How a Little Bitcoin Can Change Your 60/40 Portfolio a Lot

After bitcoin’s recent slide, it may be tempting to buy the dip. Here’s what to consider when thinking about adding it to a balanced portfolio.

/s3.amazonaws.com/arc-authors/morningstar/a3ffb7d7-3689-49a2-bfde-9235ef1e06ad.jpg)

This article was updated to correct the omission of a drawdown period in Exhibit 4.

The price of bitcoin has stumbled after skyrocketing over the past year. From mid-April through June 25, 2021, the popular cryptocurrency lost nearly half its value. The CMBI Bitcoin Index, which tracks its spot price, posted a 49.1% loss over the period (though it’s still up more than 11% for the year to date and 240% over the past year as of June 28).

If you’re considering buying the dip, keep in mind that even a small amount can alter the risk profile of a typical balanced portfolio. Like plutonium for your portfolio: A little bit has a big impact.

In this article, we examine the token’s historical volatility and correlations to stocks and bonds, to help investors who are considering adding bitcoin to their portfolio determine how much might make sense, and where they may want to fund it from (stocks, bonds, or both). Of course, this is not a recommendation to buy bitcoin. It is a backward-looking exercise of a wildly volatile asset without a very long history. This study also ignores any related costs and difficulties that come with buying bitcoin, which can be significant. As such, handle this initial inquiry into bitcoin from a multi-asset lens with care.

Volatility Goes Both Ways

Bitcoin’s volatility may have been easy to overlook when it booked a 300% gain in 2020 and a 1,300% return in 2017. As the recent price crash has shown, however, outsize returns rarely come without stomach-dropping reversals along the way.

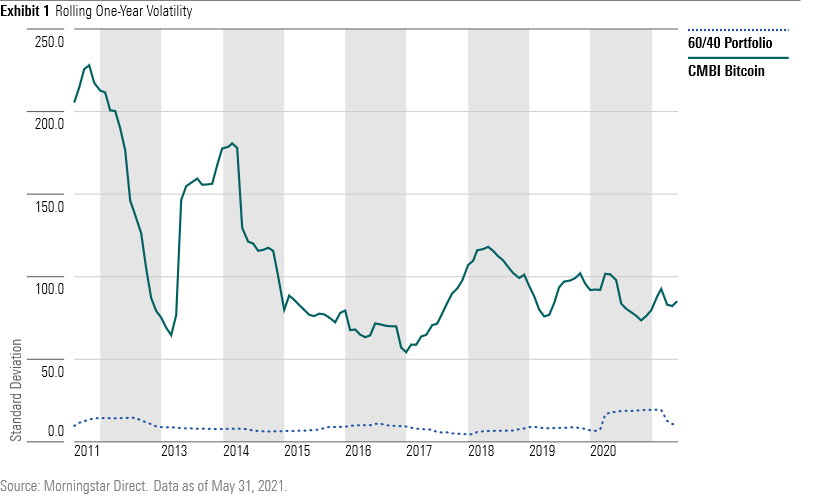

Exhibit 1 depicts the rolling one-year standard deviation--a measure of volatility--using daily returns over the life of the CMBI Bitcoin Index (launched mid-July 2010), comparing both the index and a basic 60/40 stock/bond portfolio composed of the Morningstar Global Markets Index and Morningstar US Core Bond Indexes (two broadly diversified indexes representing the global stock and U.S. bond markets), rebalanced monthly.

Bitcoin has taken investors on a wild ride. Compared with the 60/40 portfolio, bitcoin has on average been 13 times more volatile over the period. Like many risky assets, volatility comes and goes over shorter periods, but even at the lower ends of its historical range you still need unshakable nerves to invest. Over the trailing one-year period, bitcoin was 8.6 times more volatile than the 60/40 portfolio.

A Little Bitcoin Can Go a Long Way

An allocation to any given security or asset class can have a bigger impact on a broad portfolio’s risk profile than it first appears. For example, at a glance, a standard 60/40 portfolio may appear to source 60% of its risk from equities and 40% from bonds. However, since equities are much more volatile than bonds, more like 90% of the portfolio’s risk comes from equities. With that in mind, the impact on the risk profile of the same portfolio by introducing bitcoin, which is incredibly more volatile, is jarring.

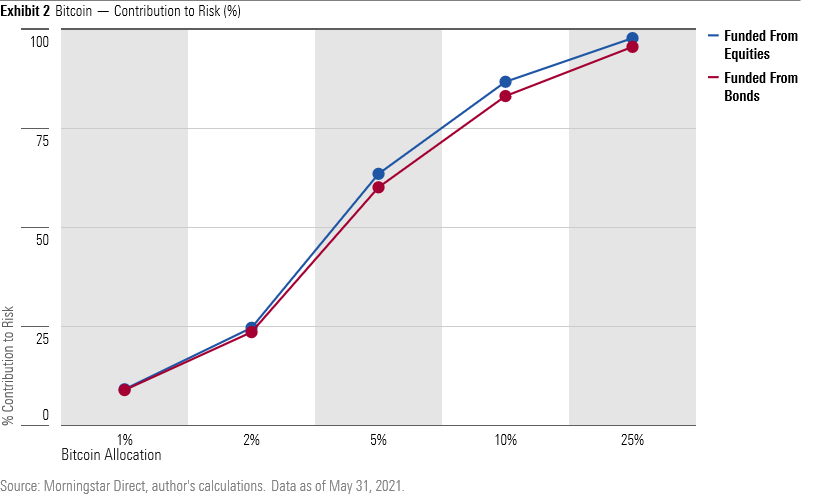

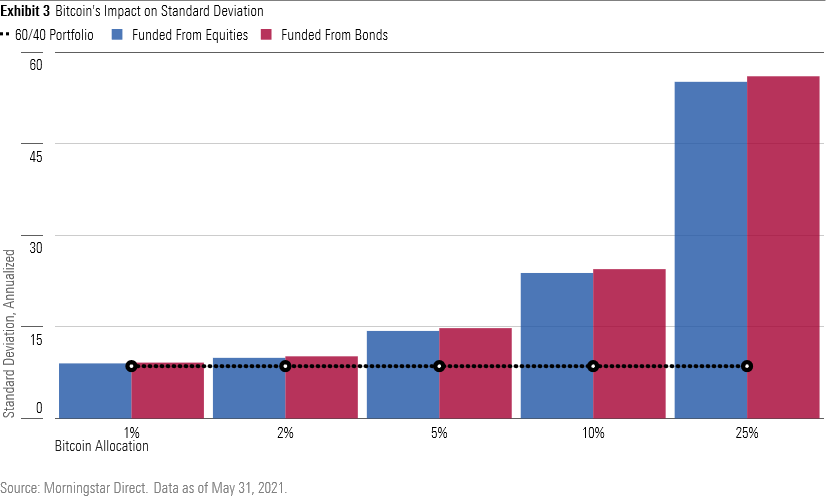

Exhibit 2 depicts bitcoin’s risk contribution to the 60/40 portfolio when holding bitcoin, as approximated by the CMBI Bitcoin Index, at various weights (1%, 2%, 5%, 10%, and 25%) and when sourcing the allocation from both the stock and bond sleeves. Exhibit 3 shows how each hypothetical portfolio’s standard deviation changed over the period given the varying allocations to bitcoin.

With a 1% or 2% exposure to bitcoin, the impacts on the risk profile and volatility of the portfolio are notable; it contributes roughly 9% and 24% of total risk, respectively, but result in a de minimis change in overall volatility, as shown in Exhibit 3.

However, greater exposures significantly shift the portfolio’s total risk toward bitcoin and drive the overall volatility drastically higher. At 5%, the bitcoin allocation contributes more than 60% of the portfolio’s total risk and increases volatility by roughly 70%.

With a 25% allocation, the contribution to risk jumps dramatically to 96% when taken from the bond sleeve and 98% when sourced from equities. The overall volatility is more than six times greater compared with the 60/40 portfolio. Investors allocating even seemingly small amounts to bitcoin should keep this in mind as a risk-control measure.

Diamond Hands Required

Being aware of bitcoin’s risk and its effect on your portfolio is paramount when allocating to the cryptocurrency. Its sharp, roughly 50% decline from mid-April 2021 through June 25 isn’t a new phenomenon for the cryptocurrency. Investors that held or bought more during past declines, as hair-raising as those could be, have reaped the benefits.

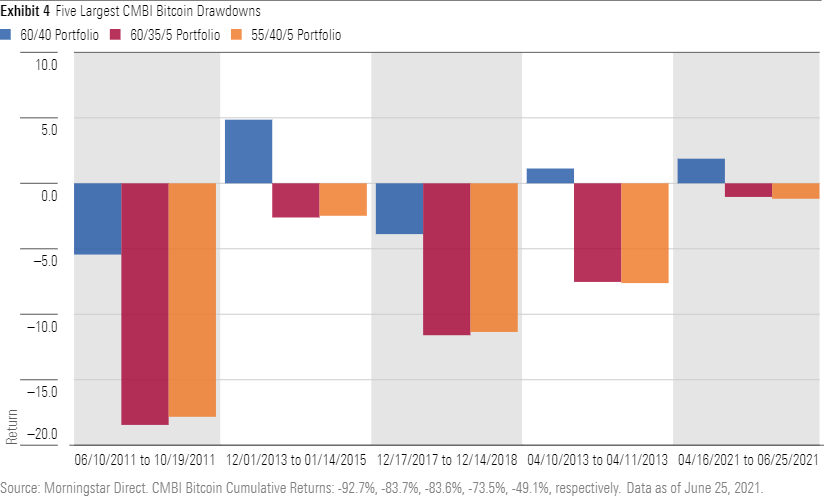

A balanced portfolio with a 5% bitcoin allocation over the past decade through May 2021 delivered a 15.4% annualized return when sourced from fixed income and 15.1% return when sourced from equities, assuming monthly rebalances. Each outpaced the 7.3% return for the 60/40 portfolio. However, standing pat during bitcoin's sell-offs is much easier said than done. Exhibit 4 shows the returns of each portfolio during the CMBI Bitcoin Index's five largest drawdowns over its nearly 11-year track record, ranging from negative 49% to negative 93% peak-to-valley.

Over these five stress periods, the straightforward 60/40 portfolio held up better than the portfolios with bitcoin allocations by about 7.9% on average. During bitcoin's recent nosedive, which began in mid-April through June 25, 2021, the standard 60/40 portfolio posted a 1.9% gain, while the bitcoin portfolios trailed that mark by 3 percentage points. It can be difficult to stick with portfolios that are struggling when stocks and bonds are doing well.

Where to Fund Your Crypto?

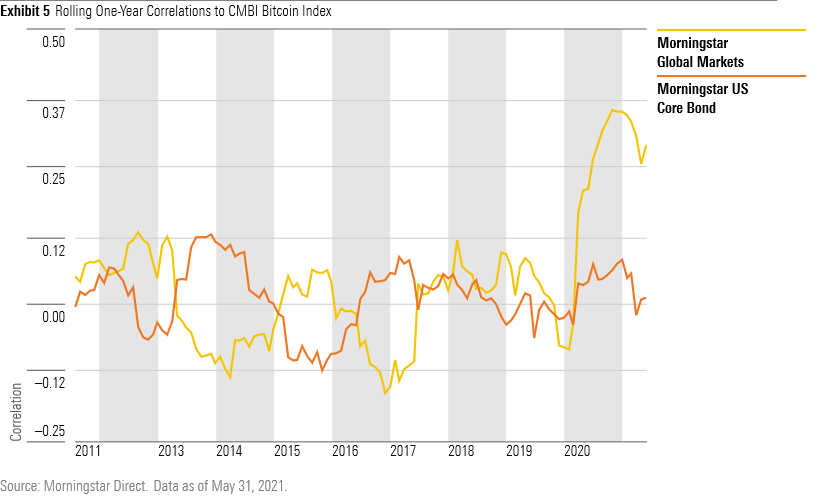

The decision to allocate to bitcoin from your equity or bond exposure hasn’t been that important in the past. Why? Bitcoin’s correlation with broader equity and fixed-income markets was essentially zero. But very recent data suggests that might be changing. Exhibit 5 shows rolling one-year correlations of the indexes to bitcoin using daily returns, which hovered around 0.0 for a majority of the past 10 years.

With seemingly no correlation to stocks or bonds, bitcoin provided a diversifying return stream to investors' portfolios irrespective of which asset class they funded it from. More recently, however, bitcoin’s one-year rolling correlation to broader equity markets has risen, hovering between 0.25 and 0.35. Yes, that’s still low and it may fall back to near zero again, but it’s still notable. If we see a sustained shift in bitcoin’s correlation to stocks or bonds, the importance of where the allocation is sourced increases. That decision has been trivial for most of bitcoin’s history, but it may become a more important consideration going forward.

Overall, bitcoin’s returns have been explosive but have also come with an exceptional amount of volatility. Its recent decline pressures the buy and hold investor, while potentially enticing those closely monitoring from the sideline.

No matter the situation, investors considering bitcoin should be aware of the investment’s substantial volatility and should make an informed decision regarding which part of their portfolio they fund it from. Because, although past performance may look particularly strong, it is no indication of future results.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

/d10o6nnig0wrdw.cloudfront.net/07-25-2024/t_56eea4e8bb7d4b4fab9986001d5da1b6_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/BU6RVFENPMQF4EOJ6ONIPW5W5Q.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/a3ffb7d7-3689-49a2-bfde-9235ef1e06ad.jpg)