The 60/40 Portfolio Isn’t Dead, and Neither Is Bitcoin. But Mixing Them Can Be Lethal.

A little cryptocurrency can change your portfolio a whole lot.

/s3.amazonaws.com/arc-authors/morningstar/eda620e2-f7a7-4aef-bb6c-3fb7f1ac7a38.jpg)

Bitcoin has performed surprisingly well for the year to date. The CMBI Bitcoin Index posted a 76.4% return through July 2023 in defiance of the gloomy narratives that haunt the rest of the cryptocurrency ecosystem.

The trusty balanced portfolio has also beaten expectations as of late. Vanguard Balanced Index VBAIX has turned in a respectable 12.8% for the year to date after a lousy 2022 that augured the age-old question of whether the 60/40 fund (referring to its split between stocks and bonds) might be dead. Balanced funds’ performance owes a great deal to the excellent performance of U.S. stocks, which have returned a hearty 20.6%, as measured by the Morningstar US Market Index.

So far in 2023, risk has paid handsomely. That fact may leave many investors wondering whether to add some extra firepower to their portfolio in the form of an allocation to bitcoin.

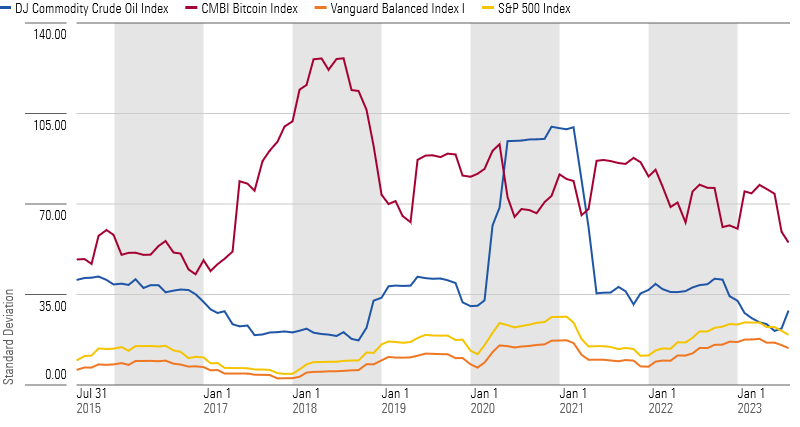

Compared with other assets, though, bitcoin’s volatility is more kerosene than kindling. Over the 10-year period ended July 2023, bitcoin was 16.8 times as volatile as Vanguard Balanced Index. (The only asset that comes anywhere close is oil, although the price history of the Dow Jones Crude Oil Index only goes back to 2015.)

Rolling One-Year Volatility of Bitcoin Exceeds Other Assets

Even though bitcoin has performed favorably since the last time we examined bitcoin’s impact on the 60/40 in 2021, its returns are still nearly 4 times as volatile as those of a balanced fund. That means that even a smidge of bitcoin changes the behavior of an investor’s portfolio a whole lot.

How Much Is a Lot?

Let’s say that in August 2013 a hypothetical investor added a 2% allocation to bitcoin to a costless 60/40 portfolio—that’s $20 in bitcoin for every $1,000 invested. (For the purposes of this example, let’s also assume the investor furnished that $20 investment from their bond portfolio, although it doesn’t change the results much whether that money comes from stocks or bonds. We also rebalanced this portfolio on a monthly basis—that will become important in a second.)

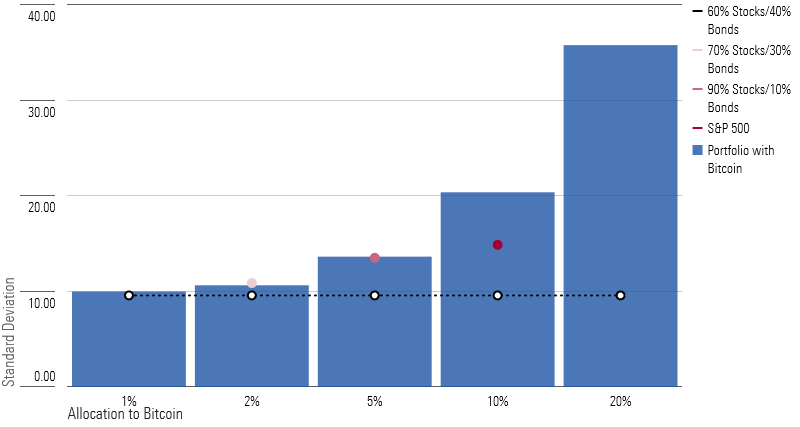

Our study found that a 2% sliver of bitcoin reshaped the return profile of their portfolio nearly as much as adding a 10% stake in stocks would have: A 60%/38%/2% split between stocks/bonds/bitcoin yielded a standard deviation of 10.7 over the past 10 years, in line with how a 70%/30% S&P 500/Bloomberg U.S. Aggregate Bond portfolio would have behaved.

Bitcoin Alters Standard Deviations Far More Than Additional Stock Exposure

Further up the risk spectrum, a portfolio with a 5% stake in bitcoin had a risk profile closer to a 90/10 portfolio than a 60/40. In fact, if that hypothetical portfolio was a fund, adding bitcoin would have easily pushed it out of the moderate allocation Morningstar Category to which most balanced funds belong. The closest match among allocation categories is the aggressive allocation category, meaning that the portfolio leapfrogged the moderately aggressive allocation category altogether. (Meanwhile, any portfolio with a 10% allocation or more to bitcoin courted more risk than the S&P 500 on its own!)

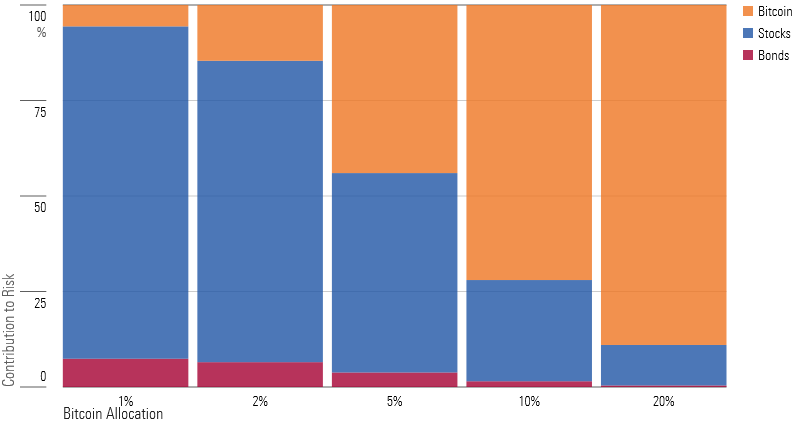

Decomposing that risk reveals even more. Effectively, a 1% allocation to bitcoin has a negligible effect on risk, either in terms of absolute volatility or relative contribution. But a 2% allocation to bitcoin explains close to 15% of a portfolio’s overall volatility, a much heftier contribution. Meanwhile, a 5% allocation accounts for nearly 45% of the return volatility the portfolio experienced, and overall volatility was meaningfully higher.

Bitcoin's Relative Contribution to Risk Increases With Additional Exposure

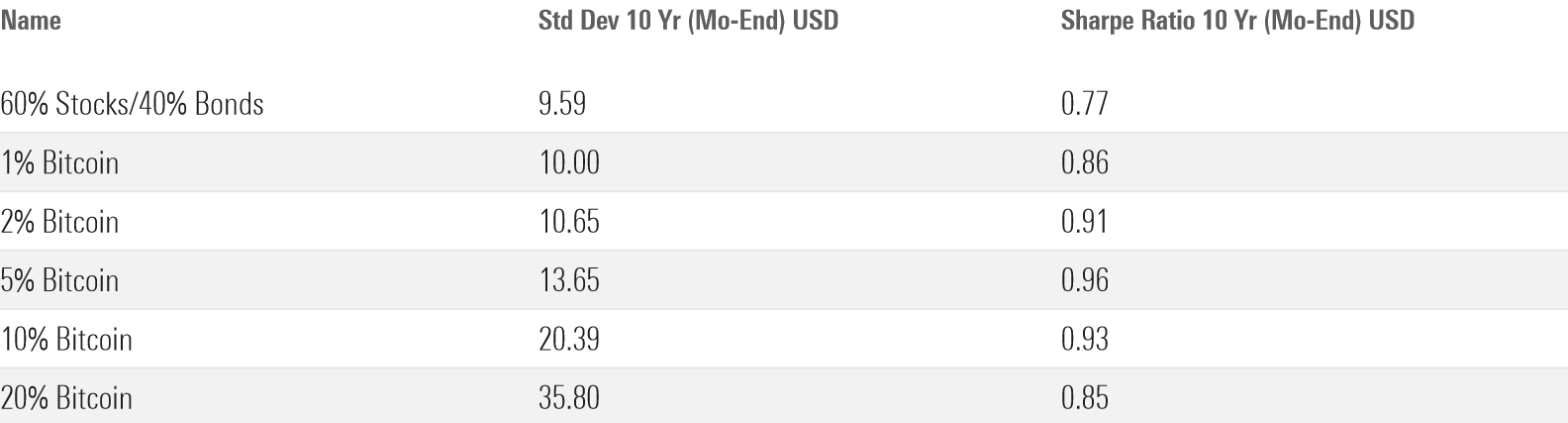

Although adding bitcoin does open up the risk throttle on these hypothetical portfolios, it’s worth pointing out that investors would have been fairly compensated for doing so. A costless 60/40 portfolio would have turned in a Sharpe ratio (a return metric that accounts for risk) of roughly 0.77 over the past decade. Each portfolio that contains bitcoin improves upon that result, although incremental improvements peak at a 5% slice.

Bitcoin Has Compensated Investors for Additional Risk

With that being said, our portfolios were crafted using a fairly narrow set of assumptions that aren’t likely to hold in practice. That’s because regulators in the United States have barred most brokerages from offering bitcoin alongside traditional stock and bond investments. Most digital assets are quarantined in a separate wallet or exchange account, which makes it tedious for investors to rebalance on a monthly cadence like we did in our study. Whether because of inertia or mental accounting or both, many investors opt not to rebalance at all.

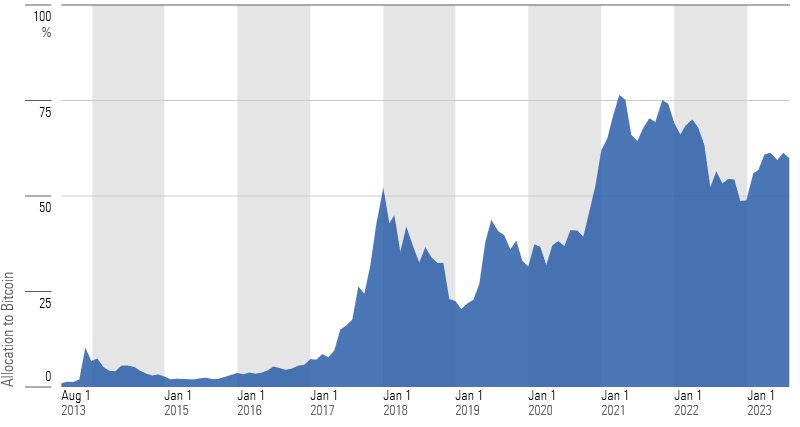

When it comes to security selection—picking individual stocks, for example—the “Do Nothing” approach may have some merit. But when it comes to asset allocation, there are consequences to portfolio neglect. For example, a 1% allocation to bitcoin (funded proportionally from stocks and bonds this time, to replicate the experience of segregating assets) can quickly spiral into a 60% allocation if investors fail to reap what they’ve sown.

Failing to Rebalance Has Significant Consequences for an Investor's Asset Allocation

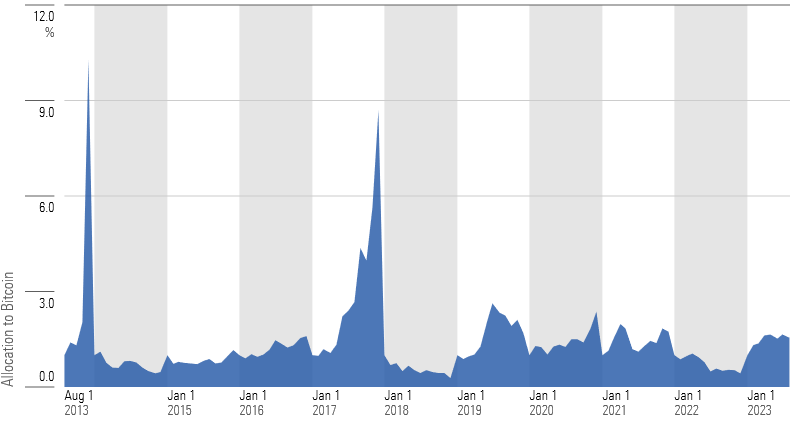

Even one annual rebalance makes a world of difference. There are some edge cases, like 2013 and 2017, where the allocation to bitcoin would have climbed above 5%. But mostly it plods along somewhere between 1% and 2%. For only 15 months out of the entire 10-year holding period does the portfolio overtake that 2% threshold where the portfolio experiences volatility that’s out of spec with the risk profile of a 60/40 portfolio.

Annual Rebalances Partially Succeed in Keeping Allocation to Bitcoin in Check

While the SEC weighs proposals that might broaden investor access to bitcoin by way of an exchange-traded fund, we see a marginal benefit to existing owners of digital assets who would have an easier time trying to rebalance this high-octane holding if it’s permitted to live alongside their traditional investments. But without the investor protections that other asset classes provide, we continue to advise that investors treat purchases of digital assets (including bitcoin) as a sunk cost rather than an investable asset.

Even so, there are investors who fall somewhere in between these two extremes and treat bitcoin as something more than a sunk cost but less than a full-blown portfolio holding. I would advise those investors to tread cautiously. Like caviar or dynamite, a little bit of bitcoin goes a long way.

A note on the disclaimer below: Most digital assets, including the cryptocurrencies mentioned in this article, are not currently classified as shares of registered securities by the SEC and therefore do not fall under Morningstar’s editorial policies. However, in the interest of full disclosure, the author of this article does own digital assets mentioned in this article.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/EC7LK4HAG4BRKAYRRDWZ2NF3TY.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/6ZMXY4RCRNEADPDWYQVTTWALWM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/URSWZ2VN4JCXXALUUYEFYMOBIE.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/eda620e2-f7a7-4aef-bb6c-3fb7f1ac7a38.jpg)