A Bold Fund Blindsided by a Biotech Blowup

Invesco Global Opportunities took a big hit when its Nektar stock lost that sweet taste.

/s3.amazonaws.com/arc-authors/morningstar/657019fe-d1b1-4e25-9043-f21e67d47593.jpg)

Not being a fund manager myself, I can’t say for sure what a manager’s worst nightmare would be. But here’s one possibility: A company near the top of your portfolio—a longtime favorite of yours, with more than 5% of fund assets—suddenly declares its most prominent product doesn’t work. It then lays off 70% of its workforce. The stock price plummets. At mid-year, its price sits nearly 80% lower than it had been a year earlier.

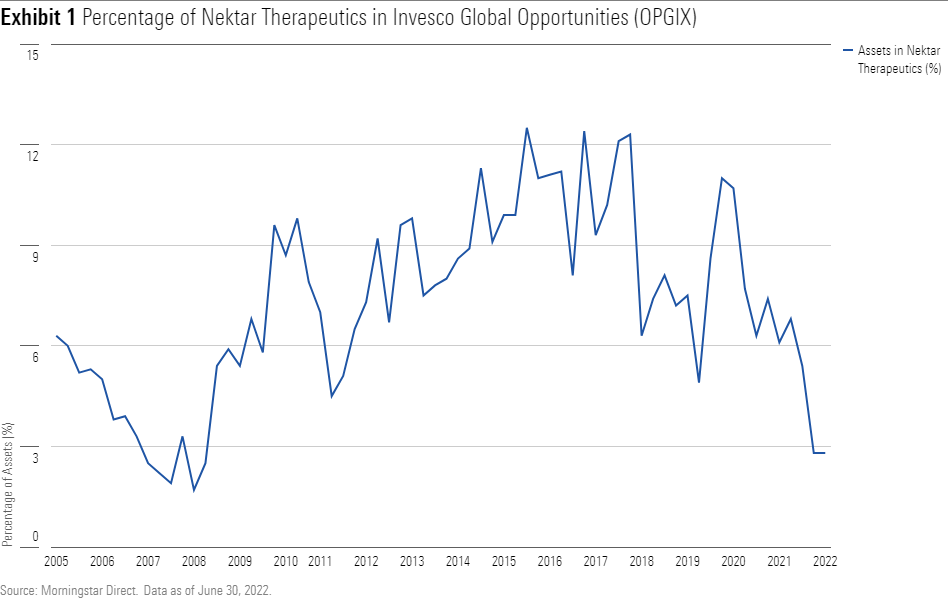

That dreadful scenario struck Invesco Global Opportunities OPGIX this year. The culprit was Nektar Therapeutics NKTR, which lead manager Frank Jennings has owned for more than 20 years. Often, it's been the fund’s top holding; it’s rarely been lower than No. 2. More important, Nektar stock has consistently had a weighting of 5% to 10% in the portfolio—occasionally, even a bit more.

The story illuminates several key issues faced by fund managers and fund investors alike. Where is the line between the taking prudent risks to avoid index-hugging, and stretching too far in that pursuit? Which miscalculations are understandable, and which can be faulted? This episode also reveals that the most critical determinant of investment outcomes is not always what you own, but how much of it, and when.

Small Stock, Big Shock

Nektar’s most-watched drug, known as bempeg, had shown much promise treating various types of cancer in earlier trials conducted in combination with a drug from Bristol-Myers Squibb BMY. But this March, it failed the late-stage trial for one potential use. Then, in April, Nektar and Bristol-Myers Squibb announced that bempeg had failed two other trials. The companies stopped all trials and abandoned further plans for the drug. Investors pummeled Nektar’s share price in March and pushed it down further in the following months.

The fund’s troubles weren’t confined to Nektar. With the market souring on high-priced growth stocks, and technology in particular, other holdings also plunged in value. Top-holding Advanced Micro Devices AMD (6.5% of the portfolio entering 2022) was down 41% through Aug. 31. Nordic Semiconductor NDCVF (2.2%) and Exact Sciences EXAS (1.6%) sank 56% and 54%, respectively.

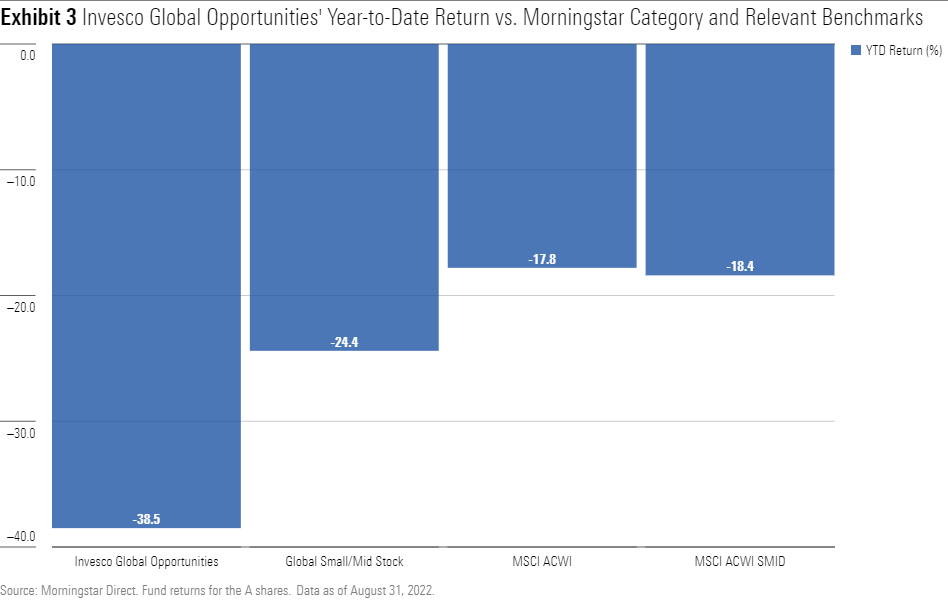

As for the fund itself, its A shares were down 38.5% for the year to date through Aug. 31, nearly 14 percentage points worse than the global small/mid stock Morningstar Category average and about 20 points behind the MSCI ACWI and MSCI ACWI SMID indexes.

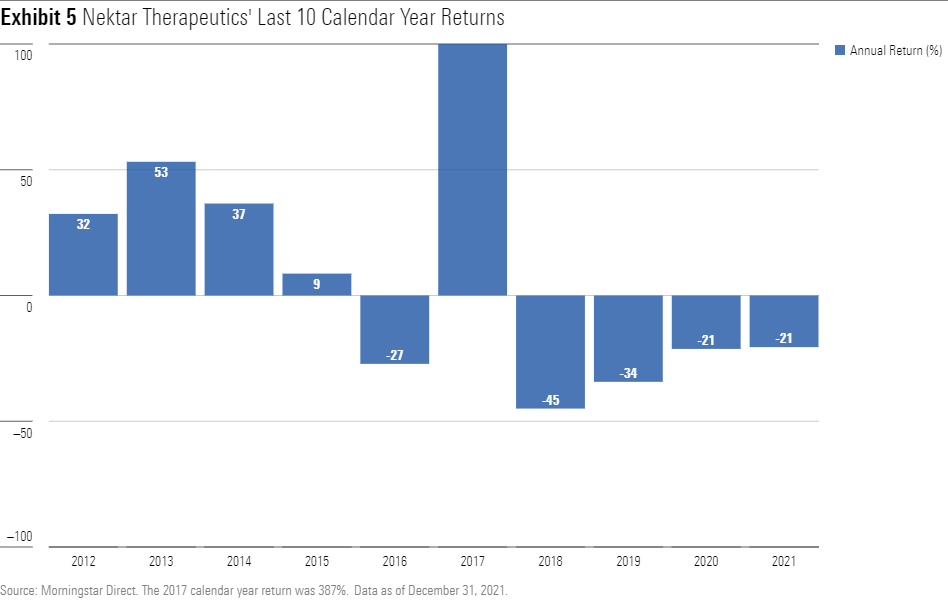

At least Advanced Micro Devices, Nordic Semiconductor, and Exact Sciences had produced impressive—in some cases spectacular—gains in the prior few years. By contrast, Nektar Therapeutics—which, by the way, isn’t profitable—had posted declines of between 20% and 45% in each of the four years before its disastrous 2022.

An Unusual Approach That Delivered

Although it looks like an awful mistake now, owning Nektar stock was consistent with Jennings’ approach. (He now works with comanager Máire Lane, who joined him as an analyst in 2017 before her 2020 promotion.) For years, Jennings has devoted the bulk of the portfolio to small and midsize healthcare, biotech, and technology stocks. He’s willing to own unprofitable companies with the expectation that at some point—maybe years away—they would post impressive earnings.

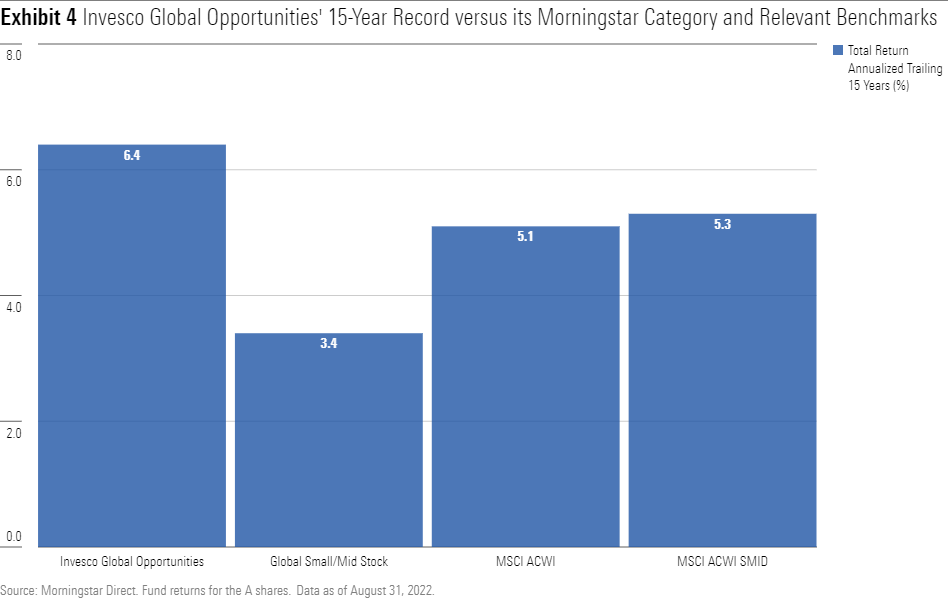

Despite some rocky stretches, this approach paid off handsomely over the long run. For the 15 years through 2021, the A shares’ annualized return of 10.6% crushed the global small/mid stock average of 7.6% and also topped the MSCI ACWI and MSCI ACWI SMID indexes, which gained 7.1% and 7.3%, respectively. Even after this year’s pummeling, the fund’s 15-year record through Aug. 31 stood well above the category norm and the indexes.

So, Was Owning Nektar a Mistake?

Although certainly not a conservative pick, Nektar does have other drugs in development, so it wasn’t technically a “binary” play—a company dependent on the success or failure of just one product because it doesn’t have any others. Binary stocks face only two possible paths: enormous gains if the drug succeeds, or a stock-price collapse if the drug fails.

However, while Nektar technically wasn’t binary, comanager Lane told Morningstar that investors had begun to treat Nektar as if it were totally dependent on the success of bempeg. Perception became reality.

If there were any doubt that Nektar was no staid holding, a look at its yearly share-price gyrations would put that idea to rest. It had oscillated wildly for many years before 2022.

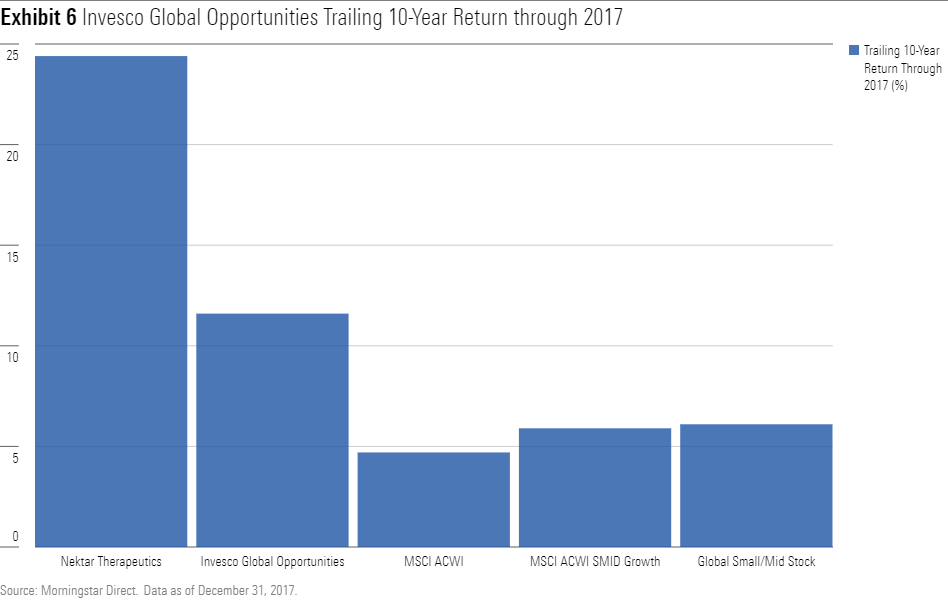

In nine of the previous 10 years Nektar’s stock price either rose or fell at least 20%, sometimes much more. It posted stellar gains from 2012 through 2015, and it rose an eye-popping 386.7% in 2017. Over the 10 years through 2017, owning Nektar stock proved quite a boon for the fund; the stock’s 24% annualized gain during that stretch demolished the indexes—even the growth variant of the MSCI SMID Index—and the global small/mid stock Morningstar Category average. (Even if one extends the period out another year to include the stock’s 45% decline in 2018, Nektar still outperformed by wide margins.)

Thus, it wouldn’t be accurate to look at this year’s disaster and conclude that owning Nektar stock was a mistake. Owning it in other time periods—including some lengthy ones—substantially benefited the fund. In short, it could have been a bold and volatile but ultimately very successful stock pick. Why wasn’t it?

The Investor’s Challenge

The answer is that for a fund manager, deciding to own a stock is just the start. More-complex and consequential decisions await. The manager must decide how much of the portfolio to devote to that stock and whether to fill that position gradually or all at once. After the stock is in the portfolio, the choices multiply. Trim the position size or add to it? If so, when and by how much? At some point, the question becomes when, if ever, to dump it entirely. It’s in the realm of these challenging, ongoing decisions—the importance of which investors often underestimate—that Invesco Global Opportunities’ managers can be faulted.

After all, the managers didn’t put 5% to 10% of assets into every stock they owned. For many years, they deemed only two companies worthy of that level of confidence: Nektar Therapeutics and Advanced Micro Devices. All other holdings received more-conservative allocations, usually 3% of assets or less. The managers even added a bit to their Nektar position in late 2021, keeping it above 5% of assets after its share price had fallen.

No manager can outperform without taking risks; as a result, every manager will make mistakes. But while occasional missteps with small positions can be brushed off, that's not the case with portfolio holdings receiving substantial allocations. They don't necessarily have to post superior performance, but such holdings at least can't crash, for their weights ensure that such declines will have serious consequences for the fund.

Granted, Nektar Therapeutics didn’t enter this year with the 11% or 12% weight that it occasionally had in the past, but even positions half that size can have a deep impact.

What Now?

As of July 31, Nektar remained in the portfolio, at a reduced weight of 2.6%. The marked decline in its weight owed solely to the plunging share price; as of that date, the managers hadn’t sold any shares this year. Nektar was the fourth-largest holding on July 31, barely behind two other sub-3% positions, with Advanced Micro Devices at 7%.

Why continue to own it? Speaking with Morningstar in June, Lane conceded the devastating impact of bempeg’s failure, but said its other drugs, currently in earlier-stage trials, appear promising, and noted that the company is not currently in a cash crunch.

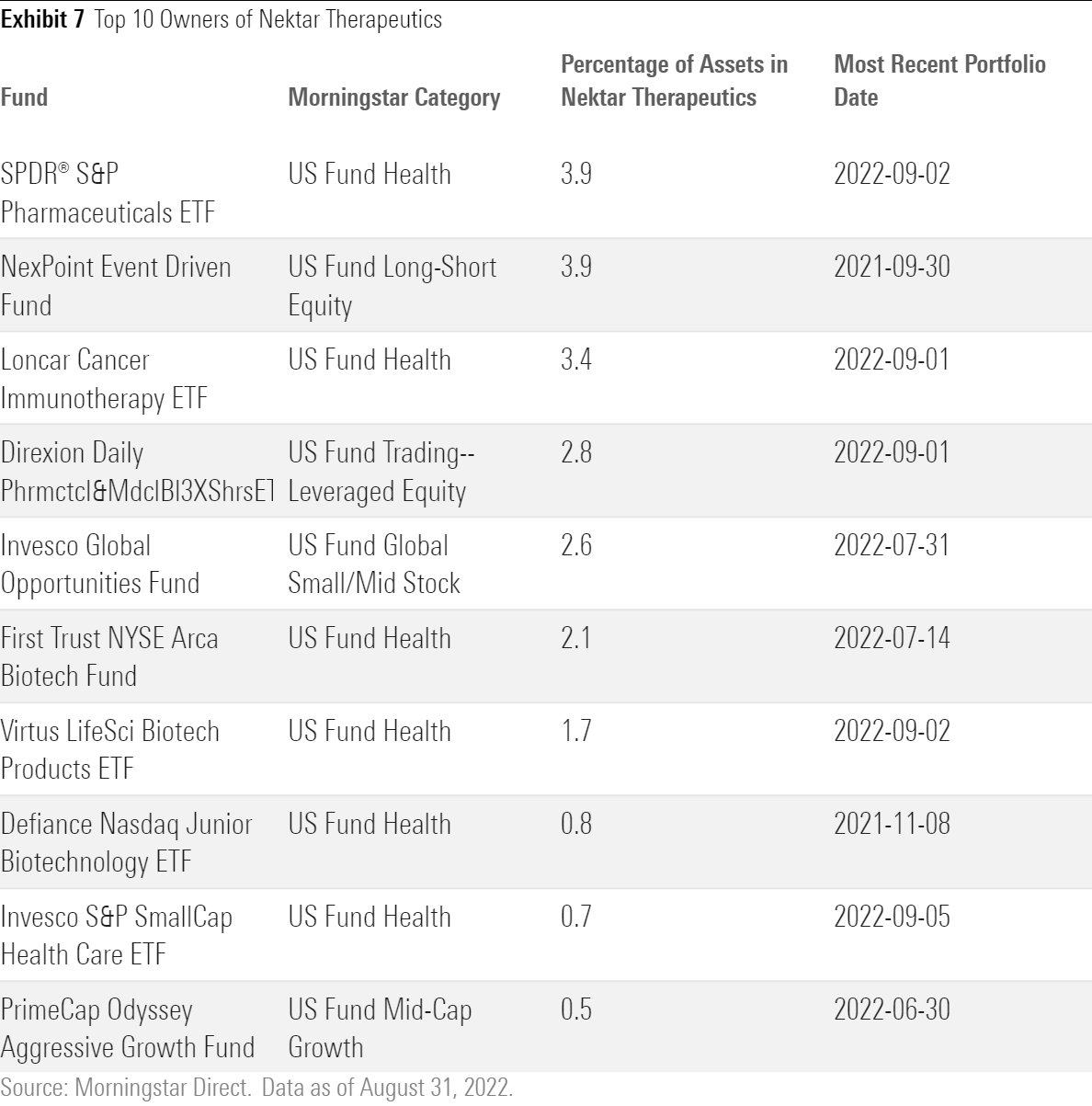

Even if they wanted to trim or sell, the managers might find it a challenging task. According to Nektar Therapeutics’ April 29, 2022, proxy statement, Invesco Global Opportunities owned 19.4% of the company’s shares outstanding as of April 11. (Invesco Ltd. as a whole held 19.8%.) When one investor owns such a large percentage of a company’s shares, it can be hard to sell a meaningful portion of them without depressing the price.

In the latest available portfolios, no other actively managed fund in the global small/mid stock Morningstar Category owned Nektar. No others owned it at year-end 2021, either. Funds in other categories did, and some of those offerings still hold it. But most of them are narrowly focused sector funds with a limited universe of stocks to choose from, or index funds that have no choice but to own it.

Morningstar’s View, Then and Now

Despite Invesco Global Opportunities’ outstanding record, for many years Morningstar manager-research analysts, while not critical or dismissive, have been suitably wary of the fund’s approach. The fund’s stellar long-term performance did not earn it a Morningstar Analyst Rating of Gold, Silver, or Bronze. It has been rated Neutral since 2015, when it was downgraded from Bronze owing to an increase in Nektar’s weighting to about 11% of assets, and, around the same time, the departure of Jennings’ sole analyst for a different position at the firm.

The strategy retained its overall Neutral rating and Average Process and People Pillar ratings even as performance remained impressive. For example, when we covered the fund a little over three years ago—measuring its results through May 31, 2019—its trailing five-, 10-, and 15-year returns all landed in the top decile of the global small/mid stock category. It also beat the MSCI ACWI SMID Index over all of those periods. Yet its Neutral rating remained in place.

The Neutral ratings didn’t mean we foresaw the debacle in Nektar’s future. Rather, we noted the fund’s substantial allocation to one unprofitable stock; the level of risk and uncertainty in its overall approach; and the fact for a long time Jennings had no named successor or even any analysts. There’s a likely successor in place now—comanager Lane—but she has no independent managerial record. With these factors in mind, we couldn’t confidently state that we believed the fund would outperform over a full market cycle.

A Final Note

This episode also demonstrates the importance of investigating a fund’s characteristics before buying. Just because a fund is not labeled as a sector fund doesn’t mean it is broadly diversified. As always, take time to look into the portfolio’s makeup and the fund’s strategy before deciding whether it is appropriate for you. That way, you have a better chance to avoid enduring an investment nightmare of your own.

Research and graphics assistance provided by senior manager-research analyst Jack Shannon and associate manager-research analyst Sachin Nagarajan.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/FGC25JIKZ5EATCXF265D56SZTE.jpg)

/d10o6nnig0wrdw.cloudfront.net/04-25-2024/t_d30270f760794625a1e74b94c0d352af_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/DOXM5RLEKJHX5B6OIEWSUMX6X4.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/657019fe-d1b1-4e25-9043-f21e67d47593.jpg)