5 min read

Portfolio Risk Assessment: Key Tools and Tips

To deliver personalized solutions, financial advisors must measure investment risk with confidence.

Key Takeaways

- Risk assessments allow advisors to deliver portfolios that better align with clients’ goals along with their ability and willingness to take risks.

- It’s essential to consider an investor’s portfolio risk score, risk tolerance, and risk comfort range for a more holistic view.

- Morningstar Direct Advisory Suite offers risk profiling and risk scoring tools designed to help create clarity and build client trust.

Investing will always come with risk. Still, conducting a thorough portfolio risk assessment can help advisors recommend portfolios that make sense for each client.

Ultimately, risk assessments only work if advisors understand their clients’ true appetite for risk and then match them to appropriate investments. But the output of traditional risk profiles typically squeezes investors into one of five or six investment profile bands, which may limit your ability to truly build a portfolio that reflects investors’ goals and emotions.

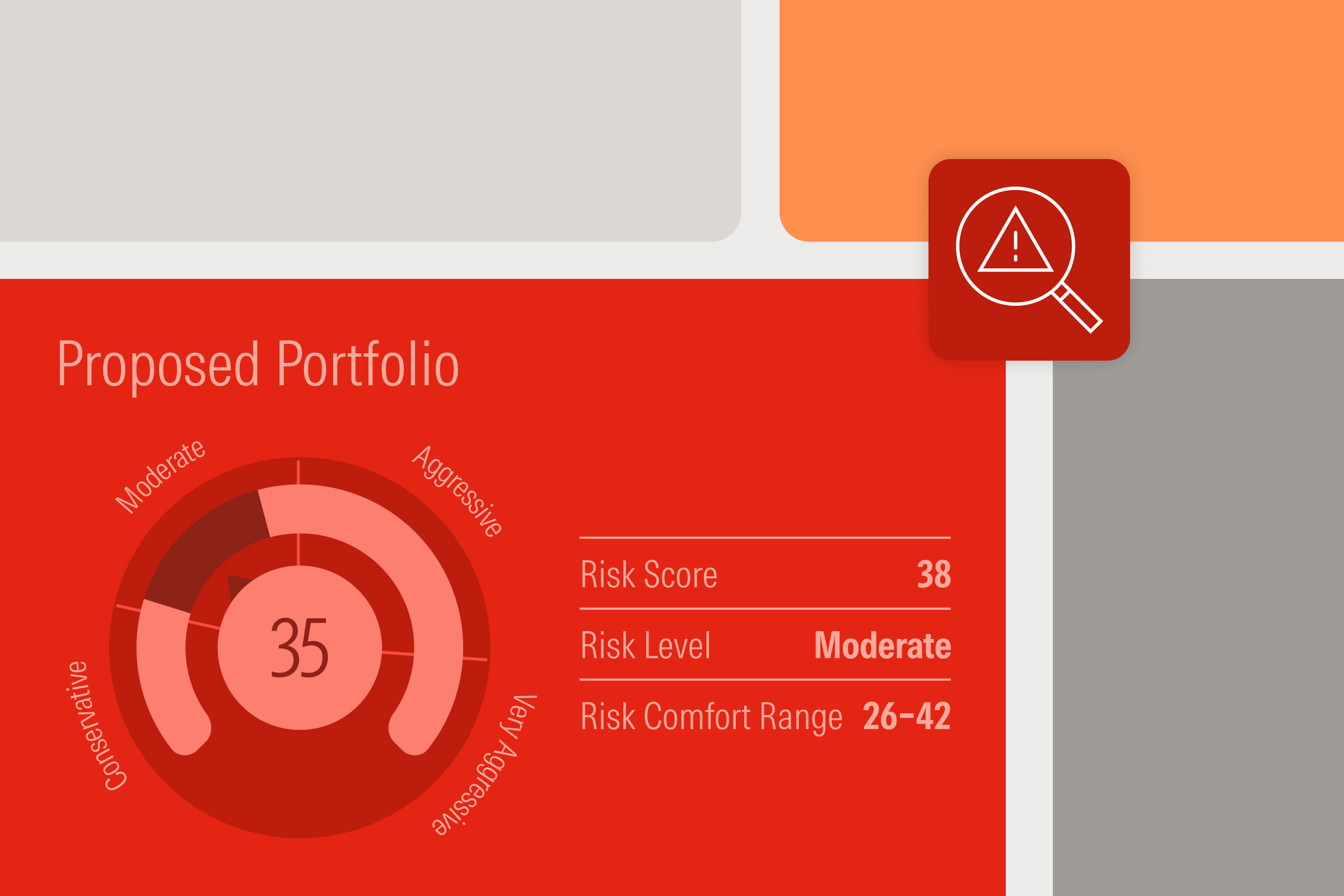

With the support of our Portfolio Risk Score, advisors can create clarity around portfolio risk and initiate productive client conversations. The powerful, proven tool measures and compares investment risks at a holdings level, allowing you to more confidently find the right portfolio fit for investors.

Here’s how to get started.

What Does Morningstar’s Portfolio Risk Score Do?

Our risk assessment tool can help you determine how much risk your client is currently taking in their accounts versus our own industry benchmarks, the Morningstar Target Allocation Indexes.

These five indexes capture the collective wisdom of the market’s target asset allocation fund managers. They give you a consistent, unbiased way to compare multi-asset portfolios and locate your clients’ accounts on a spectrum from conservative to aggressive.

Using our robust holdings-based risk model, we take a closer look at each index and every client account. Our Portfolio Risk Score, in conjunction with our Target Allocation Indexes, can create a volatility profile based on over 30 factors to get a clear picture of each account’s risk—applying the actual underlying investments, not just the asset allocation. We may then indicate a risk level for each one with the indexes serving as reference points.

Morningstar’s proposal tool can show how investment recommendations affect overall portfolio risk.

How Do You Measure Investment Risk?

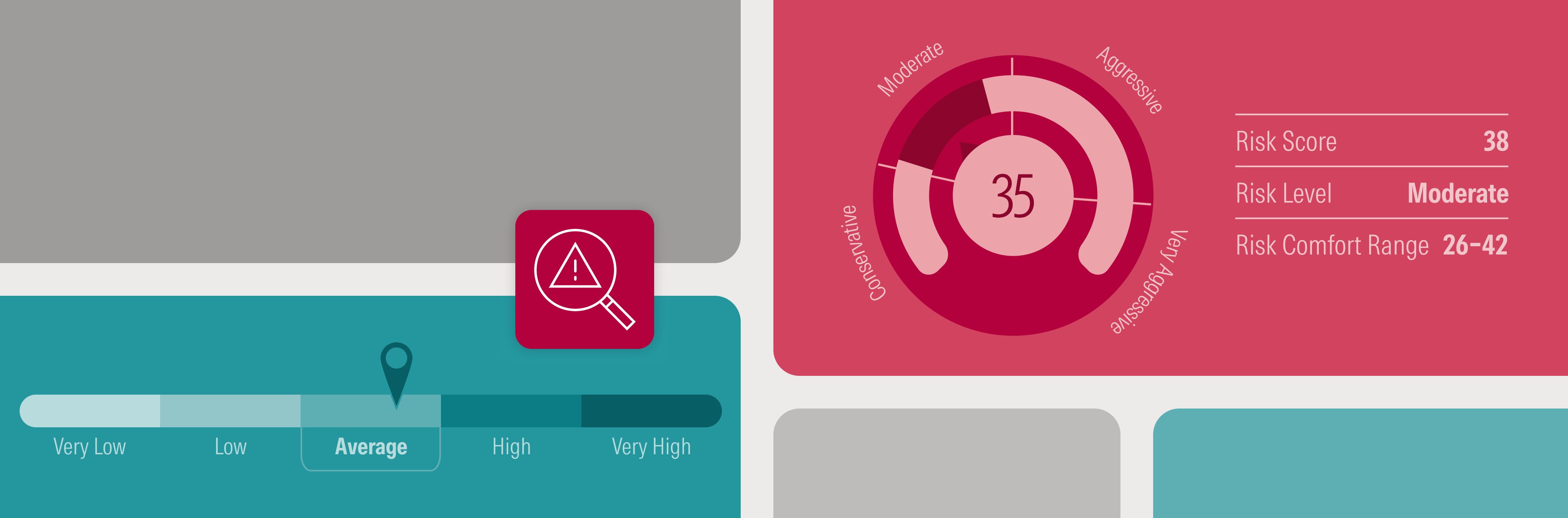

Along with identifying a risk score, advisors must also consider clients’ risk tolerance and comfort range. While risk tolerance is how people feel about taking risk, their comfort range exists as a flexible zone of risk scores that fit their personality and expectations.

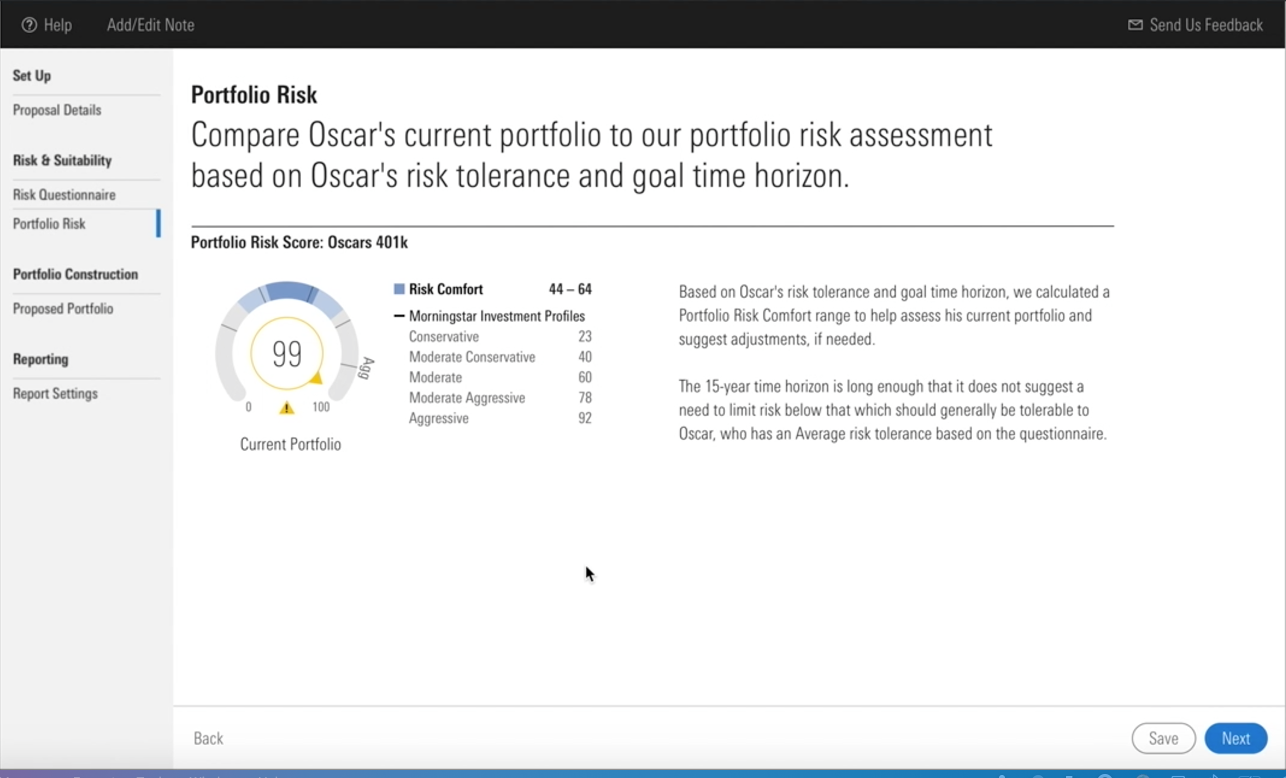

Imagine you have a client who wants to roll over his 401(k), for example. As a mid-career professional, he has 15 years or more before he plans to withdraw money from his account. What could an appropriate portfolio look like for him?

Let’s start by analyzing the makeup of his current 401(k), which in this case has a Portfolio Risk Score of 99—riskier than even Morningstar’s most aggressive profile benchmark of 92. With the Morningstar risk tolerance questionnaire, you can assess and stress-test how much risk your client may handle. This psychometric assessment will compare your client's answers against a carefully controlled data set of more than two million other completions.

Our tool allows advisors to compare the amount of risk in a client's portfolio to their tolerance of risk.

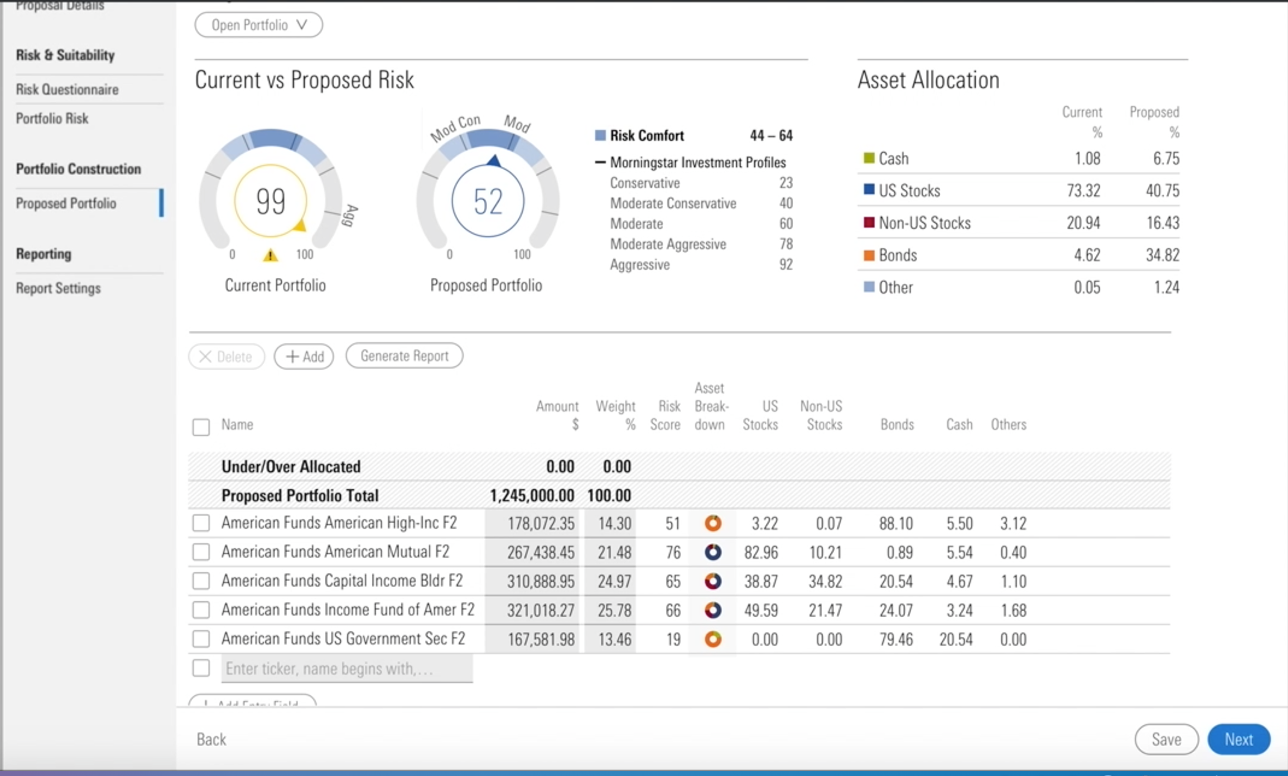

Say based on your client’s responses, he falls into the Average risk-tolerance group. His personalized Risk Comfort Range is between 44 and 64—well below his current 401(k) risk score of 99. Based on this information, your client’s portfolio may need to take some risk off the table to stay in his comfort range and most effectively meet his long-term objectives.

Our dial visual also makes it easy for clients to understand the changes between their original portfolio and your proposal—showing them how you tailored your recommendations to meet their goals and preferences.

The tool’s dial visual helps clients compare their original portfolio to an advisor’s proposal.

Why Should You Identify Investment Risk?

Combining Morningstar’s Portfolio Risk Score, Risk Tolerance Score, and Risk Comfort Range not only leads advisors to better understand investors’ attitudes and willingness toward risk, but start meaningful conversations through making risk real for clients.

Access these risk tools within Morningstar's Direct Advisory Suite. Illustrate clients’ current risk exposure and the amount of risk they should be taking—all while driving trust in your recommendations by aligning with their needs.