Going Into Earnings, Is Eli Lilly Stock a Buy, a Sell, or Fairly Valued?

Watching the outlook for the company’s key drugs, here’s what we think of Lilly’s stock.

/s3.amazonaws.com/arc-authors/morningstar/a90c659a-a3c5-4ebe-9278-1eabaddc376f.jpg)

Eli Lilly LLY is set to release its fourth-quarter earnings report on Feb. 6, before the start of trading. Here’s Morningstar’s take on what to look for in Eli Lilly’s earnings and our outlook for its stock.

Key Morningstar Metrics for Eli Lilly Stock

- Fair Value Estimate: $450.00

- Morningstar Rating: 2 stars

- Morningstar Economic Moat Rating: Wide

- Morningstar Uncertainty Rating: High

What to Watch for In Eli Lilly’s Q4 Earnings

Key drug sale forecasts: How strong is the growth trajectory of Mounjaro (diabetes) and Zepbound (weight loss), and how are their manufacturing capacity and insurance coverage coming along? Has Trulicity lost market share to Mounjaro?

Earnings outlook: What is the company’s 2024 guidance, and will it be strong enough to support its high valuation?

Other product updates: Are there any updates to the approval timelines for donanemab (Alzheimer’s) and lebrikizumab (atopic dermatitis), which are both expected in the first half of 2024? How is Verzenio doing in breast cancer versus Pfizer’s PFE Ibrance, given the stronger label of Verzenio?

Eli Lilly Stock Price

Fair Value Estimate for Eli Lilly Stock

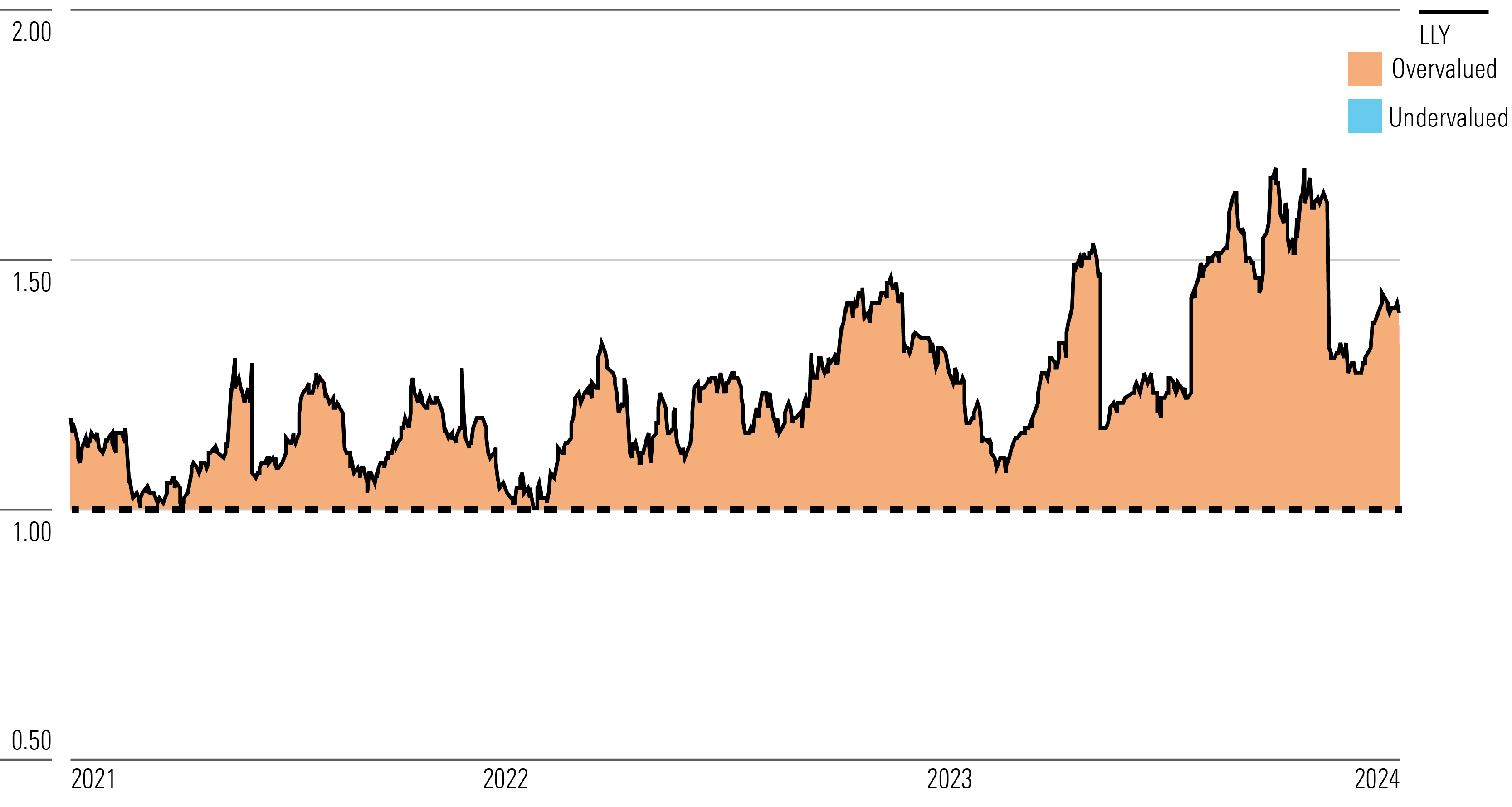

With its 2-star rating, we believe Eli Lilly’s stock is overvalued compared with our long-term fair value estimate.

We previously raised our fair value estimate to $450 from $368 after updating our long-term GLP-1 model to include the wider use of and greater adherence to these cardiometabolic drugs. Overall, we assume a greater proportion of patients will receive (and stay compliant with) treatment, albeit with more competition and at a lower price. We now think more than 25% of obese Americans and 15% of overweight Americans will receive treatment in 10 years, with the vast majority receiving branded GLP-1 therapies. We think U.S. prices could fall substantially as volumes increase (in line with payer contracts) and new entrants launch (beginning in 2026-27), with average net prices falling from roughly $8,000 annually to $3,000 in 10 years.

The company looks well-positioned to drive top-line growth. We project annual sales increases of close to 22% during the next five years as a result of new drug launches offsetting patent losses. We expect Mounjaro, Zepbound, Jardiance, Trulicity, Verzenio, and Taltz to remain important drivers of cash flow. Donanemab should also ramp to meaningful sales following its expected approval this year.

Another important point driving our valuation is cost controls and operating leverage from new drugs. While the outcome of operating cost controls will depend on new revenue associated with the success of recently launched drugs and the pipeline, we expect Lilly will significantly improve operating margins. We estimate a weighted cost of capital at 7%, in line with the peer group.

Eli Lilly Historical Price/Fair Value Ratio

Read more about Eli Lilly’s fair value estimate.

Economic Moat Rating

Patents, economies of scale, and a powerful distribution network support Lilly’s wide moat. The firm’s patent-protected drugs carry strong pricing power, which lets it generate returns over its cost of capital. The patents also give the company time to develop the next generation of drugs before generic competition arises. Lilly’s diversified product portfolio means the company’s top drugs represent only a moderate amount of total sales, with the largest drug, Trulicity, representing almost 25%, which sets up manageable cash flow declines as new products mitigate the generic competition. However, we do expect increasing dependence on Lilly’s new GLP-1 drugs will mean close to two-thirds of sales will be from this class by 2032.

Lilly’s operating structure allows for cost-cutting after patent losses to reduce the margin pressure from lost high-margin drug sales. Overall, the company’s established product line creates the enormous cash flows needed to fund the average $800 million in development costs required by a new drug. In addition, Lilly’s powerful distribution network sets it up as a strong partner for smaller drug companies that lack its resources. Its recently launched biologic drugs also create higher hurdles over traditional small molecule drugs for biosimilars to gain market share following their eventual patent expirations.

Read more about Eli Lilly’s moat rating.

Risk and Uncertainty

We are maintaining our High Uncertainty Rating for Lilly, based on the highly variable outcomes for several key drug launches. Diabetes and weight loss drugs Mounjaro and Zepbound are likely to be major. However, their cone of uncertainty is higher, as several variables affect their sales potential, especially for the weight loss indication. Donanemab could potentially also become a big player, but there’s less visibility on market uptake. With donanemab and Mounjaro/Zepbound representing close to two-thirds of Lilly’s projected sales by the end of the next 10 years, we believe a High rating is appropriate. Most big biopharma firms tend to have Medium Uncertainty Ratings. Beyond product-specific uncertainties, Lilly faces tough competition from generics manufacturers and brand-name drugmakers. The company encounters considerable regulatory and legal risks, including product approvals, patent challenges, and liability lawsuits.

Our rating is not materially affected by ESG risks, although we see access to basic services (tied to drug pricing) as the biggest ESG risk that the firm needs to manage. Lilly generates close to 60% of total sales from U.S. prescription drug sales (slightly higher relative to peers) so additional major pricing reforms could weigh on sales and margins. Additionally, we assume a more than 50% probability of Lilly seeing future costs related to product governance ESG risks (such as off-label marketing or litigation related to side effects), and model base case annual legal costs at 3% of non-GAAP net income (on the high end relative to peers based on Lilly’s product portfolio being more prone to possible litigation).

Read more about Eli Lilly’s risk and uncertainty.

LLY Bulls Say

- Lilly is developing a new Alzheimer’s drug (donanemab) that could become a major blockbuster, especially because the FDA appears to have a lower threshold for approval for this disease.

- Lilly’s cancer drug Verzenio reported strong data in early-stage breast cancer, opening up the potential for it to be the first CDK4/6 drug to launch in this multi-billion-dollar market.

- Lilly is creating the next generation of diabetes and weight loss drugs, which hold major market potential, given the high prevalence of these diseases.

LLY Bears Say

- The risks to success for Alzheimer’s drug donanemab remain high, both in clinical development and insurance coverage.

- Several of Lilly’s next-generation diabetes drugs could lead to the cannibalization of its current approved drugs.

- Increasing competition for weight loss drug Zepbound could significantly increase over the next three years.

This article was compiled Freeman Brou.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

MORN DODFX VINIX VWILX TSVA EGO WU Brightstart429plan MRO VZ MOAT T NKE CMCSA GOOG

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/RNODFET5RVBMBKRZTQFUBVXUEU.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LJHOT24AYJCHBNGUQ67KUYGHEE.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/V33GR4AWKNF5XACS3HZ356QWCM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/a90c659a-a3c5-4ebe-9278-1eabaddc376f.jpg)