Utilities Face Inflation, Interest-Rate Fears

But there is a bright side: clean energy and clean balance sheets.

/s3.amazonaws.com/arc-authors/morningstar/ea0fcfae-4dcd-4aff-b606-7b0799c93519.jpg)

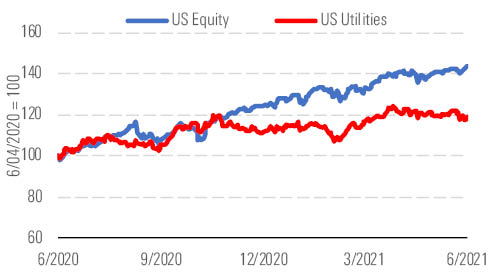

Utilities can’t shake their pandemic swoon. Now with inflation ticking up and talk of Federal Reserve interest-rate hikes during the next 12-18 months, utilities face an uphill battle against the market. Hawkish comments from the Fed in mid-June sent the Morningstar US Utilities Index down 3% on June 18, its largest dip since last October. Utilities were the worst-performing sector through the first half of this year and still haven’t reached their prepandemic high.

Utilities continue to miss out on the market rally. - source: Morningstar

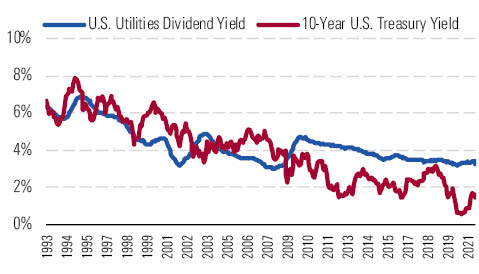

Despite the macro challenges, there are some positives. Utilities remain one of the few places in the market for stable, growing income. With the 10-year U.S. Treasury yield hanging near 1.5%, the spread between interest rates and utilities’ 3% average dividend yield remains historically attractive.

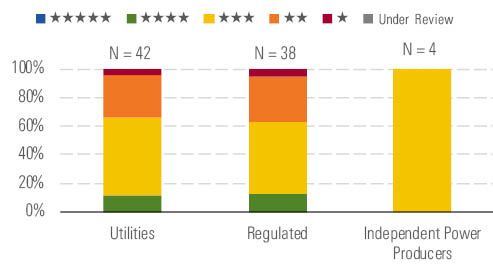

Some high-quality utilities now trade below fair value. - source: Morningstar

Utilities also have two hefty tailwinds. First, interest rates remain low. A long stretch of low interest rates has allowed utilities to strengthen their balance sheets, issuing or refinancing debt at rates that will keep interest expense low for a long time. This creates a cushion for earnings and dividend growth.

Utilities’ dividend yields holding steady even as interest rates rise. - source: Morningstar

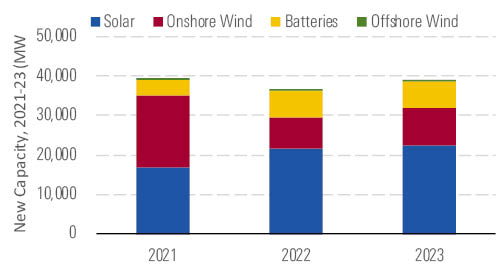

Second, clean energy growth is in full throttle. Utilities will lead the economywide decarbonization through investments in renewable energy, electric grid upgrades, and electric vehicle infrastructure. At the beginning of the year, utilities and developers planned to add 28 gigawatts of wind and solar projects in 2021, according to government data. But the U.S. is on track to top that easily. In the first quarter, 5.6 GW of new wind and solar projects went into service, and the latest data show 26.6 GW either came on line during the second quarter or is set to come on line this year.

Solar, battery development accelerate while wind growth drops off. - source: Morningstar

In 2021-23, the U.S. is set to add 97 GW of wind and solar, but that number will probably continue to grow. This far outpaces the 20 GW of planned coal plant retirements and will require huge investments in the transmission and distribution grid. Washington’s latest iteration of the infrastructure spending plan includes as much as $130 billion for water and electric investment. All of this means a long pipeline of steady, transparent growth for utilities.

Top Picks

NextEra Energy NEE Star Rating: ★★★ Economic Moat Rating: Narrow Fair Value Estimate: $75 Fair Value Uncertainty: Low

Although the stock isn’t screaming cheap, we think investors should look at NextEra, one of the highest-quality and fastest-growing utilities in the U.S. No utility in the U.S. is better positioned to benefit from the renewable energy transition. Management's history of execution leaves us confident that NextEra will deliver nearly 30 GW of new renewable energy projects by 2024. NextEra is also planning 10 GW of new solar by 2030 at its Florida utility, where it receives regulated returns on its investments. Florida’s constructive regulation allows NextEra to earn industry-leading returns and support a fast-growing dividend.

Edison International EIX Star Rating: ★★★★ Economic Moat Rating: Narrow Fair Value Estimate: $70 Fair Value Uncertainty: Medium

Edison offers a triple play of value, growth, and income with a yield above 4%. California’s progressive energy policies offer more growth opportunities than other states. Edison has widespread support for $5 billion of annual electricity grid investments that facilitate wildfire mitigation, renewable energy, and electric vehicle adoption. Edison is one of the few utilities with no direct carbon emissions exposure. We forecast 6% average annual earnings growth during the next five years with similar dividend growth. We think the market is too concerned about Edison’s wildfire liability risks and long-term capital needs.

American Electric Power AEP Star Rating: ★★★ Economic Moat Rating: Narrow Fair Value Estimate: $70 Fair Value Uncertainty: Low

Most of the states where AEP operates were slow to embrace renewable energy, but that is changing. AEP plans to install 10.6 GW of wind generation and 5.9 GW of solar generation while retiring nearly 5 GW of coal generation. This plan offers significant growth opportunities in its transmission and distribution network, which is the largest in the U.S. More than 80% of AEP’s five-year $37 billion investment plan is dedicated to expanding and modernizing its network to support renewable energy. This is a key driver of our 6% earnings growth estimate through 2025, the midpoint of management's 5% to 7% earnings target.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/RNODFET5RVBMBKRZTQFUBVXUEU.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LJHOT24AYJCHBNGUQ67KUYGHEE.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/V33GR4AWKNF5XACS3HZ356QWCM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ea0fcfae-4dcd-4aff-b606-7b0799c93519.jpg)