3 Themes Shaping the Future of 529 Savings Plans

Despite the evolution of these plans, there's still plenty of progress left to make.

/s3.amazonaws.com/arc-authors/morningstar/eda620e2-f7a7-4aef-bb6c-3fb7f1ac7a38.jpg)

As a graduation month, May augurs promise. Students reflect on the knowledge they have acquired and how to put it to use going forward.

In a year when many 529 savings plans reached the same age as the college graduates who've tapped their tax-advantaged coffers, it makes sense to consider how these savings tools have evolved, how they can improve, and what they might offer going forward.

Since Morningstar assigned its first forward-looking ratings to 529 savings plans in 2012, we've witnessed multiple improvements to these tax-advantaged investing programs as assets climbed from $167 billion to $394 billion.

In the 2021 529 Savings Plan Landscape, we identify a few trends that will continue to shape these plans for investors saving for college, K-12, or other types of education expenses going forward. Morningstar Direct and Office clients can access the full paper here.

- Asset-allocation practices continue to change. There are now 3 times as many portfolios using gradual glide paths to reduce their risk over time--either with target enrollment approaches or age-based steps of less than 10%--than there were in 2016.

- 529 savings plans now offer more flexibility than at any time since they were introduced. Once, investors could only use 529 savings plan assets to pay for college expenses. But as the list of qualified education expenses has grown, 529s are nearing a future where it could be possible for beneficiaries to tap their savings throughout their working lives when personal, social, or economic forces spur them to pivot to new careers or learn new skills, as the pandemic has prompted many to do recently.

- Several highly populated states are working to broaden the accessibility of 529 savings plans through initiatives like child savings accounts.

The Past Year's Top Trends

Last year pandemic-driven campus and economic shutdowns spurred college tuition inflation to sink nearly 50% from a historical 10-year average of 2.8%. Our research shows that all but two 529 portfolios met their goal of beating tuition inflation over the past three years.

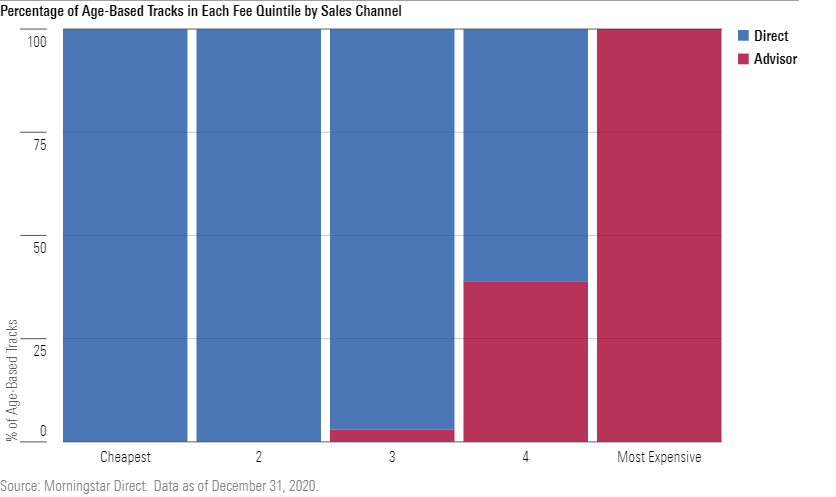

As ever, falling fees across the investment industry have been a boon to 529 beneficiaries, though direct-sold options continue to have an advantage over advisor-sold options, whose average fee is 0.54 percentage points higher. In fact, as shown below, no advisor-sold age-based tracks fall in the cheapest or second-cheapest quintiles. And when it comes to college savings, every dollar paid in fees is one less dollar for educational expenses.

Portfolio improvements haven't all gone smoothly. In early 2021, education savers in The Vanguard 529 Plan got a lucky break that may have amounted to over $200 million in extra earnings. In October 2020, Vanguard applied the wrong recommendations in Nevada's The Vanguard 529 Plan, leaving its accountholders with 20 percentage points more in stocks than they should have had. Luckily, this occurred as equity markets rallied in late 2020 and early 2021, so the mistake actually helped investors.

Nevada, the plan's investment consultant, and Vanguard didn't notice the mistake for several months before fixing it in March, illustrating that vigilant implementation is as important as plan structure, even for straightforward portfolios like Vanguard's. This is reflected in our updated 529 plan ratings methodology, which assigns value to diligent stewardship and thoughtful collaboration between a state and its program manager or investment consultant.

Sharper Asset Allocation in 529 Savings Plans

Age-based portfolios are typically the most popular investment options in a 529 savings plan's lineup, followed by static options. These portfolios start out with more equity-heavy asset allocations and transition to conservative portfolios dominated by fixed income as beneficiaries near enrollment, requiring thoughtful curation.

There are two types of transitions from stocks to bonds, commonly called glide paths:

- An age-based glide path makes abrupt shifts to bonds from stocks at predetermined dates by moving assets from one investment option to another, often every few years on a particular date.

- A progressive track keeps investors' assets in a single investment option--similar to a target-date retirement fund--and uses smaller, more frequent asset-allocation adjustments. This provides a smoother transition that is less susceptible to locking in losses if a rebalance occurs during a period of extreme market stress.

Our research shows asset-allocation rebalances of 10 percentage points or less mitigate much of this market risk.

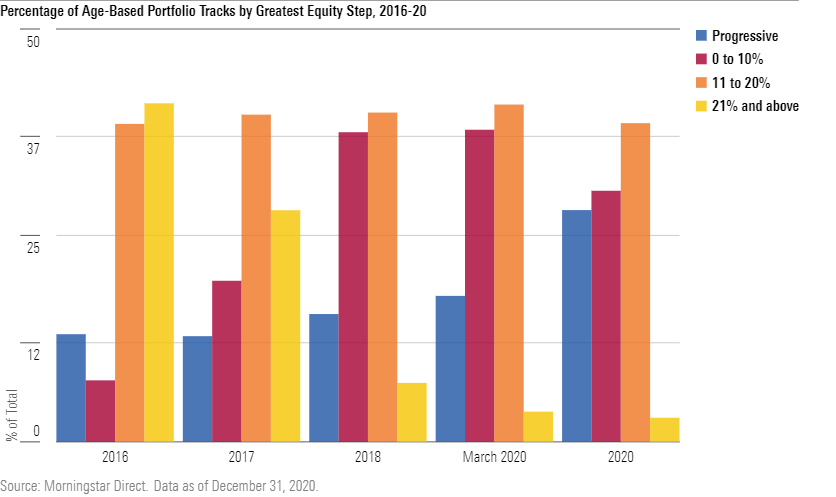

Over time, these age-based portfolios have improved by incorporating more gradual risk reductions. As shown below, the percentage of 529 savings plans with large (21% and above) equity steps has steadily decreased (from 41% in 2016 to a mere 3% in 2020) as the percentage of plans with progressive glide paths or minimized equity step-downs (10% or less) has markedly increased (from 21% in 2016 to 58% in 2020). The percentage of plans with a moderate equity step-down (11% to 20%) remained steady at roughly 40% in each of the past five years.

Enhanced Flexibility on Approved Education Expenses

Once investors could only use 529 savings plan assets to pay for qualified college expenses, but 529 plans now offer far more flexibility than at any time since they were introduced.

In 2017, K-12 educational expenses joined the list of approved uses for the funds, and the 2019 Secure Act made it possible to pay for apprenticeship programs and cover up to $10,000 in outstanding student loan debt. If they keep evolving like this, 529 savings plans could morph into tax-advantaged pools of assets that beneficiaries could tap throughout their working lives in order to pivot to new careers or learn new skills.

Today, investors with nontraditional time horizons or lumpy expenses can use static options, which are stand-alone investments that don't shift asset allocations over time. These options span the risk spectrum, from money market funds all the way to international-stock funds, and plans usually have an array of options for investors to choose from. If flexible spending gains popularity, 529 savings plans could start offering asset-allocation options managed to indefinite horizons, as health savings accounts do.

Treading New Ground to Make Education Accessible

State-sponsored education plans took their current shape under section 529 of the tax code over 21 years ago. Through tax incentives that encourage families to invest over time to fund education expenses, these plans help reduce the burden of education loans on young adults and their families. However, from a tax perspective, higher-income families have benefited the most from these incentives. Currently, joint filers making $80,000 or less don't pay taxes on investment gains in taxable accounts. This, in turn, has shaped 529 plan participation, which skews to wealthier households.

Many states are working to broaden the accessibility of these investment tools to include lower-income households. Child savings accounts are one idea. These state programs, such as Pennsylvania's Keystone Scholars program (launched in 2019), seed 529 savings accounts with an initial deposit, typically ranging from $50 to $100, for every baby born to or adopted by in-state families. Illinois and California plan to launch similar programs soon. Combined, these three states' initiatives will expand the availability of these accounts to families within three of the 10 largest states in the United States.

Child savings accounts encourage lower-income households to start making regular contributions early, but they also may limit savers' choices and lock them into subpar in-state 529 savings plans. Whether a 529 plan has an associated child savings account or not doesn't affect its Morningstar Analyst Rating, which focuses on the people, parent, and process that directly support a plan. Plans with child savings accounts, though, may appeal to investors who consider environmental, social, and governance factors in their decisions since the programs attempt to help solve a social issue.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

/d10o6nnig0wrdw.cloudfront.net/07-25-2024/t_56eea4e8bb7d4b4fab9986001d5da1b6_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/BU6RVFENPMQF4EOJ6ONIPW5W5Q.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/eda620e2-f7a7-4aef-bb6c-3fb7f1ac7a38.jpg)