Lessons Learned From Surviving Thematic Funds

Long-term success remains rare among this group.

/s3.amazonaws.com/arc-authors/morningstar/c00554e5-8c4c-4ca5-afc8-d2630eab0b0a.jpg)

It is difficult to survive in the land of thematic funds. During the 15 years through Dec. 31, 2021, more than 80% of thematic funds worldwide closed their doors. Most thematic funds prove to be one-hit wonders or don't live long enough to see their investment theses pan out. Timing is a crucial element for thematic funds, and merely staying open long enough to have their time in the limelight can be critical to their long-run viability.

Here, I take a close look at the survivors of the thematic fund universe. These journeymen among thematic funds can share lessons on what it takes to make it and highlight just how rare long-term success is among thematic funds.

Which Funds Are the Thematic Survivors?

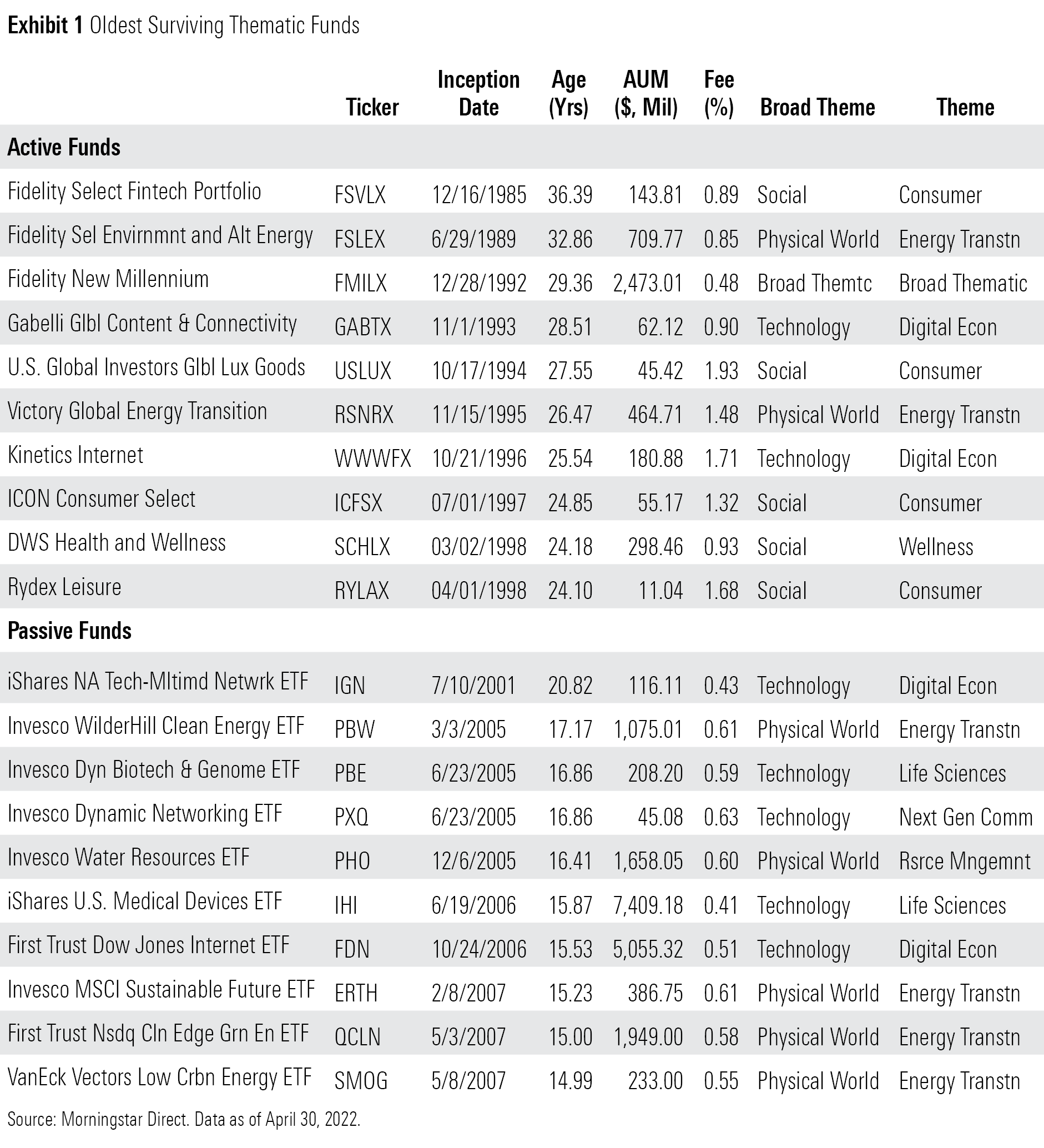

Exhibit 1 contains a snapshot of the oldest surviving thematic funds. These funds' themes are emblematic of the time they made their debut. Most of the active funds on this list came to market in the 1990s and focused on the internet and consumer spending trends. Five of the passive funds in this list came to market in the 2000s and focused on sustainable investment themes. Through the years, these themes haven't been consistently popular with investors, but the funds have nonetheless persisted.

Survivors Are Not Superstars

While surviving for more than 15 years is no small feat, not all of our 20 survivors have become stars. Only one active and five of the passive survivors had more than $1 billion in assets under management as of April 30, 2022. Two out of these five passive funds—First Trust Nasdaq Clean Edge Green Energy ETF QCLN and Invesco WilderHill Clean Energy ETF PBW—only recently joined this $1 billion AUM club, thanks to the 2020 boom in clean energy investing.

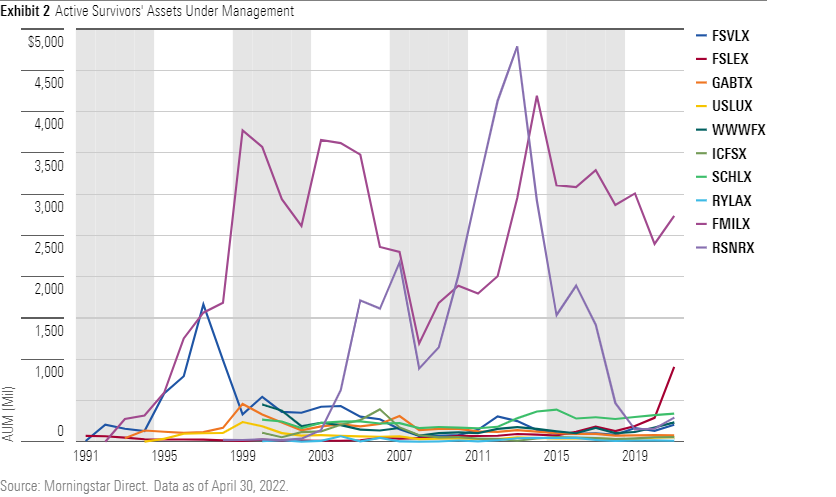

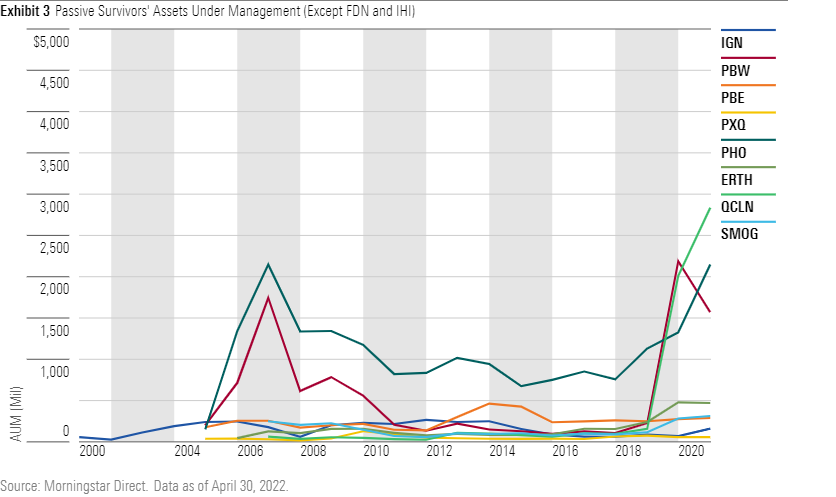

Exhibits 2 and 3 plot the year-end assets under management for the active and passive survivors, except for First Trust Dow Jones Internet Index ETF FDN and iShares U.S. Medical Devices ETF IHI as their asset growth was quite literally off the charts.

Both FDN and IHI have steadily gathered assets throughout their existence, particularly during the past five years. Each ended 2021 with nearly $10 billion in assets. However, these funds were outliers that do not sing the same tune as the other passive survivors,most of which barely ever breached the $500 million AUM threshold.

The trend is similar on the active side, as the majority of the funds experienced tepid asset growth with the exception of a few outliers. Fidelity New Millennium FMILX and Victory Global Energy Transition RSNRX were the only two active offerings with more than $1 billion in assets for more than half of their life, though Victory Global Energy Transition's asset base is much smaller now. Fidelity Select Environmental and Alternative Energy's assets under management reached nearly $1 billion in 2021, as its asset base more than tripled. However, the fund has spent most of its nearly 33-year existence with less than $100 million in shareholders' money.

Many of these funds gathered the bulk of their assets at launch when their theme was center stage. But investor interest subsequently subsided, and they quietly plodded along for most of their existence. The postcoronavirus boom in thematic funds boosted assets for some of these funds, but none are household names.

Muddy Track Record

How well have these funds served investors? In short: Not well. Throughout their existence, most of the thematic survivors underperformed the broader U.S. market as proxied by the Morningstar US Market Index. Only three active and three passive funds managed to outperform the Morningstar US Market Index from their respective inceptions through April 2022.

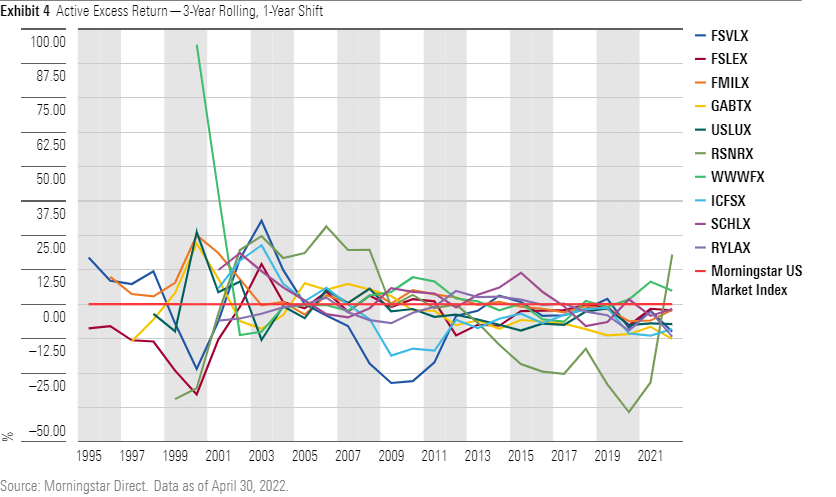

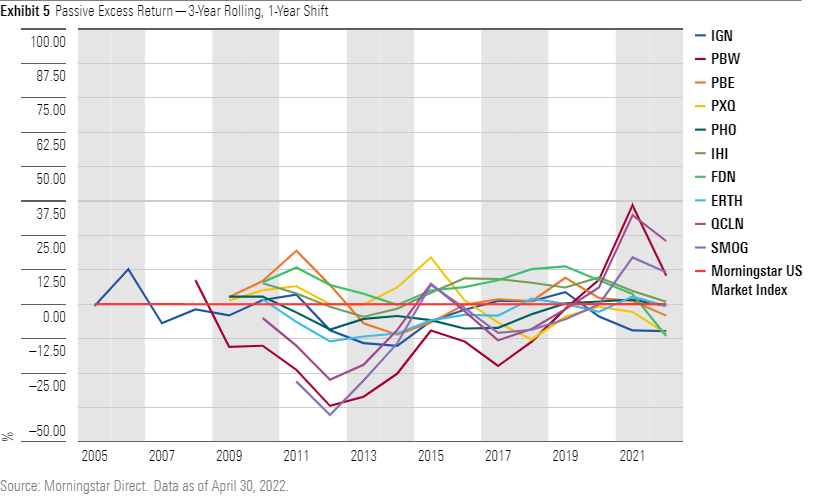

Exhibits 4 and 5 plot the excess returns of these funds against the broad US market over a three-year rolling window.

Many of the active funds started out strong, but all of them lost steam by the 2010s. Most notably, Kinetics Internet WWWFX outperformed the Morningstar US Market Index by nearly 100% annualized during the three-year period from May 1997 through April 2000. However, it quickly fell back to earth. Similarly, many of the other active survivors peaked in the early 2000s, accompanied by a high volatility of returns relative to the broader market. In the 2010s, volatility tempered and most of the funds settled into a consistent pattern of underperforming the market.

The passive survivors' returns were even more volatile. While more funds managed to have stretches of outperformance, the passive cohort also suffered larger drawdowns. In particular, three of the clean energy funds suffered large losses in the early 2010s before spiking again after the coronavirus-related selloff in early 2020. This points to the opportunistic manner in which many thematic funds have been used by investors.

Investors in thematic funds need to be prepared for an added dose of volatility and long performance droughts. Even the most durable themes go in and out of style.

Old, but Not Gold

Thus far, most of these long-surviving thematic funds have failed. If anything, their longevity seems to speak more to their backers' willingness to keep them open than it is a testament to their track record. Most of the active funds' managers have had a long history with the strategies; some of these managers have been around since nearly the beginning. On the other hand, most of the passive funds have maintained the same index since their inception with minimal changes to their methodologies.

Regardless of why they are still open, these funds' performances evoke caution, not confidence. If even the oldest surviving thematic funds can't capture investors' imaginations and assets or beat the market, the odds of success for newer, less-proven thematic funds are probably quite low.

Investors in thematic funds are making a trifecta bet: The theme must play out as expected, the companies in the portfolio must benefit significantly from the trend, and the investor must buy in at the right price. The odds of winning this bet are low, but the payout can be high.

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click here for a list of investable products that track or have tracked a Morningstar index. Morningstar, Inc. does not market, sell, or make any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/FGC25JIKZ5EATCXF265D56SZTE.jpg)

/d10o6nnig0wrdw.cloudfront.net/04-25-2024/t_d30270f760794625a1e74b94c0d352af_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/DOXM5RLEKJHX5B6OIEWSUMX6X4.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/c00554e5-8c4c-4ca5-afc8-d2630eab0b0a.jpg)