2 Sectors With The Largest Fair Value Increases

Here are the energy stocks and basic materials companies that saw the largest fair value increases during earnings season.

The number of companies in the U.S. market that saw a boost in their fair value estimates slowed, with basic materials and energy stocks taking up the lion’s share of valuation upgrades during 2022’s first-quarter earnings season.

The average fair value estimate among the 850 stocks covered by Morningstar for two or more quarters was essentially unchanged, rising 0.1%. That is a drop from the 2.7% average increase seen during fourth-quarter earnings. The fair value estimate for 503 stocks was unchanged after March 31, when the quarter ended, up from the 399 in the previous period.

Only 200 stocks had a fair value increase, down from the 325 average seen per quarter for the prior year. Among those with the largest fair value increases were basic materials and energy stocks. Both benefited from Morningstar analysts’ updated commodity price forecasts for chemicals, metals, and oil. A list of the stocks with the largest fair value increases can be found at the end of this article.

Morningstar analysts conduct a fundamental review and create models to determine an estimate of the fair value of a company's shares. While Morningstar analysts stick to a long-term approach to investing, they monitor quarterly earnings results to update their assumptions, and potentially their estimates.

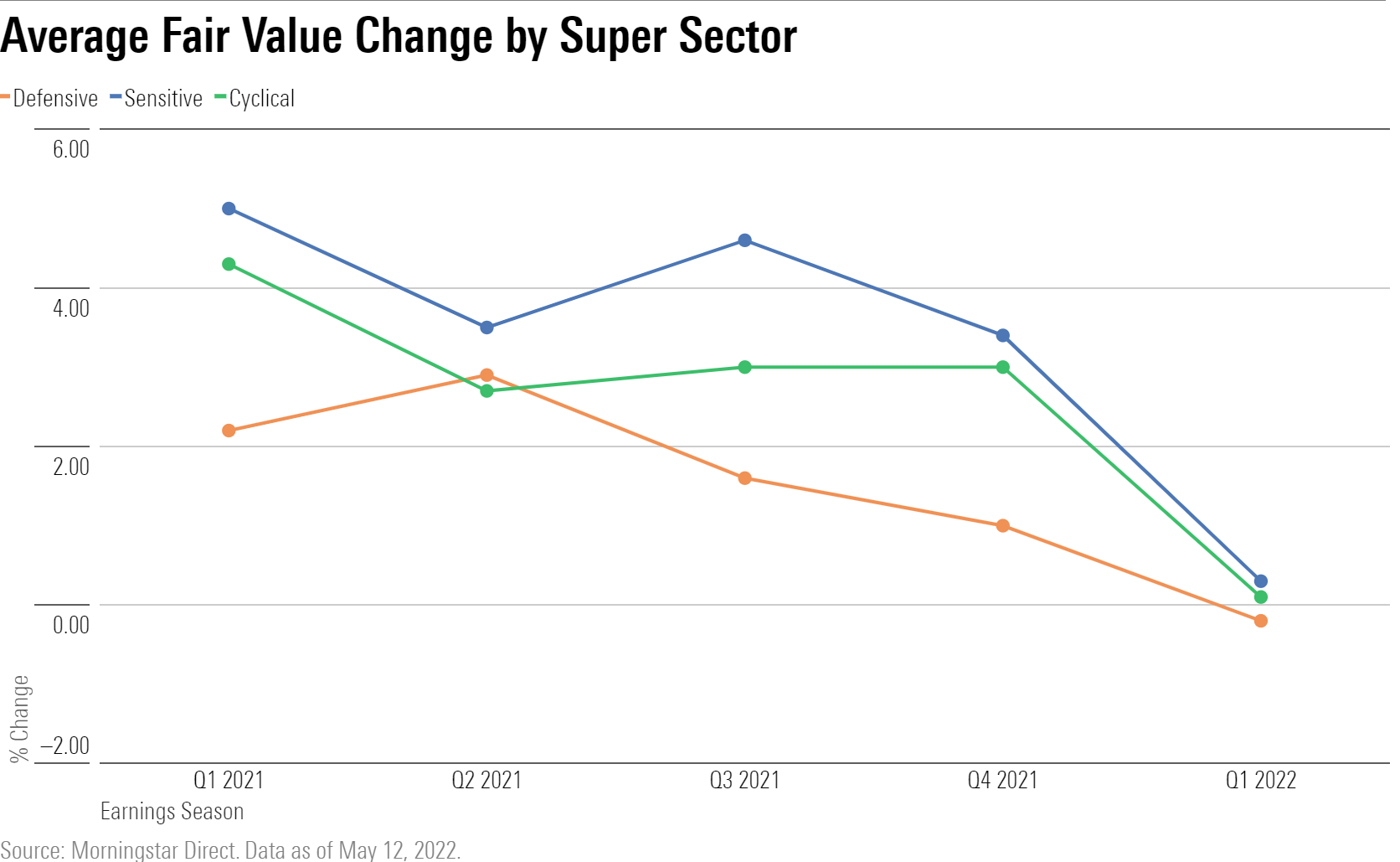

The chart below shows the average percentage change in fair value estimates following and during earnings for the past five quarters. Fair value estimates were pulled from Morningstar Direct for the end dates of each quarter and compared against the estimates six weeks after each quarter ended.

We’ve sorted data by what Morningstar calls Super Sectors, companies that fall into the categories of cyclical, defensive, and sensitive.

Cyclical sectors are those that are heavily correlated with the business cycle. As the economy grows and expands, cyclical sectors follow.

The defensive sector includes industries that are relatively immune to economic cycles.

Sensitive sector industries ebb and flow with the overall economy, albeit with less volatility and fall between defensive and cyclicals.

The rate of fair value estimate changes was essentially flat for each Super Sector. Sensitive stocks had a slight lead in fair value increases, with an average rise of 0.3%, followed by cyclical stocks at 0.1%, while defensive stocks had an average decrease in their valuations by 0.2%.

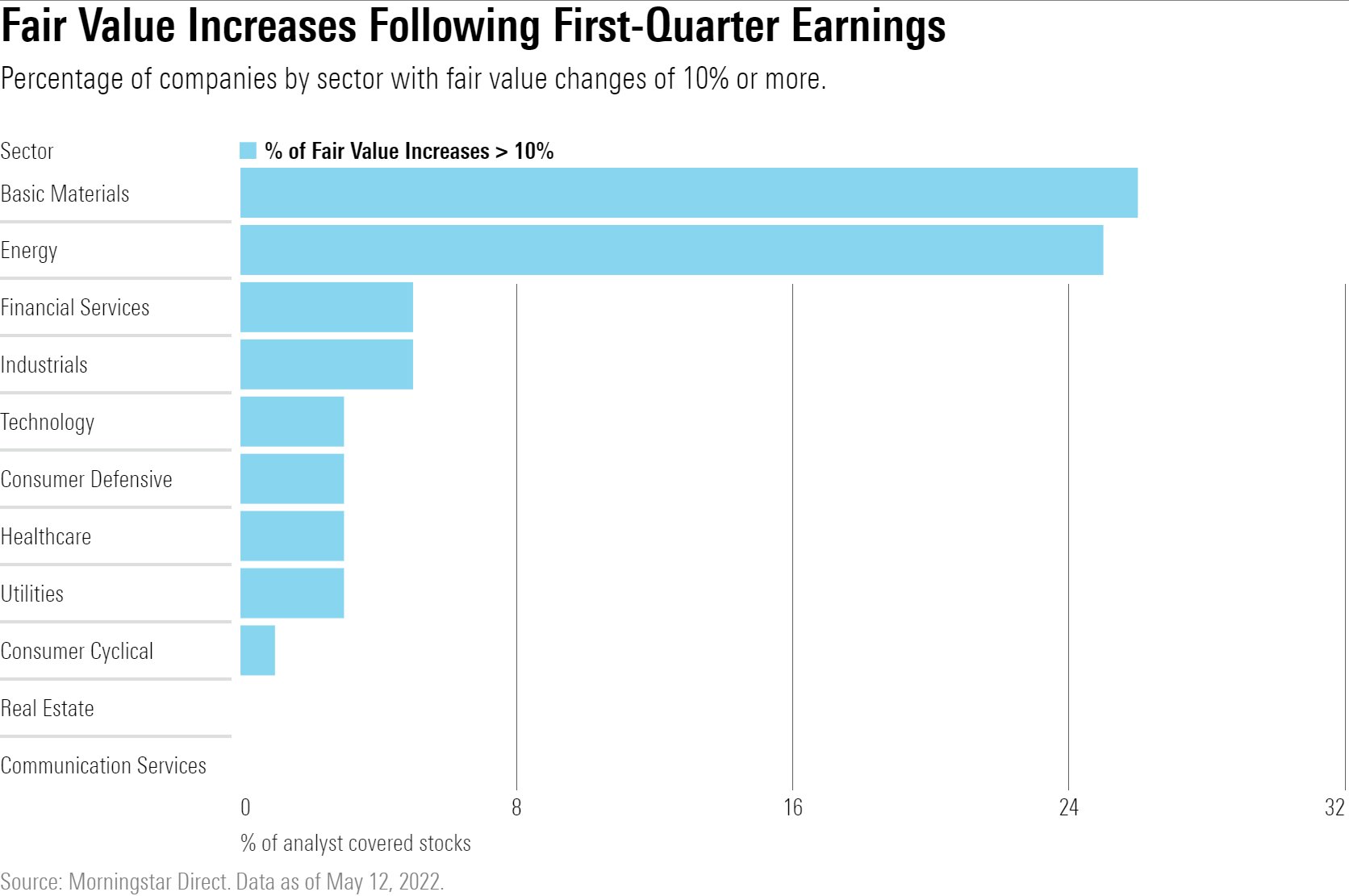

To highlight the most important fair values increases, we screened for those companies that rose 10% or more. Of those, earnings season increases were found to be concentrated in basic materials and energy stocks. Eight, or 26%, of the 27 basic materials stocks under coverage had notable fair value increases of 10% or more. Meanwhile, 14, or 25%, of the 53 energy companies also increased by that same amount.

Basic Materials

Surging commodity prices have lifted the valuations of basic materials stocks by an average of 6%. Russia’s invasion of Ukraine exacerbated supply issues for various metals and agricultural inputs, prompting Morningstar analysts to increase their forecasts.

Leading basic materials in fair value increases was Livent LTHM, a low-cost lithium producer. Morningstar senior equity analyst Seth Goldstein increased his valuation of the company to $35 per share from $25. Demand for lithium is growing in the high double digits as electric vehicle adoption continues. Also benefiting was Albemarle ALB, the world’s largest lithium producer, whose fair value increased to $270 from $225. Both Livent and Albemarle stocks are considered fairly valued based on their recent prices, Goldstein says.

Higher price forecasts for palladium, copper, and iron ore also lifted fair value estimates for mining companies. Anglo American NGLOY rose to $21.40 from $17.30, and Rio Tinto RIO, to $76 from $66. Following their fair value increases, both stocks are considered fairly valued.

Fertilizer producer CF Industries’ CF fair value rose to $75 from $65 after Goldstein boosted his long-term forecasts to $320 per metric ton from $280. He also anticipates the firm will generate record profit in 2022, with fertilizer prices near all-time highs. While Goldstein boosted his fair value for CF Industries, he thinks the company’s shares are now trading at prices that put it in overvalued territory.

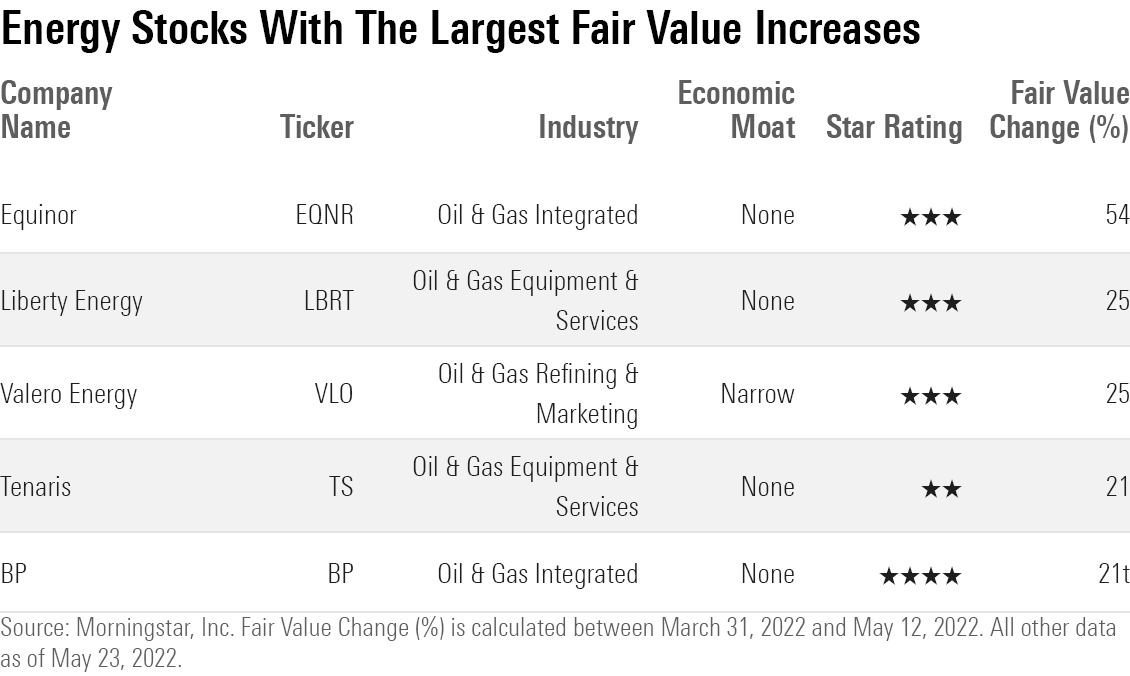

Energy

Fair value estimates for energy stocks increased by an average of 5%, the second-largest increase among Morningstar’s 11 stock sectors. Driving the rise was an updated outlook for oil prices in 2022 and 2023.

Oil and gas firms that operate alongside the extraction, transportation, and refinement parts of production were among those that saw the biggest gains. Topping the energy sector list were Equinor EQNR, whose fair value rose to $40 per share from $26, and BP BP, up to $37.50 from $31. Both companies are now trading in undervalued 4-star territory. Morningstar energy sector strategist Allen Good raised his estimates in part due to an increase in the average price for Brent oil to $101 per barrel in 2022 from $80, and $95 per barrel in 2023 from $80.

Oil refiner Valero Energy's VLO valuation increased following an updated outlook for their refining margins. Good set his long-term outlook for the company's margin on both West Texas Intermediate and Brent oil to $5 per barrel, and boosted their fair value estimate to $101 per share from $93. Valero’s shares are currently trading in fair value territory.

Morningstar equity analyst Katherine Olexa sees room for growth in oilfield-services provider Liberty Energy LBRT after the company posted its first quarterly operating profit in two years. The firm’s vertical integration of OneStim, acquired in 2020, and PropX in 2021, boosted results, Olexa says. She sees operating margins reaching 8% in the long-term and revenue growing about 11% annually in the next five years. Olexa raised Liberty’s fair value to $15 from $12.

Similarly, Olexa also increased the fair value estimate for Tenaris TS, a company that provides tubes crucial for oil transportation, to $23 from $19. High demand for its products has increased the company’s pricing power, and Olexa sees margins averaging 12% per year through 2026, and revenue growing 10% per year in the same period. Shares of Liberty are considered fairly valued, but Tenaris is considered overvalued at current prices.

Data notes: Fair value estimates were sourced from Morningstar Direct for the end dates of each quarter. In some cases, fair value adjustments may have been made before company earnings reports. Stocks without a fair value estimate at the beginning and/or end of the six-week period were excluded from data aggregation to account for any changes in our equity coverage list.

The underlying list of stocks can change from quarter to quarter owing to changes in analyst coverage or other factors. Stocks portrayed in sector tables may not reflect those that had the largest fair value moves within the sector. Demonstrated stocks were selected to emphasize sectorwide trends and/or at the recommendation of Morningstar analysts.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/WC6XJYN7KNGWJIOWVJWDVLDZPY.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HHSXAQ5U2RBI5FNOQTRU44ENHM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/737HCNGRFLOAN3I7RKGB7VPEKQ.png)