After Earnings, Is Coinbase Stock a Buy, a Sell, or Fairly Valued?

Amid a renewed cryptocurrency boom and a big rally in the stock, here’s what we think of Coinbase.

Coinbase COIN released its fourth-quarter earnings report on Feb. 15. With the stock’s price up more than 230% over the past year, here’s Morningstar’s take on Coinbase’s earnings and outlook.

Key Morningstar Metrics for Coinbase

- Fair Value Estimate: $110.00

- Morningstar Rating: 2 stars

- Morningstar Economic Moat Rating: None

- Morningstar Uncertainty Rating: Very High

What We Thought of Coinbase’s Q4 Earnings

- Coinbase’s results were better than expected. The firm’s trading revenue increased by more than we anticipated, and it continues to benefit from a leaner cost structure following major cuts. Heading into earnings, we were already well aware that the company’s trading volume had benefited from a strong recovery in cryptocurrency prices. However, in the results, we saw that this recovery was disproportionately driven by Coinbase’s retail users becoming more active, rather than its institutional user base. This has positive ramifications for its average fee rate, since retail users pay higher fees, and it speaks positively for the health of the firm’s platform and the durability of retail interest in cryptocurrency.

- A core component of the bull thesis for Coinbase is that it is the preferred home for US cryptocurrency users who want a safe place to trade that allows them to charge premium pricing. The firm’s results support the idea that while interest in cryptocurrency is well below its peak, there is still a client base that can be reactivated by strong market conditions. Additionally, there is still no sign that Coinbase’s pricing is under any pressure.

- Coinbase’s business is inherently volatile, since much of its revenue is either heavily correlated with or directly tied to cryptocurrency prices. This does create the potential for significant revenue and earnings growth if cryptocurrency markets continue to rally. However, at its current market price, the stock’s risk/reward dynamic is far too lopsided. The shares are well above our fair value estimate, trading at more than 15 times 2023 revenue. At this point, the market is pricing in a much longer cryptocurrency rally than what we think is reasonable.

Coinbase Stock Price

Fair Value Estimate for Coinbase

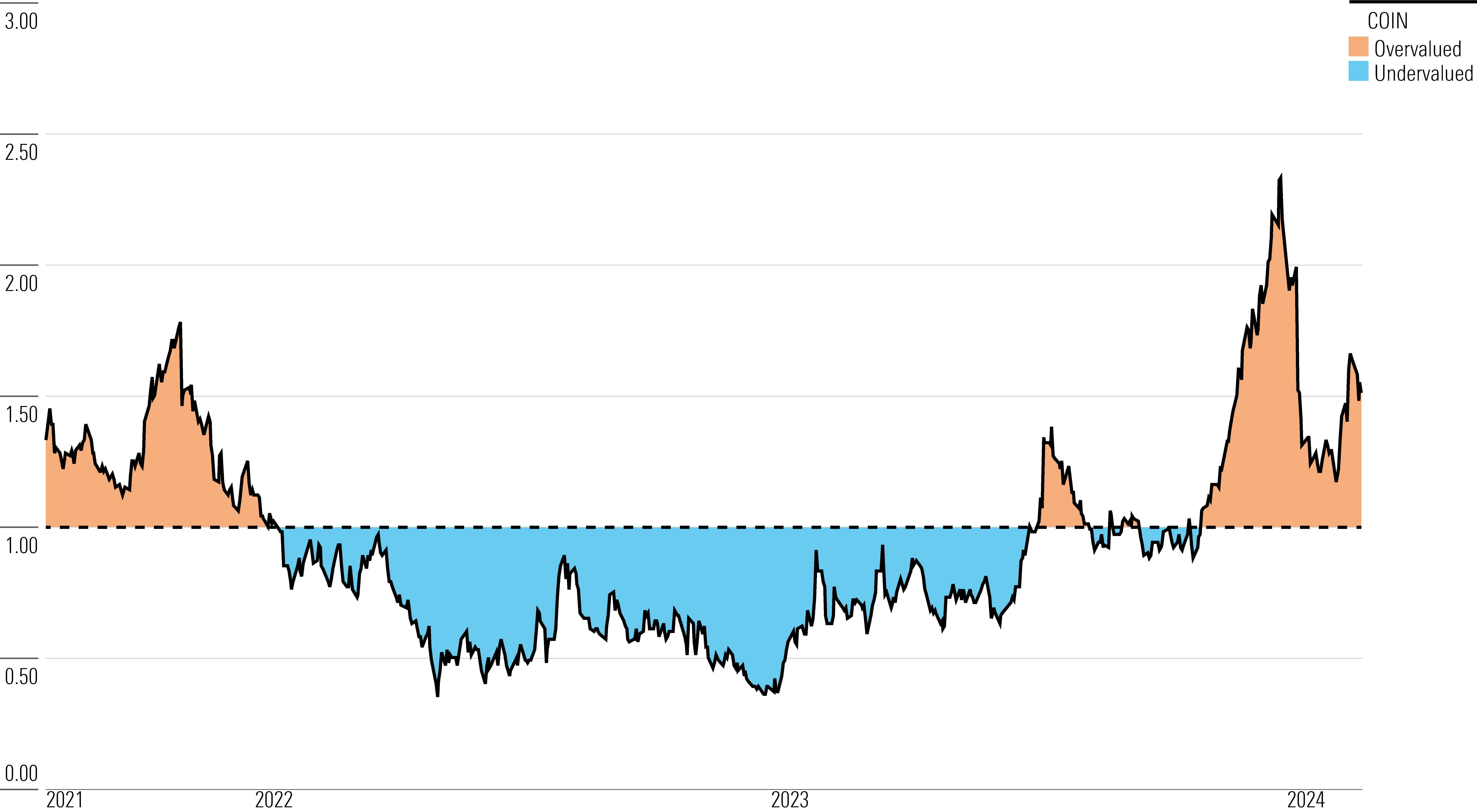

With its 2-star rating, we believe Coinbase’s stock is overvalued compared with our long-term fair value estimate of $110. That estimate depends heavily on assumptions for trading volume—how the company’s trading fees compress over time—as well as interest income projections from its partnership with Circle for the stablecoin USDC.

Coinbase’s largest source of revenue is trading fees, which are assessed as a percentage of the amount being traded on its platform. This ties its long-term revenue growth to the size of the overall cryptocurrency asset class as well as its market share. This is still a speculative asset class; the number of available cryptocurrencies to trade, the space’s eventual market capitalizations, and even its continued existence are still major unknowns.

A sharp decline in prices and retail interest in cryptocurrency in 2022 led to a dramatic decrease in Coinbase’s revenue and pushed it into unprofitability. That said, the firm drastically reduced its operating expenses in 2023, limiting its losses. More recently, news and speculation around Bitcoin spot ETFs have led to a sharp recovery in cryptocurrency prices and higher trading volume on Coinbase’s platform. Our current projections now see the company regaining profitability in 2024, though the longevity of such a resurgence will depend on market conditions.

Read more about Coinbase’s fair value estimate.

Coinbase Historical Price/Fair Value Ratio

Economic Moat Rating

In our view, Coinbase does not have an economic moat despite being the leading cryptocurrency exchange in the United States. It has carved out a strong place in the cryptocurrency exchange industry by intentionally positioning itself as a reliable and compliant platform with which to buy and sell in an industry filled with risk, weak security practices, and spotty regulatory enforcement. This has let the company charge higher fees than many peers while building a large pool of liquidity on its platform.

Coinbase’s reputational advantages have only grown in recent years following the collapse of one of its largest rivals, FTX, due to financial fraud. While we expect fee compression in the long term, recent events will likely allow Coinbase to continue to charge a premium in the immediate future. However, the firm relies on the growth and success of Bitcoin, ethereum, and other cryptocurrencies to generate returns on its invested capital. Cryptocurrency is still highly speculative, and its long-term success and viability are by no means guaranteed. Speculation on future price appreciation remains a key part of the space’s appeal, particularly in the lesser-known “altcoins.”

Coinbase has built a strong competitive position, but without more confidence in the long-term viability of cryptocurrency as an asset class, there is too much potential that the company’s returns on invested capital could rapidly evaporate for us to award it a moat.

Read more about Coinbase’s moat rating.

Risk and Uncertainty

We give Coinbase a Very High Uncertainty Rating. The firm gets more than half of its net revenue from trading fees at its exchange business. Fees are charged as a percentage of the underlying assets being traded, creating direct exposure to cryptocurrency prices. This is a highly volatile and deeply cyclical market. In 2022, Coinbase’s revenue fell more than 59% from the prior year as cryptocurrency prices collapsed. The number of active traders on its platform can vary sharply based on market performance.

On an even broader scale, should cryptocurrency prove to not be durable as an asset class, it is unlikely that Coinbase’s business would be able to retain much (if any) value. The company also has exposure to interest rates through its participation in USDC, which generates significant interest income.

There is also a material amount of environmental, social, and governance risk in Coinbase’s business. It operates with a broad scope, acting as an asset custodian, broker, and exchange in the cryptocurrency economy. This creates significant potential for conflicts of interest, which could lead to reputational damage or regulatory action. There are also legal and regulatory gray areas in Coinbase’s business. It is possible that some of the assets that trade on its platform could be ruled as unregistered securities, forcing the firm to delist them.

Read more about Coinbase’s risk and uncertainty.

COIN Bulls Say

- Coinbase has established itself as the leading US cryptocurrency exchange, with a strong reputation for security in an industry filled with risk for traders.

- Cryptocurrency prices increased sharply at the end of 2023, leading to much higher trading volume and revenue for Coinbase.

- There is a worldwide market for cryptocurrency. Regulatory approval from international regulators will let Coinbase expand its operations and increase its global footprint.

COIN Bears Say

- Cryptocurrency markets have historically been deeply cyclical, with long periods of low prices and depressed trading volume. This adds considerable volatility to Coinbase’s revenue flow.

- The regulatory landscape and long-term viability for cryptocurrency remain unclear, with regulators becoming more aggressive in the aftermath of the high-profile fraud and failure of FTX.

- The SEC has accused Coinbase of acting as an unregistered securities exchange, creating major regulatory and legal uncertainty.

This article was compiled by Frank Lee.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/d10o6nnig0wrdw.cloudfront.net/05-02-2024/t_7b0d5ad1cbc64c2db440c298c6bcccd7_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/5GAX4GUZGFDARNXQRA7HR2YET4.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/U746MWXQHFFZPLSMTEJSUD7HLY.png)