Markets Brief: Bond Yields Rise, Bank Stocks Struggle

Major banks start reporting. Delta and travel stocks rise higher. Healthcare stocks reverse gains while Nvidia and AMD extend losses.

/s3.amazonaws.com/arc-authors/morningstar/ed529c14-e87a-417f-a91c-4cee045d88b4.jpg)

While the stock market has become a bit cooler in recent weeks after a volatile first quarter, the action is continuing in the bond market.

With inflation continuing to run extremely hot (although showing small hints of a future cooldown) and the Federal Reserve signaling a determination to substantially raise rates this year, bond yields have continued to push higher. The U.S. Treasury 10-year note hit 2.83% this past week, up from 2.39% on April 1 and 1.52% on the final day of 2021.

Much of the attention this year has been on the headwinds that higher rates meant for stocks of fast-growing companies, especially last-year’s high-flying technology and communications names. More recently, higher mortgage rates have dented homebuilders and furnishing retailers.

Another interesting story has been bank stocks. Many bank stocks came into 2021 on a tear. Among the industry’s giants, Wells Fargo WFC surged 61% last year, Bank of America BAC jumped 49.6%, and JPMorgan Chase JPM rose 27.7%. Those returns helped lift the bank-heavy Financial Select Sector SPDR ETF XLF 34.8% in 2021.

A big reason for the rally was the fact that long-term interest rates were rising but short-term rates were being kept low by the Fed. The result was a "steepening yield curve," which is good news for bank profits. Banks can bring in cash at low short-term rates and lend to customers at higher longer-term rates, boosting their net interest income. At the same time, the economy is chugging along and creating a great environment for making loans. Pretty much a goldilocks scenario.

The downside was the valuations on many bank stocks were at or above Morningstar’s fair value estimates. Bank of America, for example, finished last year 17% above its fair value estimate.

As Morningstar strategist Eric Compton cautioned in January, “most bank sector theses we see are simply ‘higher rates equals good earnings momentum, which means you should buy banks.’ Eventually, we think investors will have to move beyond this.”

That story has changed significantly in 2022. As it became clear the Fed will be raising the federal-funds rate, short-term market rates have jumped to the point where two weeks ago, the yield on the two-year note briefly rose above that of the 10-year, a dynamic known as an “inverted yield curve” and one that removes the tailwind from bank net interest income profits.

At the same time, the economic outlook has been cloudier with inflation remaining higher than many had expected and eating into consumers ability to spend. The ripples from Russia's invasion of Ukraine have only added to the uncertainty, and in some cases, forced global banks to take losses related to the Russian attack and sanctions.

Earlier this month, Compton wrote “with interest-rate expectations high, we think it's imperative that investors consider their rate risk exposure. There is downside at today's prices if the higher rate narrative falls apart and economic growth stalls. With some indicators of recession risk rising, we can see this playing out in real time.”

Meanwhile, a number of bank stocks have taken a beating this year. With that has come a drop in valuations.

So what’s next for bank stocks? As first-quarter earnings have come in, the picture has been mixed.

With JPMorgan, while overall first-quarter earnings were hit by higher expenses and a drop in investment banking fees, Compton writes that the bank's results suggest a still strong net interest income outlook.

For Wells, Compton labeled the first quarter earnings report “disappointing,” and while net interest income was basically flat, “the news wasn’t all bad,” he wrote. “Due to recent changes in rate expectations as well as better-than-expected loan growth, management now thinks they could potentially grow net interest income by a midteens amount this year, roughly double the 8% growth guide from last quarter.”

We’ll get more clarity as earnings continue to be posted in the coming week, with Bank of America due out Monday.

Among the events scheduled for next week:

- Monday: Bank of America earnings.

- Tuesday: Netflix NFLX and Johnson & Johnson JNJ earnings.

- Wednesday: Tesla TSLA and Procter & Gamble PG earnings.

- Thursday: United Airlines UAL, American Airlines AAL, Huntington Bancshares HBAN, AT&T T, and Snap SNAP are all due to report earnings.

For the trading week ending April 14:

- The Morningstar US Market Index was down 1.82%.

- The best-performing sector was basic materials, up 0.96%.

- The worst-performing sectors were technology, down 3.39%, and healthcare, off 2.77%.

- Yields on the U.S. 10-year Treasury note rose to 2.83% from 2.71%.

- Oil ended the week up 8.84% to $106.95 per barrel.

- Of the 866 U.S.-listed companies covered by Morningstar, 355, or 41%, rose, while 511, or 59%, fell.

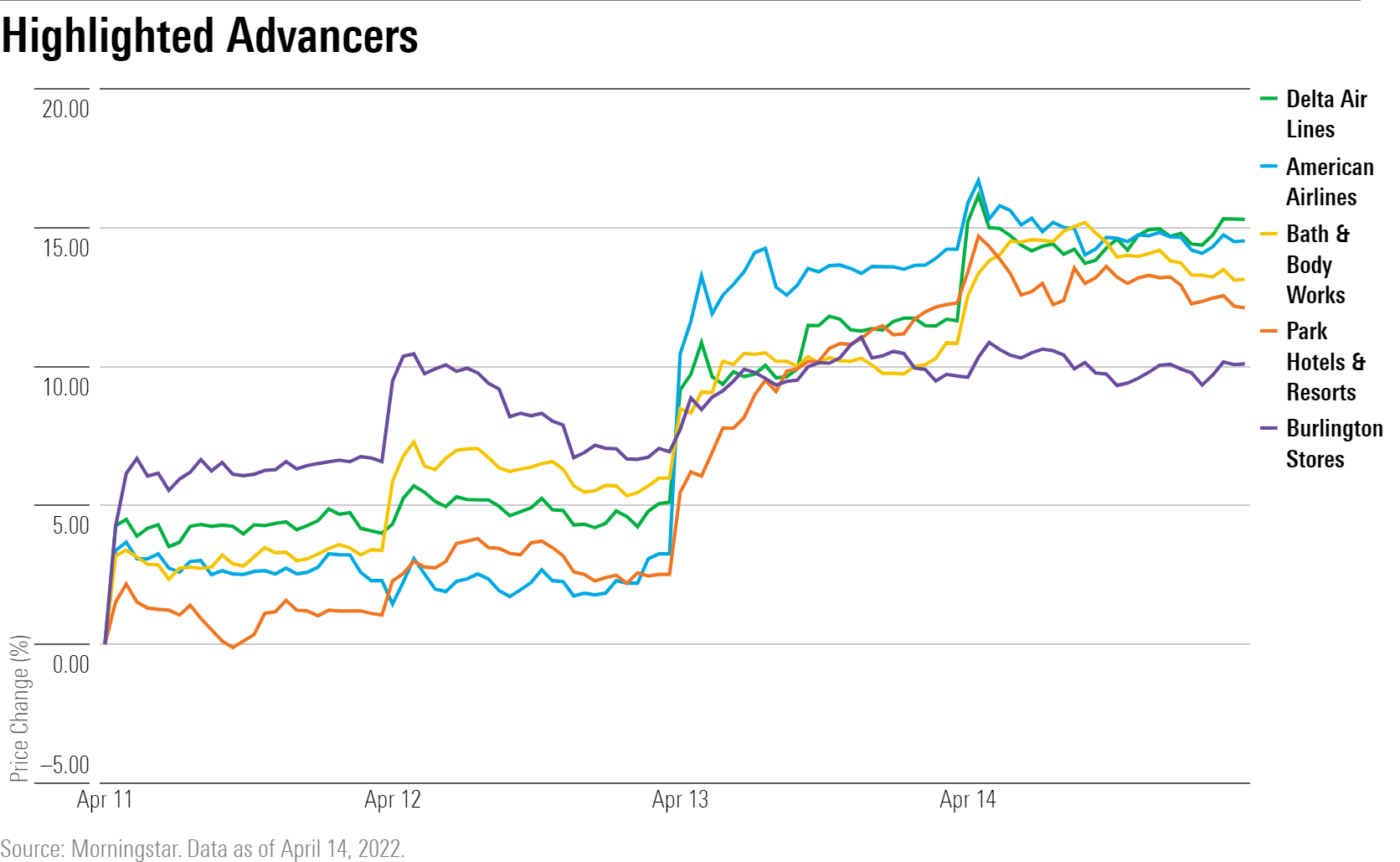

What Stocks Are Up?

The best-performing stocks last week were VNET Group VNET, ESAB ESAB, Delta Air Lines DAL, American Airlines, and Southwest Airlines LUV.

Several travel stocks rallied after Delta Air Lines beat earnings. American Airlines and United Airlines rose higher ahead their earnings calls this Thursday. Hotel stocks also closed higher, led by Park Hotels & Resorts PK, Pebblebrook Hotel PEB, and Host Hotels & Resorts HST.

Retailers Burlington Stores BURL, Macy’s M, and GAP GPS closed higher after U.S. retail sales rose 0.5% in March despite inflation pressures. While most of the increase was attributed to higher gas prices, spending increased in various categories including apparel, electronics, and appliances.

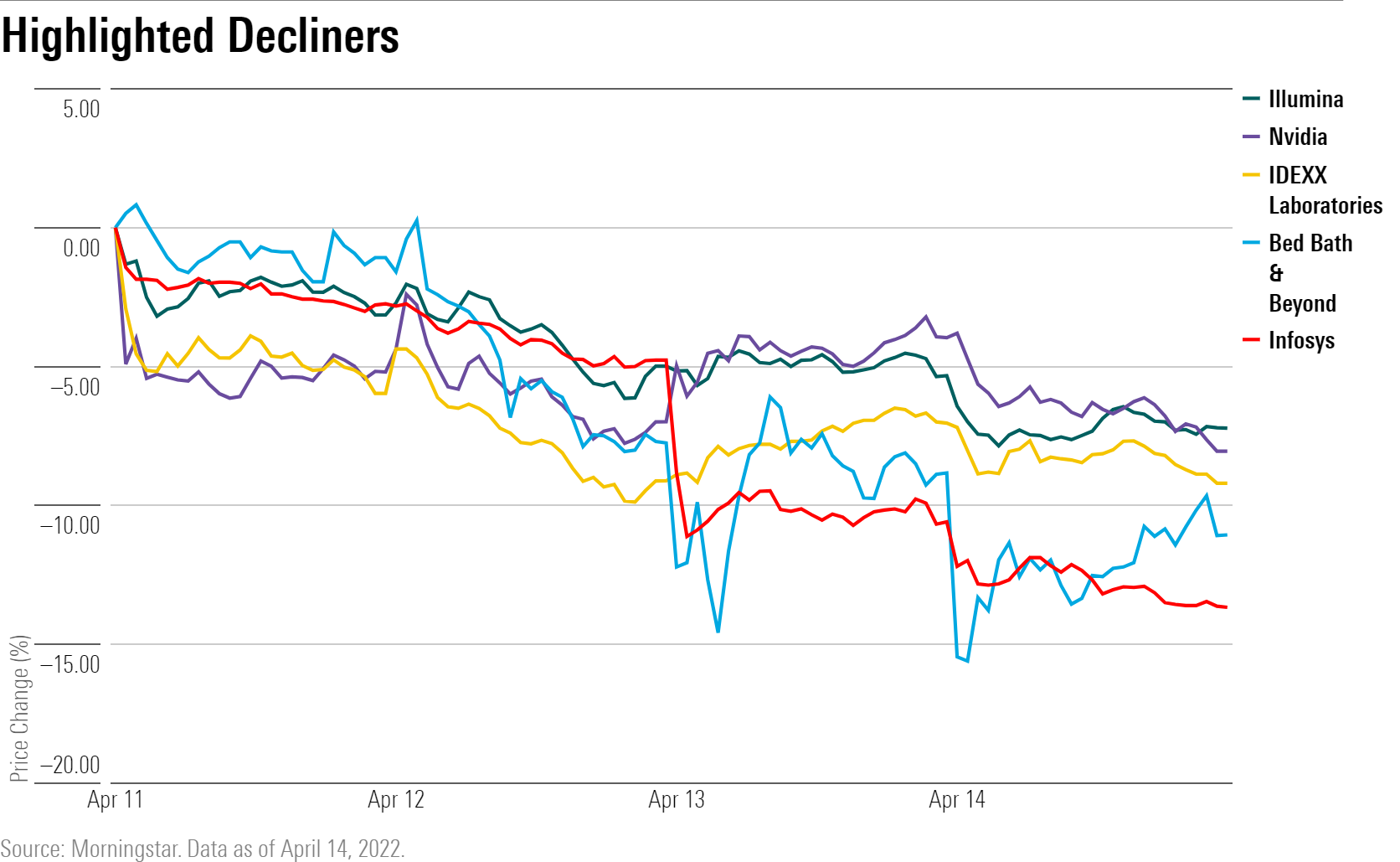

What Stocks Are Down?

The worst-performing stocks last week were Just Eat Takeaway JTKWY, Infosys INFY, Generac Holdings GNRC, Ericsson ERIC, and Bed Bath & Beyond BBBY.

Shares of Bed Bath & Beyond fell after the retailer posted disappointing results for the fourth quarter, an earnings per share loss of 92 cents, lower than the market consensus of a 3 cent profit, according to FactSet. Earnings results also dragged down shares of India-based IT services provider Infosys.

Healthcare stocks reversed gains from the week prior, among the worst performers were diagnostic and research firms such as Idexx Laboratories IDXX, Illumina ILMN, and Danaher DHR.

Semiconductor firms extended losses from the prior week, with Synopsys SNPS, Nvidia NVDA, and Advanced Micro Devices AMD lower.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/347BSP2KJNBCLKVD7DGXSFLDLU.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/UBLNP5GU6FGPFN3AAPXRHIRQ5U.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/G7LHSQ2WCVH73BP6DDQQS5H6FA.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ed529c14-e87a-417f-a91c-4cee045d88b4.jpg)