3 Undervalued Western Utilities

Record-breaking fires are causing the market to overestimate the companies' financial risks.

/s3.amazonaws.com/arc-authors/morningstar/ea0fcfae-4dcd-4aff-b606-7b0799c93519.jpg)

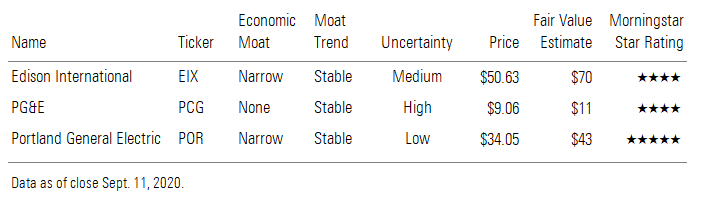

We are reaffirming our fair value estimates for Portland General Electric POR, Edison International EIX, and PG&E PCG as the utilities manage record-setting wildfires in the West. All three continue to trade well below what we think they’re worth and among the lowest valuation multiples in the sector.

Portland General’s stock fell as much as 16% on Sept. 10 after reports that downed power lines might have sparked fires near Portland. Presumably, investors fear that Portland General could face fire-related liabilities such as those that sent California utility PG&E into bankruptcy last year.

We urge investors to keep in mind that these reports--and any semblance to PG&E’s experience--are grossly speculative. The probability, timing, and scope of financial liabilities are too uncertain for us to include in our forecasts. Most important, we don’t believe Portland General would face inverse condemnation-related liabilities as PG&E faced in California. Legal and regulatory precedent appears to absolve Oregon utilities from unintentional property losses.

The fires follow Portland General’s self-inflicted challenges earlier this year, obscuring its attractive long-term outlook. The management team was among the few in the sector to cut earnings guidance this spring; the board unexpectedly postponed its dividend increase; and the company recently disclosed $128 million of energy trading losses, resulting in a cut in our fair value estimate. Potential fire liabilities aside, we think investors are right to heighten their skepticism.

At a minimum, the fires and pre-emptive blackouts are likely to hurt relationships with regulators, customers, and politicians. Alternatively, additional wildfire safety investments could support earnings growth. We already assume Portland General will invest 30% more than its current base plan in 2022 and beyond, supporting 6% annual earnings and dividend growth.

In past years, large wildfires created substantial investment risk for California utilities. But we think legislative and regulatory changes during PG&E’s bankruptcy last year have made fire risk similar to natural disaster risks that all utilities face.

PG&E’s service territory continues to be the most fire-prone, but we think the market is overestimating the utility’s fire-related financial risk. Although fires are likely to lead to higher operating and capital costs, we expect PG&E will be able to recover these through existing rate-making structures.

If PG&E were found responsible for fires, new legislation substantially reduces its financial exposure. In a worst-case scenario, we estimate PG&E would face a maximum $2.4 billion of shareholder losses, or about 10% of its current market value after tax. We believe this is already priced into the stock based on its valuation relative to peers.

We think Edison has a more attractive investment profile with lower fire risk and a cheaper valuation. It trades nearly 30% below our fair value estimate with a 5% dividend yield and 12 price/earnings multiple. We expect the board will raise the dividend next quarter as it has following the last three fire seasons.

This year’s wildfires demonstrate the urgency of both California utilities’ wildfire safety investments. Wildfire safety investments are a large part of PG&E’s $40 billion capital investment plan in 2020-24, supporting our 10% annual earnings growth forecast. Edison’s $3.9 billion of wildfire safety investments are part of its $21 billion capital investment plan in 2020-23, supporting our 8% annual earnings growth forecast.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/RNODFET5RVBMBKRZTQFUBVXUEU.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LJHOT24AYJCHBNGUQ67KUYGHEE.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/V33GR4AWKNF5XACS3HZ356QWCM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ea0fcfae-4dcd-4aff-b606-7b0799c93519.jpg)