What’s Next for the Relationship Between Stocks and Bonds

Can you still count on your core bond allocation to be a ballast?

/s3.amazonaws.com/arc-authors/morningstar/c00554e5-8c4c-4ca5-afc8-d2630eab0b0a.jpg)

Editor’s Note: The article was published in the September issue of Morningstar ETFInvestor.

Diversification is often considered the only free lunch in investing. And for much of the past two decades, high-quality U.S. bonds were an effective diversifier thanks to their negative correlation with stocks. Yet the first half of 2022 saw stocks and bonds moving in lockstep, with both producing negative absolute returns—a discouraging sign for the typical diversified investor. Is the diversification benefit of bonds no longer holding ground?

The answer, as always, is never straightforward. Myriad factors drive the relationship between stocks and bonds, making it difficult to predict what might happen over the longer term. Thus, examining the drivers of this relationship and understanding bonds’ full impact on a portfolio is a solid first step in knowing what to expect.

Causation Meets Correlation

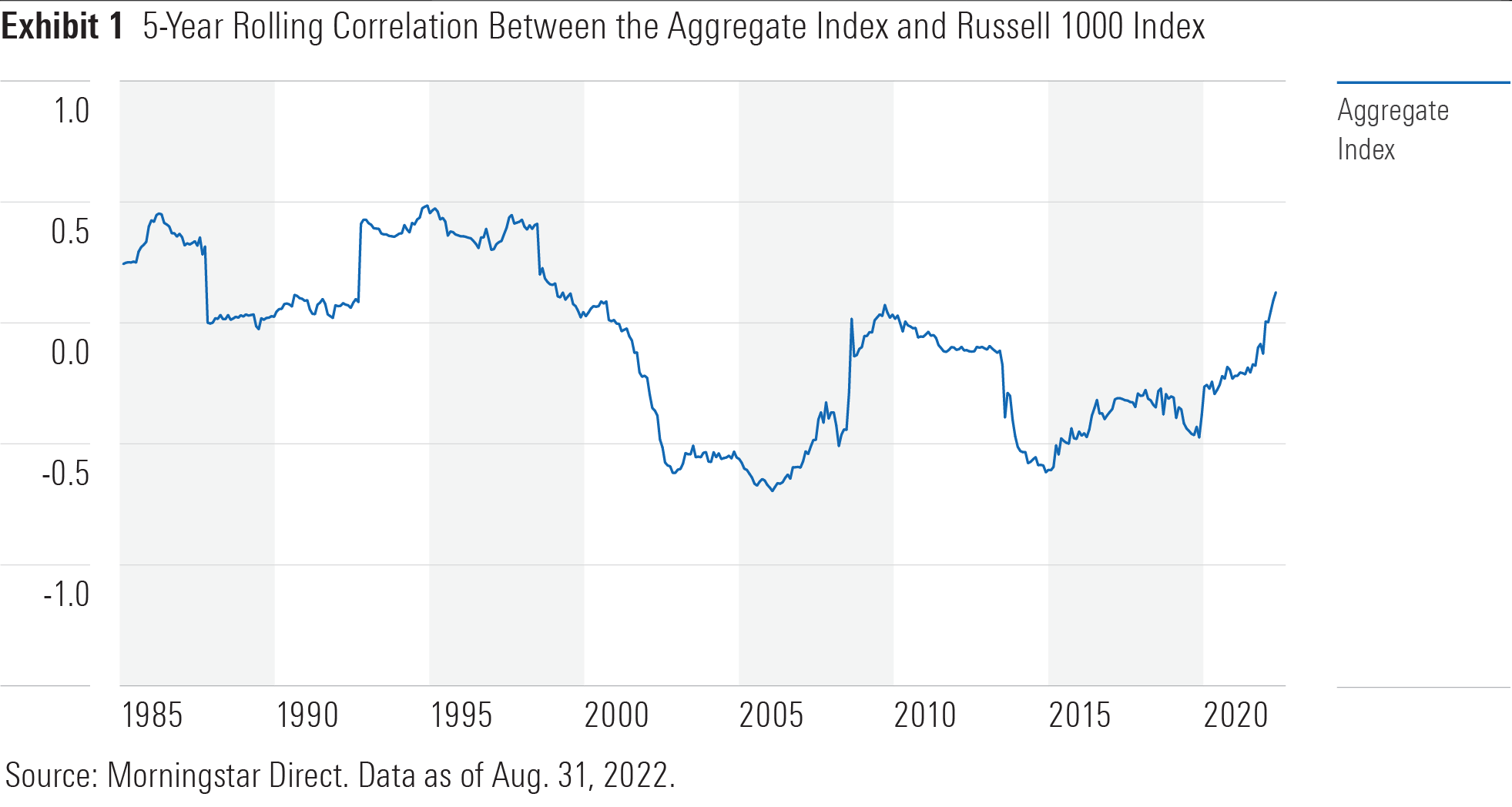

Exhibit 1 displays the historical correlation between the two common components of a 60/40 portfolio: a core bond holding, represented by the Bloomberg U.S. Aggregate Bond Index, and a core large-cap equity holding, proxied with the Russell 1000 Index. While we have experienced long stretches of negative correlation during the past two decades, this has not been the historical norm. This relationship was mostly positive over the two decades prior to the 2000s. What drove this change, and can we expect the negative correlation of the past 20 years to continue?

Stock market volatility and economic growth usually have opposite effects on investors’ interest in stocks and bonds. In theory, volatility in the stock market should drive investors toward bonds as a safe haven. And a strong economy breeds confidence in companies’ earning potential, allowing investors to comfortably move away from safer but lower-yielding bonds into riskier assets like stocks.

On the other hand, major economic factors, such as inflation and interest rates, can have a similar effect on the stock and bond markets. High inflation tends to have a negative impact on fixed-income and equity returns as prices adjust to higher real rates, although the magnitude can be different. The real value of bonds’ return streams is directly reduced by higher inflation, as higher real rates cause their prices to fall. Likewise, companies’ share prices usually decline, despite expectations that cash flows may eventually grow alongside inflation. This stems from various factors, such as inflation’s impact on real earnings growth, increasing equity risk premiums, or investors’ behavioral biases. Higher interest rates, which often come in response to higher inflation, also increase the discount rate of future cash flows, which reduces the prices of both bonds and equities.

Beyond the immediate impact of inflation and interest rates, uncertainty over their future trajectories may also influence the correlation between stocks and bonds. Less certain future economic conditions likely reduce investors’ appetite for risk and could drive them away from both asset classes in favor of more-liquid instruments such as cash. To this end, volatile inflation numbers or inconsistent signaling from the Federal Reserve can contribute to a downturn for both stocks and bonds.

The negative correlation we have seen since the beginning of the millennium is a result of stable and low interest rates combined with stable and low inflation. This wasn’t always the case. The 1960s through the early 1980s witnessed both inflation and interest rates climbing higher. The 1970s experienced stagflation, as inflation ran wild and rates became more difficult to predict. Thus, the positive stock-bond correlation during the first part of 2022 is not without precedent.

The more difficult question to answer, then, is whether bonds will adequately hedge stock risk when the market turns south. It wouldn’t be unreasonable to expect a return to negative correlations between stocks and bonds if inflation is short-lived. However, a bearish outlook on the market’s recovery, such as sustained inflation or persistently high interest rates, would indicate otherwise. As the whirlwind of March 2020 reminded investors, attempting to forecast monetary policy and the market’s future is difficult and often has a wide margin for error.

Beyond Correlation

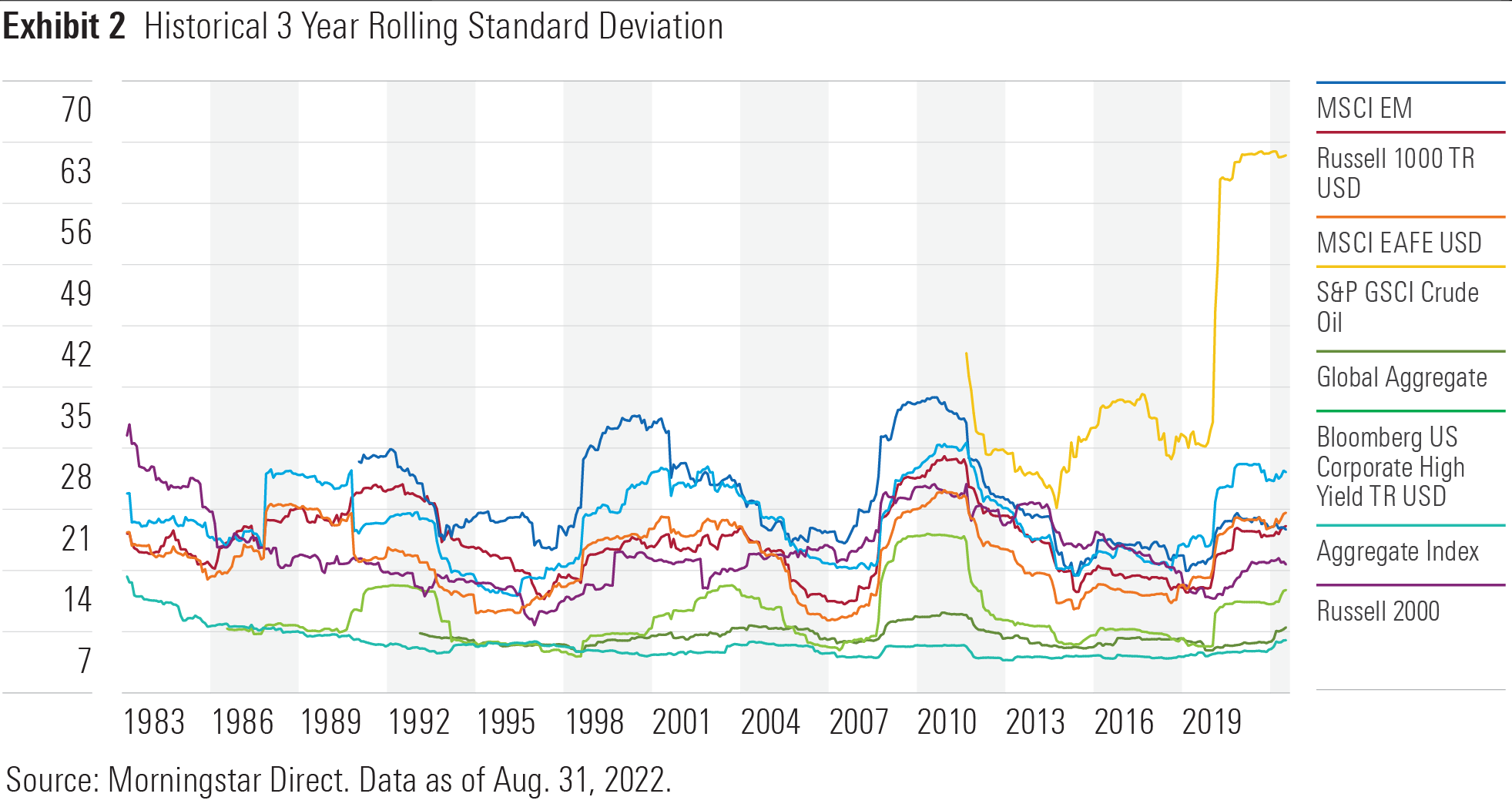

Even as stock-bond correlation increases, bonds can still be a ballast for an investor’s portfolio thanks to their relatively lower volatility and more-reliable payoff. Exhibit 2 displays rolling historical three-year volatility for several different asset classes that could potentially act as a portfolio buffer. The Russell 2000 Index proxies for domestic small caps, and the Bloomberg U.S. Corporate High Yield Index proxies for domestic high-yield bonds. The S&P GSCI Gold and S&P GSCI Crude Oil indexes represent their respective commodities. Internationally, the MSCI Emerging Markets and the MSCI EAFE indexes measure emerging- and developed-markets stocks, while the Bloomberg Global Aggregate Bond Index represents global investment-grade bonds.

Amid these options, the Aggregate Index has consistently been the least volatile, reflecting U.S. bonds’ relative stability. High-yield and global investment-grade bonds have historically maintained lower volatility than large-cap U.S. stocks, though foreign bonds can harbor currency risk and geopolitical tail risk.

Adding any of the other asset classes to a portfolio means stomaching a higher risk profile. While these allocations can pay off at times, they haven’t consistently delivered the same level of protection as U.S. investment-grade bonds.

Crude oil won the first half of 2022, but it also dropped around 60% in March 2020. Emerging-markets stocks fared better than domestic large caps during the 2008 global financial crisis, but they were crushed in the 1997 financial crisis. These asset classes can deliver diversification benefits, but their higher volatility requires investors to more carefully craft their optimal allocation based on personal risk tolerance.

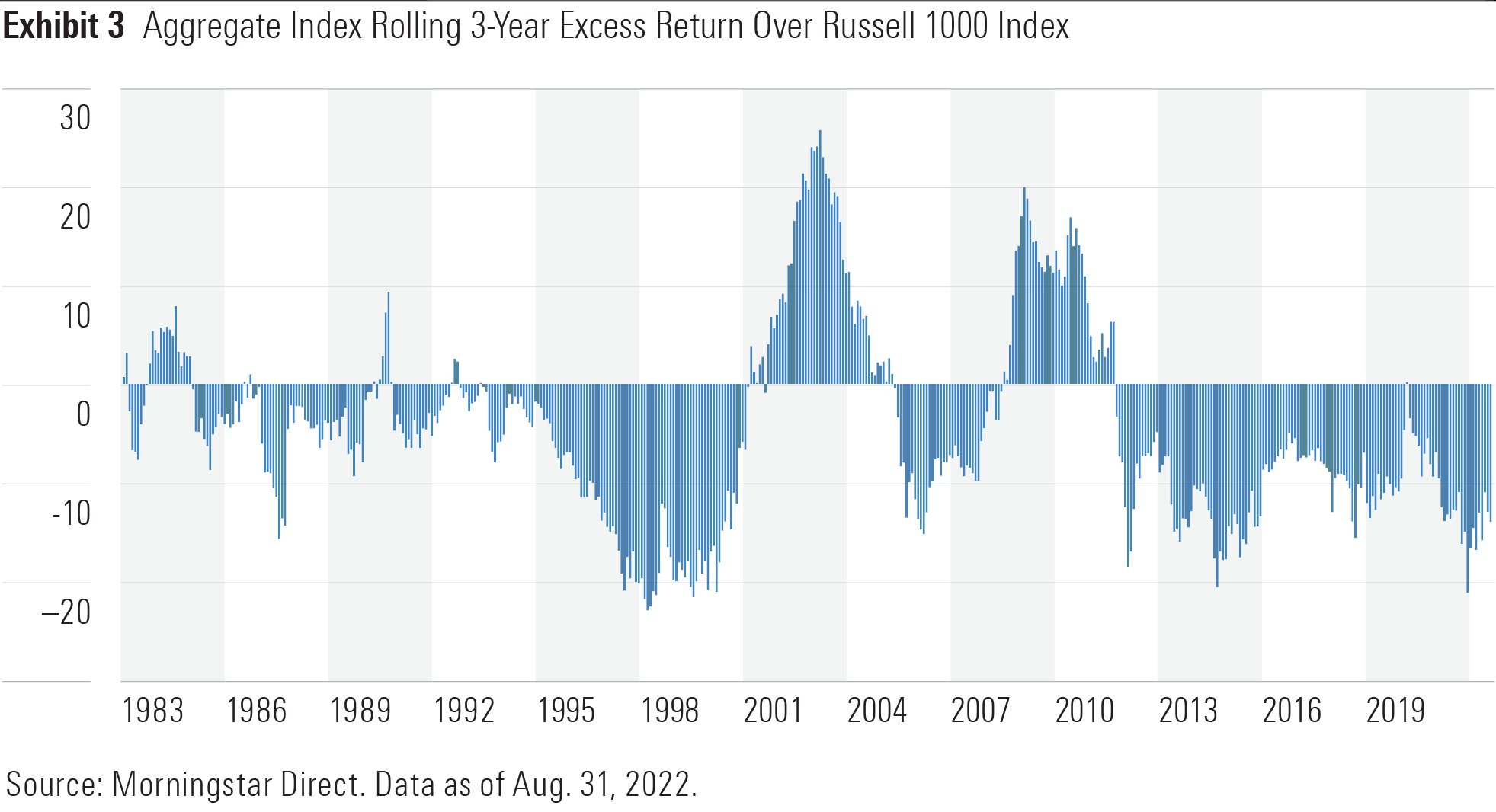

On top of lower volatility, high-quality bonds also tend to deliver strong absolute returns compared with stocks during stressed markets. Exhibit 3 plots the Aggregate Index’s excess three-year rolling return over the Russell 1000 Index’s. Bonds’ relative performance was strongest during deep bear markets when their correlation with stocks was negative, like during the dot-com crash in the early 2000s and the global financial crisis a few years later. But bonds still provided downside protection for stocks even when correlation between the two ran higher by virtue of their shallower drawdowns. Past performance does not guarantee future returns, but these trends support our current understanding of bonds’ risk/reward profile, which is unlikely to materially change anytime soon.

Overall, U.S. investment-grade bonds should continue to be a good option to round out an equity position, even if their correlation with equities starts to climb back into positive territory. Their investment merits remain strong as a ballast and risk reducer for a portfolio.

An Open Question

For investors interested in exploring different options for potential diversifiers, Morningstar has recently published the 2022 edition of our Diversification Landscape. The report provides a comprehensive look into correlations across equities and different asset classes, including sub-asset classes in fixed income, alternatives, commodities, and more.

The diversification dilemma will continue to be a contentious problem, as changes in any of the various short-term technical factors and long-term macro-economic trends can derail pre-existing assumptions. Rather than searching for a one-size-fits-all answer, which arguably does not exist, investors might be better served by a clear understanding of the factors that affect correlations while keeping a keen eye on market changes. Thorough portfolio hygiene will also be crucial, such as re-evaluating your personal risk budget and tolerance and stress-testing your current allocation against a shock to any of the relevant factors.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/24UPFK5OBNANLM2B55TIWIK2S4.png)

/d10o6nnig0wrdw.cloudfront.net/04-25-2024/t_29c382728cbc4bf2aaef646d1589a188_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/c00554e5-8c4c-4ca5-afc8-d2630eab0b0a.jpg)