Healthcare Stocks: Valuations Look Attractive Across Almost All Industries

Our top picks in the sector are Illumina, Moderna, and Zimmer Biomet.

/s3.amazonaws.com/arc-authors/morningstar/a90c659a-a3c5-4ebe-9278-1eabaddc376f.jpg)

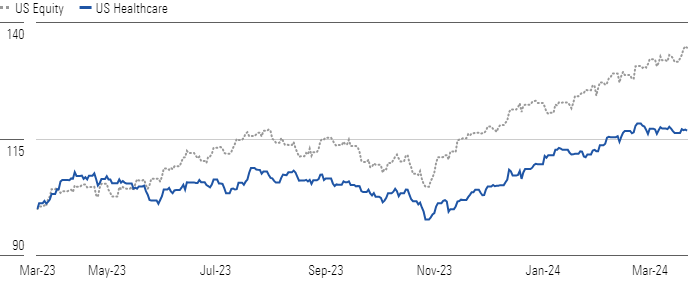

Over the past 12 months, overall equity has outperformed the Morningstar US Healthcare Index by over 17%. As concerns about recessionary pressures appear to have decreased, this more defensive sector underperformed over the past several months.

Healthcare Underperformed the Market Over the Past 12 Months

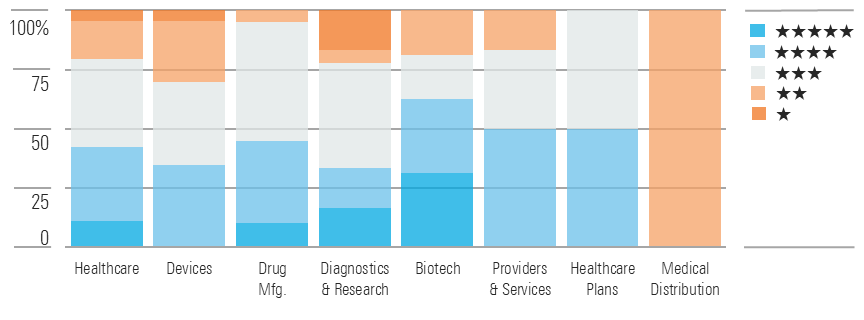

We view healthcare as undervalued, with nearly 45% of these stocks rated 4 or 5 stars and 20% rated 1 or 2 stars. In aggregate, our healthcare coverage trades below our overall estimate of intrinsic value. Besides medical distribution and devices, these industries look largely undervalued.

Majority of Healthcare Industries Undervalued

Within the biotech and drug manufacturing group, the market is not fully appreciating innovation in several therapeutic areas (including oncology, immunology, and rare diseases), as well as the industry leaders’ wide moats. In the healthcare plan industry, we believe the short-term headwinds of potential pharmacy benefit reforms, Medicaid redeterminations, and Medicare Advantage deceleration are creating undervalued opportunities, as the industry can offset these challenges over the long run.

In the device and diagnostic industries, we see compelling valuations after falling from a period of over-optimism during the peak of the covid-19 pandemic. As perceptions normalize, we believe the sector will increase in value. We believe the industry’s largest market in the United States will likely face some volatility during the 2024 election cycle and related political rhetoric, but we are not expecting major fundamental changes for most healthcare industries.

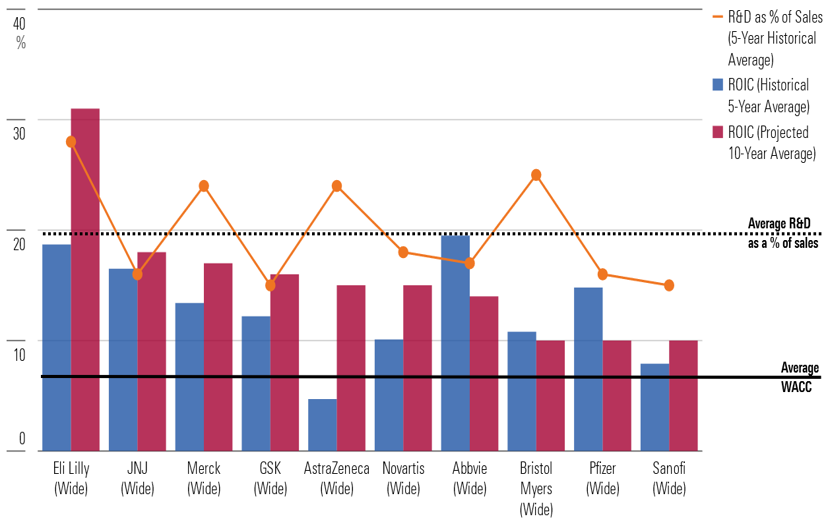

Investments In R&D Support Returns

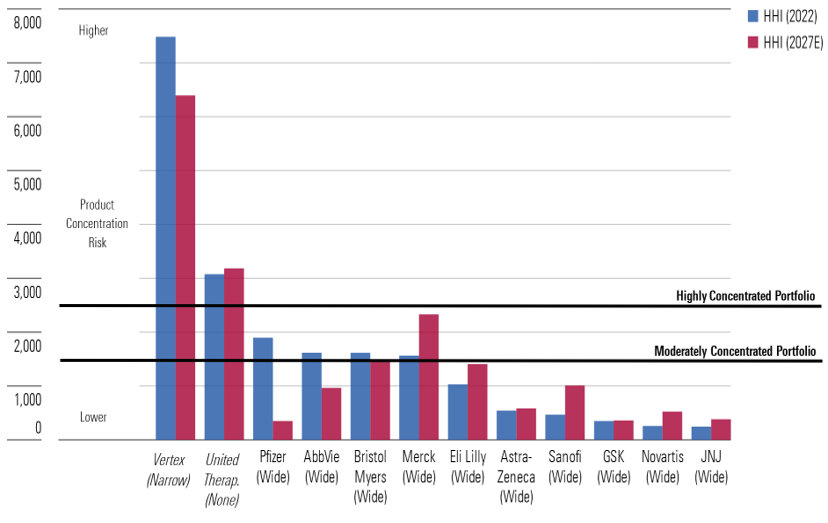

Big Pharma looks well-positioned to maintain wide moats, based on strong innovation trends that should mitigate the industry’s next significant patent cliff, which starts around 2028 with the loss of several current mega-blockbusters. These firms continue to generate strong returns on invested capital and invest in new drugs through R&D. Big Pharma companies have lower product concentration risk than more focused firms like Vertex VERX and United Therapeutics UTHR.

Big Pharma Firms Tend to Have Diversified Portfolios

Top Healthcare Sector Picks

Illumina

- Fair Value Estimate: $228.00

- Morningstar Rating: 5 stars

- Morningstar Economic Moat Rating: Narrow

- Morningstar Uncertainty Rating: High

Illumina ILMN may face more competition in its legacy genomic sequencing technology than it has in the past, but we think the factors that determine its economic moat in genomic sequencing-—intangible assets and switching costs for end users—remain intact and should help the firm generate economic profits for the long run, especially considering its new sequencing instruments. Illumina also owns the Grail liquid biopsy assets, which are targeting a nascent exponential technology opportunity for the earlier detection of cancer. The firm plans to divest Grail by late 2024, and if it does so, earnings should rise immediately. A tax-free spinoff to existing shareholders could be a good way to satisfy regulators while also giving them long-term optionality in the Grail technology.

Moderna

- Fair Value Estimate: $227.00

- Morningstar Rating: 5 stars

- Morningstar Economic Moat Rating: None

- Morningstar Uncertainty Rating: Very High

While we have modest expectations for sales of Moderna’s MRNA covid-19 vaccine after massive pandemic-fueled demand in 2021 and 2022, we think the firm’s pipeline of mRNA-based vaccines and treatments is advancing rapidly across multiple therapeutic areas. At the end of 2023, Moderna had 37 development candidates in clinical trials. Even as sales dip in 2023-24 ahead of new launches from the pipeline, we’re increasingly confident in the long-term sales trajectory of the diversified pipeline. We think Moderna’s technology looks well validated in respiratory virus vaccines (RSV vaccine to launch in 2024, covid/flu combo to launch in 2025), oncology (melanoma launch possible by 2025), and rare diseases (accelerated approvals also possible).

Zimmer Biomet Holdings

- Fair Value Estimate: $175.00

- Morningstar Rating: 4 stars

- Morningstar Economic Moat Rating: Wide

- Morningstar Uncertainty Rating: Medium

With the addition of smaller competitor Biomet, Zimmer ZBH is the undisputed king of large joint reconstruction. We expect favorable demographics, which include aging baby boomers and rising obesity, to fuel solid demand for large joint replacements that should offset price declines. Zimmer stumbled into a series of pitfalls in 2016-17, including integration issues, supply challenges, and quality concerns. But new management has tackled these issues, and the firm is poised to ramp up growth.

MORN DODFX VINIX VWILX TSVA EGO WU Brightstart429plan MRO VZ MOAT T NKE CMCSA GOOG

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/347BSP2KJNBCLKVD7DGXSFLDLU.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/TP6GAISC4JE65KVOI3YEE34HGU.jpg)

/d10o6nnig0wrdw.cloudfront.net/04-29-2024/t_d0e8253d77de4af9ae68caf7e502e1bf_name_file_960x540_1600_v4_.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/a90c659a-a3c5-4ebe-9278-1eabaddc376f.jpg)