25 Overstuffed Stocks

The most expensive U.S. stocks we cover aren't necessarily bad investments, but they feel a little rich today.

/s3.amazonaws.com/arc-authors/morningstar/3a6abec7-a233-42a7-bcb0-b2efd54d751d.jpg)

In this column we usually highlight our equity research analysts' best investment ideas that are trading at compelling valuations.

Great bargains aren't always easy to sniff out, particularly following a trailing five-year period during which the Morningstar US Stock Market Index nearly gained nearly 16% per year. In fact, a large portion of our equity coverage is at least fairly valued or overvalued; according to Morningstar's Market Fair Value tool, the median stock in our coverage is trading at a price/fair value ratio of 1.03.

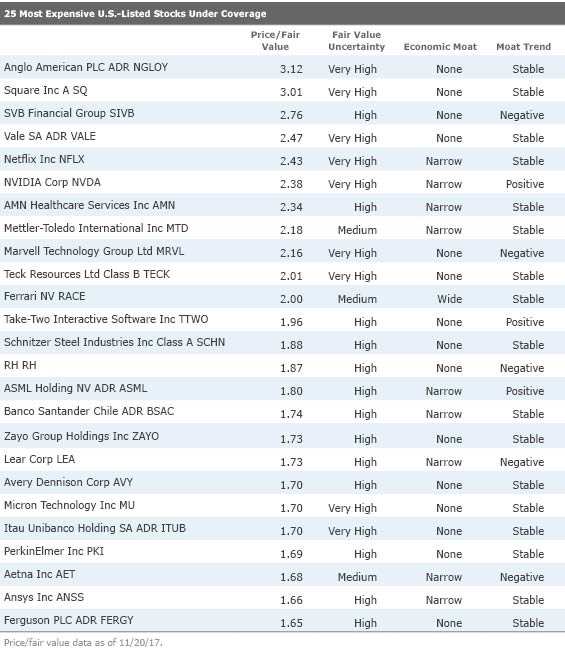

This week I thought we would switch things up and see what a list of the most expensive stocks we cover looks like. I sorted our entire U.S. coverage list by price/fair value to find the 25 most overvalued firms (excluding stocks with extreme fair value uncertainty ratings).

I was tempted to label the stocks on the resulting "most expensive" list as "turkeys" in celebration of the upcoming holiday. But this isn't a list of terrible investments; in fact, it contains many stocks that we'd love to own at the right price. I'll settle for "overstuffed" instead.

Below, we list the 25 most expensive stocks on our U.S. coverage list, and we take a closer look at three overvalued companies we'd look at more closely if the prices were right.

From its origins as a DVD rental by mail service, Netflix has morphed into a pioneer in streaming video on demand and the largest online video provider in the U.S. Equity analyst Neil Macker's narrow moat rating is based on intangibles and a network effect resulting from the use of Big Data stemming from the firm's massive subscriber base in the U.S.

Already the largest provider in the U.S., Netflix is expanding rapidly into markets abroad, Macker says. The firm has used its scale to construct a massive data set that tracks every customer interaction. It then leverages this customer data to better purchase content and produce original material. Macker believes that this data and ability to leverage will help Netflix remain the largest provider in the U.S. and enjoy success in many of its newer markets.

But despite its impressive subscriber growth in recent quarters, however, Macker is concerned that the firm continues to burn cash at a faster pace than it did in the same period last year. The move to more original content adds costs and risks, particularly with competition from the likes of Hulu and Amazon. We would recommend waiting for a wider margin of safety to our $80 fair value estimate before tuning in.

Ferrari's heritage originates from the engineering, manufacturing, and competition racing since Enzo Ferrari founded Scuderia Ferrari in 1929 under Alfa Romeo ownership, writes senior equity analyst Richard Hilgert. This aspirational luxury brand commands substantial pricing power, which bolsters the company's ability to generate stable streams of revenue and economic returns through the business cycle.

Hilgert thinks Ferrari stock will regularly trade at rich, luxury goods valuation multiples. He believes the long-term stability of Ferrari's revenue, addressable market growth, expansive profit margin, and solid returns on invested capital throughout economic cycles to be compelling reasons to invest in this wide-moat business at the right price.

Right now, though, the stock is too rich for our blood, trading at a 100% premium to our fair value estimate of EUR 50 or $55 (using a spot exchange rate of 1 EUR/$1.09).

As a result of greater regulation, volatile political risk, and a narrowing of profitable growth markets, the aggregate investment outlook for managed-care organizations is uncertain. However, even with a more difficult operating environment, senior equity analyst Vishnu Lekraj thinks Aetna possesses competitive advantages that should allow it to produce outsize economic profits over an extended period.

The managed-care organization industry will encompass a significantly greater degree of transparency, competition, and costs, through the implementation of exchanges and standard insurance policy formats, Lekraj explains. With capped gross profitability through mandated medical loss ratios only players with large enough membership bases will be able to earn economic profits. Aetna's solid 23 million total medical members give it the ability to scale its fixed costs, maintain underwriting expertise, gain greater pricing leverage, and solidify a robust provider network.

Lekraj also believes Aetna also has an opportunity to expand its membership base and build its operational advantages through the acquisition of midtier health insurers--a strategy will be even more critical given the uncertainty of current healthcare legislation and its failed acquisition of Humana, Lekraj said.

With the shares trading at a 68% premium to our $104 fair value estimate, however, we'd wait for a better entry point.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/RNODFET5RVBMBKRZTQFUBVXUEU.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LJHOT24AYJCHBNGUQ67KUYGHEE.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/V33GR4AWKNF5XACS3HZ356QWCM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/3a6abec7-a233-42a7-bcb0-b2efd54d751d.jpg)