Sustainable Funds Weather Downturns Better Than Peers

ESG strategies lose less money than non-ESG funds during market declines.

/s3.amazonaws.com/arc-authors/morningstar/ed529c14-e87a-417f-a91c-4cee045d88b4.jpg)

/s3.amazonaws.com/arc-authors/morningstar/11b6f4c1-25d3-4bbc-8deb-d1c1aeedcce7.jpg)

Editor’s note: Read the latest on how the coronavirus is rattling the markets and what investors can do to navigate it.

As environmental, social, and governance investing has grown in popularity over the past few years, it has moved beyond being a feel-good idea. In a world threatened by climate change, the coronavirus pandemic, and with greater recognition of the costs that bad corporate stewardship have on a company's bottom line, ESG investing can mitigate those kinds of threats to a portfolio.

At the same time, evidence has been building that ESG investments can provide a cushion in portfolios to protect against stock market declines and volatility.

During the late-2018 stock market decline, for example, ESG funds proved more resilient than most funds. Then came the spread of COVID-19 and some of the most volatile conditions in stock market history. During the market turmoil, returns on many ESG funds proved to be more buoyant than those on comparable non-ESG funds.

While some of that outperformance is attributable to ESG funds’ significant underweighting of energy stocks--a group pummeled by the plunge in oil prices--the first quarter was just the most recent, and extreme, example of ESG funds performing better during down markets than their non-ESG peers. If ESG funds can show a broader benefit to a portfolio besides aligning with the investor’s values, that’s a win-win situation.

One way to answer this question is to take a broader look at how ESG funds perform based on two key metrics. First, does a fund fall more or less than the broad market or category of funds when stock prices decline? To determine this we used down capture, which measures the decline of a fund’s return compared with the fall in its Morningstar Category benchmark. That means, for example, comparing large-blend ESG funds and large-blend funds overall against the Russell 1000 Index.

Another question is, How volatile is the fund compared with other funds? In this case we used standard deviation readings, a volatility yardstick that measures how far a fund’s returns deviate from average over different time periods.

At a broad level, the story was consistent: In the past one-, three-, and five-year periods, ESG stock and allocation fund strategies lost less money than non-ESG funds during market declines and displayed less volatility. Among 11 Morningstar Categories, the average down capture for ESG funds through the year ended March 31 was nearly 12 percentage points better than category averages.

In addition, as we dug into the numbers, we found that ESG funds with higher Morningstar Sustainability Ratings did an even better job of offering downside protection and lower volatility than those with lower ESG ratings. In other words, the more that a fund held stocks of companies with stronger practices for mitigating ESG risks in their industries, the better the risk profile of the funds.

The Screen We started with a list of 230 diversified stock and allocation funds with an ESG mandate (available to premium subscribers here), as designated by Jon Hale, Morningstar's director of sustainability research.

When screening for ESG funds, we met one of the same hurdles advisors and investors face: The overall number of ESG funds is still relatively small. Some categories have only a half dozen offerings, and many have less. Many strategies are new, and many have a tiny level of assets.

Nearly 100 of the funds didn’t even crack the $100 million mark, so we decided to draw the line at $50 million. This left us with a list of 137 funds across 19 categories.

One caveat to the data: In eight of the categories, only one or two funds made it through the screen, such as foreign large growth and foreign small/mid-growth. While we included those categories in the overall medians, for most of this article, we focused on the 11 more-populated categories, such as U.S. large blend, foreign large blend, large growth, and mid-cap blend.

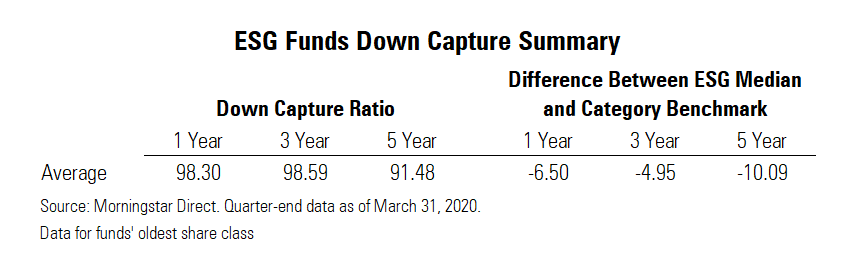

The Results Overall, for the trailing one year, the median ESG fund only lost an amount equal to 98.3% of its category benchmark's decline. This was much better than the average fund, which actually posted losses greater than the category benchmark index, at 104.8%. As a result, the median ESG fund outperformed by capturing 6.5 percentage points less of its category benchmark's decline than did the average fund in its Morningstar Category.

Exhibit 1

It was a broad-based outperformance. Out of the 19 categories, the average ESG fund in 16 categories captured less of the downside return of its Morningstar Category over the past one and three years ended March 31. For the five-year period, the average ESG fund in 14 out of the 19 categories showed better downside performance than its category average.

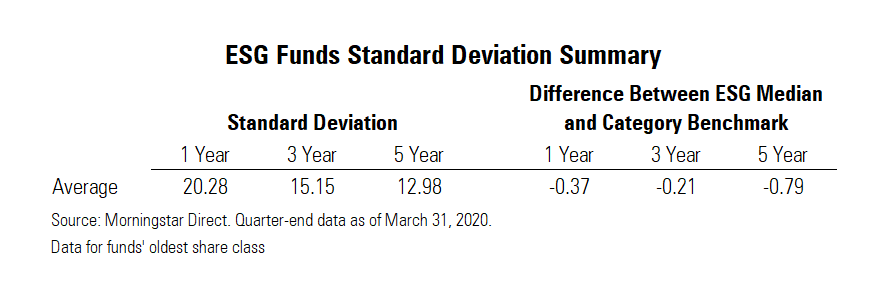

The standard deviations of ESG funds were also lower than category averages for all three time frames.

Exhibit 2

Environmental, social, and governance funds had lower average standard deviations than the category average in 14 of the 19 categories for the 12 months ended March 31, including the four most populated categories: large blend, large growth, foreign large blend, and world large stock.

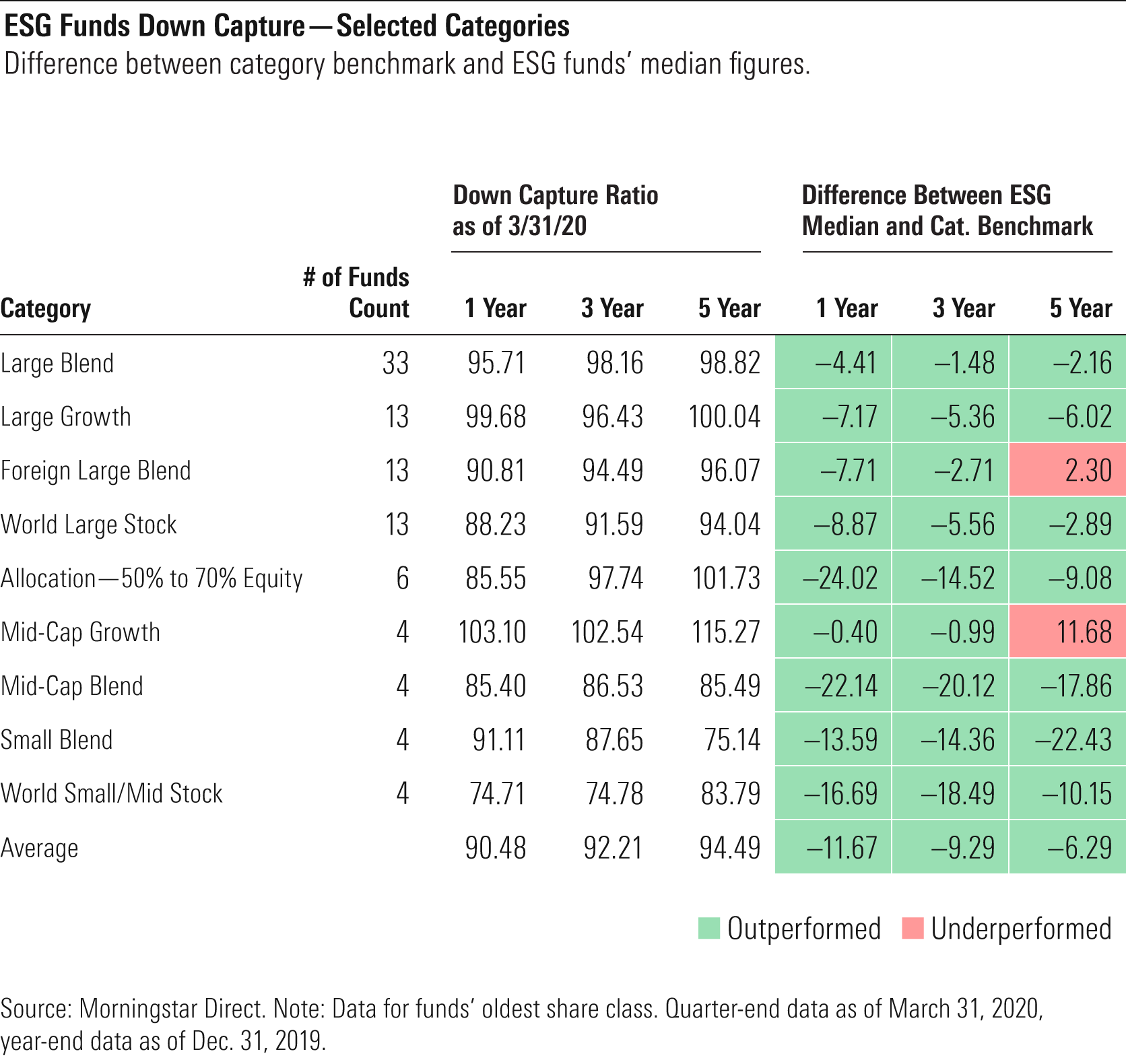

Most-Populated ESG Categories However, as we noted earlier, a number of the categories had fewer than four ESG funds that passed our initial screen, such as mid-cap value and several non-U.S. stock categories. When we excluded those 10 categories, the results were still in ESG funds' favor, including lower risk readings in key portfolio-building-block categories such as large blend, large growth, mid-cap blend, and small blend.

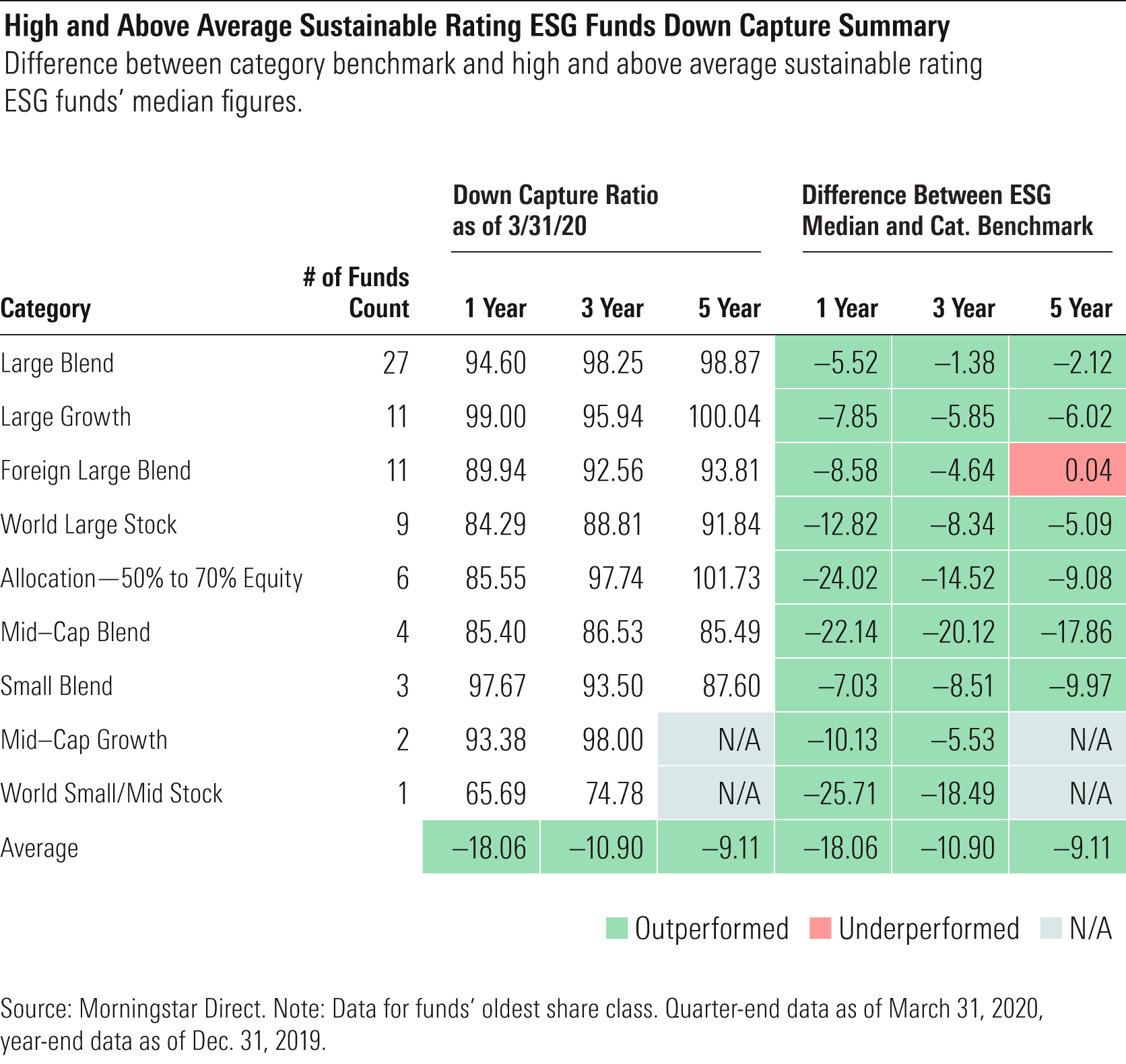

The following table highlights the results for the nine categories where four or more funds passed our ESG screen. The data show the difference between the median down capture for ESG funds in each category and that category’s average down capture relative to an index.

Take large-blend funds. When compared against the Russell 1000 Index, the median ESG fund in that category experienced 95.7% of the declines in the benchmark over the one-year period, while the median down capture for the entire category was 100.1%. With down capture of 4.4 percentage points less than the average fund, ESG funds fared better at protecting investors. We've color-coded the table so that green denotes ESG outperformance.

Exhibit 3

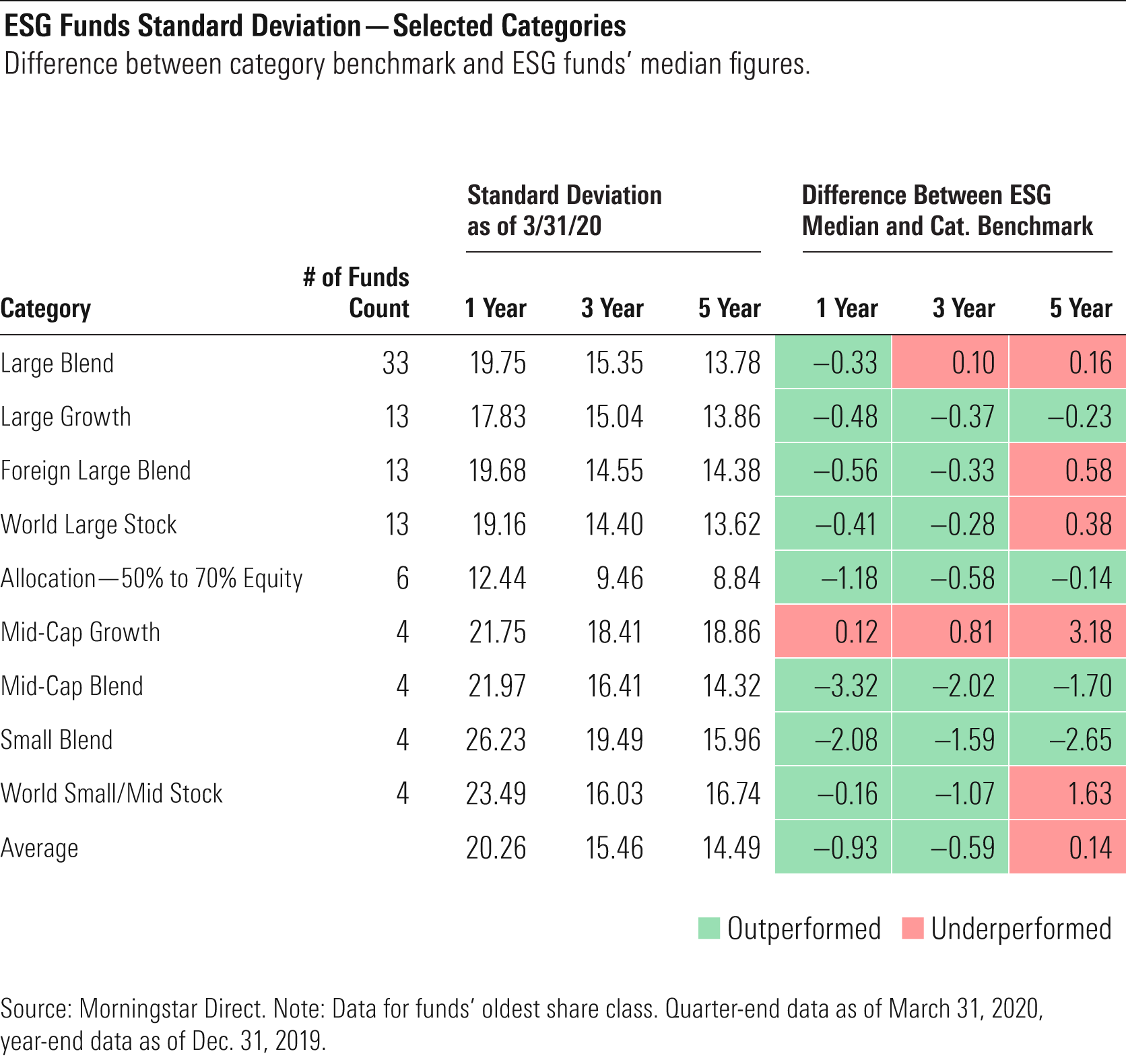

Here’s the same group, with data for standard deviation.

Exhibit 4

Funds With Higher Sustainability Ratings If the improved risk profile were reflective of ESG factors, and not some other attribute, then readings should improve when we screen for funds with better ESG risk ratings by removing lower-rated funds. And on balance, they did.

For the following tables, we filtered out 1-, 2-, and 3-globe funds on Hale’s list of funds with ESG mandates. (Just because a fund has an ESG mandate doesn’t necessarily mean it carries out that mandate in practice.) These funds earned Low, Below Average, and Average Morningstar Sustainability Ratings, respectively.

When we only included funds that earned 4 and 5 globes, these ESG funds, on average, improved their down capture by 6 percentage points against the category benchmark for the trailing year through March 31. It improved by a smaller amount for the three-year period but became worse for the past five years of returns. Note that with the additional screen, some of the categories were left with very few funds.

Exhibit 5

Fund Highlights One large-blend fund with a standout risk profile is Parnassus Core Equity Investor PRBLX, which has a Morningstar Analyst Rating of Silver and a Morningstar Sustainability Rating of 5 globes.

For the $8.6 billion fund, ESG analysis is integrated into the fund’s principal investment approach. Companies must meet Parnassus’ ESG criteria, covering various factors such as corporate governance and business ethics, charitable giving, product safety, and environmental impact. Morningstar analyst Connor Young notes that the fund fared better than S&P 500 during March’s sell-off, and it no doubt benefited from Parnassus Investments’ firmwide decision to stop investing in fossil fuel companies in the fourth quarter of 2019.

Parnassus Core Equity Investor only captured 75.5% of the market’s downturn over one year through March 31, while the average large-blend fund captured 94.6%. Its long-term risk profile also greatly outperforms the category average: Over the 10-year period ended March 31, the fund captured 83.1% of the market’s downside, while the average large-blend fund’s downside was slightly more than the market’s.

Large growth is another category where ESG funds posted better risk results. A standout among those is Calvert Equity CSIEX, with a 5-globe Sustainability Rating and $3.5 billion in assets. Calvert’s ESG analysts analyze companies by using The Calvert Principles for Responsible Investment. They analyze each company relative to an appropriate peer group based on material ESG factors as determined by Calvert.

Over one year through March 31, Calvert Equity’s performance during down markets was a stellar 39 percentage points better than the category average. Over three years, the fund was 33.8 percentage points better than the category average during down markets. Over five years, it was 33 percentage points better, and the fund was 21.3 percentage points better on a 10-year basis.

Conclusion Although performance varies among individual funds, and low weightings in energy stocks have been a boon for ESG strategies, evidence continues to build that ESG funds provide less downside risk than do their traditional peers. Investing in sustainable strategies has the potential to offer investors beneficial portfolio risk attributes and downside cushioning over short- and long-term time horizons. Add in the long-run benefits of investing in companies better poised to navigate risks poised by climate change or highlighted by the COVID-19 pandemic, and the ESG story is becoming more compelling.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/RFJBWBYYTARXBNOTU6VL4VSE4Q.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/WYB37DY4NVDTVNZTSBDENH3GMI.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/JPJHXR5CGSNR4LKQF5ZKLCCVYQ.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ed529c14-e87a-417f-a91c-4cee045d88b4.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/11b6f4c1-25d3-4bbc-8deb-d1c1aeedcce7.jpg)