5 Underperforming and Undervalued Stocks in Q3

Some of these stragglers just turned cheap.

Consumer cyclical and communication-services stocks struggled in the third quarter of 2021 and dominated the list of underperforming names among those covered by Morningstar's equity analysts.

But the flip side for investors is that many of these names are now trading at attractive prices, including Alibaba BABA.

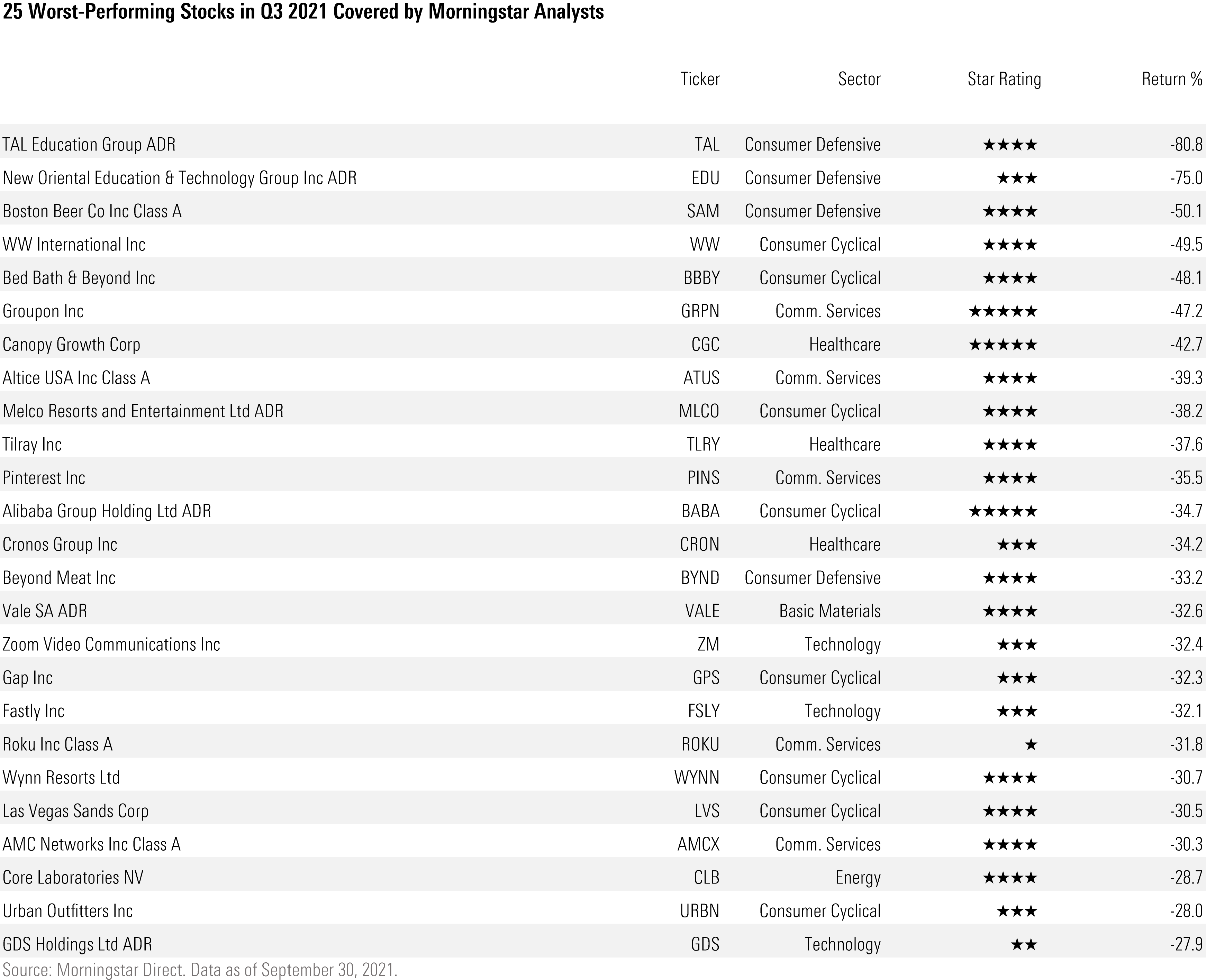

Each quarter we look at the 25 stocks that fared the worst among those that are listed on a U.S. exchange and covered by Morningstar. The third-quarter list contained 839 names. From there, we look at how their shares measure up against our analysts' fair value estimates and also highlight trends that may have held back the performance of particular sectors and industries.

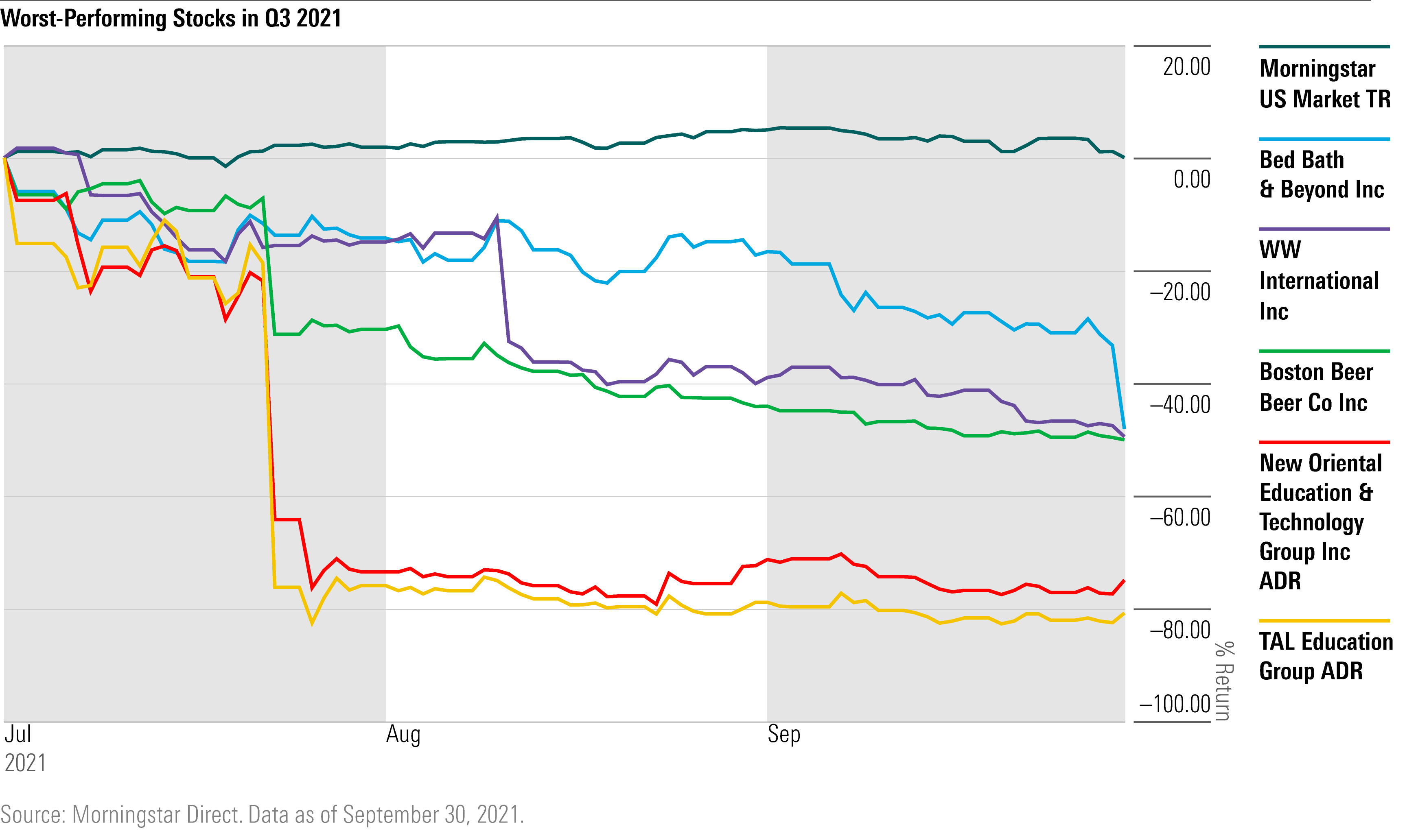

Below are the five worst performers from the third quarter. The full list of the 25 can be found at the end of this article.

A recurring theme across the third-quarter list is the impact of China's regulation. In particular, stocks in the Chinese private education services industry were pummeled for the second consecutive quarter. TAL Education Group TAL and New Oriental Education & Technology Group EDU retained their spots as the most underperforming stocks on Morningstar’s coverage list. TAL Education collapsed 80.8% during the quarter and finished September down 93.8% for the year. New Oriental Education was close behind, sliding 75.0% in the third quarter and 88.5% for the year to date.

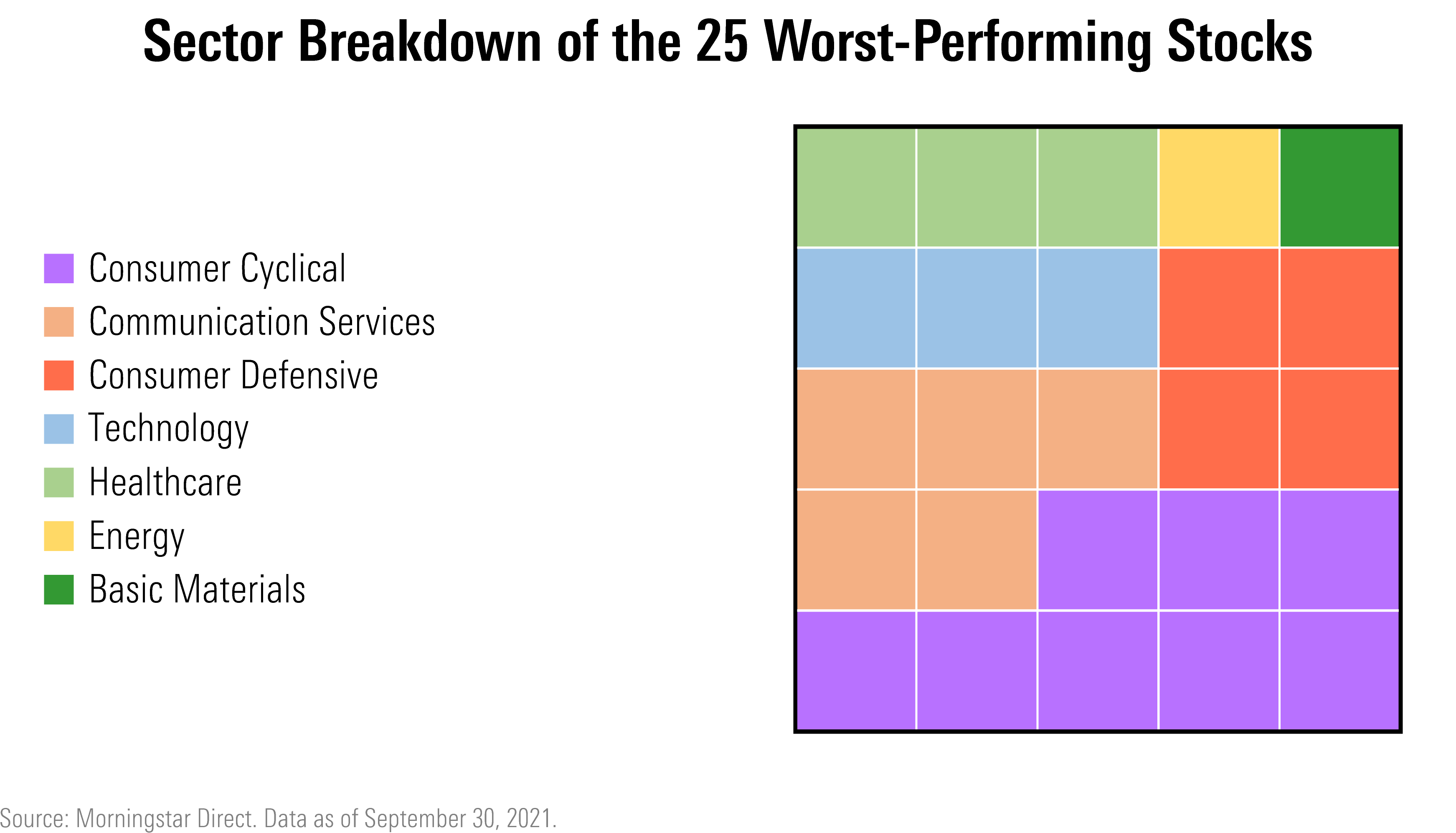

From a sector standpoint, the bulk of the underperformers on the coverage list were consumer cyclicals.

The worst performers were retailers. Bed Bath and Beyond BBBY was down 48.1%, Gap GPS fell 32.3%, and Urban Outfitters URBN slid 28.0%. While U.S. retail sales and consumer demand has surpassed prepandemic levels in recent months, retailers have faced immense pressure as supply chain constraints created inventory bottlenecks and cost pressures threatened profitability.

"Whether retailers can push prices higher to compensate should be a meaningful story over the quarters ahead," says Morningstar equity analyst Zain Akbari.

Other stocks in the consumer cyclical space taking a hit were casino operators. Melco Resorts and Entertainment MLCO, Wynn Resorts WYNN, and Las Vegas Sands LVS all dropped more than 30% in the third quarter. All three casino companies have significant stakes in the Macao gambling industry where Chinese regulators are looking to heighten governmental supervision on gaming companies' operations.

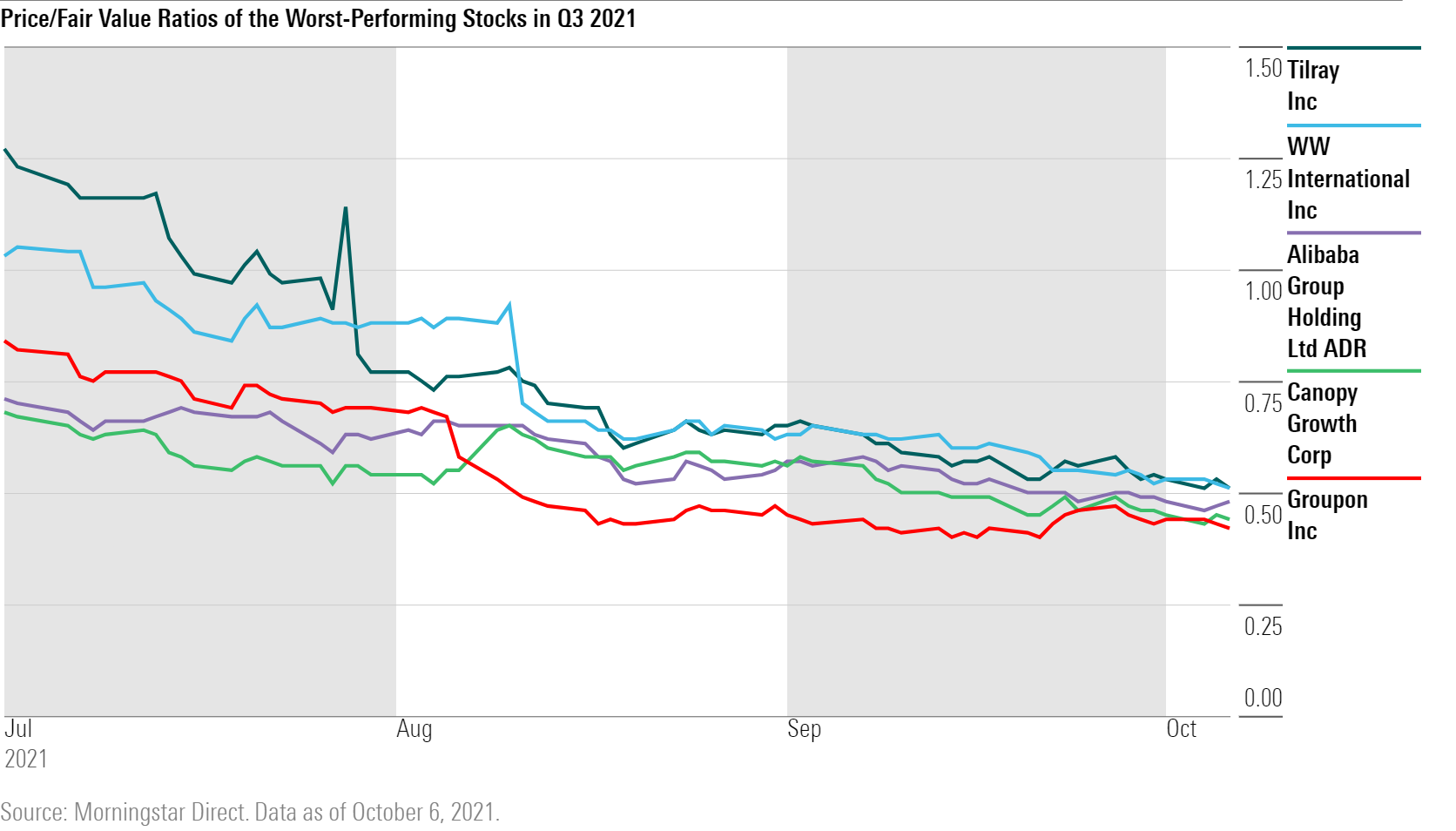

However, third-quarter declines opened more entry points for stock investors looking for pockets of value. Of the 25 underperformers, only two stocks remained overvalued as of the end of the quarter. Roku ROKU was the most overvalued, trading at an 89% premium, followed by GDS Holdings GDS at a 24% premium.

Seventeen stocks were undervalued with a 5- or 4-star Morningstar Rating. Below are the five cheapest stocks among the underperformers.

Groupon GRPN was the most undervalued stock on our underperformers list, trading at a 58% discount to its fair value. Canopy Growth CGC was 56% below fair value, while Alibaba sat at a 52% discount. Both Tilray TLRY and WW International WW were trading 49% below their fair values at the time of writing.

Here's what our analysts had to say about these stocks:

Groupon

"As a first-mover in the local-market daily deals space, Groupon has captured a leadership position, but robust profitability has not followed. Groupon's revenue growth has been decelerating and gross margins have been declining since the company went public in 2011. Additionally, the firm is implementing a more aggressive customer acquisition strategy that requires higher marketing expenses. Although a restructuring plan is in place for a turnaround, we remain concerned about future revenue growth and gross margin compression, both of which may prevent Groupon from yielding excess returns on capital in the long run."

--Ali Mogharabi, senior equity analyst

Canopy Growth

"Canopy Growth grows and sells cannabis products primarily in Canada, which accounts for roughly 50% of sales. Non-THC product sales account for about 30%.

"Canopy also exports medical cannabis globally. The global market looks lucrative, given higher prices and growing acceptance of cannabis' medical benefits. Exporters must pass strict regulations to enter markets, protecting early entrants like Canopy. Partially offsetting the global markets' potential for Canadian producers are threats of future production from countries with cheaper labor--the single largest cost. However, many Canadian companies have pulled back expansion plans given ongoing cash burn. We forecast around 15% average annual growth through 2030."

--Kristoffer Inton, equity strategist

Alibaba

"Alibaba is a big data-centric conglomerate, with transaction data from its marketplaces, financial services, and logistics businesses allowing it to move into cloud computing, media/entertainment, and online-to-offline services. We think a strong network effect allows leading e-commerce players to extend into other growth avenues, and nowhere is that more evident than Alibaba.

"Alibaba's marketplace monetization rates have generally been on an upward trend despite recent macro uncertainty, indicating that sellers are increasingly engaging with Alibaba's marketplaces and payment solutions, although increased compliance of antitrust laws and more competition will put pressure on monetization in the near to medium term."

--Chelsey Tam, senior equity analyst

WW International

"We've been encouraged by WW's efforts to position itself as a lifestyle brand focused on a more holistic approach to health/wellness to differentiate itself from calorie-counting mobile apps, activity monitors, and other weight management solutions. In particular, we believe it is taking steps to incorporate personalized and on-demand offerings across its in-person, online, and mobile platforms. Its 'myWW' platform offers greater member flexibility while still offering features like SmartPoints (which puts an emphasis on eating leaner proteins, fruits, and vegetables), ZeroPoint foods (foods don't have to be weighed, measured, or tracked), and Connect (a social media tool giving users access to community members). We also believe Direct 360 (a premium coaching offering with live and on-demand content) will help attract a younger audience to the WW ecosystem and drive higher lifetime customer values."

-Jaime Katz, senior equity analyst

Tilray

"Tilray cultivates and sells cannabis in Canada and exports into the global medical market. It also sells CBD products in the United States. The company is the result of legacy Aphria acquiring legacy Tilray in a reverse merger and renaming itself Tilray in 2021.

"In 2020, legacy Aphria acquired SweetWater, a U.S. craft brewery. Legacy Tilray previously acquired Manitoba Harvest to distribute CBD products in the U.S. It finally secured a toehold into U.S. THC when it acquired some of MedMen's outstanding convertible notes. Upon U.S. federal legalization, Tilray would own 21% of the U.S. multistate operator. Furthermore, Tilray paid a great price while also getting downside protection as a debtholder.

"We think the U.S. offers the fastest growth of any market globally. However, the regulatory environment is murky with individual states legalizing cannabis while it remains illegal federally. We expect federal law will eventually be changed to allow states to choose the legality of cannabis within their borders."

--Kristoffer Inton, equity strategist

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/RNODFET5RVBMBKRZTQFUBVXUEU.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LJHOT24AYJCHBNGUQ67KUYGHEE.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/V33GR4AWKNF5XACS3HZ356QWCM.jpg)