internally or acquired from one of the several smaller firms developing drugs within this mechanism of action. We believe the opportunity for drugs targeting the GLP-1 mechanism of action is very large, and even though Eli Lilly and Novo Nordisk are likely to be the key players in the space in the near term, we believe the market can support several competitors.”

Read more of Conover’s take on Pfizer.

Amgen

- Fair Value Estimate: $268.00

- Morningstar Rating: 3 stars

- Morningstar Economic Moat Rating: Wide

- Morningstar Uncertainty Rating: High

“Amgen is being driven by a combination of steady growth from established osteoporosis drug Prolia and rapid growth from newer products like osteoporosis drug Evenity, asthma drug Tezspire, and leukemia drug Blincyto. While pricing remains a headwind for cholesterol-lowering drug Repatha, sales still rose 31% in the quarter as demand continued to grow at a rapid pace.

“In the pipeline, we think Amgen’s phase 3 cardiology drug olpasiran could prove complementary to Repatha and leverage Amgen’s investments in its primary care sales force. In obesity, we’re still awaiting phase 2 data from AMG 133 in late 2024, and we include sales approaching $3 billion annually by the end of our 10-year forecast. We see this program as a wild card, as its unique mechanism of action could lead to safety issues, but phase 1 efficacy and durability data was very promising.”

Read more of Andersen’s take on Amgen.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/RNODFET5RVBMBKRZTQFUBVXUEU.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LJHOT24AYJCHBNGUQ67KUYGHEE.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/V33GR4AWKNF5XACS3HZ356QWCM.jpg)