Options Income Like JEPI Isn’t for Everyone

What to know if you are considering this ETF trend.

/s3.amazonaws.com/arc-authors/morningstar/c00554e5-8c4c-4ca5-afc8-d2630eab0b0a.jpg)

The derivative income Morningstar Category netted over $25 billion in inflows in 2023, growing its asset base by half. Much of this investment went to JPMorgan Equity Premium Income ETF JEPI, which pulled in nearly $13 billion throughout the year. Still, money diligently poured into other options-income products launched by a wide range of asset managers.

Options income isn’t a novel concept, but it isn’t for everyone. The asymmetrical risk/reward profiles of these strategies make them susceptible to large market movements, and over the long run, many of these funds have underperformed the broader market. Investors have shown a newfound appetite for elevated yields over the past few years, but yield shouldn’t be the yardstick by which one measures these strategies. This article will break down the source of returns for these funds to give a clearer picture of their benefits and drawbacks for investors.

High Yield, Low Risk?

Consider the exchange-traded funds selling calls or puts on the S&P 500, passing through the sales proceeds (options premiums) to investors as “income”:

- Options can provide insurance for buyers against future volatility or leverage to benefit from it, so sellers demand a premium to compensate for this risk. This premium, the price of the options, correlates to the S&P 500′s implied volatility at the time of sale.

- Most of the current options-income ETFs use covered calls, but some offer cash-secured puts. These funds hold the underlying index portfolio (for covered calls) or enough cash to purchase the index at the established strike price (for cash-secured puts).

- The payoff received from selling options is received at the onset and solidifies a component of the fund’s return regardless of what happens at the options’ expiration.

- Covered calls: The equity portfolio mimics the S&P 500 up to the call’s strike price, at which point it is expected to be called away. The risk of loss is 100% minus the call premium. Potential upside is capped at the strike price plus the call premium.

- Cash-secured puts: Put sellers lose money when the S&P 500 drops past the put’s strike price. The risk of loss is substantial to the downside, but the upside is capped at the interest rate earned on cash plus the put premium.

The payoff profiles for these strategies are highly asymmetrical. The options premiums help cushion declines, but they remain exposed to index losses. Meanwhile, their upside is capped. These funds’ market beta and standard deviation of returns fail to reflect this skewed tail risk. Selling options effectively shorts volatility, making the fund appear less risky than the market despite similar exposure to a significant drop. Likewise, robust yields distract from the opportunity cost of forgone upside exposure.

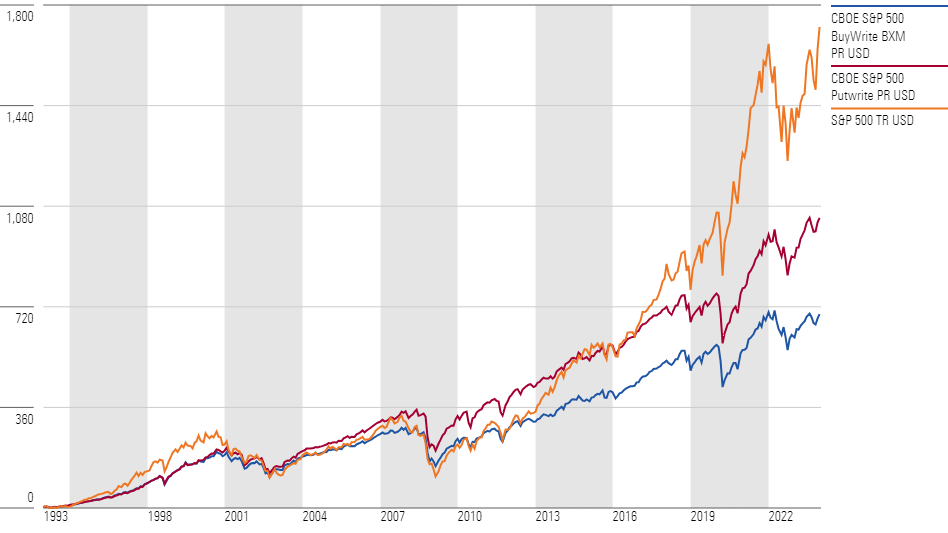

Options-income strategies’ high yield is hardly a free lunch. Many investors have been drawn in by the eye-catching payouts, but yields paint an incomplete picture. The exhibit below compares the 30-year performance of the S&P 500 against the CBOE S&P 500 BuyWrite Index (call selling) and the CBOE S&P 500 PutWrite Index (put selling). The option premiums harvested by these strategies cushioned against downturns, including some of the worst in recent decades, such as the 2008 global financial crisis or the 2000 dot-com bubble. But the slight cushion failed to compensate for the lost upside, causing both options-income indexes to severely underperform the S&P 500 over the full period.

Growth of Options Selling Strategies versus the S&P 500

Risk Premium Over Options Premium

These strategies have their time and place, but yield isn’t the right framework to evaluate them. Options transform risk—the yield is nothing more than cashing in on expected volatility. Instead, options sellers should target the volatility risk premium, which should provide profit beyond a simple risk transfer. This is the observable gap between implied volatility (what the market expects) and realized volatility (what actually happens). Options sellers receive a price based on implied volatility, yet their outcome depends on realized volatility. When realized volatility is lower than implied volatility, the options sellers can harvest a positive volatility risk premium.

Lucky for sellers, the persistence of a volatility risk premium has been widely documented and established in US equity markets. This gap between expectation and reality often stems from market participants overestimating the frequency of “black swan” events and overly hedging against them. Options buyers have a tendency to be risk-averse and therefore are willing to pay a higher premium for puts than calls, all else equal.

Although the volatility risk premium can be observed in any market environment, high implied volatility often produces the sky-high premiums that investors seek. As volatility tends to increase more during downturns than rallies, option-selling strategies have shown the ability to collect high payouts and outperform the market in bad years. Yet chasing performance doesn’t often end well for investors, particularly in this category. Derivative income funds’ outstanding performance in 2022 turned sour in 2023, the year after the category doubled assets.

If You’re Still Interested

For investors with a long-term horizon, these funds are unlikely to outperform the market as a buy-and-hold strategy. Nonetheless, those with sizable short-term needs for cash could consider these strategies to extract cash flow from the portfolio. Consider some best practices:

- Understand the tax consequences. Index-based options are generally taxed at a 60% long-term and 40% short-term tax rate regardless of holding period. This could be advantageous when compared with the tax rate on interest income but lacking when compared with selling holdings that qualify for long-term capital gains. Certain accounting rules might also require an options-income fund to distribute payouts as a return of capital, a tax-free event that reduces your cost basis, setting you up for higher capital gains in the future.

- Adjust your expectations. Understand the payoff profiles of options-income funds in different market conditions and whether you have the risk budget to stick with them.

- Let the yields go. Chasing funds with the highest payouts will lead you astray. Understand how each fund is harvesting the volatility risk premium and evaluate them accordingly.

- Don’t depend on one path. Investors should seek to invest in funds that diversify options-selling across different strike prices and expirations to reduce their reliance on a single outcome.

- Don’t forget the equity sleeve. Many options-income funds take active risks in the equity sleeve to enhance dividends or lower volatility. These can be helpful tweaks, but they also can add risks of their own.

The article appeared in the January 2024 issue of Morningstar ETFInvestor. Click here for a sample issue.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/24UPFK5OBNANLM2B55TIWIK2S4.png)

/d10o6nnig0wrdw.cloudfront.net/04-25-2024/t_29c382728cbc4bf2aaef646d1589a188_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/c00554e5-8c4c-4ca5-afc8-d2630eab0b0a.jpg)