What Will the Upcoming GDP Report Show About the U.S. Economy?

GDP growth in the first quarter is likely to look solid, but we expect a drop-off after that.

/s3.amazonaws.com/arc-authors/morningstar/010b102c-b598-40b8-9642-c4f9552b403a.jpg)

While all signs point toward a solid performance for the U.S. economy in the first quarter, we expect gross domestic product growth to slow for the rest of 2023. Economic activity is likely to be stuck in the doldrums until 2024, when we expect the Federal Reserve to deploy aggressive interest-rate cuts.

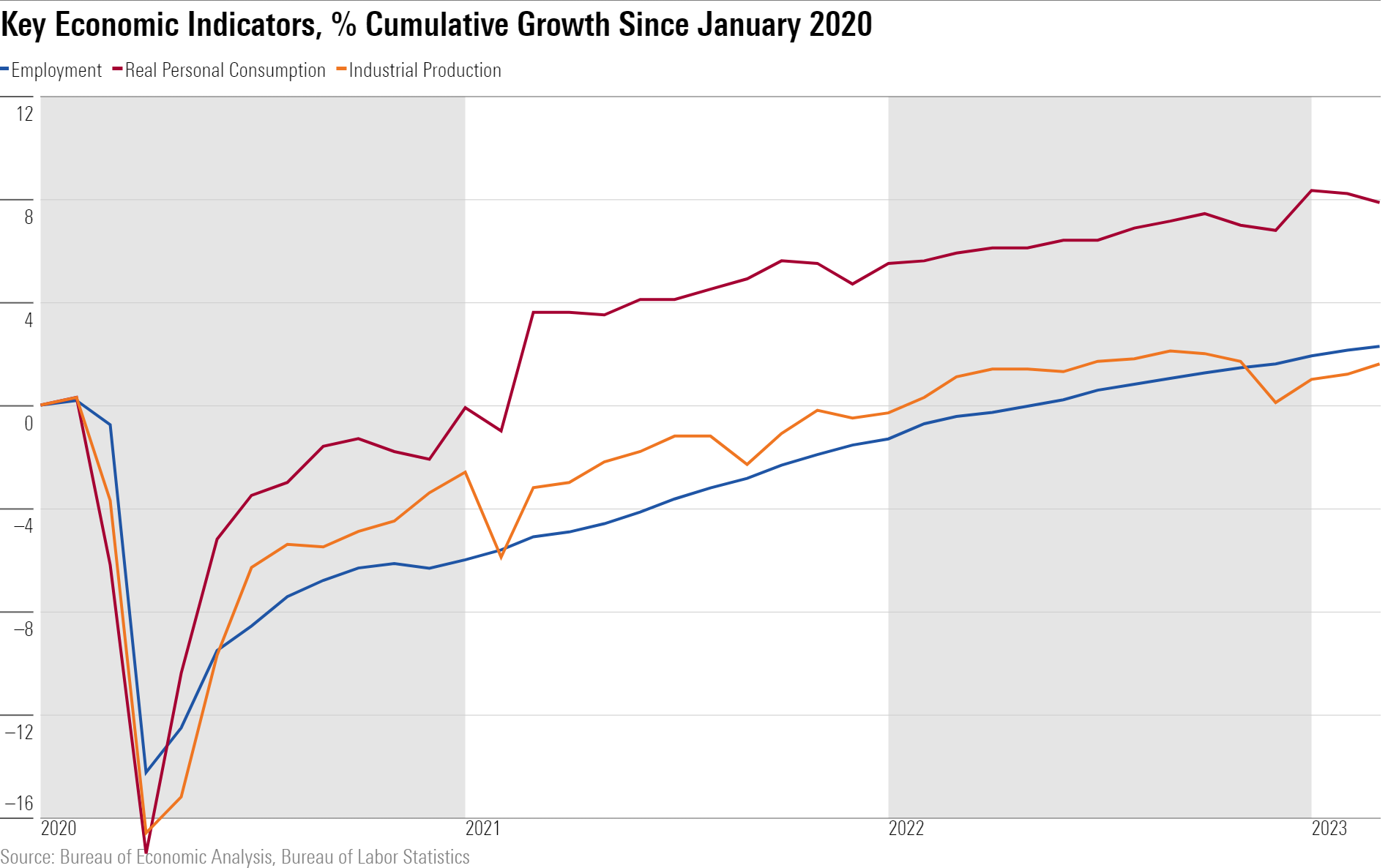

First-quarter GDP figures are soon going to be released by the U.S. Bureau of Economic Analysis. But we already have a good read on what the GDP data is likely to show. Most indicators of economic activity showed a continued uptrend in the first quarter. Employment growth continues to be the most bullish indicator of economic activity. Real consumption also showed a rebound after a weak holiday season in the fourth quarter of 2022. Industrial production remains the main weak spot in the data, which presages a slowdown in investment expenditure.

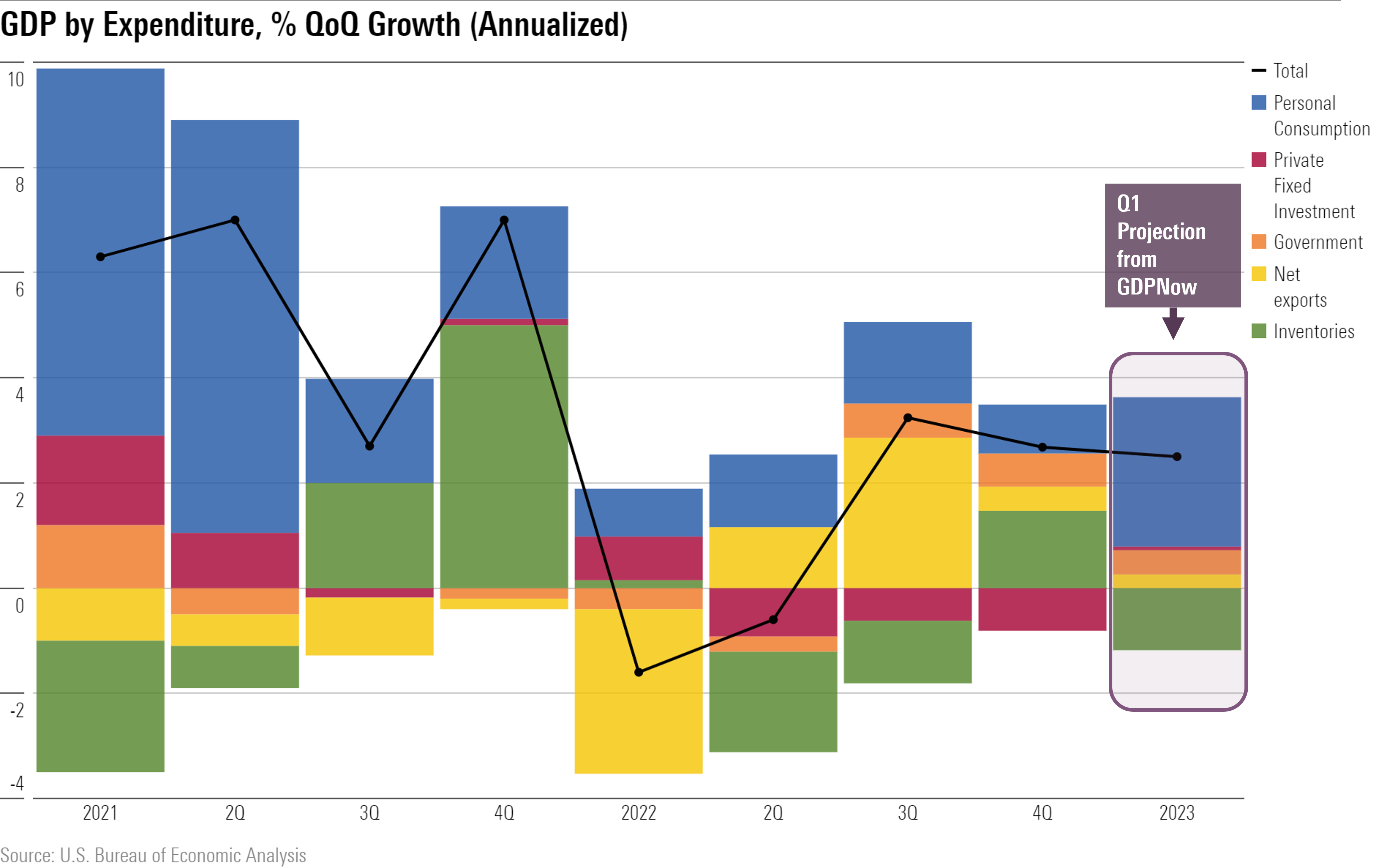

Likewise, the latest projections from the Federal Reserve Bank of Atlanta’s GDPNow show that first-quarter real GDP is likely to rise by 2.5% annualized. This is expected to be driven mainly by consumption, posting its strongest contribution since 2021.

After the first quarter, however we expect real GDP growth to slow greatly, averaging around 0% in sequential terms for the rest of the year. This is consistent with a 30% to 40% probability of a formal recession being declared. Regardless of whether a recession happens or not, we expect GDP growth to bounce back in 2024 and the following years as monetary policy easing boosts housing and other struggling parts of the economy.

In the meantime, we expect a major driver of weaker growth for the rest of 2023 will be more cautious consumer behavior. Households saved just 3.8% of their personal income in 2022, compared with a prepandemic rate of 8.8%. Outsize spending was propped up by the excess savings accumulated earlier in the pandemic, but those stockpiles are running low.

Additionally, the job market is likely to slow in 2023 off of quite robust recent growth rates. Employers seem to still be stuck in the mentality dominant a year ago of struggling against rampant labor shortages, but that will change or else businesses risk cutting into profit margins.

Despite all of the recent concern around banking failures, banking sector distress looks contained. Deposit outflows from banks have been muted in recent weeks after massive outflows in early March. This leaves the Fed to focus primarily on fighting inflation in its setting of monetary policy. We expect inflation to return most of the way back to normal by the end of 2023, clearing the way for the Fed to begin cutting the federal-funds rate.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/PKH6NPHLCRBR5DT2RWCY2VOCEQ.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/GJMQNPFPOFHUHHT3UABTAMBTZM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZYJVMA34ANHZZDT5KOPPUVFLPE.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/010b102c-b598-40b8-9642-c4f9552b403a.jpg)