Where We See Opportunities After an Ugly Month for Stocks

Our US stock market outlook and valuation for May 2024.

/s3.amazonaws.com/arc-authors/morningstar/54f9f69f-0232-435e-9557-5edc4b17c660.jpg)

Key takeaways:

- Stocks drop enough in April to return to fair value from stretched.

- Value and small-cap stocks remain most attractively priced for long-term investors.

- Real estate, communications, and basic materials are the most undervalued sectors.

- Weak economy + sticky inflation = worst of both worlds.

Stocks Retreat in April, Falling to Fair Value

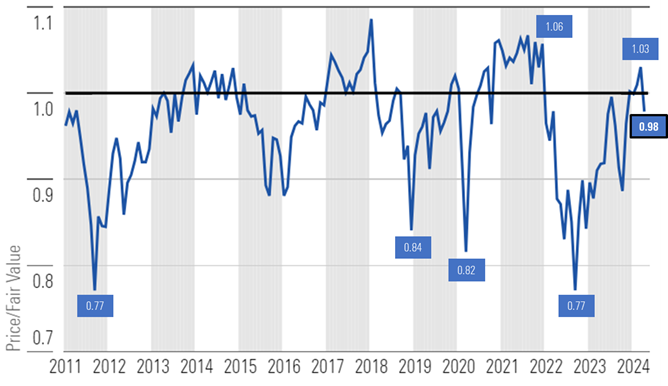

In our 2Q 2024 Quarterly US Market Outlook, we noted that at the end of March 2024, our price/fair value metric for the US market was 1.03. At a 3% premium, the market had not officially entered overvalued territory, yet we noted that it was definitely feeling stretched. In fact, since 2010, the market has only ever traded at that much of a premium or more only 14% of the time.

Over the course of April, the Morningstar US Market Index, our broadest measure of the US stock market, fell 4.30%. As of April 30, the US stock market was trading at a 2% discount to a composite of our fair values.

Price/Fair Value of Morningstar's US Equity Research Coverage at Month-End

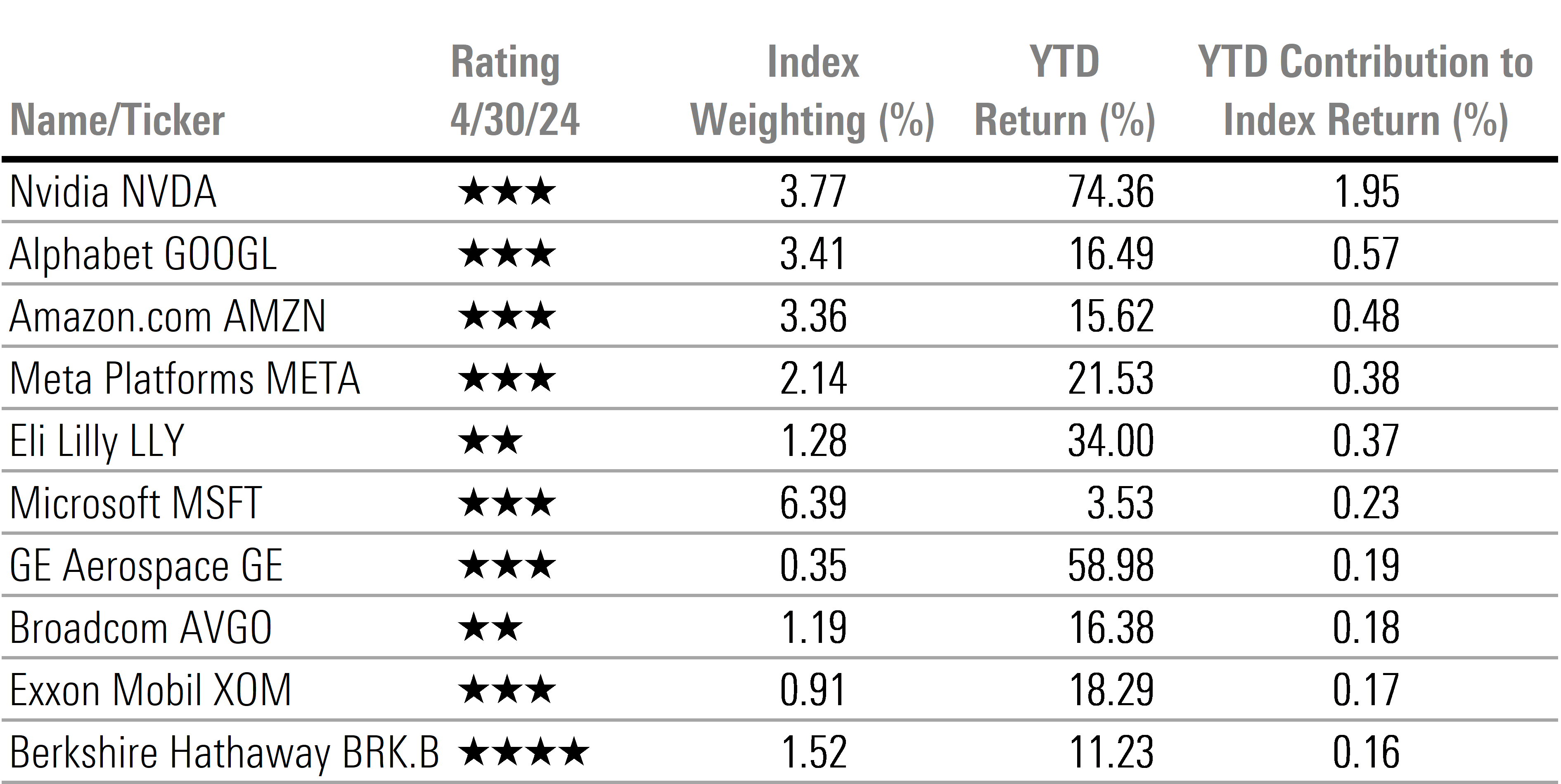

Market returns remain heavily concentrated, with just 10 stocks accounting for 85% of the market’s gain for the year to date. We continue to expect that future returns will widen out across the market as those 10 stocks are either fairly valued, or overvalued, with only Berkshire Hathaway BRK.B remaining undervalued and rated 4 stars.

Morningstar US Market Index Attribution Analysis

According to our valuations, we think it is unlikely that what has worked in the markets for the past year and a half will be what continues to work. Those stocks that have driven the preponderance of the gains since the market bottom in October 2022 are now trading in fair value territory. We continue to think it is a good time for investors to look for contrarian investment opportunities, especially in those areas that have underperformed, are unloved, and are—most importantly—undervalued.

Growth Stocks Suffer Greatest Selloff in April

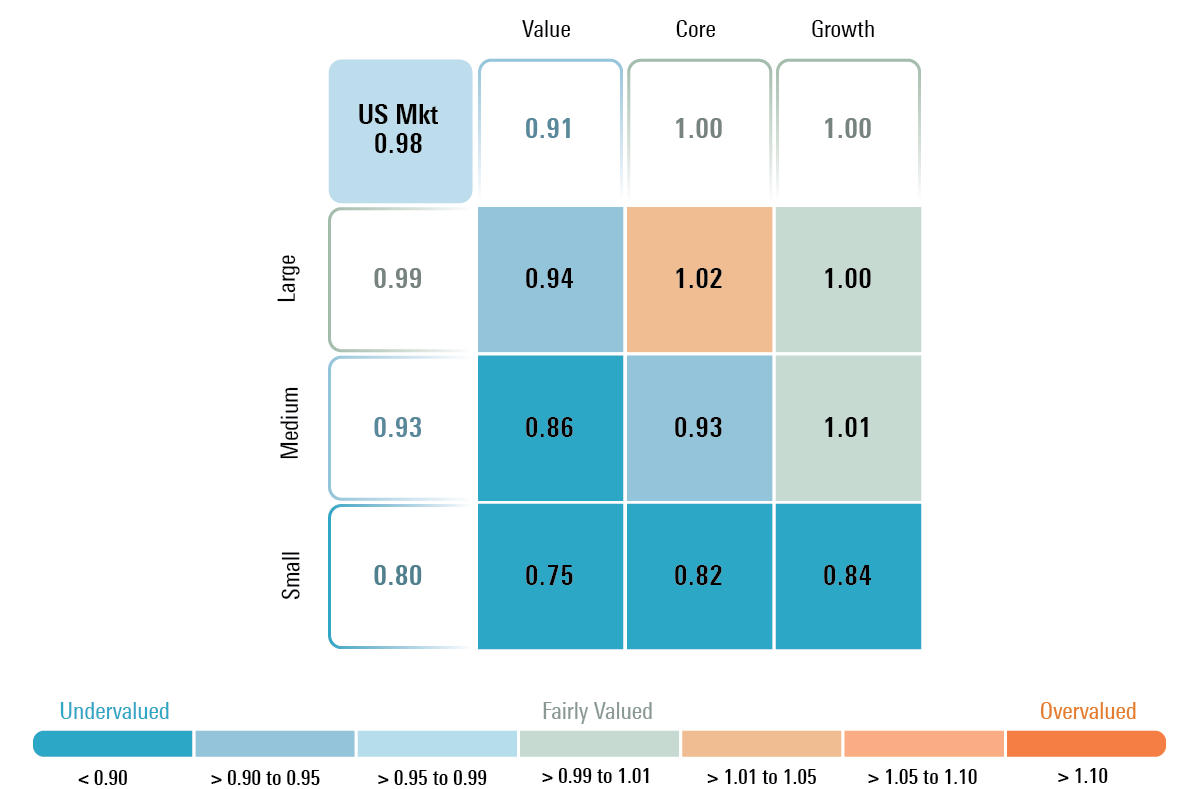

By style, the growth category fell the most in April, retreating 5.92%, whereas the core category held up the best, only falling 3.50%, and value split the difference, falling 4.39%. By capitalization, investors took refuge in large-cap stocks, which only fell 3.87%, while mid-cap stocks dropped 5.07% and small-cap stocks declined 6.56%.

According to our valuations, the value category remains the most attractive, trading at a 9% discount to fair value. Both the growth and core categories are trading at fair value, having fallen from trading at 8% and 3% premiums, respectively, at the end of March.

By capitalization, small-cap stocks remain the most attractive at an even deeper 20% discount, followed by mid-caps at a 7% discount, while large caps are near fair value, trading at only a 1% discount to a composite of our fair values.

Based on these valuations, we recommend overweight positions in value and slight underweights in core and growth to fund the overweight in value. By capitalization, we advocate for an underweight position in large-cap stocks in favor of overweighting small-cap stocks and a slight overweighting in mid-cap stocks.

Price/Fair Value by Morningstar Style Box Category

Real Estate Retreats, Overvalued Tech Tumbles, and Healthcare Hemorrhages

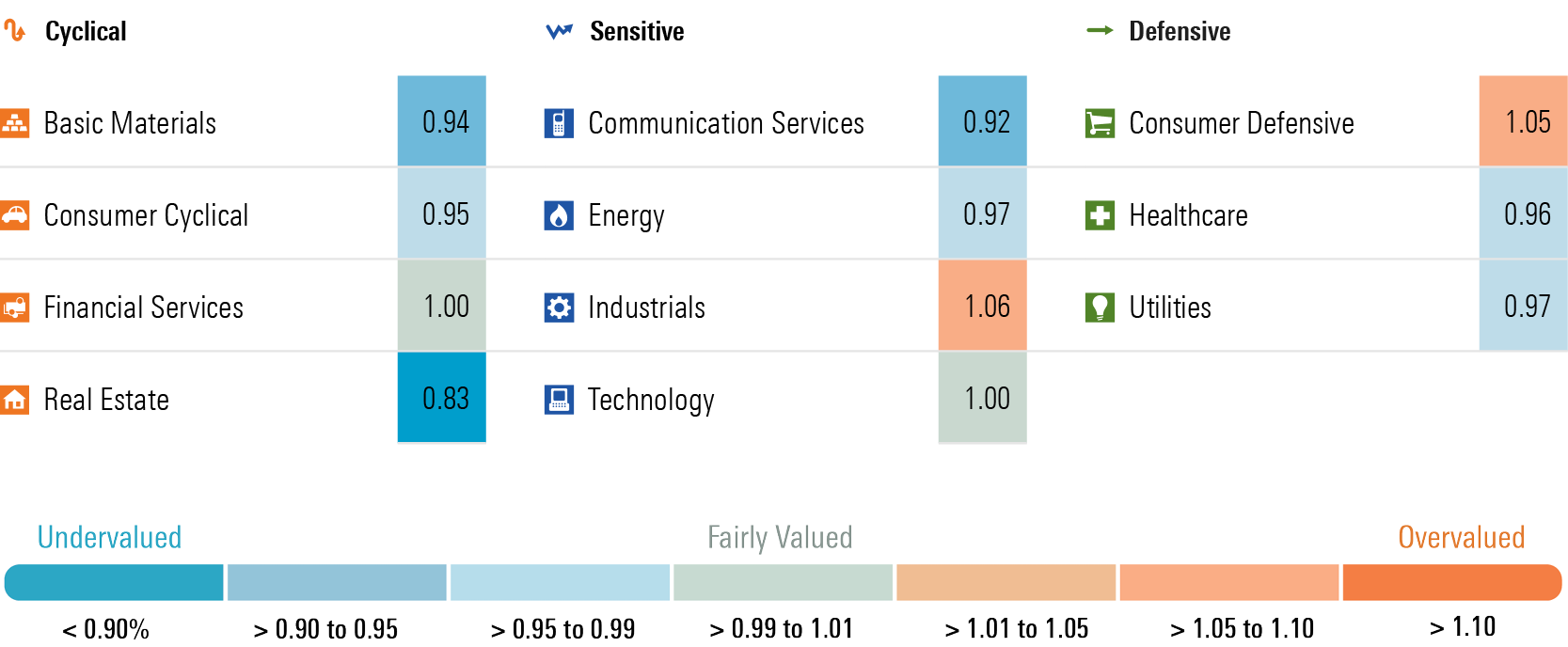

The three worst-performing sectors in April were led by real estate, which dropped 8.14%, followed by technology falling 5.71%, and healthcare, which declined 5.24%.

Within the real estate sector, losses were widespread, with only a handful of stocks able to register gains. Much of the pullback was likely due to increasing interest rates, as real estate is negatively correlated with interest rates. During April, the yield on the 10-year US Treasury bond rose 40 basis points. Some of the leading detractors in the real estate index included REITs focused on industrial facilities and data centers. While we would continue to shy away from urban office space, we continue to see opportunities in real estate assets that have defensive characteristics, such as those tied to healthcare facilities (Ventas VTR and Healthpeak DOC) or triple net lease providers (Realty Income O), that trade at a wide margin of safety from our intrinsic valuation and pay healthy dividends.

Technology was the second most overvalued sector coming into April. One general takeaway from this earnings season is that, while many of those technology stocks directly tied to artificial intelligence continued to perform well, those technology stocks that are tied to traditional technology sectors have struggled, as their outlook is more closely tied to the lackluster economy. Between the amount the technology sector fell and incorporating a few rare fair value increases, the technology sector is now trading at fair value and can be moved to a market weight from underweight. One notable change following earnings was our 20% increase in fair value for NXP Semiconductors NXPI. This was the single largest increase in fair value this earnings season across our US coverage. It was enough to drive NXP into 4-star territory as the stock is trading at a 13% discount to the updated fair value. ServiceNow NOW also moved into 4-star range as the stock pulled back slightly after earnings, whereas we slightly lifted our fair value.

Within the healthcare sector, losses were widespread as only a handful of stocks within the sector were able to register gains in April. Healthcare was trading at a slight premium to fair value at the end of March and is now trading at a 4% discount. Following the pullback in healthcare, we are seeing a number of stocks that rarely have traded at much of a discount, such as Johnson & Johnson JNJ, slip into 4-star territory. The most notable exception was Eli Lilly LLY. Eli Lilly put up good numbers for the first quarter, and we increased our fair value 8% to $540. However, we continue to think 2-star-rated Eli Lilly is significantly overvalued and is in fact one of the most overvalued stocks across our coverage. Within healthcare, we prefer stocks such as Medtronic MDT and Zimmer Biomet ZBH, which not only trade at a discount to our fair values and have long-term durable competitive advantages but also are tied to the long-term secular trend of the aging baby boomer generation.

Utilities’ Upward Bound; Energy & Consumer Defensive Lose Least

The three best-performing sectors in April were utilities, which rose 1.69% (the only sector to register a gain in April), energy, which only fell 0.88%, and consumer defensive, which retreated 1.31%.

While we still see a number of attractive stocks in the utility sector, such as Entergy ETR and NiSource NI, the sector as a whole is now only trading at a 3% discount from fair value. The sector had traded as much as a 17% discount last October. We continue to think the fundamentals for utilities are as strong as they have ever been, but as discounts have narrowed, we recommend moving toward a market-weight position from an overweight position in utilities.

Within the energy sector, large exploration and production companies such as Exxon Mobil XOM and Chevron CVX rose slightly, whereas services companies such as Schlumberger SLB and refiners such as Phillips 66 PSX slid. While the broad sector only trades at a 3% discount to fair value, we continue to think the sector provides a natural portfolio hedge against inflation and heightened geopolitical risk.

Within the consumer defensive sector, some of the largest detractors to performance in April included stocks that started off the month in 2-star range, including Target TGT, Monster Beverage MNST, and Walmart WMT, as well as 1-star-rated Costco COST. Where we see the best value for investors is in the consumer packaged-food area such as 4-star-rated Kellanova K and General Mills GIS. These companies have been under pressure as they have struggled to raise prices as fast as their own costs, but as inflation moderates, we expect they will be able to raise their operating margins back toward historical averages as price increases and efficiencies improve.

What We See Across Our Remaining Sector Coverage

Among the other sectors, we continue to see attractive opportunities in the communications sector. Alphabet GOOGL is rated 3 stars and trades at a 7% discount to our $179 fair value, which we bumped up following a strong first quarter. Meta Platforms META remains overvalued as it trades at an 11% premium to fair value, but it is trading at much less of a premium following its 11% decline in April. In our opinion, many of the more traditional communications stocks such as AT&T T and Verizon VZ provide a significant margin of safety from our intrinsic valuation and offer high dividend yields.

The basic materials sector is trading at a 6% discount. Within the sector, two areas we find especially attractive include the gold miners and crop chemical producers. Gold miners such as Newmont Mining NEM trade at a deep discount to our fair value, even though we have a relatively bearish view on the long-term price of gold. If gold prices stay elevated or move higher, we think there is even greater upside potential. Crop chemical producers, such as FMC Corporation FMC, fell throughout 2023. The agricultural industry overordered too much product in 2021-22 because of supply constraints and shipping bottlenecks. As a result, sales were constrained in 2023 as those excess inventories were used up. We think the supply/demand dynamics will normalize this year and therefore see opportunity in undervalued crop chemical producers.

Industrials remain overvalued and should be underweighted in portfolios. Within the industrials sector, transportation stocks such as Saia SAIA and XPO Logistics XPO remain some of the most overvalued names across our coverage. One of the few areas we see undervalued stocks in this sector include aerospace and defense contractors such as RTX Corporation RTX.

Morningstar Price/Fair Value by Sector

Worst of Both Worlds: Slowing Economic Growth and Higher Than Expected Inflation

While our US economics team had projected that the rate of economic growth would slow in the first quarter, even we were surprised by the paltry 1.60% annual rate of real gross domestic product growth. Looking forward, we continue to expect a sluggish economy over the remainder of the year. We project quarter-over-quarter real GDP growth to hover around 1.00%-1.25% annualized through early 2025, with year-over-year growth troughing at 1.20% in first-quarter 2025.

Our inflation forecasts for 2024 have ticked up again after a string of unexpectedly high readings. As a result, our US economics team pushed back when it thinks the Fed will first begin to lower the federal-funds rate to September.

While inflation has remained stickier than we originally modeled, our US economics team continues to expect that the rate of inflation will moderate. Real-time indicators of rent prices indicate that shelter inflation will slow in the months ahead and a sluggish economy will result in slower job growth and slow down wage growth. Additionally, the impact of high interest rates will slow consumption, especially among high-ticket durable goods that are financed such as housing and autos.

What’s an Investor to Do?

With the broad equity market trading at fair value, we advocate for investors to position themselves at a market weight within their targeted long-term asset allocations between equity and fixed income. With the rate of economic growth projected to slow for the next few quarters, stock markets could become increasingly volatile this summer and pullbacks could provide an opportunity to move back to overweight equity positions.

Within the equity portion of a portfolio, we continue to see the best valuation in the value category and in small-cap stocks. Undervalued sectors to overweight include real estate, communications, and basic materials. However, within these sectors, we think individual stock-picking remains vital.

Within the fixed-income allocation of portfolios, we advocate for moving further out on the yield curve to lock in currently high interest rates as our US economics team forecasts long-term rates to decline. However, we continue to think that credit spreads for both investment-grade and high-yield corporates are not wide enough to compensate investors for downgrade and default risk. As a result, we suggest investors focus on government bonds.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/MQJKJ522P5CVPNC75GULVF7UCE.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZYJVMA34ANHZZDT5KOPPUVFLPE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/S7NJ3ZTJORFVLCRFS2S4LRN3QE.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/54f9f69f-0232-435e-9557-5edc4b17c660.jpg)