The Harrowing Story of a Top Manager’s Biggest Investing Mistake

Oakmark’s David Herro waited years for Credit Suisse to deliver. It never did.

/s3.amazonaws.com/arc-authors/morningstar/657019fe-d1b1-4e25-9043-f21e67d47593.jpg)

Professional investors make mistakes all the time. It’s part of the job. But some matter more than others.

When David Herro, lead manager of Oakmark International OAKIX, sold the last of the fund’s shares in Credit Suisse earlier this year, it was no ordinary transaction. This was not a bottom-of-the-portfolio bet that happened to fall short. Credit Suisse had once been a leading Swiss bank. Herro had owned it for two decades. For much of that time, he was one of its most prominent supporters. Often he provided an optimistic take on Credit Suisse when most other investors harbored doubts.

But by the end, Credit Suisse had become notorious, associated not with respectable wealth management but with scandals, missteps, regulatory penalties, and a plummeting share price. When Herro disposed of those final shares, a long, fraught relationship marked by disappointment and controversy had reached its end. No wonder he recently told Morningstar that, after the final sale, it felt as if an immense weight had been lifted from his shoulders.

The Value Investor’s Challenge

Herro, who has managed Oakmark International since its 1992 inception, is known as a value investor—one who seeks companies whose share prices are depressed because the firms are small or obscure, have unrecognized potential, or face real but fixable issues. Herro placed Credit Suisse in the latter camp and stuck with it through its travails. With many other holdings over the years, Herro’s contrarian instincts—his willingness to flout conventional wisdom—paid off. Not this time.

A Remarkable Panoply of Woes

Herro first bought Credit Suisse for the fund in the summer of 2002. Given the size of Oakmark International’s asset base, and because other Oakmark vehicles also owned it, Harris Associates—Oakmark’s advisor—became one of the bank’s top shareholders, in later years holding more than 8% of its shares. Herro became one of Credit Suisse’s most visible backers (except for the times he became its most vocal critic). He didn’t just opine from the sidelines, either; he met regularly with bank management.

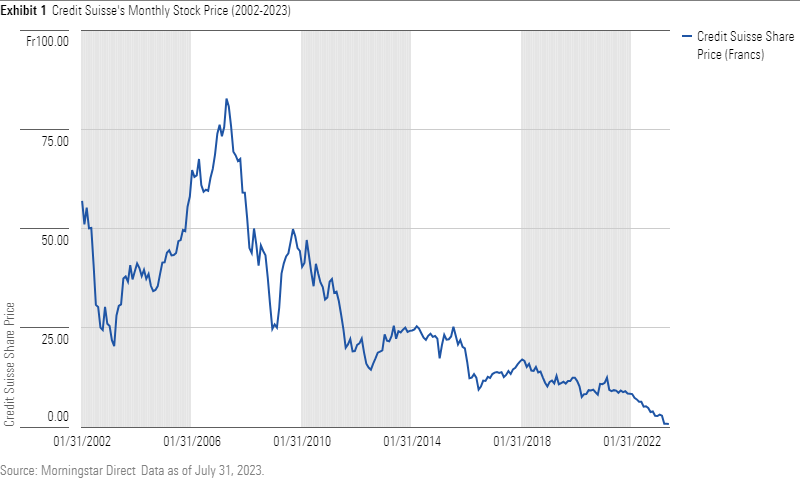

The initial years went swimmingly—the shares soared in the four years or so after Herro bought them. But over the remainder of Oakmark International’s two-decade relationship with Credit Suisse, a remarkable panoply of woes dogged this once-respected Swiss bank. While none quite matched the spectacle of Nissan CEO Carlos Ghosn’s stealth escape from Japan hidden in a crate, some came close. The number and variety of these incidents was so vast that a Morningstar timeline covering just the past three years struggled to find room for all of them.

The misdeeds spanned quite a range. They included violating U.S. sanctions against Iran; enabling tax evasion in Germany, Italy, and the United States; failing to catch money laundering by a Bulgarian drug ring; hiring private detectives to spy on a recently departed colleague and others; a bribery scandal involving Mozambique loans—aka the “tuna bonds” affair; and in 2021, disastrous involvements with the failed U.S. hedge fund Archegos and the U.K. lender Greensill. There’s more.

Credit Suisse’s reputation fell dramatically throughout the period, and its share price nose-dived.

Credit Suisse's Monthly Stock Price

Credit Suisse was by no means the only major bank engaging in dubious or illegal activities during this time. But the level and frequency of its misconduct stood out even when placed in that disheartening context.

Why Herro Owned—and Continued to Own—Credit Suisse

Herro held Credit Suisse for more than two decades. Although it usually sat near the top of the portfolio, it wasn’t an outlier. It rarely had the highest weighting, and it was consistently joined in the portfolio’s top 10 by other European banks—most notably BNP Paribas BNP, Intesa Sanpaolo ISP, and Lloyds Banking Group LLD. The four banks typically had roughly similar weights in the portfolio.

While not free of misconduct themselves, those other banks never attracted the waves of notoriety that engulfed Credit Suisse. Thus, even given its relatively modest weights, Herro’s lengthy attachment bears investigation. What kept him attracted to a bank that continually made the news for its problems rather than its achievements?

Fortunately, Herro has often made clear his thinking. His initial purchase, he recently explained to Morningstar, occurred when the share prices of many European banks had been pummeled owing to their exposure to technology firms that were struggling in the early 2000s’ growth-stock rout. He thought the banks had adequately dealt with that issue. A rebounding franchise seemingly available at a bargain price is a value investor’s dream. Herro dove in.

It was a wise move: The stock performed remarkably well over the next several years—until its price sank during the global financial crisis. In the summer of 2008, amid that meltdown, Herro expressed confidence, telling Morningstar analysts that Credit Suisse was one of the companies he felt would be able to thrive despite the dire conditions because of its leadership position in its field.

Instead, Credit Suisse endured a series of stumbles. Nevertheless, Herro stuck with it, and at the Morningstar Investment Conference in 2014, he explained in detail why he still owned it. In that interview, Herro said he had as much confidence in Credit Suisse as ever. He described its wealth-management unit as “a really good business,” noting it was one of the world’s largest such entities with “revenues and profits grow[ing] midsingle digits consistently through time.” He conceded that Credit Suisse’s investment bank was less impressive, having been too aggressive in the past. But he believed its leaders had learned their lesson and had reduced risk. “You didn’t see huge write-downs and huge losses on all the CMOs and these things [that you saw] at the other investment banks. So, they did a very good job at preserving value there.”

He said these two entities, along with Credit Suisse’s other units, made for a combined business that “generated good cash flow streams that sells, in our belief, under 10 times normal earnings and less than 1 times book.” He called this “a very good dynamic for a company that, from here, should be growing cash flows by at least midsingle digits over the medium and long term.”

A reasonable, defensible case. Yet problems continued to plague the investment bank, which not only posted weak financial performance but also accounted for most of Credit Suisse’s embarrassing and costly regulatory and legal wrangles. A few years and many unpleasant headlines later, Herro remained a Credit Suisse supporter, but with a caveat. He told Morningstar analysts that its wealth-management operation remained strong but allowed that the investment bank needed work. He thought improvement was possible.

From Secret Surveillance to a Bitter Boardroom Battle

Herro’s confidence remained intact even after the scandal that thrust Credit Suisse beyond the financial headlines into the tabloids. In 2019, Credit Suisse executives were caught conducting surveillance on a recently departed colleague, suspecting him of recruiting others to join him at rival bank UBS. They instructed private detectives to follow him by car and on foot. When he noticed he was being tailed, he confronted the detective and filed a police report. Later, it became clear that he hadn’t been the only Credit Suisse executive under surveillance.

The bizarre affair—which included the apparent suicide of a security contractor hired by the Credit Suisse executives masterminding the operation—became a staple of news coverage for months afterward.

Credit Suisse’s CEO at the time, Tidjane Thiam, came under fire. An independent investigation concluded that Thiam had not known of the spying campaign, which was pinned on the bank’s chief operating officer. But critics argued that Thiam was responsible for the culture that allowed such behavior. Herro called the affair “quite a soap opera and a distraction,” according to The Wall Street Journal, but he defended Thiam. Herro had been impressed by Thiam’s wide-ranging reorganization plan—which included reforming the investment bank—and urged the board of directors to retain Thiam. He advised the directors to oust the board chair, Urs Rohner, instead. Herro argued that Rohner, who’d held leadership roles at Credit Suisse for much longer than Thiam had been CEO, bore more blame for the bank’s many missteps. But the board went ahead and forced out Thiam.

Herro angrily denounced the decision. Yet he continued to believe in Credit Suisse’s future.

The Tipping Point That Wasn’t

Herro now concedes he should’ve seized this opportunity to walk away. The CEO who had implemented changes that Herro had long wished for—and which were bearing fruit in the bank’s financial results—had left the scene. Remaining in charge were the chair in whom he had no confidence and the board that had explicitly rejected his advice. Why stick around?

Herro says a main reason was that Rohner said he’d be leaving in a year, and Herro figured that the new CEO, not Rohner, would make the key decisions in that period. Yet even if those expectations justified hanging on for a while after Thiam’s departure, Herro could have changed his mind at any time thereafter. Indeed, the events of the following year offered further incentive to sell.

Constantly in the Headlines—and Not in a Good Way

In early 2021, two more scandals rocked Credit Suisse. First, Greensill Capital, a U.K. financial firm involved in complex lending operations, collapsed. It emerged that Credit Suisse had been deeply involved with the firm and its CEO. Swiss regulators later concluded that Credit Suisse had “seriously breached its supervisory obligations” in the affair.

A few weeks later, Credit Suisse became entangled in the demise of U.S.-based hedge fund Archegos Capital. A review by an outside law firm placed the blame on “a fundamental failure of management and controls” in Credit Suisse’s investment bank and added that its focus on maximizing short-term profits “enabled Archegos’s voracious risk taking.” But Herro was unfazed, touting the firm’s potential in a late March 2021 interview with Bloomberg TV. The damage can be repaired, he said, voicing confidence in the incoming chair to spruce things up.

But that chair—António Horta-Osório—lasted less than nine months, pressured to resign owing in part to his breaking COVID-19 protocols. Other executives already had been sent packing after the Archegos and Greensill debacles, including Credit Suisse’s chief of risk and compliance; the head of the investment bank; that unit’s head of credit risk; and a number of others.

Despite the turmoil, as late as the second and third quarters of 2022, Herro was still buying shares of Credit Suisse for Oakmark International, even as he trimmed many other holdings. In Oakmark International’s Sept. 30, 2022, annual report, he wrote that investors were “over-penalizing Credit Suisse for past errors” and offered detailed reasoning why he expected it to bounce back.

Enough!

A few weeks later, though, Herro finally gave up. He says the final straw was a complicated restructuring plan that included a proposal to spin off the investment bank. One might think that idea would appeal to Herro, but he told the Financial Times that the structure of the plan was “cumbersome and far more costly in terms of cash burn than we expected.” Later he wrote that the spinoff plan provided “NO insight into the proceeds from the asset sales as well as the costs of restructuring the investment bank.”

Moreover, he had lost faith in Credit Suisse’s wealth-management business, long the bulwark of his investment thesis. “There have been large outflows from wealth management,” he told the Financial Times, calling into question “the future of the franchise.”

Herro recently told Morningstar that some facets of the restructuring plan seemed unwise and the sheer complexity and opacity of the proposal made it impossible for him to accurately value Credit Suisse. A value investor who can’t ascertain a firm’s value can’t determine whether to own it.

Therefore, in 2022′s fourth quarter, he sold nearly one third of Oakmark International’s Credit Suisse shares. In the new year, he gradually dumped the rest, completing the task around March 1. A few weeks later, Credit Suisse itself was gone. The collapse of Silicon Valley Bank and other U.S. regional lenders had prompted investors to cast a skeptical eye on other banks that appeared to be on shaky ground. Credit Suisse’s finances couldn’t withstand the scrutiny. With investor confidence evaporating and its share price nearing zero, Credit Suisse was taken over by UBS in a controversial deal brokered by the Swiss government.

In a Financial Times piece following Oakmark International’s final sale, Herro sounded exhausted, frustrated, and somewhat mystified at the dismal conclusion of his two-decade journey with Credit Suisse. “It has been a measurable drag on our performance,” he conceded. He realized that an investor “can’t win every time” but candidly admitted that, although he meets with every company he owns, “you spend a lot more time with your problem children. Credit Suisse has been a drain of time and value for years.”

Few would argue with that conclusion.

The Case for the Defense—and What Went Wrong

A problem child indeed. But while selling a child is not an option, selling a stock is. Herro could have sold Credit Suisse at any time. Why didn’t he?

First, Herro, an astute investor, wasn’t imagining things when he touted Credit Suisse’s wealth-management arm. It was indeed one of the biggest and most highly regarded of such operations. By 2019, The Wall Street Journal reported, revenue from wealth management had grown to nearly two thirds of Credit Suisse’s overall total, up from around half when Thiam had become CEO four years earlier—a result of Thiam’s reforms and just the type of mix Herro seemed to prefer. In June 2019, the asset level in the wealth-management business stood at its highest level ever.

Second, when assessing a company, fund managers don’t simply assemble a portfolio of the “best” companies, however defined; they balance the quality of a firm and its future prospects against its share price. A value-oriented investor such as Herro wouldn’t have to believe that Credit Suisse, judged solely as a business, outshone any other company he could have owned. He only had to believe that Credit Suisse’s prospects and the depressed level of its stock price, considered together, made it a compelling choice.

Third, whenever Herro may have had reason to doubt the wisdom of holding on, there was always a reason to stick around: a new CEO, a new chair, a revised action plan, or a commitment to finally buckle down on risk management. It would be understandable if, having hung on for so long, it felt reasonable to give the new person or plan a bit more time to succeed.

What went wrong? Most notably, an ever-optimistic mindset can lead to an endless cycle of dashed hopes. Herro himself alluded to that idea when he provided a concise, candid accounting of his history with Credit Suisse in Oakmark International’s March 2023 semiannual report. Although Credit Suisse endured “repeated lapses in risk management,” he wrote, he and his team “incorrectly remained focused on our sum-of-the-parts valuation and gained comfort in the strong performance of the wealth management, asset management, and Swiss Universal Bank businesses as they continued to generate better-than-average returns. We believed [they] represented good value and that the investment bank was repairable. Despite numerous attempts by multiple leadership teams at Credit Suisse, our thesis was proven wrong.”

A Muted Impact

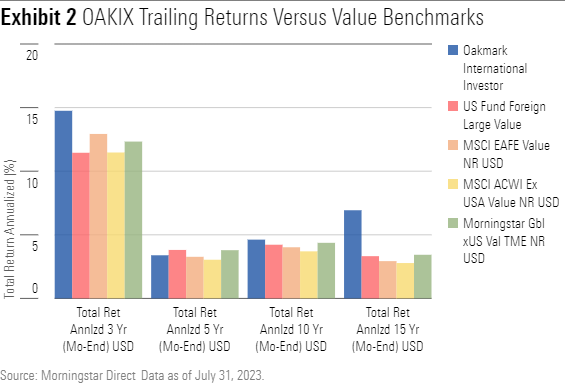

The debacle could have sunk Herro’s reputation and decimated Oakmark International’s returns. Yet despite some very tough years—2018 and 2022 stand out—as of July 31, 2023, Oakmark International’s 10-year record beat 60% of its foreign large-value Morningstar Category rivals and its 15-year return topped all of them. Even its three-year record, which includes a bottom-decile showing in 2022, was in the top quartile. Its 15-year record also surpassed all relevant value and core indexes by wide margins and the 10-year record beat the value indexes.

OAKIX's Trailing Returns Versus Value Benchmarks

How did it stay above water, even prosper, given its continued ownership of such a troubled stock? One answer lies in Herro’s weighting decisions. Despite his oft-expressed confidence in Credit Suisse’s prospects, he never allowed the bank to take up an inordinate amount of assets. True, a weighting of 5%, which it occasionally had, can have an impact. But more often, Credit Suisse had more-modest weights of 3% to 4%—meaning, of course, that more than 95% of the fund’s assets was devoted to other companies or sitting in cash.

Even at the top of its range, at just over 5%, the weight assigned to Credit Suisse was far from the stakes of 8% to 20% or higher allocated to stocks that have memorably exerted damage on other concentrated funds, such as Longleaf Partners LLPFX, Sequoia Fund SEQUX, and Invesco Global Opportunities OPGIX.

In fact, position sizes of 7% or 8% can be found currently in a variety of diversified funds. In recent years, many large-growth managers have felt compelled to place 11% or 12% of assets in Apple AAPL and Microsoft MSFT merely to match those stocks’ weights in the benchmark.

Not Off the Hook

That doesn’t mean Herro’s Credit Suisse attachment had no cost. He concedes that fund shareholders paid a penalty for his devotion. He recently told Morningstar that Oakmark’s calculations placed the cost at 21 basis points (0.21 percentage point) of total return on an annualized basis over the course of the fund’s ownership. That might not sound like much, but over two decades, a meaningful amount of money was subtracted from a loyal shareholder’s account.

Put another way, Herro said, the fund lost roughly two thirds of its investment in Credit Suisse over the full holding period. And shareholders who bought in during recent years, when Credit Suisse’s share price was almost continually falling, didn’t get the benefit of the earlier occasional bounces.

More broadly, Herro’s willingness to stick with out-of-favor or struggling companies, including those that eventually pay off, results in unusually volatile performance patterns that can prompt some shareholders to sell at inopportune times rather than deal with the roller-coaster ride. For example, net outflows surged in the fourth quarter of 2018, a year in which the fund’s 23.5% loss was far worse than the respective 15.4% and 14.4% losses of the foreign large-value and foreign large-blend Morningstar Categories. Those who fled missed out on the following year’s 24.2% gain, which was well above the category averages.

What Can We Learn?

Oakmark International’s history with Credit Suisse is complex. Fund investors hoping to draw one simple lesson will likely come up short. Choosing funds that buy only the most popular stocks would be a recipe for average performance or worse. Ditto for avoiding managers who stick with downtrodden companies when it seems obvious they should bail. Struggling or controversial investments often pay off further down the line.

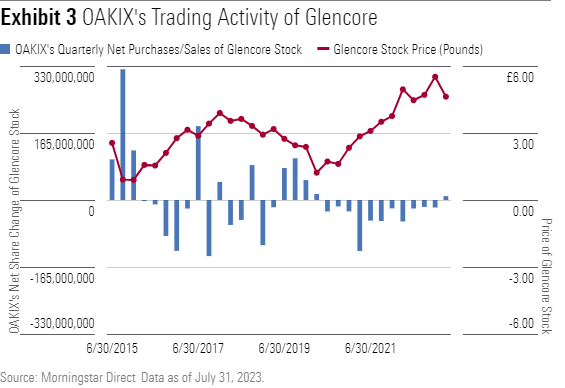

Examples appear in Oakmark International’s own portfolio. Herro bought heavily into mining and trading firm Glencore GLEN in 2015 after its share price had plummeted, and then traded in and out, generally at opportune times, as its share price quickly soared, then declined a bit, then rose again. The fund garnered huge gains, without getting overexposed to the stock.

OAKIX's Trading Activity of Glencore

Meanwhile, two other holdings—Ashtead AHT and Safran SAF—provide examples of Herro’s patience paying off. In both cases, the stocks—a U.K. industrial group and a French aircraft equipment firm, respectively—provided nice gains in the first years, fell back, and then really took off four or five years after the initial purchase.

That said, investors can benefit from evaluating management missteps. How often do the manager’s picks misfire? Are these incidents inconsistent with the manager’s style, philosophy, and experience? For example, perhaps one wouldn’t penalize a value manager for buying an out-of-favor stock that failed to rebound but should be less forgiving if the damaging purchase was a high-priced growth stock in a sector with which the manager has little familiarity.

For fund managers, the lesson might be more clear-cut. While they can often succeed by owning assets that others shun, they need not overdo the commitment. That applies to both the weighting and the length of time allowed for the thesis to work out. In the case of Credit Suisse, Herro limited the weighting but allowed his overly optimistic take on the investment bank to linger far too long.

Perhaps the most apt lesson comes from successful managers we’ve spoken with in the past: Don’t follow the crowd, but don’t ignore it either. Sometimes the crowd is right.

Note: Associate manager research analyst David Carey and senior manager research analyst Jack Shannon contributed research and graphics assistance for this article.

The author or authors own shares in one or more securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

/d10o6nnig0wrdw.cloudfront.net/07-25-2024/t_56eea4e8bb7d4b4fab9986001d5da1b6_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/BU6RVFENPMQF4EOJ6ONIPW5W5Q.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/657019fe-d1b1-4e25-9043-f21e67d47593.jpg)