5 Cheap Stocks With Growing Dividends

We turn to the Morningstar US Dividend Growth Index for stock ideas.

/s3.amazonaws.com/arc-authors/morningstar/35408bfa-dc38-4ae5-81e8-b11e52d70005.jpg)

Here in Chicago, you're either a Cubs fan or a White Sox fan. (Given that my husband and I met at what was then called Comiskey Park, you can guess where my allegiance lies.) In much the same way, investors who favor dividend-paying stocks generally fall into one of two camps.

Those investing for current income usually prefer the dividend stocks with the highest yields, which means leaning toward utilities, REITs, and consumer defensive names. Often the highest-yielding are highly leveraged, lower-quality companies.

Other dividend investors are less focused on absolute yield and instead favor stocks with a history of increasing their dividends. These dividend growers are able to raise their payouts over time because their cash flows are solid--they're generally higher-quality companies.

Today, we're providing some investment ideas for that latter group of dividend investors, plucking insights from the Morningstar US Dividend Growth Index. The index focuses on stocks that have grown--and are poised to continue to grow--their dividends. To be included in the index, stocks must meet the following criteria:

- The stock's dividend must be qualified income. As such, REITs are excluded from the index.

- The stock's indicated dividend yield must not be in the top 10% of the investable universe. This criterion helps weed out firms that are more likely to experience dividend cuts and financial distress.

- The stock must have a positive consensus earnings forecast and a dividend payout ratio less than 75%. These metrics help measure the sustainability of the dividend growth.

- The stock must have at least five years of uninterrupted annual dividend growth.

We reconstitute the index annually.

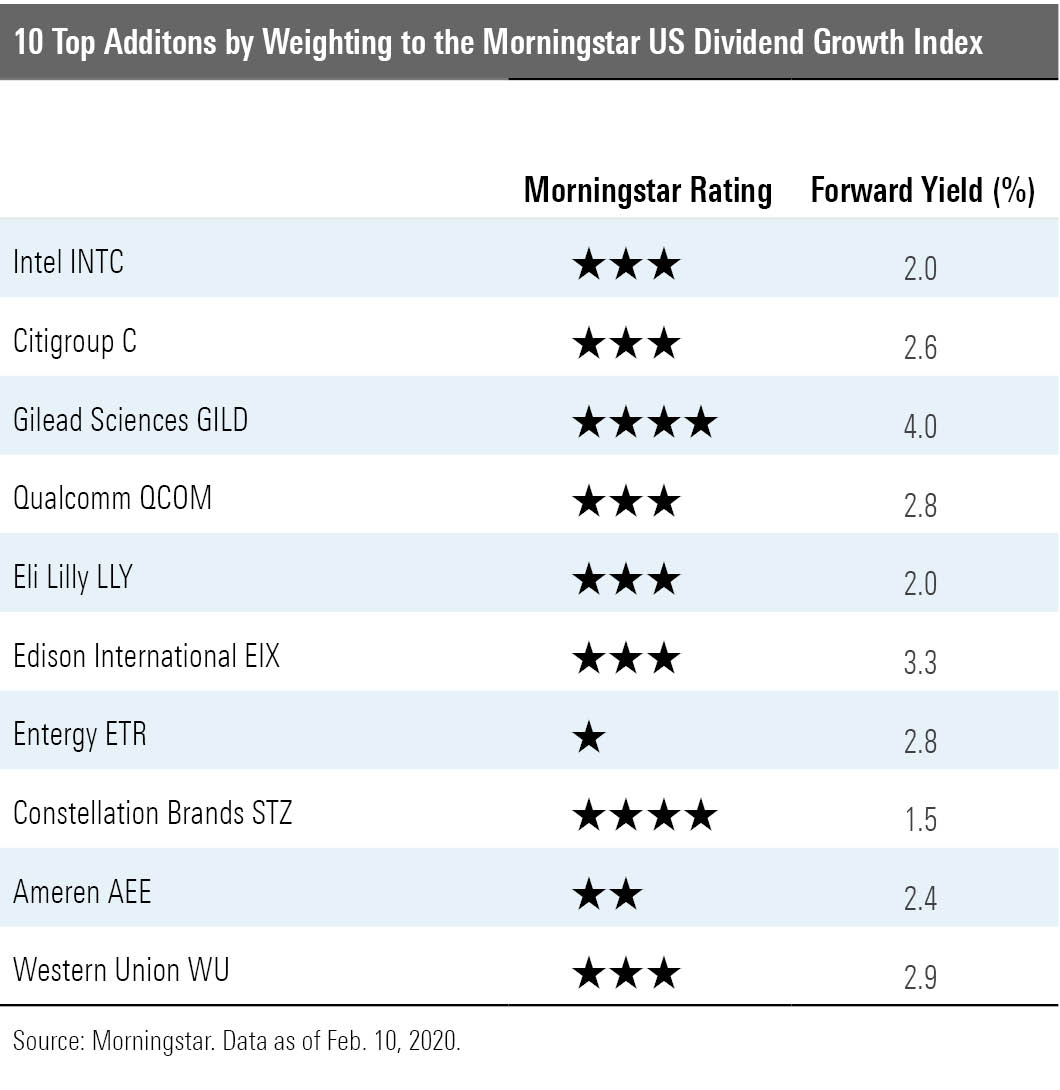

Here are the top additions from the December 2019 reconstitution, ranked by their weighting in the index. Note that we're only including stocks that our analysts actively cover.

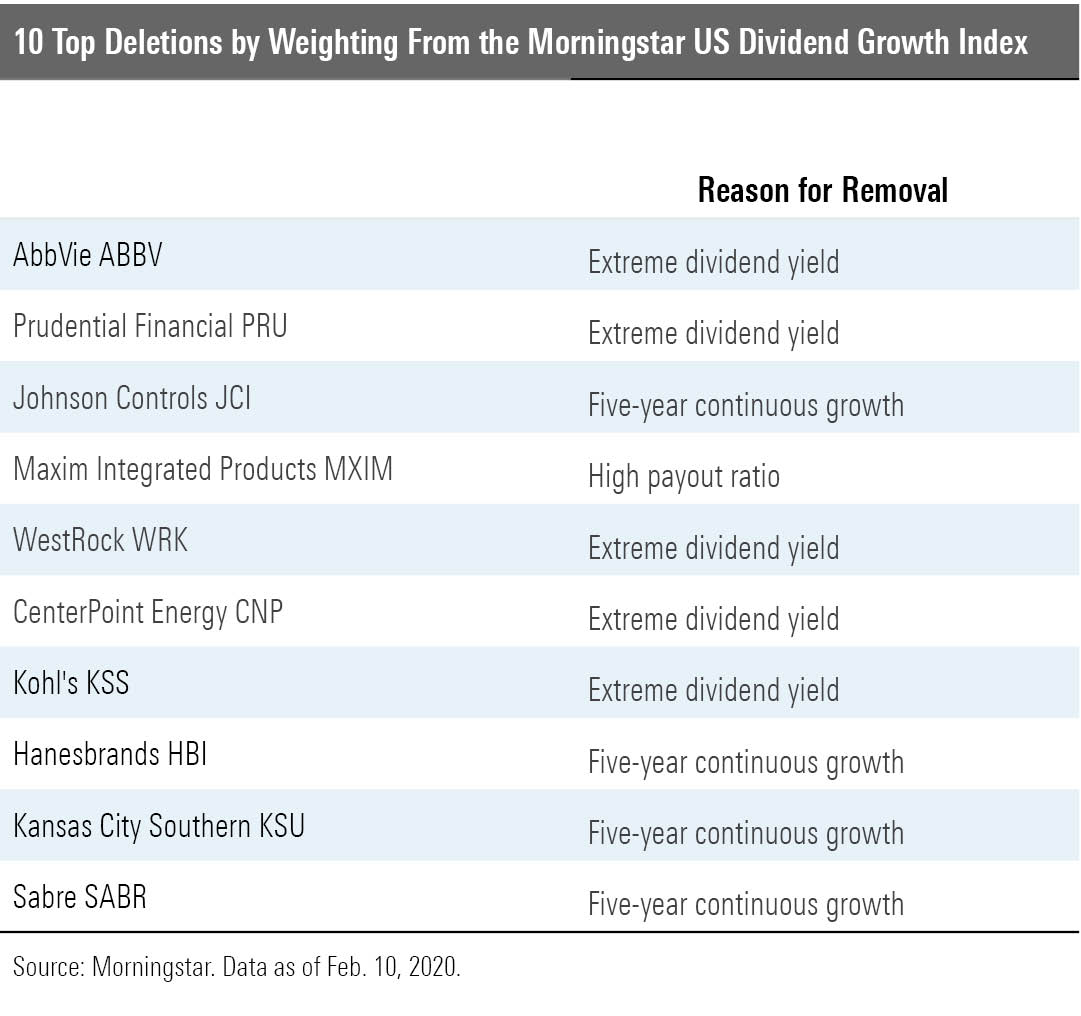

These are the stocks in the index that were the most heavily weighted and under analyst coverage that were cut in December.

Four of the names--Johnson Controls JCI, Hanesbrands HBI, Kansas City Southern KSU, and Sabre SABR--were let go because they broke their five-year continuous dividend-growth streaks. The indicated dividend yields on five stocks—AbbVie ABBV, Prudential Financial PRU, WestRock WRK, CenterPoint Energy CNP, and Kohl's KSS--landed in the top 10% of the index's investable universe at the time of reconstitution. And Maxim Integrated Products' MXIM payout ratio breached 75%.

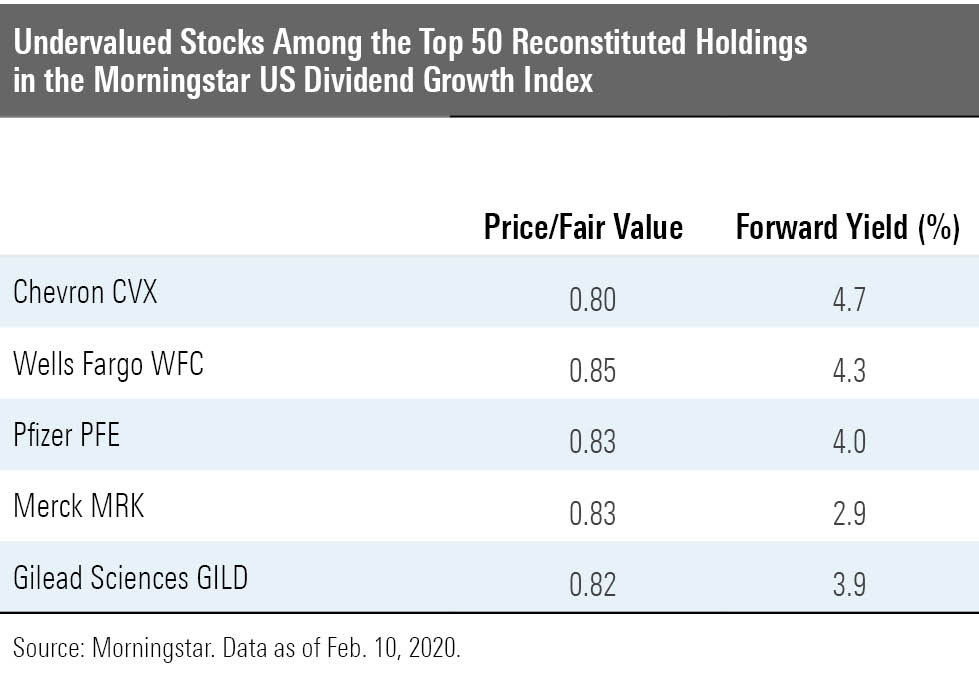

Only five of the 50 most heavily weighted names in the index are undervalued as of this writing.

Here's a little bit about the business strategy and outlook of each from our analysts.

Chevron CVX "Historically, Chevron has benefited from an oil-leveraged portfolio that has led to peer-leading margins and returns on capital. We expect it to maintain its edge as it moves into the next phase of growth, which is centered on leveraging its large Permian Basin position.

"Chevron is delivering robust growth because of new production from the Permian Basin, Gulf of Mexico, and Western Australia. In 2018, it realized peer-leading volume growth of 7% and expects similar results in 2019, with growth of 4% to 7% owing to continued shale growth and liquefied natural gas project ramp-up.

"Its two LNG projects in Australia, Gorgon and Wheatstone, have been the primary drivers of growth, collectively adding 400,000 barrels of oil equivalent a day, once at peak production in 2019. The investment in LNG production allows Chevron to preserve its peer-leading liquids exposure as prices are largely indexed to oil. Also, projects like LNG, with long-plateau production levels that require little additional capital expenditure, help reduce decline rates while generating significant free cash flow to support reinvestment elsewhere or shareholder returns. However, these projects will also weigh on returns as they were sanctioned at the top of the cycle and experienced budget overruns (Gorgon).

"Positively, however, we expect cash flow to rise during the next five years because of cost-cutting and the addition of higher-margin volumes, which should result in greater free cash flow despite a modest increase in capital spending during the past few years. Spending will also be directed toward shorter-cycle, less capital-intensive projects such as unconventional production in the Permian Basin and brownfield expansion of existing projects that provide flexibility and deliver high returns.

"Chevron's next phase of growth will be driven by its differentiated Permian position (size, quality, and lack of royalty). Progress in improving cost and performance has prompted the company to increase investment in the basin."

--Allen Good, sector strategist

Wells Fargo WFC "Wells Fargo remains one of the top deposit gatherers in the United States, even after years of negative headlines related to the bank's scandals. Its strategy historically rested on deep customer relationships, sound risk management, and operational excellence. While the operational excellence has been questionable of late, the bank has easily outearned its cost of equity for decades and continues to do so today. Wells Fargo arguably has the best branch network in the U.S., excels in the middle-market commercial space, has a strong advisory network, and as a result has generally generated more revenue per dollar of assets than most peers over time. We still believe the bank has an attractive lineup of business units and a core group of loyal, longtime customers. Indeed, account closures were well controlled even during the worst of its sales problems, demonstrating that customers are willing to stick with the bank. This is not to say that Wells does not still face many issues, including getting the asset cap removed, regaining a more positive reputation among potential advisor clients, turning around its asset-management unit, and generally returning to offense instead of constantly being on defense. That said, we do not see a fundamental reason why the bank can't consistently earn returns on tangible equity of 14% longer term, which would warrant a better valuation.

"Unlike its major competitors, Wells is not a top player in the capital markets. Its business model is more akin to a regional bank than a money-center institution. Wells is also almost entirely U.S.-focused. These factors can make the business simpler and results less volatile. For these reasons, we believe Wells deserves a lower cost of capital than its money-center peers.

"While we think the hiring of Charles Scharf as CEO is a big step in the right direction, we also believe it will be some time before Wells Fargo has fully dealt with all of its issues and has turned around each business segment. In the meantime, the bank is likely to struggle for growth as it rebuilds."

--Eric Compton, analyst

Stock Analyst Update: Wells Fargo Reports a Tough Fourth Quarter

Pfizer PFE "Pfizer's foundation remains solid, based on strong cash flows generated from a basket of diverse drugs. The company's large size confers significant competitive advantages in developing new drugs. This unmatched heft, combined with a broad portfolio of patent-protected drugs, has helped Pfizer build a wide economic moat around its business.

"Pfizer's size establishes one of the largest economies of scale in the pharmaceutical industry. In a business where drug development needs a lot of shots on goal to be successful, Pfizer has the financial resources and the established research power to support the development of more new drugs. Also, after many years of struggling to bring out important new drugs, Pfizer is now launching several potential blockbusters in cancer, heart disease, and immunology.

"Pfizer's vast financial resources support a leading salesforce. Pfizer's commitment to postapproval studies provides its salespeople with an armamentarium of data for their marketing campaigns. Further, Pfizer's leading salesforces in emerging countries position the company to benefit from the dramatically increasing wealth in nations such as Brazil, Russia, India, China, and Turkey.

"While entrenched as an industry leader, Pfizer faces challenges in the near term. The loss of patent protection on several drugs will weigh on future growth. In particular, the recent 2019 U.S. patent loss on neuroscience drug Lyrica is weighing on near-term growth. However, Pfizer's recent decision to divest its off-patent division to create a new company in combination with Mylan MYL should drive accelerating growth at the remaining innovative business at Pfizer.

"Further, we believe Pfizer's operations can withstand the additional generic competition, and the 2009 acquisition of Wyeth helps insulate Pfizer from any one particular patent loss. Following the merger, Pfizer has a much stronger position in the vaccine industry with pneumococcal vaccine Prevnar 13. Vaccines tend to be more resistant to generic competition because of the manufacturing complexity and relatively lower prices."

--Damien Conover, sector director

Stock Analyst Update: Pfizer Posts Slightly Weak Quarter, but Guidance Solid

Merck MRK "Merck's combination of a wide lineup of high-margin drugs and a pipeline of new drugs should ensure strong returns on invested capital over the long term. Further, Merck is through the worst of its patent cliff, which should remove the heightened generic competition the company has experienced over the past years. And after several years of only moderate research-and-development productivity, Merck's drug development strategy is yielding important new drugs.

"Merck's new products have mitigated the generic competition, offsetting the recent major patent losses. In particular, Keytruda for cancer represents a key blockbuster with multi-billion-dollar potential: It holds a first-mover advantage in one of the largest cancer indications of non-small cell lung cancer. Also, we expect new cancer drug combinations will further propel Merck's overall drug sales. However, we expect intense competition in the cancer market with several competitive drugs likely to report important clinical data between 2019 and 2020. Other headwinds include generic competition, notably to cardiovascular drugs Zetia and Vytorin, which is likely to create a drag on overall growth.

"After several years of mixed results, Merck's R&D productivity is improving as the company shifts more toward areas of unmet medical need. Owing to side effects or lack of compelling efficacy, Merck experienced major setbacks with cardiovascular disease drugs anacetrapib, Tredaptive, Rolofylline, and TRA, along with Telcagepant for migraines. Safety questions ended the development of osteoporosis drug odanacatib. Despite these setbacks, Merck has some solid successes, including a successful launch for its PD-1 drug Keytruda in oncology. Following on this success, Merck is shifting its focus toward areas of unmet medical need in specialty-care areas, and Keytruda is leading this new direction. We expect that Keytruda's leadership in non-small cell lung cancer will be a key driver of growth for the company over the next several years."

--Damien Conover, sector director

Stock Analyst Update: Disappointing Quarter for Undervalued Merck

Gilead Sciences GILD "Gilead Sciences generates stellar profit margins with its HIV and HCV portfolio, which requires only a small salesforce and inexpensive manufacturing. We think its portfolio and pipeline support a wide moat, but Gilead needs HCV market stabilization, strong continued innovation in HIV, solid pipeline data, and smart future acquisitions to return to growth.

"Gilead's tenofovir (TDF) molecule--in Viread, Truvada, and older single-tablet regimens--historically formed the heart of the firm's $17 billion HIV franchise. Combo pills offer convenience and affordability, as patients are less likely to miss doses and develop drug resistance, and they only need to make one copayment. The newest combo pills--replacing TDF with TAF--reduce bone and kidney safety issues and are seeing rapid uptake. Gilead's biggest competitive threat in HIV is GlaxoSmithKline GSK; Triumeq saw rapid growth in 2015, and Glaxo has launched two-drug regimens based on its integrase inhibitor Tivicay (Juluca in 2017 and Dovato in 2019) that also bypass Gilead's drugs. However, Gilead's Genvoya (2015), Odefsey (2016), Descovy (2016), and Biktarvy (2018) launches push patent protection into the late 2020s and are boosting the company's market share.

"The $11 billion Pharmasset deal brought key HCV drug Sovaldi. Sovaldi and Harvoni (a combination of Sovaldi and ledipasvir) peaked at more than $19 billion in sales in 2015. However, demand has been shrinking as patients are cured, and competition from AbbVie and Merck has led to several rounds of significant price discounting. We expect Gilead and AbbVie to share a $5 billion-plus market in the long term.

"Gilead is building a pipeline outside of HIV and HCV but will need more acquisitions like Kite (with CAR-T therapy Yescarta) to see strong growth. Gilead's first cancer drug, Zydelig, launched in 2014, is limited by safety concerns, but we're more optimistic about the firm's immunology portfolio, including JAK1-inhibitor filgotinib from the Galapagos collaboration. Lead NASH program selonsertib recently failed in a phase 3 trial, but Gilead is exploring combination therapy with other mechanisms in NASH."

--Karen Andersen, sector strategist

Stock Analyst Update: No Changes to Healthcare Stocks Amid Coronavirus

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click here for a list of investable products that track or have tracked a Morningstar index. Neither Morningstar, Inc. nor its investment management division markets, sells, or makes any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ECVXZPYGAJEWHOXQMUK6RKDJOM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/KOTZFI3SBBGOVJJVPI7NWAPW4E.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/V33GR4AWKNF5XACS3HZ356QWCM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/35408bfa-dc38-4ae5-81e8-b11e52d70005.jpg)