Proxy Voting Adds Some Spice to Plain-Vanilla Index Investing

In proxy voting, similar index funds show their unique personalities.

/s3.amazonaws.com/arc-authors/morningstar/ed529c14-e87a-417f-a91c-4cee045d88b4.jpg)

This article originally appeared in Morningstar Direct Cloud and Morningstar Office Cloud.

It may not look like it on the surface, but all those S&P 500 index funds aren’t alike.

It’s true that there may be minute differences in how the various funds implement otherwise identical investment strategies, and most significantly, fees are the primary differentiator.

But there is another layer hidden from easy view for investors interested in sustainable investing: how the funds vote as shareholders in corporate elections.

With sustainable investing, a direct connection is made between investments and their social and environmental impacts, such as climate resilience, forced labor, deforestation in supply chains, or workforce diversity. Along with the business lines and practices of the underlying companies a fund invests in, such issues are front and center in corporate elections, which can help set company policies.

An S&P 500 index fund by its nature simply invests in those companies, so its managers can’t pick and choose which stocks to invest in. But given that companies in the S&P 500 represent 80% of the U.S. stock market measured by market size--along with a massive $1.6 trillion in assets at these funds--the footprint of these funds’ voting records carries particular weight. It also provides investors with a window into a fund company’s overall tilt when it comes to sustainable investing issues.

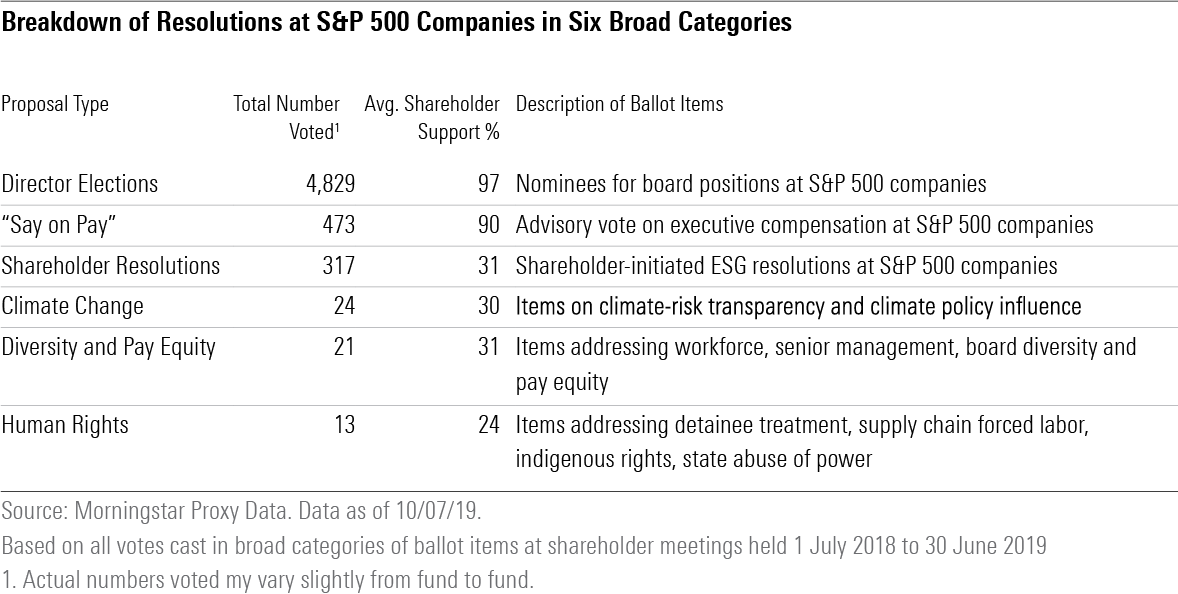

For this article, we tallied the 2019 voting records of 16 S&P 500 index funds, including the industry’s largest. These records contain votes cast at constituent company annual meetings held between July 1, 2018, and June 30, 2019, where a total of 6,060 individual ballot items were voted on.

Most of these votes were standard items that company management places on the ballot from year to year: director elections, advisory votes on executive compensation, ratifying the selection of the audit firm for the following fiscal year, and, sometimes, approving new or amended equity incentive plans.

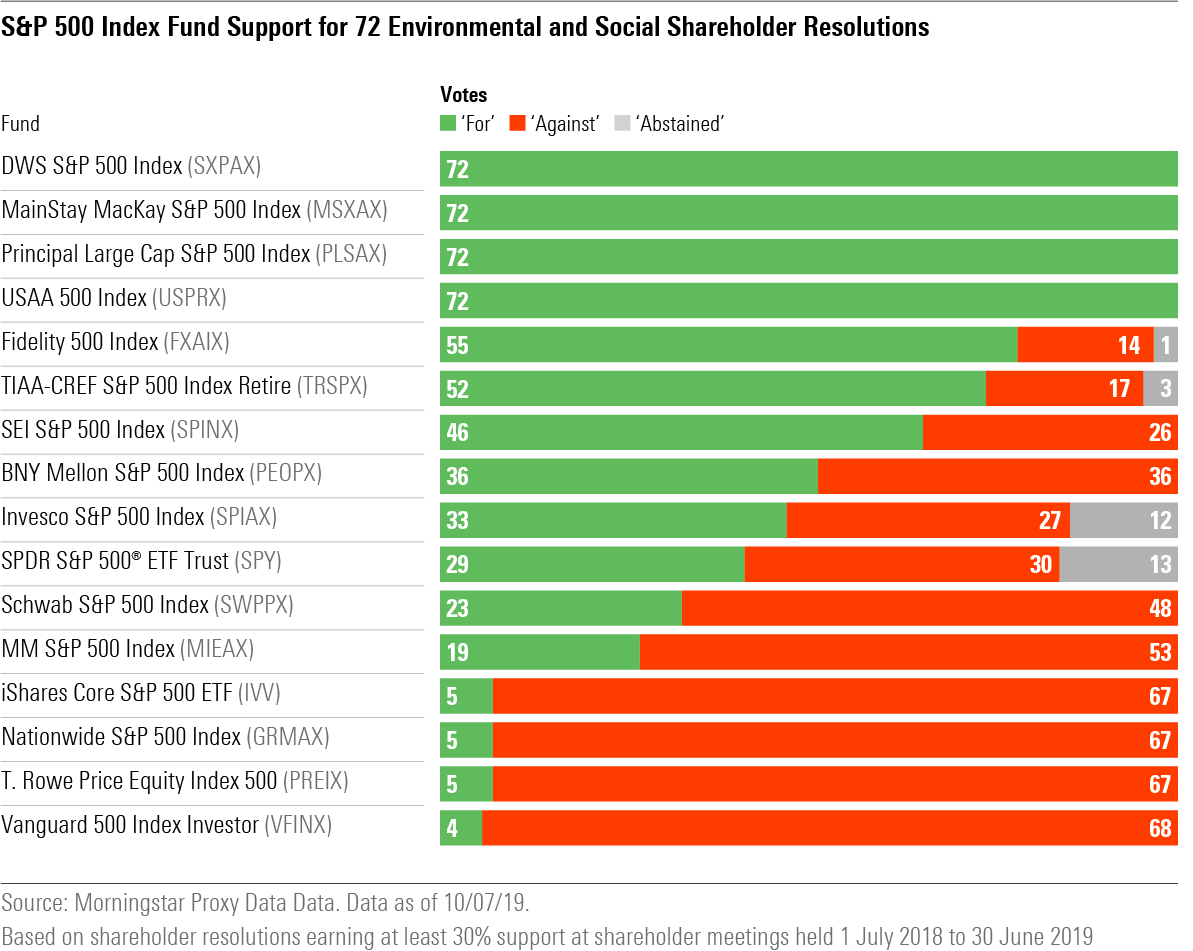

A relatively small number of voting items are placed on the proxy ballot by shareholders. In 2019, 329 ballot items were voted on by shareholders of S&P 500 companies, of which 317 addressed environmental, social, and governance concerns. Of these, 151 addressed social and environmental concerns, of which 72 achieved at least 30% shareholder support--a significant outcome that attracts the attention of boards and management. We’ll focus first on those questions that reached that 30% shareholder support level.

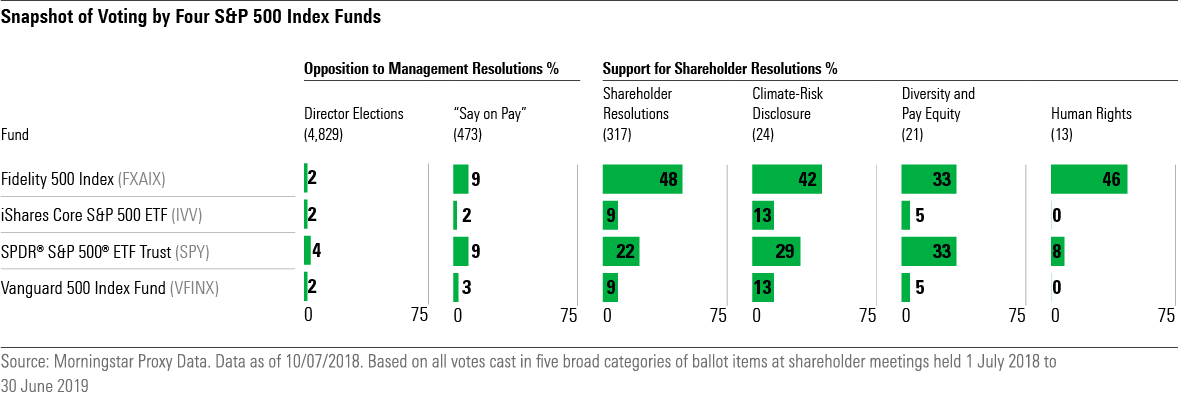

Four S&P 500 index funds supported all 72 of these ballot initiatives. Four supported five or fewer of these initiatives, including two of the three largest S&P 500 funds: Vanguard 500 Index and iShares Core S&P 500 ETF. The second-largest S&P 500 index mutual fund is Fidelity 500 Index Fund, managed by Fidelity’s Geode unit, which operates separately from the group that funds Fidelity’s actively managed stock funds. Fidelity was at the opposite end of the spectrum from BlackRock and Vanguard as it supported 55 of the 72 ballot questions.

A closer look at the aggregated votes by funds offered by the largest four asset managers shows that State Street takes the strongest stand on executive pay--admittedly, only by a few votes--and Geode voted in support of climate-risk-, human-rights-, and diversity-related issues more often than the others.

BlackRock and Vanguard often point to “engagement”--meeting with corporate managements--as their preferred method of having an impact in company policies. Many large asset managers have initiated or expanded their engagement programs in recent years. In the case of actively managed funds, a portfolio unhappy with a company’s stewardship can also sell the stock, but an index fund does not have that ability. It’s for that reason that sustainable investing advocates see a public shareholder vote as a powerful statement by index fund managers.

Here’s a broader look at the voting record of the 16 funds we examined on those 72 environmental and social shareholder resolutions achieving at least 30% support.

Among the fund providers, some are much more likely to support shareholder initiatives on social and environmental issues, and some are more likely to vote in line with management’s recommended vote--which is typically "against."

DWS supports the votes tracked by investor advocacy organization Ceres. DWS is a member of the Climate Action 100+ coalition of investors undertaking targeted collective engagements, and is also a member of the recently formed Coalition for Climate Resilient Infrastructure Investments.

USAA Asset Management Company, offering the USAA funds to military members and their families, was acquired by Victory Capital in July 2019. Mainstay funds are offered by New York Life Investments, which in turn is owned by New York Life Insurance Company. The proxy voting guidelines of Mainstay, Principal, USAA, and DWS indicate that they closely follow the model proxy voting guidelines of Institutional Shareholder Services, a proxy vote research company.

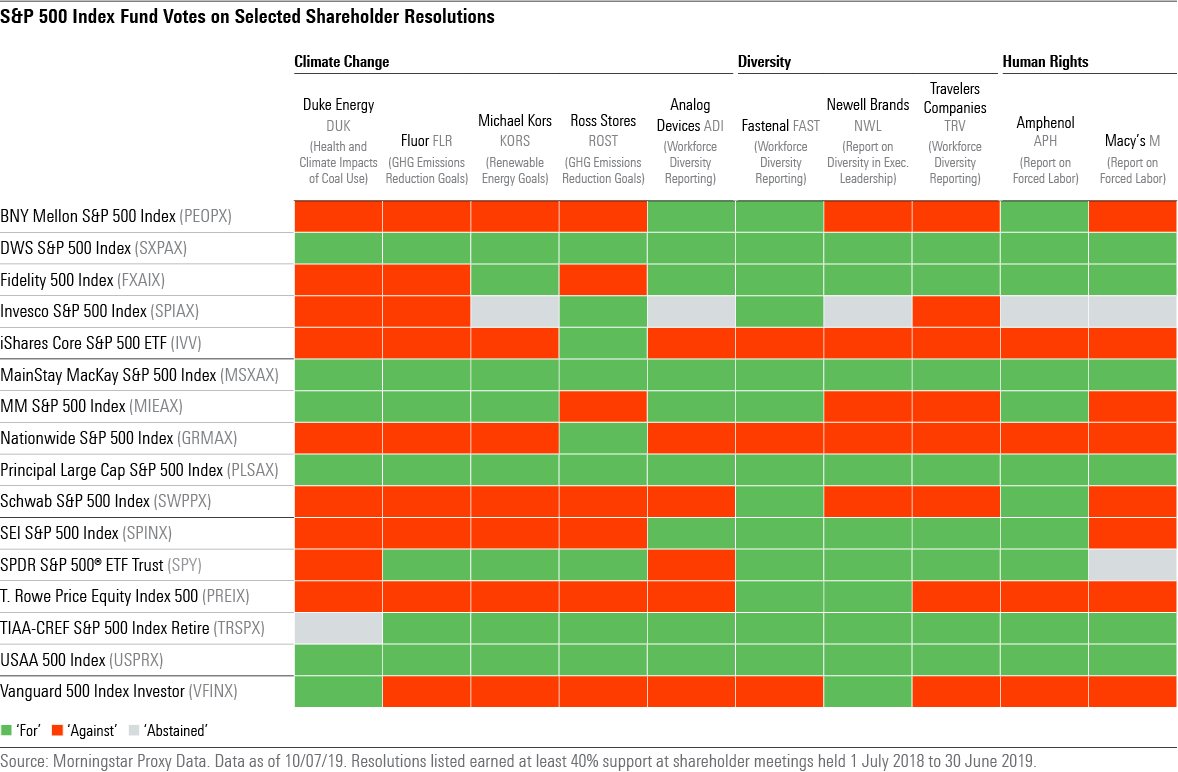

Looking in more detail at the voting patterns, the chart below shows votes on a selection of the most strongly supported ballot items in each of three broad categories: climate change, diversity, and human rights. Resolutions in these three categories generally ask companies to disclose their emission reduction and climate resilience plans; diversity at the workforce, senior management, and board levels; and what measures are being taken to eliminate forced labor from supply chains or manage operations in regions or lines of business vulnerable to state-level abuse of power.

Across the ballot, funds offered by BlackRock and Vanguard are far less likely to oppose management than are the index funds offered by Fidelity, as well as funds offered by State Street Global Advisors.

Fund for fund, advisory votes on pay practices show a high level of correspondence with votes on environmental and social shareholder resolutions: Funds that tend to support shareholder proposals also tend to vote more severely on pay practices.

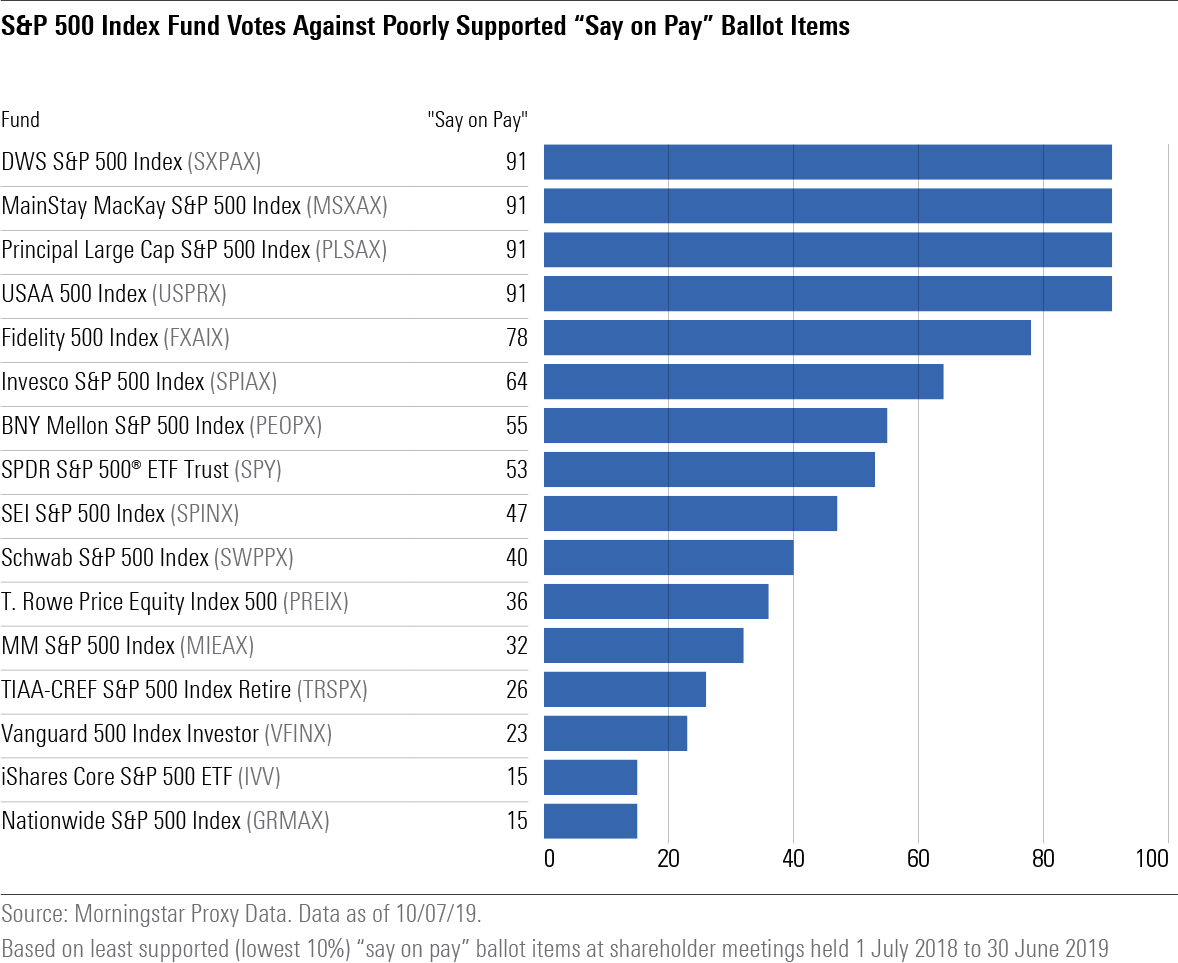

Most S&P 500 companies offer shareholders an annual "say on pay" vote. The remainder would offer this vote to shareholders once in two or three years. This is a voting right that shareholders have had since 2011 under the Dodd-Frank Act. While the outcome is nonbinding, it gives an indication of how satisfied shareholders are with pay practices at the company.

In 2019, 477 "say on pay" resolutions came to vote across the index of companies, earning an average of 90% support. Ten percent of these resolutions earned 75% or less support. A low result typically reflects shareholder concerns about the link between pay and performance and, more recently, with the advent of the new pay-ratio disclosures, with high CEO pay relative to that of the "median worker" for a given industry. "Say on pay" vote outcomes are a noisy signal but one that boards, management, and their advisors watch closely.

The four funds most likely to support shareholder resolutions addressing environmental and social issues are also more likely to vote down the worst-performing "say on pay" resolutions. Conversely, three of the four funds at the bottom of the shareholder resolution support ranking are among the four that most frequently supported the 47 least popular "say on pay" resolutions. From their voting records, these funds seem to be relatively satisfied with the status quo.

When taken altogether, the varied voting patterns across S&P 500 index funds provide investors interested in the impact of their investments another set of information to weigh.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/NNGJ3G4COBBN5NSKSKMWOVYSMA.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/6BCTH5O2DVGYHBA4UDPCFNXA7M.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/EBTIDAIWWBBUZKXEEGCDYHQFDU.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ed529c14-e87a-417f-a91c-4cee045d88b4.jpg)