Markets Brief: What to Watch for in Q1 Earnings, CPI

Fed minutes trigger a tech selloff, Nvidia shares slide. Defensive sectors rally.

It’s earnings season.

The coming week will bring an initial sprinkling of first-quarter corporate earnings, including financial industry heavyweights JPMorgan Chase JPM and BlackRock BLK.

What should investors watch for as first-quarter results roll in over the next several weeks?

David Sekera, Morningstar’s chief U.S. market strategist, highlights three themes to keep an eye on: inflation, supply chains, and overall updated profit outlooks for 2022.

When it comes to inflation, Sekera says to watch for the impact of higher prices on margins. Have companies been able to pass along rising costs to their customers? Or are margins being pressured? Likewise, Sekera says, updates on supply chain constraints will provide insights into whether shortages are starting to improve and from there, help alleviate upward pricing pressures.

“I want to hear if supply chain disruptions and bottlenecks are dissipating or if they are still causing management headaches,” Sekera says.

Investors should also look for signs that the global economic ripples from Russia’s attack on Ukraine are leading to less certainty about the profit outlook.

“Between heightened geopolitical risks, a slowing economy, inflation, and supply chain issues are management teams still confident of their original outlook? Or is there a wider dispersion of uncertainty than at the beginning of the year,” Sekera says.

The coming week will also bring in fresh information on just how tough a battle the Federal Reserve has with inflation as Wednesday brings updated March numbers for the consumer price index. The CPI, which rose 0.8% in February from January, and 7.9% for the prior 12 months, is at a 40-year high. March data could show some good news in an easing of month-to-month increases in inflation, but a fresh high in the year-over-year reading. Economists expect the CPI to rise 0.5% in March from the prior month, and 8.3% for the year, according to FactSet.

Long gone are the days since inflation was seen as transitory by the Fed, as it opts to more aggressively fight inflation with greater rate hikes. The minutes from the March meeting, where the Fed raised the federal-funds rate by a quarter of a percent, also showed Fed officials seriously considered raising rates by half a percentage point. At this point, the odds seem in favor of a half-point increase when the Fed's policymaking committee next convenes in May, according to futures trading activity tracked by CME Group's FedWatch tool.

Minutes from their meeting in March also revealed potential plans to start reducing the Fed's balance sheet by $95 billion each month--a more aggressive pace from the $50 billion in 2017. The balance sheet reduction--known as quantitative tightening--will erase demand for U.S. Treasuries that kept yields low during the coronavirus recession.

While the news out of the Fed painted a picture of the central bank taking a more aggressive stance than they had previously signaled, there was only limited impact on the stock market. The Morningstar US Market Index fell 1.73%. However, in the bond market, yields rose across the board.

One notable aspect of the bond market's response to the Fed: the yield curve reversed the inversion seen at the end of the previous week as yields on the U.S. Treasury 10-year note rose above that of the 2-year note. When the yield curve is inverted--that is, when short-term yields are above long-term yields--it's often seen as a warning sign about a recession.

Among the events scheduled for next week:

- Tuesday: March consumer price index

- Wednesday: March producer price index; earnings from J.P. Morgan Chase, BlackRock

- Thursday: March retail sales; earnings from UnitedHealth Group UNH

- Friday: Good Friday, markets are closed

For the trading week ending April 8:

- The Morningstar US Market Index was down 1.73%.

- The best-performing sectors were energy, up 2.84%, healthcare, 2.75%, and consumer defensive, 2.66%.

- The worst-performing sectors were technology, down 4.68%, and consumer cyclical, 3.54%.

- Yields on the U.S. 10-year Treasury note rose to 2.71% from 2.38%.

- Oil ended the week down 1.02% to $98.26 per barrel.

- Of the 864 U.S.-listed companies covered by Morningstar, 322, or 37%, rose, while 542, or 63%, fell.

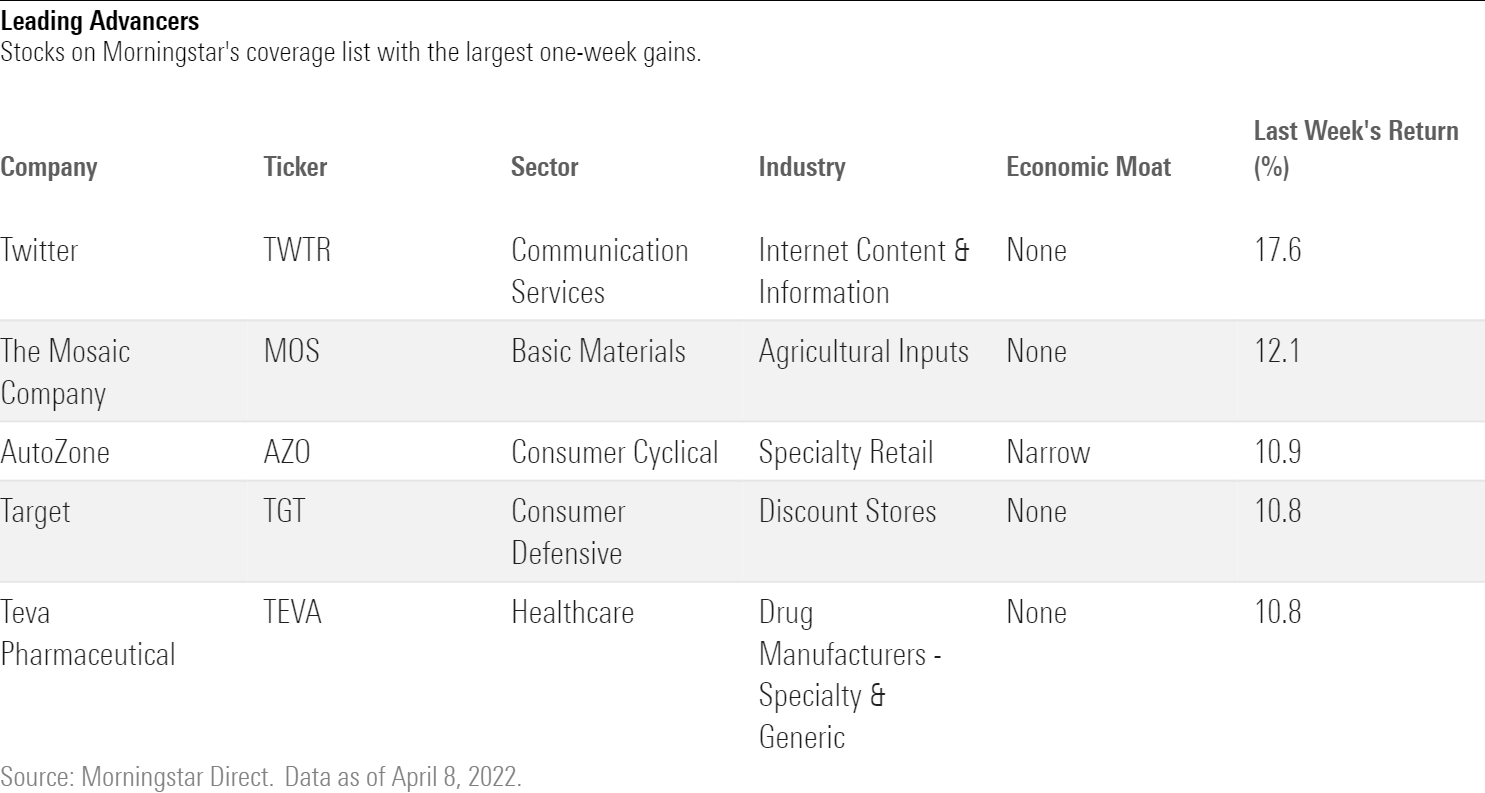

What Stocks Are Up?

The best-performing stocks in the past week were Twitter TWTR, The Mosiac Company MOS, AutoZone AZO, Target TGT, and Teva Pharmaceutical TEVA.

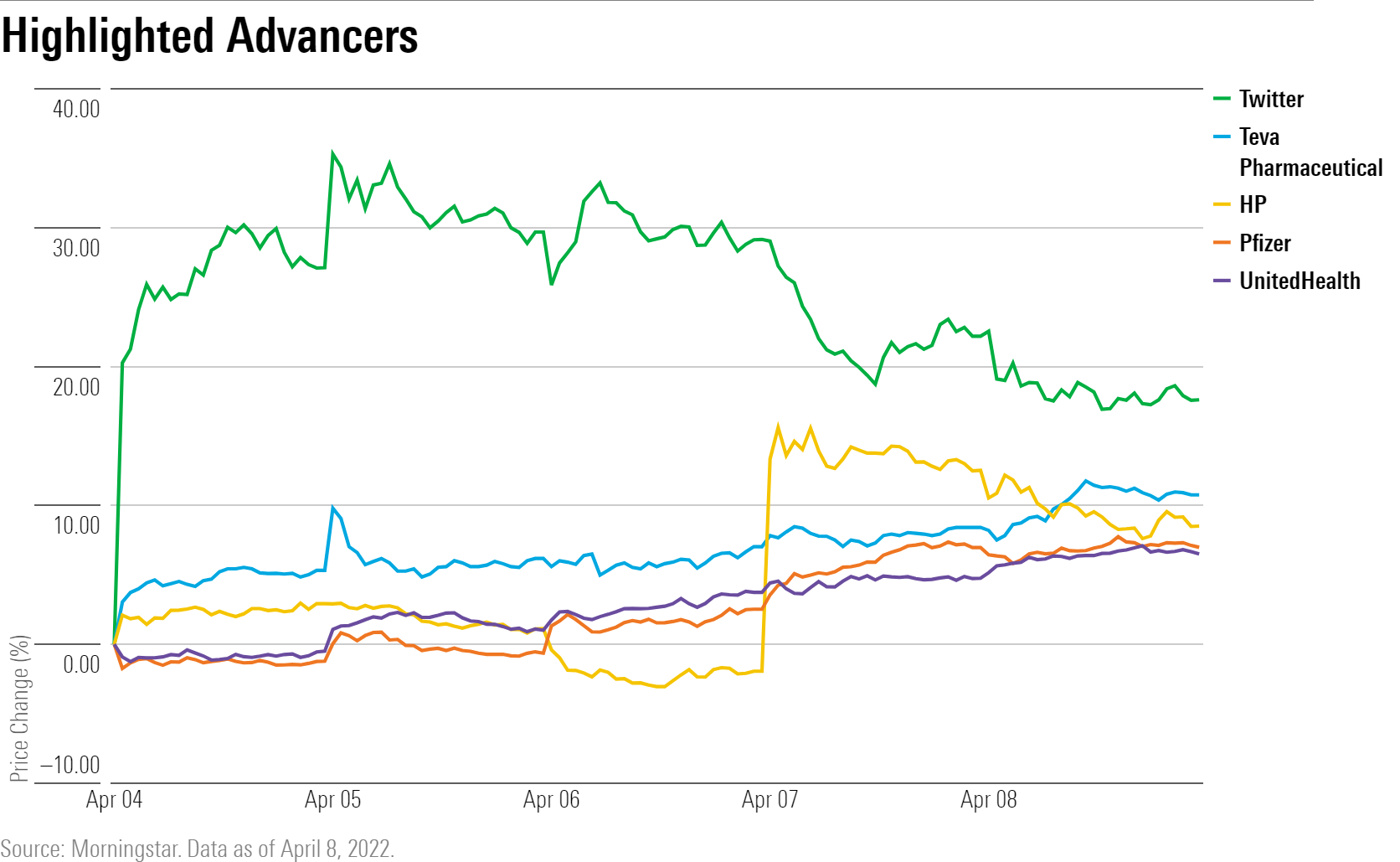

Twitter shares rose after Tesla's chief executive Elon Musk revealed a 9.2% stake, and was invited to join the social-0media company's board. Likewise, HP Inc HPQ rallied after Berkshire Hathaway BRK.B disclosed an 11% stake in the company. Healthcare dominated the best-performing stocks list in the past few days as investors rotate into defensive sectors. Drug companies Teva, Sanofi SNY, and Pfizer PFE closed higher. UnitedHealth Group rose ahead of its earnings release scheduled for Thursday. Pfizer shares rose after the company said it would acquire privately held ReViral.

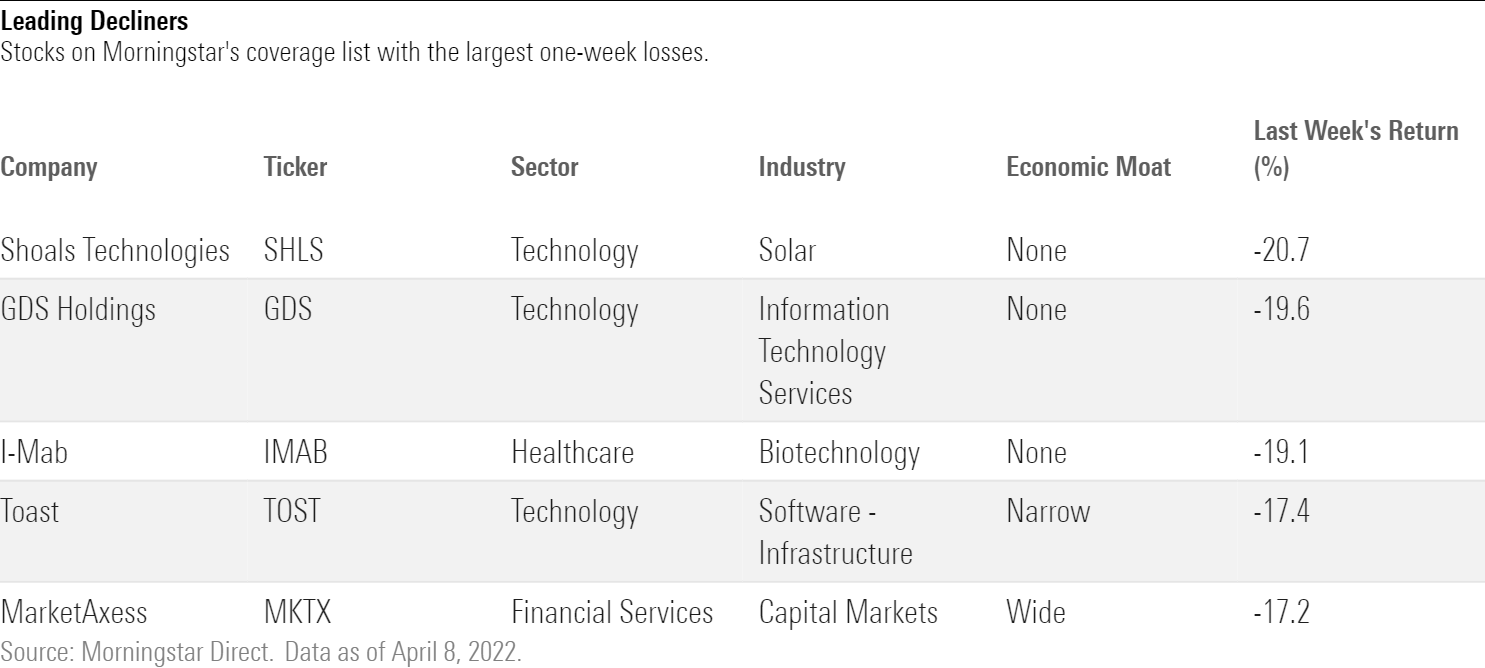

What Stocks Are Down?

The worst-performing stocks in the past week were Shoals Technologies SHLS, GDS Holdings GDS, I-Mab IMAB, Toast TOST, and MarketAxess MKTX.

Shares of Shoals Technologies fell after the company said that chief financial officer Philip Garton stepped down. Kevin Hubbard will take over on an interim basis for the solar energy solutions provider.

SoFi Technologies SOFI saw it shares fall after the Biden administration extended a moratorium on federal student loan repayments.

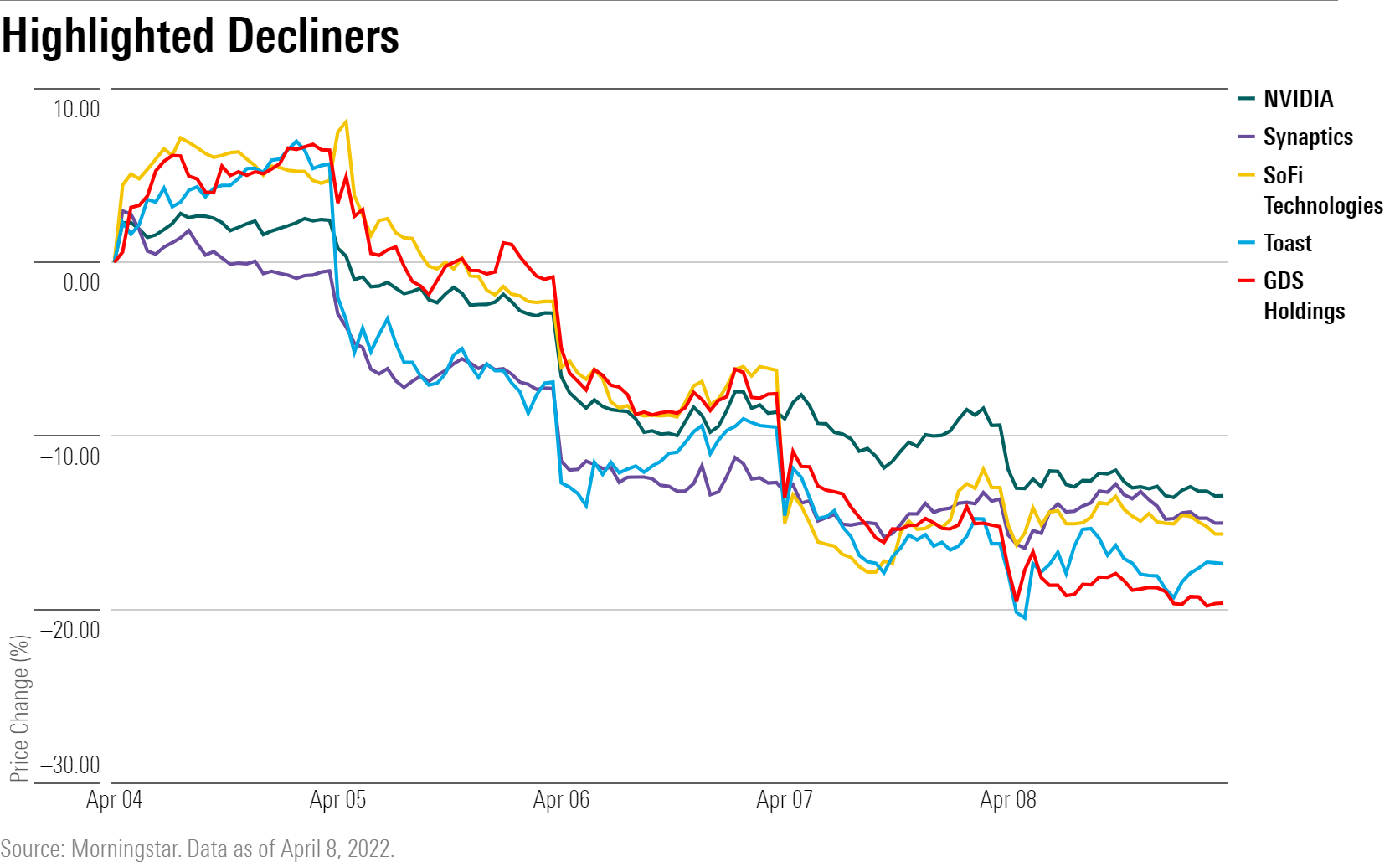

Investors sold off growth stocks following the release of minutes from the Fed showcasing a more aggressive plan to fight inflation. Among those worst hit were names in the technology sector, including GDS Holdings and Toast.

Also caught up in the selloff were shares in semiconductor companies such as Nvidia NVDA, Synaptics SYNA, and ONsemi ON.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/54RIEB5NTVG73FNGCTH6TGQMWU.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZYJVMA34ANHZZDT5KOPPUVFLPE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/MNPB4CP64NCNLA3MTELE3ISLRY.jpg)